Global Lithium Iron Phosphate Lfp Batteries Market

Market Size in USD Billion

USD

24.47 Billion

USD

52.83 Billion

2025

2033

USD

24.47 Billion

USD

52.83 Billion

2025

2033

| 2026 - 2033 | |

| USD 24.47 Billion | |

| USD 52.83 Billion | |

| % | |

|

Lithium Iron Phosphate (LFP) Batteries Market Overview

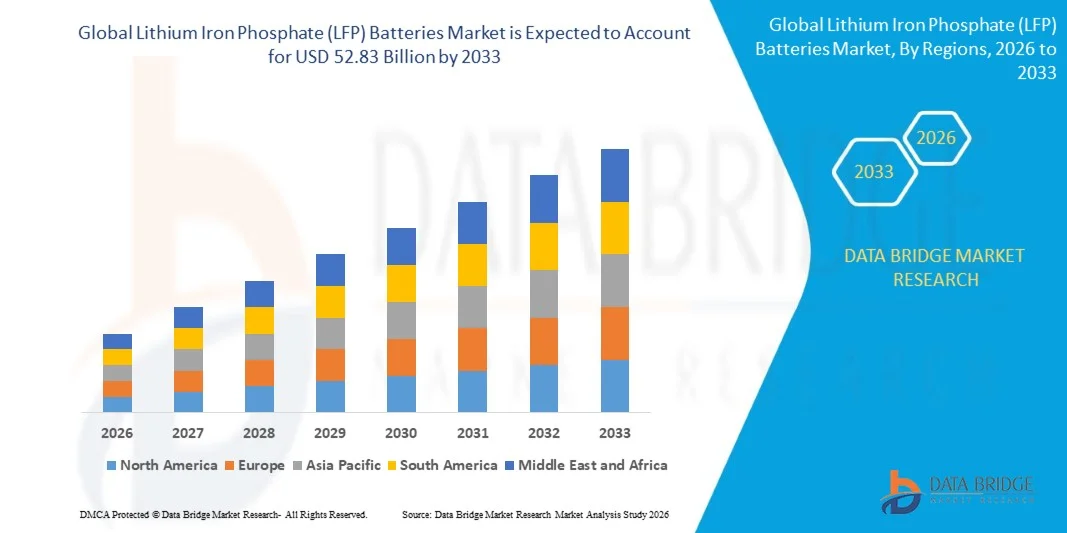

The Lithium Iron Phosphate (LFP) Batteries Market was valued at USD 24.47 billion in 2025 and is projected to reach USD 52.83 billion by 2033, growing at a CAGR of 10.10% from 2026 to 2033. The market is witnessing strong expansion driven by rising adoption of electric vehicles, increasing deployment of renewable energy storage systems, and growing demand for safer, longer-life, and cost-efficient battery chemistries compared to conventional lithium-ion technologies.

The growing emphasis on energy transition and decarbonization across transportation and power sectors is accelerating the shift toward LFP batteries due to their thermal stability, enhanced safety profile, and longer cycle life. In addition, advancements in battery manufacturing, increasing localization of supply chains, and supportive government policies promoting EV adoption and grid-scale energy storage are further strengthening market growth across global regions.

Key Market Trends & Insights

- North America held a significant revenue share of approximately 32.6% in 2025 in the lithium iron phosphate (LFP) batteries market, supported by rapid expansion of electric vehicle adoption, strong investments in grid-scale energy storage, and increasing focus on renewable energy integration.

- Asia-Pacific is expected to be the fastest-growing region, recording a strong CAGR from 2026 to 2033, driven by large-scale battery manufacturing capacity, supportive government policies, rapid electric vehicle penetration, and the presence of key market players such as China-based battery manufacturers.

- The Stationary segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong deployment in grid-scale energy storage systems, renewable integration projects, and backup power infrastructure for data centers and telecom towers. LFP batteries are widely preferred in stationary applications due to their long cycle life, high thermal stability, and lower total cost of ownership across continuous charge-discharge operations.

- The Portable segment is projected to register steady growth at a CAGR of 9.6% from 2026 to 2033, driven by rising adoption in electric vehicles, consumer electronics, and portable power systems. Increasing demand for lightweight, safe, and long-lasting battery solutions in EVs such as entry-level passenger vehicles and electric two-wheelers is accelerating segment expansion across Asia-Pacific and Europe.

