Global Lithographic Printing Chemicals Market

Market Size in USD Million

USD

16.64 Million

USD

22.77 Million

2025

2033

USD

16.64 Million

USD

22.77 Million

2025

2033

| 2026 - 2033 | |

| USD 16.64 Million | |

| USD 22.77 Million | |

| % | |

|

Global Lithographic Printing Chemicals Market Size

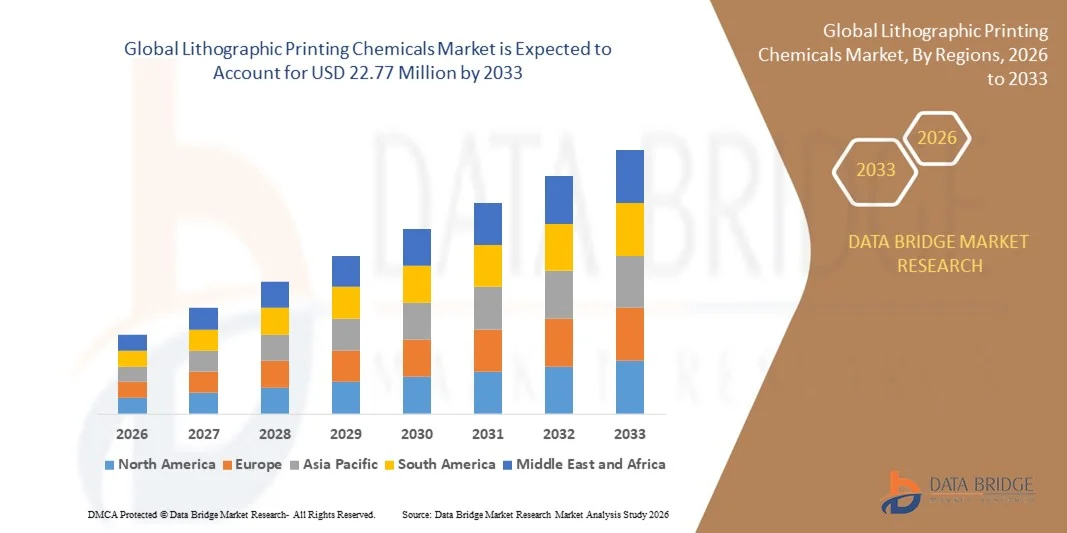

- The Global Lithographic Printing Chemicals Market size was valued at USD 16.64 million in 2025 and is projected to reach USD 22.77 million by 2033, growing at a CAGR of 4.00% during the forecast period.

- Market expansion is primarily driven by the increasing demand for high-quality printing across packaging, publishing, and commercial printing sectors, supported by advancements in printing technologies and eco-friendly chemical formulations.

- Moreover, the growing emphasis on sustainable printing solutions and the rising adoption of digital and hybrid printing methods are fueling innovation in lithographic printing chemicals, thereby accelerating market growth globally.

Global Lithographic Printing Chemicals Market Analysis

- Lithographic printing chemicals, which include fountain solutions, plate cleaners, inks, and solvents, are essential components in modern printing processes across packaging, publishing, and commercial printing applications, valued for their ability to deliver high-quality, durable, and precise print outputs.

- The growing demand for lithographic printing chemicals is primarily driven by the expansion of the packaging industry, technological advancements in printing machinery, and the increasing need for sustainable and low-VOC chemical formulations.

- Asia-Pacific dominated the Global Lithographic Printing Chemicals Market with the largest revenue share of 35% in 2025, supported by a well-established printing industry, strong adoption of advanced printing technologies, and the presence of major chemical manufacturers focusing on environmentally friendly products and high-performance formulations.

- North America is expected to be the fastest-growing region in the Global Lithographic Printing Chemicals Market during the forecast period due to rapid industrialization, increasing print demand from the packaging sector, and rising investments in commercial printing infrastructure.

- The inks segment dominated the market with the largest revenue share of 45.6% in 2025, driven by the critical role of high-quality inks in achieving vibrant, durable, and precise print outputs across packaging, commercial, and publishing applications.

Report Scope and Global Lithographic Printing Chemicals Market Segmentation

|

Attributes |

Lithographic Printing Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Lithographic Printing Chemicals Market Trends

Advancements in Eco-Friendly and Sustainable Printing Solutions

- A significant and accelerating trend in the Global Lithographic Printing Chemicals Market is the growing emphasis on eco-friendly and sustainable chemical formulations driven by tightening environmental regulations and increasing demand for green printing practices. This shift is encouraging manufacturers to innovate with biodegradable, low-VOC, and water-based products to reduce environmental impact without compromising print quality.

