Global Load Break Switch Market

Market Size in USD Billion

USD

3.20 Billion

USD

4.73 Billion

2025

2033

USD

3.20 Billion

USD

4.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.20 Billion | |

| USD 4.73 Billion | |

| % | |

|

Load Break Switch Market Size

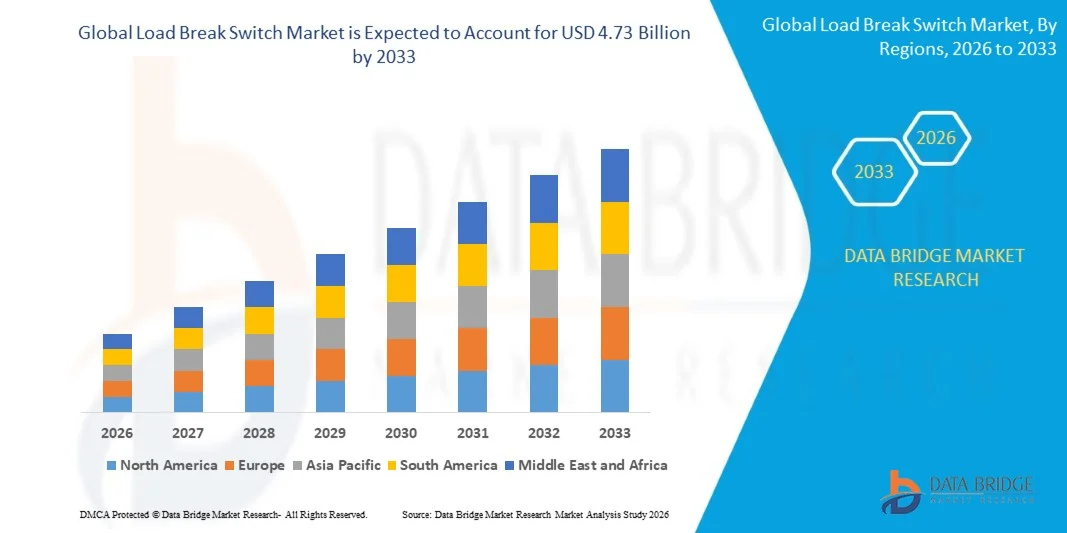

- The global load break switch market size was valued at USD 3.20 billion in 2025 and is expected to reach USD 4.73 billion by 2033, at a CAGR of 5.01% during the forecast period

- The market growth is largely driven by continuous expansion and modernization of power transmission and distribution networks, supported by rising electricity demand from urbanization, industrialization, and infrastructure development across both developed and emerging economies

- Furthermore, increasing integration of renewable energy sources and the need for reliable load management and fault isolation are positioning load break switches as essential components of medium-voltage networks, thereby accelerating market adoption and overall industry growth

Load Break Switch Market Analysis

- Load break switches, designed to safely interrupt and control electrical loads in medium-voltage distribution systems, play a critical role in ensuring grid reliability, operational safety, and efficient power flow across utility, industrial, and commercial applications

- The growing demand for load break switches is primarily fueled by grid modernization initiatives, rising focus on reducing power outages, and increasing investments in smart grids and renewable energy integration, all of which require advanced and dependable switching solutions

- Asia-Pacific dominated the load break switch market with a share of 36.2% in 2025, due to rapid expansion of power distribution networks, increasing electrification projects, and large-scale investments in grid infrastructure

- North America is expected to be the fastest growing region in the load break switch market during the forecast period due to large-scale grid modernization programs and rising investments in renewable energy integration

- Gas-insulated segment dominated the market with a market share of 36.9% in 2025, due to its compact design, high dielectric strength, and superior performance in space-constrained substations. Utilities increasingly prefer gas-insulated load break switches due to their high reliability, low maintenance requirements, and suitability for urban power distribution networks. Their ability to operate safely under harsh environmental conditions further strengthens adoption across modern grid infrastructure

Report Scope and Load Break Switch Market Segmentation

|

Attributes |

Load Break Switch Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Load Break Switch Market Trends

“Increasing Adoption of Smart and Digitally Enabled Load Break Switches”