- The 100,001–540,000 Mah segment held the largest market revenue share of approximately 46.7% in 2025 driven by extensive usage in electric vehicles, utility-scale energy storage systems, and commercial backup power applications. Large-capacity LFP battery packs are increasingly deployed in EV platforms and grid storage projects due to their high durability and superior thermal safety performance under heavy load conditions.

- The 50,001–100,000 Mah segment is projected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by rising demand in mid-range electric vehicles, residential energy storage systems, and industrial UPS applications. Expanding adoption of distributed energy storage solutions for solar integration is further supporting segment growth across emerging markets.

- The Automotive segment held the largest market revenue share of approximately 49.2% in 2025 driven by rapid electrification of passenger vehicles, electric buses, and commercial fleets. Leading manufacturers such as BYD and Tesla are increasingly integrating LFP chemistry into mass-market EV models to reduce cost and enhance safety performance.

- The Power segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by large-scale deployment of renewable energy storage systems and grid stabilization projects. Increasing investments in solar and wind energy infrastructure across China, India, and the U.S. are accelerating adoption of LFP batteries for efficient energy balancing and peak load management across utility networks.

Market Size & Forecast

- Global Market Value (2025): USD 24.47 Billion

- Expected Market Value (2033): USD 52.83 Billion

- Forecast CAGR (2026–2033): 10.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Lithium Iron Phosphate (LFP) Batteries Market Segmentation

|

Attributes |

Lithium Iron Phosphate (LFP) Batteries Key Market Insights |

|

Segments Covered |

· By Application: Stationary and Portable · By Power Capacity: 0–16,250 Mah, 16,251–50,000 Mah, 50,001–100,000 Mah, and 100,001–540,000 Mah · By Industry: Automotive, Power, Industrial, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• BYD Company Ltd. (China) |

|

Market Opportunities |

· Electric Vehicle Expansion · Grid Scale Energy Storage Deployment |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Lithium Iron Phosphate (LFP) Batteries Market Trends

Trend: Growth In Electric Vehicle Adoption And Advanced Energy Storage Integration

Increasing demand for high-performance, safe, and long-cycle-life battery technologies across electric mobility, renewable energy storage, and industrial backup power systems. Conventional lithium-ion chemistries such as nickel manganese cobalt (NMC) batteries face cost volatility, thermal stability concerns, and resource dependency challenges, encouraging industries to shift toward lithium iron phosphate (LFP) chemistry with improved safety and lifecycle economics.

In modern electric vehicles, manufacturers such as Tesla and BYD are increasingly adopting LFP batteries in entry-level and mid-range models, such as Tesla Model 3 RWD and BYD Dolphin, to reduce costs while maintaining stable range performance and enhancing thermal safety under high-load conditions. In stationary energy storage systems, LFP-based battery packs are being deployed in large-scale grid projects to support renewable integration from solar and wind farms, improving load balancing and peak demand management efficiency.

The rapid expansion of utility-scale battery energy storage systems is also increasing demand for durable and thermally stable chemistries capable of withstanding frequent charge-discharge cycles in harsh operating environments. In addition, energy storage deployments such as China’s State Grid battery projects and large solar-plus-storage installations in the U.S. and India continue to rely heavily on LFP chemistry due to its long cycle life and lower risk of thermal runaway. Growing industry validation through EV fleet adoption in 2025 shows LFP-based batteries achieving cycle lives exceeding 3,000–5,000 cycles with lower degradation rates compared to conventional NMC systems under similar operating conditions.

Lithium Iron Phosphate (LFP) Batteries Market Dynamics

Key Market Driver: Rising Adoption Of Cost Efficient And Safer Battery Chemistries

Industries worldwide are facing increasing pressure to reduce battery costs, improve safety standards, and enhance lifecycle performance across electric vehicles, grid storage, and consumer energy systems. High reliance on expensive and geopolitically concentrated raw materials such as cobalt and nickel in conventional lithium-ion batteries is pushing manufacturers toward LFP chemistry, which eliminates cobalt and reduces overall material cost volatility.

