Global Lubricity Improvers Market

Market Size in USD Billion

USD

2.68 Billion

USD

3.95 Billion

2024

2032

USD

2.68 Billion

USD

3.95 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.68 Billion | |

| USD 3.95 Billion | |

| % | |

|

What is the Global Lubricity Improvers Market Size and Growth Rate?

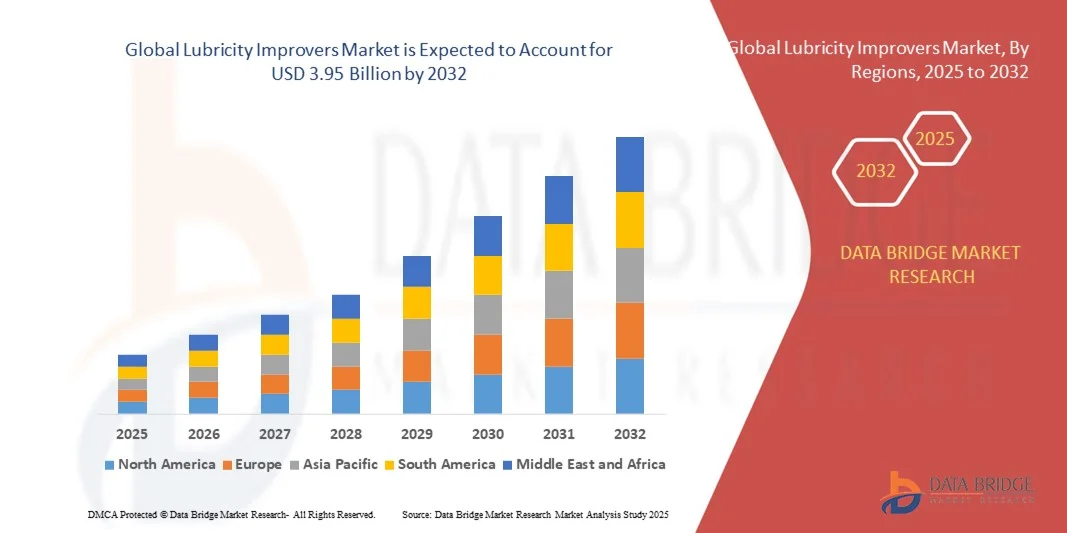

- The global lubricity improvers market size was valued at USD 2.68 billion in 2024 and is expected to reach USD 3.95 billion by 2032, at a CAGR of 5.00% during the forecast period

- The implementation of stringent environmental norms acts as one of the major factors driving the growth of lubricity improvers market. The continuous advancements in vehicle hardware and improvements in the materials used in critical areas, and stringent regulations keeping check of quality of diesel fuel in order to ensure the fuel used is good accelerate the market growth. The increase in usage of complex fuels and increased usage of these products in order to decline the maintenance cost of various other equipment further influence the market

What are the Major Takeaways of Lubricity Improvers Market?

- Research and development activities, rapid industrialization, and expansion of various end use industries positively affect the lubricity improvers market. Furthermore, rise in the use of biofuels and highly paraffinic diesel extends profitable opportunities to the market players

- On the other hand, complications in the production process of these products requiring extra care and precautionary measures are expected to obstruct the market growth. The negative impact of COVID-19 on various industries is projected to challenge the lubricity improvers market

- Europe dominated the lubricity improvers market with the largest revenue share of 39.4% in 2024, driven by the region’s robust automotive manufacturing base and stringent fuel quality standards

- The Asia-Pacific lubricity improvers market is poised to grow at the fastest CAGR of 10.98% from 2025 to 2032, driven by rapid industrialization, expanding automotive production, and rising energy demand across China, India, and Japan

- The Non-Acidic lubricity improver segment dominated the market with the largest revenue share of 64.5% in 2024, primarily driven by its superior corrosion resistance, environmental compatibility, and longer shelf life

Report Scope and Lubricity Improvers Market Segmentation

|

Attributes |

Lubricity Improvers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Lubricity Improvers Market?

