Global Load Balancer Market

Market Size in USD Billion

USD

6.11 Billion

USD

16.61 Billion

2024

2032

USD

6.11 Billion

USD

16.61 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 6.11 Billion |

Market Size (Forecast Year) |

USD 16.61 Billion |

CAGR |

% |

Major Markets Players |

|

Load Balancer Market Size

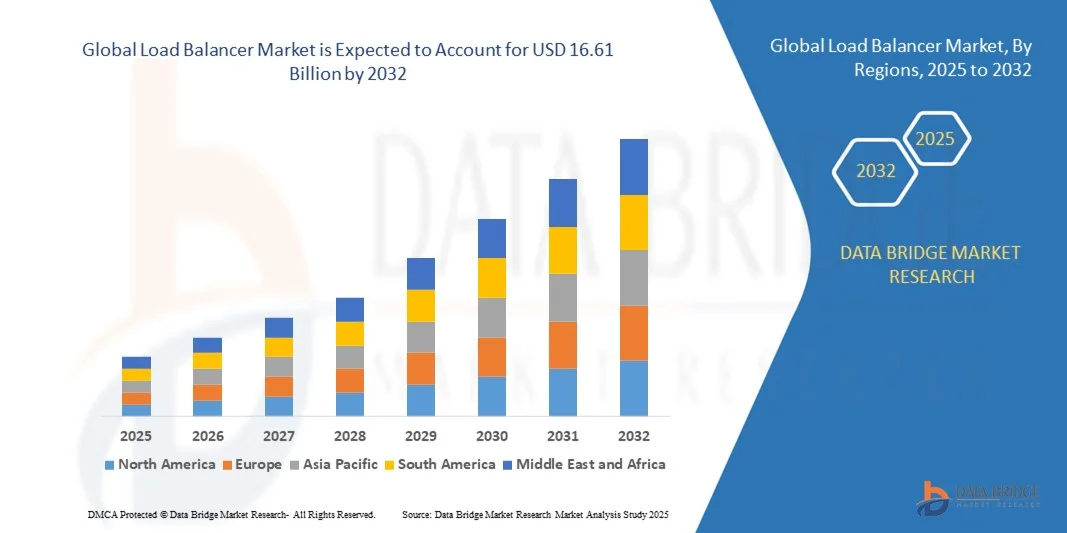

- The global load balancer market size was valued at USD 6.11 billion in 2024 and is expected to reach USD 16.61 billion by 2032, at a CAGR of 13.30% during the forecast period

- The market growth is largely fuelled by the increasing adoption of cloud computing, rising demand for high-availability applications, and the need for efficient traffic management across enterprise networks

- Rapid digital transformation, growing dependence on online services, and the increasing volume of data traffic across IT infrastructure are further driving the market

Load Balancer Market Analysis

- The global load balancer market is witnessing rapid growth due to the increasing adoption of cloud computing, virtualization, and digital transformation across enterprises

- Rising demand for high-availability applications, efficient traffic management, and uninterrupted user experiences is fueling market expansion

- North America dominated the load balancer market with the largest revenue share in 2024, driven by widespread adoption of cloud computing, virtualization, and enterprise IT infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global load balancer market, driven by rapid cloud adoption, increasing IT modernization initiatives, and rising demand for high-performance and secure networking solutions across emerging economies

- The hardware segment held the largest market revenue share in 2024, driven by its robust performance and reliability in handling high-volume enterprise traffic. Hardware-based solutions are preferred by large organizations for mission-critical applications requiring low latency and high availability

Report Scope and Load Balancer Market Segmentation

|

Attributes |

Load Balancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Load Balancer Market Trends

Rising Adoption of Cloud-Based and Software-Defined Load Balancers

- The increasing shift toward cloud-based and software-defined load balancers is transforming enterprise network management by enabling real-time traffic distribution and optimized application performance. These solutions allow IT teams to dynamically allocate workloads, reduce latency, and ensure high availability, especially in complex multi-cloud environments