Electric vehicle manufacturers are increasingly deploying LFP batteries in mass-market EVs to improve affordability and reduce fire risk, such as BYD integrating LFP Blade Battery technology across multiple vehicle platforms to enhance structural safety and energy density efficiency. In the energy storage sector, utility operators are deploying LFP-based systems for renewable integration and grid stabilization to manage fluctuating solar and wind output more efficiently.

Similarly, telecom towers and data center backup systems are transitioning from lead-acid and NMC-based storage to LFP batteries due to longer lifespan and lower maintenance requirements, improving total cost of ownership and operational reliability. Large-scale deployment projects in India’s renewable energy parks and China’s provincial grid storage systems in 2024–2025 indicate LFP-based installations achieving operational lifespans exceeding 10–15 years with stable degradation profiles under continuous cycling.

Key Restraint/Challenge: Lower Energy Density Compared To High Nickel Chemistries

Despite strong safety and cost advantages, LFP batteries generally exhibit lower gravimetric and volumetric energy density compared to nickel-rich chemistries such as NMC and NCA, limiting their use in long-range electric vehicles and high-performance applications. This constraint reduces driving range per unit battery pack size, creating challenges for premium EV segments where energy density is a critical performance factor.

In addition, space limitations in aerospace, aviation, and high-performance electronics restrict widespread adoption of LFP chemistry where compact high-energy output is required. Manufacturers often need to compensate for lower energy density by increasing battery pack size, which can add weight and reduce system efficiency in mobility applications.

Commercial performance benchmarks indicate that LFP batteries typically achieve energy densities of around 140–180 Wh/kg, while advanced NMC chemistries can exceed 220–300 Wh/kg, creating a significant gap in applications requiring maximum energy storage within limited space constraints.

Key Market Opportunity: Expansion In Grid Scale Energy Storage And Affordable EV Platforms

The growing global focus on renewable energy integration and electrification of transport is creating strong opportunities for LFP batteries in both stationary and mobility applications. Increasing installation of solar and wind power plants requires large-scale storage systems capable of balancing intermittent generation, making LFP batteries a preferred choice due to long cycle life, safety, and cost efficiency.

Electric vehicle manufacturers are increasingly adopting LFP chemistry for entry-level and fleet vehicles, such as ride-hailing and commercial delivery EVs, to reduce total ownership cost and improve operational reliability. Companies such as BYD, Tesla, and CATL are scaling LFP production to support mass-market EV adoption across Asia-Pacific and Europe.

In addition, advancements in cell-to-pack and blade battery technologies are improving volumetric efficiency and structural integration, opening opportunities in compact EV platforms, residential energy storage systems, and microgrid applications. Large-scale deployments in China and India during 2025 show LFP-based grid storage projects achieving round-trip efficiency levels of around 85–92%, supporting stronger renewable energy utilization and grid stability.

Lithium Iron Phosphate (LFP) Batteries Market Scope

The market is segmented on the basis of application, power capacity, and industry.

- By Application

On the basis of application, the lithium iron phosphate (LFP) batteries market is segmented into Stationary and Portable. The Stationary segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong deployment in grid-scale energy storage systems, renewable integration projects, and backup power infrastructure for data centers and telecom towers. LFP batteries are widely preferred in stationary applications due to their long cycle life, high thermal stability, and lower total cost of ownership across continuous charge-discharge operations.

The Portable segment is projected to register steady growth at a CAGR of 9.6% from 2026 to 2033, driven by rising adoption in electric vehicles, consumer electronics, and portable power systems. Increasing demand for lightweight, safe, and long-lasting battery solutions in EVs such as entry-level passenger vehicles and electric two-wheelers is accelerating segment expansion across Asia-Pacific and Europe.

- By Power Capacity

On the basis of power capacity, the lithium iron phosphate (LFP) batteries market is segmented into 0–16,250 Mah, 16,251–50,000 Mah, 50,001–100,000 Mah, and 100,001–540,000 Mah. The 100,001–540,000 Mah segment held the largest market revenue share of approximately 46.7% in 2025 driven by extensive usage in electric vehicles, utility-scale energy storage systems, and commercial backup power applications. Large-capacity LFP battery packs are increasingly deployed in EV platforms and grid storage projects due to their high durability and superior thermal safety performance under heavy load conditions.

