Global Long Acting Glp 1 Analogues Market

Market Size in USD Billion

USD

18.42 Billion

USD

39.77 Billion

2025

2033

USD

18.42 Billion

USD

39.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 18.42 Billion | |

| USD 39.77 Billion | |

| % | |

|

Long-Acting GLP-1 Analogues Market Overview

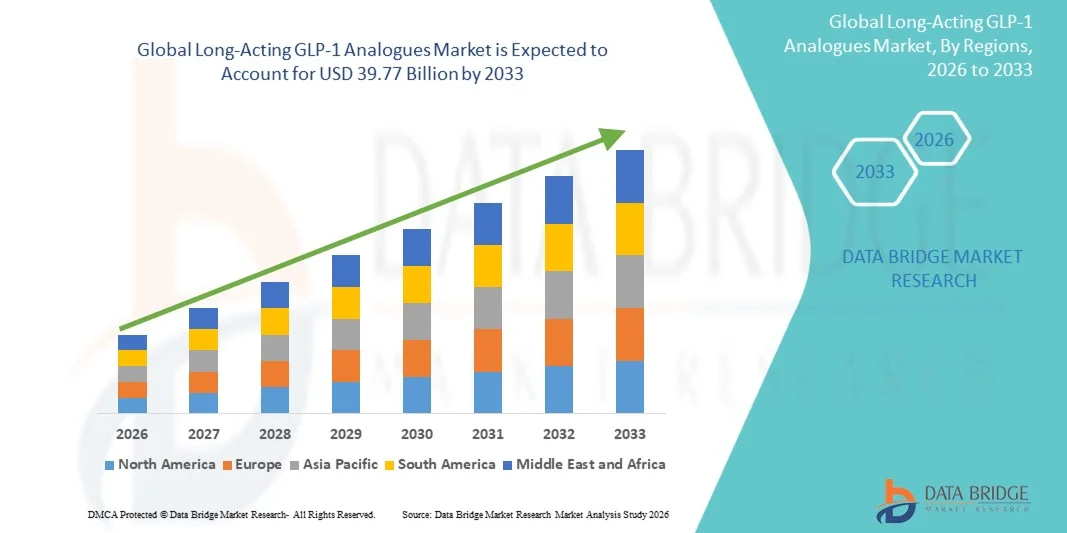

As per Data Bridge Market Research analysis, the long-acting GLP-1 analogues market was valued at USD 18.42 billion in 2025 and is projected to reach USD 39.77 billion by 2033, growing at a CAGR of 10.10% from 2026 to 2033. The market is experiencing consistent growth driven by the rising global prevalence of type 2 diabetes and obesity, increasing adoption of once-weekly GLP-1 receptor agonists, and continuous innovation in long-acting peptide formulations.

The growing demand for therapies that improve glycemic control while enhancing patient adherence, combined with expanding clinical evidence supporting cardiovascular and weight management benefits, is accelerating the adoption of long-acting GLP-1 analogues across healthcare systems. Once-weekly injectable formulations are increasingly replacing daily dosing regimens in many treatment settings, offering improved convenience, sustained therapeutic efficacy, and better long-term disease management for patients with chronic metabolic disorders

Market Size & Forecast

- Global Market Value (2025): USD 18.42 Billion

- Expected Market Value (2033): USD 39.77 Billion

- Forecast CAGR (2026–2033): 10.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the long-acting GLP-1 analogues market with an estimated revenue share of 36.05% in 2025, supported by high obesity and diabetes prevalence, strong healthcare infrastructure, and early adoption of innovative GLP-1 therapies

- The semaglutide segment led the market with a 34.67% share in 2025, driven by its strong clinical efficacy in glycemic control, substantial weight-loss benefits, and proven cardiovascular risk reduction outcomes

- Asia-Pacific is expected to be the fastest-growing region, projected to register a CAGR of 8.4% during the forecast period, fueled by the rising diabetic population, improving healthcare access, and expanding awareness of chronic disease management

- Dulaglutide are the fastest-growing drug type, projected to register a CAGR of 8.3%, reflecting the surge in established cardiovascular benefits, convenient once-weekly administration, and strong adoption among patients seeking simplified treatment regimens

- The diabetes segment dominated the indication category with a 74.50% revenue share in 2025, led by the substantial global prevalence of type 2 diabetes and the established role of long-acting GLP-1 analogues in glycemic management

- Parenteral accounted for 82.30% of the market, preferred by the widespread use of once-weekly injectable GLP-1 analogues such as semaglutide, dulaglutide, and exenatide extended-release formulations