- For instance, leading companies such as Flint Group and Toyo Ink SC Holdings have introduced advanced water-based inks and solvent-free solutions designed to minimize emissions and improve workplace safety. Similarly, Sun Chemical and DIC Corporation are investing heavily in bio-based resins and recyclable packaging inks to meet evolving sustainability goals.

- Sustainable chemistry innovations in lithographic printing chemicals are also enhancing press performance and print efficiency. New-generation fountain solutions and cleaning agents are formulated to extend plate life, reduce waste, and optimize ink-water balance—key factors in achieving consistent, high-quality outputs.

- Furthermore, the integration of digital monitoring technologies in modern printing presses allows for precise control of chemical usage, reducing overconsumption and improving operational sustainability. This alignment of chemical innovation and digital optimization is reshaping production workflows across the printing industry.

- This trend toward sustainability is not only redefining product development but also transforming market competitiveness, as clients increasingly prefer environmentally responsible suppliers. Companies such as Huber Group and Siegwerk are at the forefront of this transition, developing complete ranges of eco-friendly lithographic printing chemicals that align with global sustainability standards.

- The demand for sustainable and performance-driven lithographic printing chemicals is expanding rapidly across both developed and emerging markets, as industries prioritize greener production methods and adopt environmentally conscious printing technologies.

Global Lithographic Printing Chemicals Market Dynamics

Driver

Growing Demand Driven by Packaging Expansion and Technological Advancements

- The increasing demand for high-quality and durable printing across packaging, publishing, and commercial applications, coupled with advancements in printing technology, is a significant driver for the rapid growth of the Global Lithographic Printing Chemicals Market.

- For instance, in March 2025, Flint Group announced the launch of its next-generation VIVO Colour Solutions designed to enhance print accuracy and reduce waste in packaging production. Such strategic innovations by key players are expected to propel market expansion over the forecast period.

- As industries continue to prioritize visually appealing and sustainable packaging, lithographic printing chemicals—such as inks, fountain solutions, and cleaning agents—are gaining prominence for their ability to deliver superior print precision and efficiency.

- Furthermore, the rising adoption of automation and hybrid printing technologies is fostering greater productivity and consistency in lithographic printing processes, enabling faster turnaround times and improved cost-effectiveness for manufacturers.

- The growing emphasis on eco-friendly and low-VOC chemical formulations, combined with increasing investments in research and development for high-performance printing materials, is further accelerating market demand. Continuous innovation in ink composition and pressroom chemistry is enabling printers to meet diverse customer needs while adhering to environmental regulations.

Restraint/Challenge

Environmental Regulations and High Production Costs

- Stringent environmental regulations regarding volatile organic compound (VOC) emissions and waste disposal present significant challenges to the lithographic printing chemicals industry. As governments worldwide tighten sustainability standards, manufacturers are required to reformulate products, increasing production complexity and costs.

- For instance, stricter European Union directives on solvent-based chemicals have compelled companies to transition toward water-based and biodegradable alternatives, often requiring substantial R&D investment.

- Addressing these regulatory challenges through innovation in sustainable chemistry and compliance-driven product development is essential for maintaining competitiveness. Leading players such as Toyo Ink SC Holdings and DIC Corporation are actively developing low-VOC inks and solvent-free cleaning solutions to align with environmental goals.

- Additionally, fluctuations in raw material prices and the high cost of advanced eco-friendly formulations can limit market accessibility, particularly for small- and medium-scale printing enterprises. This economic constraint is most apparent in emerging markets where budget-sensitive printers prioritize cost efficiency over sustainability.

- To overcome these challenges, the industry must continue investing in green technologies, promote recycling initiatives, and educate end-users on the long-term economic and environmental benefits of adopting sustainable lithographic printing chemicals.

Global Lithographic Printing Chemicals Market Scope

Lithographic printing chemicals market is segmented on the basis of product type and end use.

- By Product Type

On the basis of product type, the Global Lithographic Printing Chemicals Market is segmented into inks, fountain solutions, and cleaning solutions. The inks segment dominated the market with the largest revenue share of 45.6% in 2025, driven by the critical role of high-quality inks in achieving vibrant, durable, and precise print outputs across packaging, commercial, and publishing applications. Advances in low-VOC and eco-friendly inks further enhance their appeal, as businesses seek sustainable solutions without compromising print quality.