The 50,001–100,000 Mah segment is projected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by rising demand in mid-range electric vehicles, residential energy storage systems, and industrial UPS applications. Expanding adoption of distributed energy storage solutions for solar integration is further supporting segment growth across emerging markets.

- By Industry

On the basis of industry, the lithium iron phosphate (LFP) batteries market is segmented into Automotive, Power, Industrial, and Others. The Automotive segment held the largest market revenue share of approximately 49.2% in 2025 driven by rapid electrification of passenger vehicles, electric buses, and commercial fleets. Leading manufacturers such as BYD and Tesla are increasingly integrating LFP chemistry into mass-market EV models to reduce cost and enhance safety performance.

The Power segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by large-scale deployment of renewable energy storage systems and grid stabilization projects. Increasing investments in solar and wind energy infrastructure across China, India, and the U.S. are accelerating adoption of LFP batteries for efficient energy balancing and peak load management across utility networks.

Lithium Iron Phosphate (LFP) Batteries Market Regional Analysis

North America Lithium Iron Phosphate (LFP) Batteries Market Insight

North America held a significant revenue share of approximately 32.6% in 2025 in the lithium iron phosphate (LFP) batteries market, supported by rapid expansion of electric vehicle adoption, strong investments in grid-scale energy storage, and increasing focus on renewable energy integration. The region benefits from well-established EV infrastructure, high technology adoption, and strong policy support for clean energy transition, particularly in the U.S. and Canada. LFP batteries are increasingly preferred due to their superior safety profile, long cycle life, and cost advantages compared to nickel-based chemistries, making them suitable for both mobility and stationary storage applications.

U.S. Lithium Iron Phosphate (LFP) Batteries Market Insight

The U.S. LFP batteries market captured the largest revenue share within North America in 2025, driven by rapid electrification of transportation, expansion of utility-scale battery storage projects, and increasing deployment of renewable energy systems. Growing adoption of LFP chemistry in electric vehicles such as Tesla’s standard range models and commercial fleet EVs is strengthening market penetration. In addition, large-scale energy storage installations in states such as California and Texas are accelerating demand for LFP systems to support grid stability and peak load management.

Europe Lithium Iron Phosphate (LFP) Batteries Market Insight

The Europe LFP batteries market is expected to witness strong growth from 2026 to 2033, driven by stringent carbon emission regulations, aggressive EV adoption targets, and rapid expansion of renewable energy capacity. Increasing investments in battery gigafactories and localized supply chains are supporting adoption across Germany, France, and the Nordic region. Europe is also witnessing rising demand for stationary storage systems to balance wind and solar energy fluctuations, further strengthening LFP deployment across utility and industrial applications.

U.K. Lithium Iron Phosphate (LFP) Batteries Market Insight

The U.K. LFP batteries market is expected to register strong growth from 2026 to 2033, driven by increasing EV penetration, rising investments in renewable energy storage, and government initiatives supporting net-zero emissions. Growing adoption of residential and commercial battery storage systems is supporting demand for LFP chemistry due to its safety advantages and long lifecycle. In addition, expansion of EV charging infrastructure and fleet electrification programs is accelerating market growth across urban regions.

Germany Lithium Iron Phosphate (LFP) Batteries Market Insight

The Germany LFP batteries market is expected to witness robust growth from 2026 to 2033, supported by strong automotive manufacturing base, increasing EV production, and expansion of energy storage infrastructure. Germany’s focus on industrial decarbonization and renewable integration is driving demand for safe and durable battery technologies. Automotive OEMs are increasingly evaluating LFP batteries for entry-level EV platforms, while utility-scale projects are deploying LFP systems to enhance grid reliability and energy efficiency.

Asia-Pacific Lithium Iron Phosphate (LFP) Batteries Market Insight

The Asia-Pacific LFP batteries market accounted for the largest revenue share of approximately 44.8% in 2025, driven by large-scale EV production, strong battery manufacturing ecosystem, and rapid deployment of renewable energy storage systems. Countries such as China, Japan, and India are leading adoption due to supportive government policies, high EV penetration, and strong domestic manufacturing capabilities. The region remains the global hub for LFP production, supported by leading battery manufacturers and cost-efficient supply chains.