- The oral segment is the fastest-growing route of administration category, with a CAGR of 9.2%, driven by increasing patient preference for non-invasive treatment options and the ongoing development of oral GLP-1 formulations

Report Scope and Long-Acting GLP-1 Analogues Market Segmentation

|

Attributes |

Long-Acting GLP-1 Analogues Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Long-Acting GLP-1 Analogues Market Trends

Trend: Expanding Use of Long-Acting GLP-1 Analogues Beyond Glycemic Control

Long-acting GLP-1 analogues are increasingly being adopted beyond type 2 diabetes management for obesity, cardiovascular risk reduction, and chronic metabolic disease management. Growing clinical evidence supporting sustained weight loss, reduced major adverse cardiovascular events, and improved patient adherence with once-weekly formulations is accelerating physician prescribing and regulatory approvals. Pharmaceutical companies are also expanding oral GLP-1 development pipelines to improve convenience and broaden patient access. For instance, in November 2023, results from the SELECT trial published in the New England Journal of Medicine showed that once-weekly semaglutide 2.4 mg reduced the risk of major adverse cardiovascular events by 20% in adults with overweight or obesity and established cardiovascular disease without diabetes, highlighting the expanding role of long-acting GLP-1 analogues beyond glycemic control into cardiovascular risk reduction.

Expanding therapeutic indications and strong cardiovascular outcome evidence are transforming long-acting GLP-1 analogues into comprehensive metabolic disease therapies rather than diabetes-only treatments.

Long-Acting GLP-1 Analogues Market Dynamics

Key Market Driver: Rising Global Burden of Type 2 Diabetes and Obesity

The increasing prevalence of obesity and type 2 diabetes worldwide continues to drive demand for long-acting GLP-1 analogues that offer effective glycemic control, substantial weight reduction, and cardiovascular protection. Growing clinical guideline recommendations, expanding reimbursement coverage, and increasing physician confidence are further accelerating adoption across developed and emerging healthcare markets. For instance, in January 2024, the World Health Organization (WHO) warned that unprecedented global demand for GLP-1 receptor agonists had resulted in widespread supply shortages and increased reports of falsified products, highlighting the rapidly expanding utilization of these therapies worldwide.

The growing global diabetes and obesity burden, coupled with increasing clinical adoption, remains the primary growth driver for the long-acting GLP-1 analogues market.

Key Restraint/Challenge: Supply Constraints and Limited Accessibility of GLP-1 Therapies

A major challenge for the market is the persistent imbalance between rapidly growing demand and available manufacturing capacity. The widespread adoption of long-acting GLP-1 therapies for both type 2 diabetes and obesity has placed significant pressure on global supply chains, resulting in recurring product shortages across multiple regions. Manufacturing these peptide-based biologics requires highly specialized production facilities, complex formulation processes, stringent quality controls, and substantial capital investment, limiting the ability of manufacturers to rapidly scale output. For instance, June 2024, the World Health Organization (WHO) issued a global warning regarding falsified semaglutide products after sustained shortages of genuine GLP-1 medicines were reported in multiple markets. The WHO noted that unprecedented demand for GLP-1 receptor agonists had outpaced available supply, increasing the risk of counterfeit products entering the market and creating significant patient safety concerns

Expanding production capacity, strengthening supply chain resilience, and improving affordability and reimbursement coverage will be essential for ensuring sustainable market growth and equitable global access to long-acting GLP-1 analogue therapies.

Key Market Opportunity: Development of Next-Generation Oral Long-Acting GLP-1 Therapies

The development of oral long-acting GLP-1 analogues presents a significant market opportunity by improving patient convenience, treatment adherence, and accessibility while reducing dependence on injectable formulations. Continued innovation in peptide delivery technologies and small-molecule GLP-1 receptor agonists is expected to expand the eligible patient population and strengthen market penetration. For instance, in September 2025, Novo Nordisk announced that the Phase 3 OASIS 4 trial demonstrated once-daily oral semaglutide 25 mg produced significantly greater weight loss than placebo in adults with overweight or obesity, supporting the advancement of next-generation oral GLP-1 therapies as a convenient alternative to injectable treatments.

Oral long-acting GLP-1 therapies represent one of the strongest future growth opportunities by addressing convenience, adherence, and broader patient acceptance.

Long-Acting GLP-1 Analogues Market Scope

the long-acting GLP-1 analogues market is segmented on the basis of drug, indication, route of administration, and distribution channel.