- A prominent trend in the load break switch market is the growing adoption of smart and digitally enabled switches, driven by the need for improved grid reliability, real-time monitoring, and efficient load management in medium-voltage networks. Utilities and industrial operators are increasingly deploying intelligent load break switches to enhance fault detection, reduce outage durations, and support predictive maintenance strategies across distribution systems

- For instance, companies such as ABB and Siemens are integrating digital sensors and communication capabilities into load break switches to enable remote operation and condition monitoring. These smart features help operators gain better visibility into network performance and support faster decision-making during fault conditions

- The integration of digital technologies is gaining traction as power distribution networks become more complex due to rising renewable energy penetration. Smart load break switches help manage fluctuating power flows and improve system stability, supporting smoother integration of solar and wind energy sources

- Utilities are adopting digitally enabled switches to align with smart grid initiatives focused on automation and decentralization. These solutions support self-healing networks by enabling quicker isolation of faulty sections and restoration of power supply

- Industrial facilities are also embracing smart load break switches to improve operational safety and reduce unplanned downtime. The ability to monitor switching performance and equipment health remotely is strengthening demand for intelligent solutions

- This trend is reinforcing the transition toward automated and data-driven power distribution systems, positioning smart load break switches as critical components in modern electrical infrastructure

Load Break Switch Market Dynamics

Driver

“Expansion and Modernization of Power Transmission and Distribution Infrastructure”

- The continuous expansion and modernization of power transmission and distribution infrastructure is a key driver for the load break switch market. Growing electricity demand from urbanization, industrial growth, and infrastructure development is increasing the need for reliable medium-voltage switching equipment

- For instance, utilities investing in grid upgrades and new substations are deploying load break switches to improve operational safety and ensure uninterrupted power supply. These switches play a vital role in isolating faults and managing loads during maintenance and network expansion

- Aging power infrastructure in many regions is being replaced with modern systems that require advanced switching solutions. Load break switches support these upgrades by offering safer and more efficient load control compared to traditional equipment

- The expansion of renewable energy projects is further driving investments in transmission and distribution networks. Load break switches are essential for managing variable power inputs and maintaining grid stability in renewable-integrated systems

- As power networks continue to expand and evolve, the need for dependable and flexible switching solutions is reinforcing this driver and supporting steady market growth

Restraint/Challenge

“High Capital Cost and Complex Installation Requirements”

- The load break switch market faces challenges related to high capital costs and complex installation requirements, particularly for advanced and gas-insulated switching solutions. These factors can limit adoption among cost-sensitive utilities and smaller industrial users

- For instance, the installation of gas-insulated or vacuum-based load break switches often requires specialized expertise, precise handling, and compliance with strict safety standards. These requirements increase upfront investment and extend project timelines

- Advanced load break switches involve higher manufacturing and material costs due to the use of specialized insulation media and robust mechanical components. This raises procurement costs and can constrain budgets for large-scale deployment projects

- Complex installation and commissioning processes also increase dependence on skilled labor, which may be limited in certain regions. This can slow adoption in developing markets with constrained technical resources

- As a result, high initial investment and installation complexity remain key constraints, influencing purchasing decisions and moderating the pace of market penetration in some regions

Load Break Switch Market Scope

The market is segmented on the basis of type, voltage, installation, and end use.

• By Type

On the basis of type, the load break switch market is segmented into gas-insulated, vacuum-insulated, air-insulated, and oil-immersed switches. The gas-insulated segment dominated the market with the largest share of 36.9% in 2025, driven by its compact design, high dielectric strength, and superior performance in space-constrained substations. Utilities increasingly prefer gas-insulated load break switches due to their high reliability, low maintenance requirements, and suitability for urban power distribution networks. Their ability to operate safely under harsh environmental conditions further strengthens adoption across modern grid infrastructure.

The vacuum-insulated segment is expected to register the fastest growth from 2026 to 2033, supported by rising demand for environmentally friendly and arc-quenching efficient solutions. Vacuum technology offers longer operational life, reduced environmental impact, and enhanced switching performance, making it attractive for medium-voltage distribution systems. Increasing investments in sustainable power infrastructure and modernization of aging electrical networks are accelerating demand for vacuum-insulated load break switches.