The fountain solutions segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, fueled by increasing adoption of automated and hybrid printing presses that require advanced solutions for consistent ink-water balance, improved plate performance, and reduced waste. Continuous innovations in water-based and solvent-free fountain solutions also contribute to their growing popularity among environmentally conscious printers.

- By End Use

On the basis of end use, the Global Lithographic Printing Chemicals Market is segmented into publication, packaging, and promotion. The packaging segment accounted for the largest market revenue share of 52.3% in 2025, driven by the booming demand for high-quality, visually appealing packaging in food, beverage, cosmetics, and consumer goods sectors. The increasing focus on branding, product differentiation, and compliance with sustainability standards further reinforces market dominance.

The publication segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, supported by the sustained demand for high-quality print in books, magazines, and educational materials, coupled with technological advancements that enhance print efficiency and reduce production costs. Digital integration and eco-friendly formulations are also key factors driving adoption in the publication sector.

Global Lithographic Printing Chemicals Market Regional Analysis

- Asia-Pacific dominated the Global Lithographic Printing Chemicals Market with the largest revenue share of 35% in 2025, driven by a well-established printing industry, high demand for commercial and packaging printing, and the early adoption of advanced printing technologies.

- Manufacturers and businesses in the region prioritize high-quality, durable, and eco-friendly printing solutions, which fuels demand for premium lithographic printing chemicals such as inks, fountain solutions, and cleaning agents.

- This widespread adoption is further supported by the presence of major chemical manufacturers, robust R&D investments, and stringent quality standards, establishing North America as a key hub for innovation and supply in the lithographic printing chemicals sector. High disposable incomes, technologically advanced printing infrastructure, and a strong focus on sustainability also contribute to the region’s leading market position.

U.S. Lithographic Printing Chemicals Market Insight

The U.S. lithographic printing chemicals market captured the largest revenue share of 38% in 2025 within North America, driven by the country’s well-established printing industry and high demand for packaging, commercial, and publication printing. Manufacturers prioritize high-performance inks, fountain solutions, and cleaning agents that deliver precise, durable, and vibrant prints. The growing adoption of eco-friendly and low-VOC formulations, along with investments in automated and hybrid printing technologies, further propels market growth. Additionally, the strong presence of leading chemical manufacturers and advanced printing infrastructure supports innovation and rapid product deployment, making the U.S. a dominant player in the global market.

Europe Lithographic Printing Chemicals Market Insight

The Europe lithographic printing chemicals market is projected to expand at a substantial CAGR during the forecast period, driven by stringent environmental regulations, rising demand for sustainable printing solutions, and increased production in packaging and commercial printing sectors. Countries such as Germany, France, and the U.K. are emphasizing low-VOC inks and biodegradable solutions, fostering widespread adoption. The market growth is also supported by modernization of printing presses, increasing urbanization, and the growing need for high-quality printing outputs in residential, commercial, and industrial applications.

U.K. Lithographic Printing Chemicals Market Insight

The U.K. lithographic printing chemicals market is expected to grow at a noteworthy CAGR during the forecast period, driven by rising demand for high-quality packaging and publication printing, coupled with a strong focus on sustainable and environmentally friendly solutions. The growing adoption of modern printing technologies, including automated and digital press systems, enhances the efficiency and quality of lithographic printing. Additionally, stringent government regulations regarding VOC emissions and waste management encourage the use of eco-friendly inks, fountain solutions, and cleaning agents, supporting steady market growth.

Germany Lithographic Printing Chemicals Market Insight

The Germany lithographic printing chemicals market is anticipated to expand at a considerable CAGR during the forecast period, fueled by the country’s well-developed printing infrastructure, high industrial output, and emphasis on sustainability. German manufacturers and commercial printers increasingly adopt eco-friendly inks, water-based fountain solutions, and solvent-free cleaning chemicals to comply with regulatory standards and reduce environmental impact. The integration of advanced press technologies and automation systems also drives efficiency, consistency, and high-quality print outputs, positioning Germany as a key market in Europe.

Asia-Pacific Lithographic Printing Chemicals Market Insight

The Asia-Pacific lithographic printing chemicals market is poised to grow at the fastest CAGR of 23.5% from 2026 to 2033, driven by rapid industrialization, urbanization, and rising demand from packaging, commercial, and publication printing sectors in countries such as China, India, and Japan. Increasing disposable incomes and government initiatives supporting digitalization and smart manufacturing are further boosting market adoption. The region is emerging as both a major consumer and manufacturer of printing chemicals, offering affordable and innovative solutions to a growing customer base.