- By Drug

On the basis of drug, the market is segmented into semaglutide, exenatide, lixisenatide, liraglutide, dulaglutide, and others. The semaglutide segment dominated the market with a 34.67% share in 2025, driven by its strong clinical efficacy in glycemic control, substantial weight-loss benefits, and proven cardiovascular risk reduction outcomes. Semaglutide-based products have achieved widespread adoption across both diabetes and obesity treatment settings, supported by growing physician confidence and favorable clinical guidelines. The once-weekly dosing schedule improves patient adherence compared with daily injectable alternatives. Expanding regulatory approvals for obesity management have further strengthened market penetration. Increasing reimbursement coverage in developed healthcare markets continues to support prescription growth. Strong commercial performance and extensive clinical evidence maintain Semaglutide’s leadership position within the long-acting GLP-1 analogue market.

The dulaglutide segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by its established cardiovascular benefits, convenient once-weekly administration, and strong adoption among patients seeking simplified treatment regimens. Healthcare providers increasingly prefer Dulaglutide because of its ease of use and demonstrated efficacy in reducing HbA1c levels. Continued expansion of diabetes screening programs is supporting demand among newly diagnosed patients. Growing awareness regarding long-term diabetes management is further contributing to uptake. The drug also benefits from increasing utilization in combination therapy approaches. Ongoing investments in metabolic disease management are expected to sustain segment growth over the coming years.

- By Indication

On the basis of indication, the market is segmented into obesity, diabetes, and others. The diabetes segment dominated the market with a 74.50% share in 2025, owing to the substantial global prevalence of type 2 diabetes and the established role of long-acting GLP-1 analogues in glycemic management. These therapies improve blood glucose control while offering additional benefits such as weight reduction and cardiovascular protection. Increasing adoption of guideline-recommended therapies is driving prescription volumes worldwide. Rising healthcare expenditure and improved access to advanced diabetes treatments are further supporting growth. Healthcare providers increasingly favor GLP-1 analogues for patients requiring long-term disease management. Strong clinical evidence and broad regulatory approvals continue to reinforce the segment’s dominance.

The obesity segment is expected to witness the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing obesity prevalence and expanding regulatory approvals for weight-management indications. Long-acting GLP-1 analogues have demonstrated significant and sustained weight-loss outcomes, making them attractive alternatives to traditional obesity interventions. Growing awareness of obesity as a chronic disease is improving treatment acceptance among healthcare professionals and patients. Increasing demand for non-surgical weight-management solutions is further accelerating adoption. Pharmaceutical companies are actively expanding obesity-focused clinical programs and commercial strategies. Favorable clinical trial outcomes and rising payer interest are expected to support rapid growth in this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The parenteral segment accounted for 82.30% of the market in 2025, supported by the widespread use of once-weekly injectable GLP-1 analogues such as semaglutide, dulaglutide, and exenatide extended-release formulations. Injectable therapies have established efficacy, strong clinical acceptance, and extensive physician familiarity. They provide reliable bioavailability and sustained therapeutic effects, making them the preferred treatment option for many patients. Pharmaceutical companies have invested heavily in improving injection devices to enhance patient convenience and adherence. Strong clinical evidence supporting cardiovascular and metabolic benefits further strengthens demand. Established treatment protocols continue to reinforce the dominance of parenteral administration.

The oral segment is projected to register the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing patient preference for non-invasive treatment options and the ongoing development of oral GLP-1 formulations. Oral therapies eliminate injection-related barriers and improve treatment acceptance among newly diagnosed patients. Advances in drug-delivery technologies have significantly improved the feasibility of oral peptide administration. Growing focus on patient convenience and long-term adherence is accelerating adoption. Pharmaceutical innovation and positive clinical trial outcomes are expanding commercialization opportunities. Increasing availability of oral alternatives is expected to transform treatment patterns and support strong segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the market with a 46.80% share in 2025, owing to the high volume of diabetes and obesity prescriptions initiated within hospital and specialty care settings. Hospitals play a critical role in diagnosis, treatment initiation, patient monitoring, and management of complex metabolic disorders. The availability of specialist physicians and integrated care pathways supports the widespread dispensing of long-acting GLP-1 therapies through hospital channels. Patients with multiple comorbidities often receive treatment through hospital-based healthcare networks. Strong reimbursement frameworks in institutional settings further contribute to segment leadership. Increasing adoption of advanced biologic therapies continues to support growth.

The online pharmacies segment is anticipated to be the fastest-growing distribution channel, registering a CAGR of 10.4% from 2026 to 2033, driven by increasing digital healthcare adoption and growing consumer preference for convenient medication access. Online platforms offer home delivery services, competitive pricing, and improved accessibility for chronic disease patients requiring long-term therapy. The expansion of telemedicine services is further supporting prescription fulfillment through digital channels. Rising internet penetration and smartphone usage are accelerating online pharmacy utilization across emerging markets. Digital health ecosystems are improving patient engagement and medication adherence. Continuous investment in e-pharmacy infrastructure is expected to sustain rapid growth in this segment.