- The growing need for rapid application delivery and performance monitoring in remote and distributed IT infrastructures is accelerating the adoption of advanced load balancing solutions. Organizations are leveraging software-based and virtual load balancers to handle unpredictable traffic spikes efficiently and minimize downtime

- The scalability, flexibility, and cost-effectiveness of modern load balancers are making them ideal for enterprises of all sizes, improving overall IT performance and reliability without extensive hardware investment

- For instance, in 2023, several global e-commerce platforms reported improved website performance and reduced downtime after implementing cloud-based load balancers, resulting in enhanced customer experience and higher transaction success rates

- While cloud-based and intelligent load balancing solutions are driving market growth, their impact depends on continued innovation, cybersecurity measures, and integration capabilities. Vendors must focus on automation, AI-driven traffic management, and seamless hybrid-cloud deployment strategies to fully capitalize on this demand

Load Balancer Market Dynamics

Driver

Growing Need for High Availability, Reliability, and Optimized Application Performance

- Increasing reliance on digital services, web applications, and mobile platforms is pushing organizations to adopt load balancers as a frontline solution for uninterrupted service delivery. High traffic volumes and distributed networks necessitate real-time traffic management to prevent outages

- Enterprises are becoming more aware of the operational and financial risks associated with application downtime, including lost revenue, reduced productivity, and poor customer satisfaction. This awareness is driving widespread deployment of advanced load balancing solutions

- Organizations are investing in AI-powered and automated load balancers to enhance performance monitoring, predict traffic spikes, and optimize network utilization, resulting in more resilient IT operations

- For instance, in 2022, several financial institutions in North America implemented software-defined load balancers to ensure uninterrupted transaction processing and minimize downtime, boosting operational efficiency

- While demand and adoption are rising, there is a need to continuously upgrade systems, train IT staff, and integrate with existing enterprise infrastructure to maintain optimal performance and long-term market growth

Restraint/Challenge

High Implementation Cost and Complexity of Advanced Load Balancing Solutions

- The high cost of enterprise-grade load balancers, including hardware appliances, software licenses, and cloud subscriptions, limits adoption among small and medium-sized organizations. Initial investments and ongoing maintenance expenses remain significant barriers. In addition, frequent software updates, licensing renewals, and support fees further increase the total cost of ownership, making it challenging for budget-constrained enterprises to adopt advanced solutions

- Many organizations face challenges in integrating advanced load balancing solutions with existing legacy IT infrastructure, increasing deployment complexity and extending implementation timelines. Compatibility issues, configuration difficulties, and potential service disruptions during migration can hinder seamless adoption. This often necessitates specialized consultancy or support services, further adding to project costs and timelines

- Limited availability of trained personnel to configure, manage, and optimize load balancing systems reduces operational efficiency, especially in regions with low IT skill penetration. Organizations often struggle with proper deployment, monitoring, and troubleshooting, which can lead to suboptimal performance or security vulnerabilities. Training programs and certified workforce development are required to bridge the skills gap, but these add additional operational costs

- For instance, in 2023, several SMEs in Asia-Pacific experienced delays in deploying software-defined load balancers due to integration challenges with legacy on-premise servers and networking systems. These delays caused temporary performance degradation and impacted critical business operations. Such cases highlight the importance of robust implementation planning and the need for simplified, user-friendly deployment solutions

- While load balancing technologies continue to evolve, addressing cost, integration, and skill gaps is critical. Vendors must focus on scalable, automated, and user-friendly solutions to unlock long-term market potential. In addition, investments in cloud-native architectures, AI-driven optimization, and managed services can reduce complexity, improve adoption rates, and expand the market across SMEs and emerging regions

Load Balancer Market Scope

The market is segmented on the basis of component, load balancer type, deployment type, organization size, and vertical.