Japan Lithographic Printing Chemicals Market Insight

The Japan lithographic printing chemicals market is gaining momentum due to the country’s advanced printing technologies, high-quality standards, and strong industrial base. The demand for high-performance inks, fountain solutions, and cleaning chemicals is increasing, particularly in commercial, packaging, and publication printing. Manufacturers in Japan focus on sustainability, low-VOC formulations, and automation-compatible solutions to improve print efficiency and reduce environmental impact. Additionally, the growing emphasis on smart manufacturing and integrated printing processes supports the adoption of advanced lithographic chemicals.

China Lithographic Printing Chemicals Market Insight

The China lithographic printing chemicals market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by the country’s booming packaging and commercial printing sectors, rapid urbanization, and expanding industrial base. The increasing demand for high-quality and cost-effective printing solutions, coupled with government initiatives promoting sustainable production, fuels market growth. China’s domestic manufacturing capabilities, availability of affordable chemical solutions, and adoption of modern printing technologies position it as a dominant market in the Asia-Pacific region.

Global Lithographic Printing Chemicals Market Share

The Lithographic Printing Chemicals industry is primarily led by well-established companies, including:

• BASF SE (Germany)

• Sun Chemical (U.S.)

• Flint Group (Switzerland)

• DIC Corporation (Japan)

• Siegwerk Group (Germany)

• Hubergroup (India)

• Chromaflo Technologies (U.S.)

• Toyo Ink Group (Japan)

• Gans Ink & Supply (U.S.)

• Lubrizol Advanced Materials (U.S.)

• Dow Inc. (U.S.)

• T&K Toka Co., Ltd. (Japan)

• TCP Global (U.S.)

• Inkcups (U.S.)

• Fujifilm Speciality Ink Systems (Japan)

• Hitachi Chemical (Japan)

• Colorcon (U.S.)

• Marabu GmbH & Co. KG (Germany)

• InkTec Co., Ltd. (South Korea)

• Flint Group Packaging Inks (Netherlands)

What are the Recent Developments in Global Lithographic Printing Chemicals Market?

- In April 2024, BASF SE, a global leader in specialty chemicals, launched a strategic initiative in South Africa to expand its portfolio of lithographic printing chemicals, including advanced inks, fountain solutions, and cleaning agents. This initiative highlights BASF’s commitment to providing high-performance, eco-friendly printing solutions tailored to the specific needs of commercial and packaging printers in the region. By leveraging its global expertise, BASF aims to strengthen its presence in the rapidly growing Global Lithographic Printing Chemicals Market while promoting sustainable printing practices.

- In March 2024, Sun Chemical, a leading provider of printing inks and coatings, introduced a new range of low-VOC and water-based inks specifically designed for publication and packaging applications. The innovative product line addresses environmental regulations and rising demand for eco-friendly solutions, reflecting Sun Chemical’s focus on combining performance with sustainability. This launch reinforces the company’s position as a key innovator in the global lithographic printing chemicals market.

- In March 2024, Flint Group successfully deployed an advanced printing solutions initiative in Bengaluru, India, aimed at improving print quality and operational efficiency for commercial and packaging printers. The initiative leverages state-of-the-art lithographic chemicals, including fountain solutions and cleaning agents, to enhance productivity and reduce waste, demonstrating Flint Group’s commitment to technological innovation in the printing industry.

- In February 2024, Siegwerk Group, a leading manufacturer of printing inks, announced a strategic partnership with a consortium of packaging manufacturers in North America to develop high-performance, sustainable inks for food and beverage packaging. This collaboration aims to streamline production processes, enhance print quality, and ensure compliance with evolving regulatory standards, highlighting Siegwerk’s dedication to advancing innovation and operational excellence in lithographic printing chemicals.

- In January 2024, DIC Corporation, a prominent provider of printing inks and coatings, unveiled its latest line of eco-friendly lithographic inks at the PRINTING United Expo 2024. The new product line, featuring high durability and vibrant color reproduction, enables printers to achieve superior results while minimizing environmental impact. This launch underscores DIC Corporation’s commitment to delivering innovative, high-performance solutions in the global lithographic printing chemicals market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Lithographic Printing Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Lithographic Printing Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Lithographic Printing Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.