• By Voltage

On the basis of voltage, the load break switch market is segmented into below 11 kV, 11–33 kV, and 33–60 kV categories. The 11–33 kV segment held the largest revenue share in 2025, attributed to its widespread use in primary distribution networks and substations. This voltage range is critical for balancing power transmission efficiency and safety, making it a standard choice for utilities and industrial facilities. Strong expansion of distribution infrastructure and rural electrification projects continues to support dominance of this segment.

The 33–60 kV segment is projected to grow at the fastest rate during the forecast period, driven by rising investments in high-capacity distribution systems and renewable energy integration. Increasing deployment of wind and solar power plants requires robust switching solutions at higher voltage levels. As utilities upgrade grids to handle higher loads and reduce transmission losses, demand for load break switches in this voltage range is expected to accelerate.

• By Installation

On the basis of installation, the load break switch market is segmented into outdoor and indoor installations. The outdoor segment dominated the market in 2025, owing to extensive deployment in substations, overhead distribution networks, and rural electrification projects. Outdoor load break switches are designed to withstand extreme weather conditions and provide reliable performance in exposed environments. Their widespread use in utility-scale applications and expanding transmission networks supports their leading position.

The indoor segment is anticipated to witness the fastest growth from 2026 to 2033, driven by increasing installation of compact substations in urban and industrial settings. Indoor load break switches offer enhanced safety, reduced space requirements, and easier integration with enclosed switchgear systems. Growing demand for smart buildings, data centers, and industrial automation is further boosting adoption of indoor installations.

• By End Use

On the basis of end use, the load break switch market is segmented into utilities, industrial, and commercial sectors. The utilities segment accounted for the largest market revenue share in 2025, supported by continuous investments in grid expansion, transmission upgrades, and distribution network reliability. Load break switches play a critical role in fault isolation and load management for utility operators, ensuring uninterrupted power supply. Ongoing electrification initiatives and renewable energy integration further reinforce dominance of the utilities segment.

The industrial segment is expected to grow at the fastest pace over the forecast period, driven by rapid industrialization and increasing demand for reliable power distribution systems. Manufacturing plants, mining operations, and processing facilities require efficient load management and safe switching operations to minimize downtime. Rising adoption of automation and energy-intensive industrial processes is significantly contributing to growth of load break switches in the industrial end-use segment.

Load Break Switch Market Regional Analysis

- Asia-Pacific dominated the load break switch market with the largest revenue share of 36.2% in 2025, driven by rapid expansion of power distribution networks, increasing electrification projects, and large-scale investments in grid infrastructure

- Rising urbanization, growing electricity demand from industrial and residential sectors, and continuous upgrades of aging transmission and distribution systems are accelerating market growth across the region

- Strong government focus on renewable energy integration, smart grid development, and rural electrification programs is further supporting adoption of load break switches in medium-voltage networks

China Load Break Switch Market Insight

China held the largest share in the Asia-Pacific load break switch market in 2025, supported by massive investments in power grid expansion and modernization. The country’s strong manufacturing base for electrical equipment, coupled with extensive deployment of renewable energy projects, is driving demand for reliable switching solutions. Continuous upgrades of urban and rural distribution networks are reinforcing market growth.

India Load Break Switch Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rapid electrification, expansion of transmission and distribution infrastructure, and rising industrial power demand. Government initiatives focused on grid reliability, renewable energy integration, and reduction of power losses are increasing adoption of load break switches. Growing investments in smart substations and rural distribution networks are further strengthening market expansion.

Europe Load Break Switch Market Insight

The Europe load break switch market is growing steadily, driven by grid modernization initiatives, high penetration of renewable energy, and stringent safety and reliability standards. Utilities across the region are investing in advanced medium-voltage equipment to enhance network efficiency and reduce downtime. Emphasis on sustainable energy systems and replacement of aging infrastructure is supporting consistent market demand.

Germany Load Break Switch Market Insight

Germany’s load break switch market is supported by its advanced power infrastructure, strong focus on renewable energy integration, and leadership in smart grid technologies. The country’s emphasis on grid stability and efficient power distribution is driving adoption of high-quality switching equipment. Ongoing investments in wind and solar energy projects are further contributing to demand growth.