- By Component

On the basis of component, the load balancer market is segmented into hardware, software, and services. The hardware segment held the largest market revenue share in 2024, driven by its robust performance and reliability in handling high-volume enterprise traffic. Hardware-based solutions are preferred by large organizations for mission-critical applications requiring low latency and high availability.

The software and services segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by flexibility, cost-effectiveness, and seamless integration with cloud environments. Software-based load balancers enable dynamic traffic management, AI-driven optimization, and simplified deployment, making them increasingly popular across SMEs and large enterprises asuch as.

- By Load Balancer Type

On the basis of load balancer type, the market is segmented into local load balancer and global load balancer. The local load balancer segment held the largest market revenue share in 2024, driven by its efficiency in managing traffic within enterprise networks and data centers. These solutions are preferred for applications requiring low latency and high availability within a single region.

The global load balancer segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by the increasing adoption of multi-region cloud applications and the need for optimized global traffic distribution. Global load balancers provide seamless application delivery across geographically distributed networks, enhancing performance and reliability for international operations.

- By Deployment Type

On the basis of deployment type, the market is segmented into on-premises and cloud. The on-premises segment held the largest market revenue share in 2024, driven by high security, control, and integration with existing IT infrastructure. Enterprises with critical applications prefer on-premises solutions to ensure minimal downtime and predictable performance.

The cloud segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by scalability, cost-effectiveness, and easy integration with cloud-native applications. Cloud-based load balancers enable automated traffic management, improved elasticity, and reduced infrastructure maintenance, making them increasingly adopted by SMEs and large enterprises.

- By Organization Size

On the basis of organization size, the market is segmented into small and medium-sized enterprises (SMEs) and large enterprises. The large enterprise segment held the largest market revenue share in 2024, driven by extensive IT infrastructure and the need for uninterrupted application performance. These organizations prioritize reliability, high availability, and advanced traffic management capabilities.

The SMEs segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by cost-effective, scalable, and easy-to-deploy load balancing solutions. SMEs are increasingly adopting software-based and cloud-enabled load balancers to optimize network performance and support business growth.

- By Vertical

On the basis of vertical, the market is segmented into banking, financial services, and insurance (BFSI), IT and telecom, government and public sector, media and entertainment, retail, manufacturing, healthcare and life sciences, energy, and others. The IT and telecom segment held the largest market revenue share in 2024, driven by high-volume data traffic and growing cloud adoption. These organizations require robust load balancing to maintain seamless application performance.

The BFSI, retail, and healthcare segments is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing online transactions, digital services, and demand for high-availability applications. Load balancers in these verticals ensure reduced downtime, enhanced user experience, and optimized network performance.

Load Balancer Market Regional Analysis

- North America dominated the load balancer market with the largest revenue share in 2024, driven by widespread adoption of cloud computing, virtualization, and enterprise IT infrastructure

- Organizations in the region prioritize high availability, low latency, and optimized application performance, fueling demand for advanced load balancing solutions

- This adoption is further supported by strong IT investment, presence of leading technology providers, and the growing focus on digital transformation initiatives across SMEs and large enterprises

U.S. Load Balancer Market Insight

The U.S. load balancer market captured the largest revenue share within North America in 2024, fueled by rapid adoption of cloud services, software-defined data centers, and automated traffic management solutions. Enterprises increasingly rely on load balancers to ensure uninterrupted application delivery, enhanced cybersecurity, and optimized network performance. The growing preference for AI-driven and software-defined load balancing solutions is further propelling market expansion.

Europe Load Balancer Market Insight

The Europe load balancer market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by increasing digitalization, cloud adoption, and stringent data protection regulations. Organizations are investing in load balancing to ensure reliable application performance, compliance, and uninterrupted IT services. European enterprises across BFSI, IT, and government sectors are adopting advanced solutions to enhance operational efficiency and reduce downtime.