Long-Acting GLP-1 Analogues Market Regional Analysis

North America dominated the long-acting GLP-1 analogues market with an estimated revenue share of 36.05% in 2025, supported by high obesity and diabetes prevalence, strong healthcare infrastructure, and early adoption of innovative GLP-1 therapies. The region benefits from advanced healthcare infrastructure, extensive physician awareness, and the presence of major pharmaceutical companies actively commercializing long-acting GLP-1 products. Growing utilization of GLP-1 analogues for both diabetes management and chronic weight management is further accelerating market expansion. Favorable regulatory approvals, increasing cardiovascular outcome evidence, and strong healthcare spending continue to support demand. Rising investments in next-generation oral GLP-1 formulations and metabolic disease research are also strengthening the region’s leadership position in the global market.

U.S. Long-Acting GLP-1 Analogues Market Insight

The U.S. long-acting GLP-1 analogues market is witnessing strong growth due to the rising prevalence of obesity and type 2 diabetes, favorable reimbursement coverage, and rapid adoption of innovative metabolic therapies. The country benefits from advanced healthcare infrastructure, strong physician awareness, and early access to newly approved GLP-1 products. Increasing utilization of semaglutide and other long-acting GLP-1 therapies for both diabetes and chronic weight management is significantly driving demand. In addition, expanding clinical evidence supporting cardiovascular and renal benefits is encouraging broader prescribing across patient populations. In March 2024, the U.S. FDA approved Wegovy (semaglutide) to reduce the risk of major adverse cardiovascular events in adults with cardiovascular disease and obesity or overweight, expanding the therapeutic scope of GLP-1 analogues beyond weight management.

Europe Long-Acting GLP-1 Analogues Market Insight

The Europe long-acting GLP-1 analogues market remains a major contributor to global revenue, driven by increasing obesity prevalence, favorable healthcare reimbursement systems, and strong adoption of evidence-based diabetes treatments. The region benefits from established healthcare infrastructure, growing awareness of chronic metabolic diseases, and increasing physician confidence in GLP-1 therapies. Expanding use of these therapies for obesity and cardiovascular risk reduction is supporting market growth across several European countries. Continuous investments in diabetes management programs and preventive healthcare initiatives are further strengthening market expansion. In May 2026, the European Medicines Agency Committee for Medicinal Products for Human Use (CHMP) recommended an extension of the marketing authorization for Wegovy (semaglutide) tablets for weight management in adults with obesity or overweight and at least one weight-related comorbidity. The recommendation marked the first oral GLP-1 receptor agonist for weight management to receive a positive CHMP opinion, expanding treatment options beyond injectable formulations.

U.K. Long-Acting GLP-1 Analogues Market Insight

The U.K. long-acting GLP-1 analogues market is experiencing steady growth, supported by increasing obesity rates, growing NHS focus on preventive healthcare, and expanding access to innovative weight-management therapies. Rising awareness regarding obesity as a chronic disease and increasing adoption of guideline-recommended treatments are contributing to market expansion. The country's strong clinical research ecosystem and active participation in obesity management programs further support growth. In addition, increasing demand for effective long-term metabolic disease therapies is accelerating product uptake. The National Institute for Health and Care Excellence (NICE) expanded recommendations supporting the use of GLP-1-based obesity treatments for eligible patients within structured weight-management pathways.

Germany Long-Acting GLP-1 Analogues Market Insight

The Germany long-acting GLP-1 analogues market is expanding steadily due to the country's large diabetic population, advanced healthcare system, and strong adoption of innovative pharmaceutical therapies. Healthcare providers are increasingly prescribing long-acting GLP-1 analogues because of their proven efficacy in glycemic control, weight reduction, and cardiovascular risk management. Growing awareness regarding obesity-related complications and increasing emphasis on preventive care are further supporting market growth. Continuous clinical research and strong reimbursement mechanisms continue to enhance treatment accessibility throughout Germany. Germany remains one of Europe's largest diabetes markets, with approximately 8.5 million adults living with diabetes according to the International Diabetes Federation (IDF), creating substantial demand for advanced diabetes therapies such as long-acting GLP-1 analogues.