U.K. Load Break Switch Market Insight

The U.K. market is driven by continuous upgrades to electricity distribution networks and increasing investments in renewable energy capacity. Efforts to improve grid resilience, support decentralized power generation, and enhance safety standards are boosting demand for load break switches. The transition toward smarter and more flexible power networks is reinforcing market development.

North America Load Break Switch Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by large-scale grid modernization programs and rising investments in renewable energy integration. Increasing focus on improving grid reliability, minimizing outages, and supporting distributed energy resources is accelerating adoption. Replacement of aging infrastructure and deployment of smart distribution systems are key growth factors.

U.S. Load Break Switch Market Insight

The U.S. accounted for the largest share in the North America market in 2025, supported by substantial investments in transmission and distribution upgrades. Strong emphasis on grid resilience, renewable energy integration, and advanced power management solutions is driving demand. Presence of major electrical equipment manufacturers and widespread adoption of smart grid technologies further strengthen the country’s leading position.

Load Break Switch Market Share

The load break switch industry is primarily led by well-established companies, including:

- Hyundai Electric & Energy Systems Co., Ltd. (South Korea)

- Lucy Group Ltd. (U.K.)

- GE Grid Solutions (U.S.)

- Safvolt Switchgears Private Limited (India)

- ABB Ltd. (Switzerland)

- ORMAZABAL (Velatia) (Spain)

- Rockwell Automation, Inc. (U.S.)

- Fuji Electric FA Components & Systems Co., Ltd. (Japan)

- KATKO Oy (Finland)

- Schneider Electric SE (France)

- NOJA Power Switchgear Pty Ltd. (Australia)

- Crompton Greaves Power & Industrial Solutions Ltd. (India)

- S&C Electric Company (U.S.)

- Siemens AG (Germany)

- Arteche LBS Division (Spain)

- HUBBELL Power Systems, Inc. (U.S.)

- ENSTO Oy (Finland)

- LARSEN & TOUBRO LIMITED (India)

- Driescher GmbH (Germany)

- SOCOMEC Group S.A. (France)

- G&W Electric Company (U.S.)

- Tavrida Electric AG (Switzerland)

- BRUSH Switchgear (U.K.)

- ENTEC Electric & Electronic Co., Ltd. (South Korea)

- Eaton Corporation plc (Ireland)

Latest Developments in Global Load Break Switch Market

- In January 2025, ABB enhanced its position in the load break switch market by launching an advanced vacuum-based product range tailored for smart and medium-voltage distribution networks. This development supports higher switching efficiency, longer operational life, and reduced environmental impact, aligning with growing utility demand for sustainable and digitally enabled grid infrastructure. The introduction also strengthens ABB’s competitiveness in regions investing heavily in grid modernization and renewable energy integration

- In December 2024, Siemens Energy expanded its manufacturing footprint in Southeast Asia through a new facility focused on air-insulated and gas-insulated load break switches. This expansion improves regional supply chain reliability, reduces lead times, and enables closer alignment with rising demand from urban infrastructure projects and renewable energy installations. The move positions Siemens Energy to better serve fast-growing emerging markets with localized production capabilities

- In November 2024, General Electric formed a joint venture with a Chinese electrical equipment manufacturer to co-develop next-generation load break switches. This partnership accelerates technology development, lowers production costs through localized manufacturing, and enhances GE’s access to the Asia-Pacific market. The collaboration also supports customization of products to meet regional grid standards and expanding distribution network requirements

- In September 2024, Eaton Corporation strengthened its load break switch portfolio by acquiring a smart grid technology firm to integrate digital monitoring, automation, and predictive maintenance features. This strategic move enables Eaton to offer more intelligent switching solutions that improve grid reliability, reduce downtime, and support data-driven asset management for utilities. The acquisition aligns with the increasing shift toward smart grids and digitally connected power distribution systems

- In March 2024, Schneider Electric expanded its production capacity by establishing a new manufacturing facility in India dedicated to load break switches for developing industries. This investment enhances local manufacturing capabilities, supports faster market responsiveness, and reduces dependence on imports. The expansion also reinforces Schneider Electric’s presence in high-growth markets, benefiting from rising industrialization and infrastructure development

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Load Break Switch Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Load Break Switch Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Load Break Switch Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.