Japan Lithium Iron Phosphate (LFP) Batteries Market Insight

The Japan LFP batteries market is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of electric vehicles, focus on energy security, and rising demand for stationary storage systems. Japan’s advanced technology ecosystem and strong emphasis on safety and reliability are supporting gradual adoption of LFP chemistry in both automotive and industrial applications. Integration of renewable energy systems with battery storage is further contributing to market expansion.

China Lithium Iron Phosphate (LFP) Batteries Market Insight

The China LFP batteries market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to massive EV production scale, strong dominance of domestic battery manufacturers, and extensive deployment in grid storage systems. China is the global leader in LFP battery production, with companies such as CATL and BYD driving large-scale commercialization. Rapid expansion of electric mobility, combined with government support for clean energy infrastructure and smart grid development, continues to strengthen China’s dominance in the global LFP battery market.

Lithium Iron Phosphate (LFP) Batteries Market Share

The Lithium Iron Phosphate (LFP) Batteries industry is primarily led by well-established companies, including:

• BYD Company Ltd. (China)

• A123 Systems LLC (U.S.)

• Electric Vehicle Power System Technology Co., Ltd (EVPST) (China)

• OptimumNano Energy Co., Ltd. (China)

• K2 Energy Solutions (U.S.)

• Pihsiang Energy Technology Co., Ltd. (Taiwan)

• Aleees (Taiwan)

• Pulead Technology Industry Co., Ltd. (China)

• Panasonic Corporation (Japan)

• SAMSUNG (South Korea)

• SHENZHEN BAK BATTERY CO., LTD. (China)

• GS Yuasa International Ltd. (Japan)

• Showa Denko Materials Co., Ltd. (Japan)

• Johnson Controls (U.S.)

• Amperex Technology Limited (Hong Kong)

• Murata Manufacturing Co., Ltd. (Japan)

Latest Developments in Lithium Iron Phosphate (LFP) Batteries Market

- In December 2024, Stellantis N.V. and CATL announced a joint venture development for establishing a carbon-neutral LFP battery plant in Zaragoza, Spain, with an investment of up to USD 4.28 billion. The facility is expected to begin production in Q4 2026 with a 50 GWh capacity. This initiative aims to strengthen affordable EV battery supply for B and C segment vehicles across Europe, improving cost efficiency and scalability in the LFP battery market.

- In September 2024, Hyundai Motor Company and Kia Corporation announced a collaborative development initiative focused on advancing LFP cathode technology for EV batteries. This development aims to enhance energy density, safety, and cost efficiency, thereby supporting the production of more affordable and sustainable electric vehicles. The partnership is expected to strengthen their competitive position in the global EV ecosystem and accelerate LFP adoption in mass-market mobility.

- In September 2024, Nissan Motor Co. Ltd. announced the development of next-generation all-solid-state battery (ASSB) technology, targeting improved energy density, faster charging, and higher efficiency for electric vehicles. The company plans to begin mass production by 2028, which is expected to significantly extend driving range and enhance EV performance. This advancement is anticipated to accelerate the global shift toward high-performance sustainable mobility solutions.

- In August 2023, Contemporary Amperex Technology Co. Limited (CATL) launched a new fast-charging LFP EV battery designed to improve charging speed and performance, with plans for mass production by the end of 2024. This development strengthens CATL’s leadership in LFP innovation, supporting wider EV adoption by reducing charging time and improving user convenience across electric mobility applications.

- In March 2022, Britishvolt initiated discussions with around 20 automotive OEMs to develop high-nickel and LFP battery technologies for passenger and commercial vehicles. This strategic engagement aimed to support next-generation EV battery innovation and supply chain expansion. The development was expected to enhance collaboration between battery developers and automakers, accelerating the commercialization of advanced battery chemistries.

- In August 2021, Contemporary Amperex Technology Co. Limited (CATL) invested USD 15.6 million to establish a new automotive science and technology company in Shanghai. The development aimed to expand its R&D and manufacturing capabilities for LFP batteries used in electric vehicles, including supply partnerships with major OEMs such as Tesla and NIO. This move strengthened CATL’s production ecosystem and reinforced its leadership in global LFP battery supply chains.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Lithium Iron Phosphate Lfp Batteries Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Lithium Iron Phosphate Lfp Batteries Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Lithium Iron Phosphate Lfp Batteries Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.