U.K. Load Balancer Market Insight

The U.K. load balancer market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing cloud adoption, digital transformation initiatives, and the growing demand for high-performance IT infrastructure. Enterprises are leveraging load balancers to optimize network traffic, enhance application delivery, and improve end-user experience. The country’s mature IT ecosystem and robust service provider network further support market growth.

Germany Load Balancer Market Insight

The Germany load balancer market is expected to witness the fastest growth rate from 2025 to 2032, fueled by growing adoption of cloud, virtualization, and hybrid IT infrastructure. Organizations are increasingly deploying load balancers to manage high-volume traffic, improve reliability, and ensure business continuity. Germany’s focus on industrial automation, IT modernization, and advanced networking solutions is boosting market demand across multiple sectors.

Asia-Pacific Load Balancer Market Insight

The Asia-Pacific load balancer market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid digitalization, cloud adoption, and IT infrastructure modernization in countries such as China, India, and Japan. The region’s growing number of SMEs and large enterprises adopting scalable IT solutions is accelerating load balancer deployment.

Japan Load Balancer Market Insight

The Japan load balancer market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s advanced IT infrastructure, high demand for reliable network services, and adoption of cloud-native applications. Enterprises are increasingly implementing automated and AI-driven load balancing solutions to optimize traffic management, reduce latency, and improve service quality. The trend is further supported by Japan’s emphasis on digital transformation and smart IT infrastructure.

China Load Balancer Market Insight

The China load balancer market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding enterprise IT infrastructure, and high cloud adoption rates. Enterprises across banking, telecom, retail, and government sectors are deploying advanced load balancing solutions to enhance application performance, manage high-volume traffic, and support large-scale digital services. The presence of domestic solution providers and competitive pricing are further propelling market growth.

Load Balancer Market Share

The Load Balancer industry is primarily led by well-established companies, including:

- Cisco Systems, Inc. (U.S.)

- Amazon Web Services, Inc. (U.S.)

- IBM (U.S.)

- Microsoft (U.S.)

- Google LLC (U.S.)

- Citrix Systems, Inc. (U.S.)

- F5, Inc. (U.S.)

- Imperva (U.S.)

- Radware (U.S.)

- Fortinet, Inc. (U.S.)

- A10 Networks, Inc. (U.S.)

- Palo Alto Networks (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- NortonLifeLock Inc. (U.S.)

- Forcepoint (U.S.)

- CyberArk Software Ltd. (Israel)

- Kemp Technologies (U.S.)

- Riverbed Technology (U.S.)

- Fastly, Inc. (U.S.)

- Dialogic Corporation (U.S.)

Latest Developments in Global Load Balancer Market

- In March 2024, Kyndryl Inc., an infrastructure services provider, partnered with Cloudflare, Inc., a cloud connectivity company, to extend their collaboration. The initiative aims to help enterprises migrate and manage multi-cloud networks while ensuring robust network security. By combining Kyndryl’s expertise in consulting, enterprise networking, and resilience with Cloudflare’s cloud connectivity solutions, the partnership delivers a unified platform for enhanced security, performance, and cloud adaptability, driving greater adoption of integrated network management solutions in the market

- In March 2024, Citrix, a business unit of Cloud Software Group, Inc., launched new customer and partner incentive programs for load balancer solutions. These initiatives offer discounted rates and expanded usage privileges to encourage migration from non-Citrix deployments, including competitors such as VMware and F5. The programs simplify workload transitions while highlighting the advanced load balancing capabilities of the Citrix platform, fostering increased market penetration and adoption among both existing and new users

- In May 2024, Microsoft Corporation expanded its partnership with Broadcom to support VMware Cloud Foundation (VCF) subscriptions on Azure VMware Solution. This development enables seamless migration of VMware workloads to Azure with minimal refactoring. Integrated load balancer functionalities optimize performance across Azure’s scalable cloud infrastructure, providing enterprises with greater flexibility, reliability, and efficiency, thereby strengthening Microsoft’s position in the cloud-based load balancer market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.