Asia-Pacific Long-Acting GLP-1 Analogues Market Insight

The Asia-Pacific long-acting GLP-1 analogues market is expected to witness rapid growth, driven by the increasing prevalence of obesity and type 2 diabetes, improving healthcare access, and expanding awareness of chronic disease management across countries such as China, India, Japan, and South Korea. Growing healthcare expenditure, rising adoption of advanced diabetes therapies, and expanding pharmaceutical distribution networks are supporting regional market expansion. In addition, government initiatives focused on non-communicable disease prevention are accelerating demand for innovative metabolic therapies throughout the region. The International Diabetes Federation estimates that the Western Pacific region accounted for more than 215 million adults living with diabetes, representing the largest regional diabetes burden globally and creating significant demand for GLP-1 therapies.

Japan Long-Acting GLP-1 Analogues Market Insight

The Japan long-acting GLP-1 analogues market is witnessing consistent growth due to increasing prevalence of metabolic disorders, rising adoption of innovative diabetes treatments, and strong healthcare infrastructure. Healthcare providers are increasingly incorporating GLP-1 analogues into treatment regimens because of their ability to improve glycemic control while supporting weight management. Growing demand for therapies that reduce cardiovascular risk is also supporting adoption. Furthermore, Japan's strong pharmaceutical innovation ecosystem continues to facilitate access to next-generation GLP-1 therapies. Japan was among the earliest major markets to adopt oral semaglutide and advanced GLP-1 therapies, supported by a large aging population and increasing focus on chronic disease management.

China Long-Acting GLP-1 Analogues Market Insight

The China long-acting GLP-1 analogues market is growing rapidly, driven by increasing obesity prevalence, a large diabetic population, expanding healthcare coverage, and rising awareness of advanced metabolic disease treatments. Growing adoption of innovative biologic therapies, improving healthcare infrastructure, and increasing government efforts to address chronic diseases are significantly boosting demand. In addition, rapid expansion of pharmaceutical manufacturing capabilities and growing investment in diabetes management programs are positioning China as one of the fastest-growing markets globally. China has the world's largest diabetes population, with approximately 148 million adults living with diabetes according to the International Diabetes Federation, creating substantial demand for long-acting GLP-1 therapies and obesity-management solutions.

Long-Acting GLP-1 Analogues Market Share

The long-acting GLP-1 analogues industry is primarily led by well-established companies, including:

- Novo Nordisk A/S (Denmark)

- Eli Lilly and Company (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Boehringer Ingelheim International GmbH (Germany)

- Bayer AG (Germany)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Viatris Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Astellas Pharma Inc. (Japan)

- Hanmi Pharm.Co.,Ltd. (South Korea)

- Alnylam Pharmaceuticals, Inc. (U.S.)

Latest Developments in Long-Acting GLP-1 Analogues Market

- In March 2024, the U.S. Food and Drug Administration (FDA) approved an expanded indication for Wegovy (semaglutide 2.4 mg injection) to reduce the risk of cardiovascular death, heart attack, and stroke in adults with cardiovascular disease and either obesity or overweight. This approval marked a major advancement for long-acting GLP-1 analogues by expanding their role beyond weight management into cardiovascular risk reduction

- In November 2023, Eli Lilly and Company received U.S. FDA approval for Zepbound (tirzepatide injection) for chronic weight management in adults with obesity or overweight with weight-related medical conditions. The approval introduced a new long-acting incretin-based therapy activating both GIP and GLP-1 receptors, expanding treatment options for obesity management and increasing competition within the GLP-1 therapy landscape

- In May 2022, Eli Lilly announced the U.S. FDA approval of Mounjaro (tirzepatide) injection, the first once-weekly GIP and GLP-1 receptor agonist approved to improve blood sugar control in adults with type 2 diabetes. The approval was based on results from the SURPASS clinical trial program, which demonstrated significant HbA1c reductions and weight reduction benefits, strengthening the adoption of long-acting incretin-based therapies and expanding competition within the GLP-1 analogue market

- In June 2021, the U.S. Food and Drug Administration (FDA) approved Wegovy (semaglutide 2.4 mg once weekly injection) for chronic weight management in adults with obesity or overweight with at least one weight-related condition. The approval represented a significant milestone as Wegovy became the first FDA-approved treatment for chronic weight management in adults since 2014, strengthening the adoption of long-acting GLP-1 analogues in obesity care

- In August 2021, results from the STEP 1 clinical trial of once-weekly semaglutide 2.4 mg were published in the New England Journal of Medicine, showing substantial weight reduction in adults with overweight or obesity without diabetes. The clinical evidence strengthened the role of long-acting GLP-1 receptor agonists as effective pharmacological options for chronic weight management and accelerated broader acceptance of GLP-1-based obesity therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.