Rising Focus on Sustainable and Bio-Based Additives

- A significant trend in the global lubricity improvers market is the increasing shift toward eco-friendly and bio-based formulations that reduce environmental impact while maintaining or improving performance. Companies are developing additives derived from renewable feedstocks to meet stricter emission norms and sustainability targets

- For example, BASF SE launched its renewable-based bio-lubricity additive designed to enhance fuel efficiency and lower carbon emissions without compromising engine protection. Similarly, TotalEnergies SE

- is investing in green chemistry initiatives to expand its low-sulfur, biodegradable lubricity improver portfolio

- This movement toward sustainable chemistry is supported by global regulatory pressure such as the EU Green Deal and increasing consumer demand for environmentally safe fuel additives

- The growing adoption of bio-based lubricity improvers represents a major step toward cleaner fuel solutions, aligning the market with the global transition to carbon neutrality and sustainable industrial practices

What are the Key Drivers of Lubricity Improvers Market?

- The increasing production of ultra-low sulfur diesel (ULSD) is one of the major drivers of the Lubricity Improvers market, as desulfurization processes remove natural lubricity from fuels. To prevent engine wear, refiners rely on effective lubricity additives to maintain performance.

- For instance, in February 2024, Chevron Corporation expanded its lubricant additive line to include high-performance lubricity improvers optimized for cleaner-burning fuels. Similarly, Afton Chemical Corporation launched new fuel additives aimed at protecting critical components in low-sulfur diesel engines

- Other key growth factors include the rising demand for high-performance diesel and aviation fuels, expanding vehicle fleets, and stringent environmental standards regulating emissions and fuel quality

- The market is further propelled by industrialization in emerging economies, where fuel quality upgrades are becoming mandatory. Together, these factors are significantly boosting the demand for effective lubricity improvers across global refineries and fuel distributors

Which Factor is Challenging the Growth of the Lubricity Improvers Market?

- One of the major challenges facing the lubricity improvers market is the volatile prices of raw materials, particularly fatty acids and esters derived from petroleum or vegetable sources. These fluctuations directly affect production costs and profit margins for manufacturers

- For example, in 2024, rising global oil prices caused by geopolitical tensions and supply disruptions led to increased costs of feedstocks such as oleic acid, heavily used in lubricity improvers

- Furthermore, compatibility issues with modern fuel formulations and limited availability of sustainable raw materials can hinder product performance consistency. Compliance with evolving fuel standards also requires ongoing R&D investment

- Manufacturers are addressing these challenges by adopting cost-efficient production technologies and exploring alternative feedstocks, such as waste oils and synthetic esters. Overcoming these obstacles will be key to ensuring the long-term stability and scalability of the lubricity improvers industry

How is the Lubricity Improvers Market Segmented?

The market is segmented on the basis of product, ingredient, application, and end-use industry.

- By Product

On the basis of product, the lubricity improvers market is segmented into Acidic Lubricity Improver and Non-Acidic Lubricity Improver. The Non-Acidic Lubricity Improver segment dominated the market with the largest revenue share of 64.5% in 2024, primarily driven by its superior corrosion resistance, environmental compatibility, and longer shelf life. These additives are widely preferred in fuel blending for automotive and industrial applications as they maintain metal surface integrity and reduce engine wear.

The Acidic Lubricity Improver segment is projected to record the fastest CAGR from 2025 to 2032, supported by its cost-effectiveness and strong lubricity performance at low treat rates. Increasing use in developing regions where refining infrastructures are evolving also supports demand. Rising research on eco-friendly acidic derivatives is expected to expand its adoption in biofuel formulations over the forecast period.

- By Ingredient

Based on ingredient, the market is segmented into Xylene, Methanol, Ethanol, Acetone, and Others. The Ethanol segment dominated the Lubricity Improvers Market with a market revenue share of 38.6% in 2024, owing to its renewable origin, easy availability, and ability to enhance lubricity in low-sulfur fuels. Ethanol’s growing use in biofuel blending programs across the U.S., Brazil, and India further strengthens its dominance.

The Methanol segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its increasing use as a clean-burning alternative fuel and solvent in lubricant formulations. Its cost efficiency and ability to reduce carbon emissions make it a favorable choice for refinery and transportation fuel applications. Growing investments in methanol-to-fuel technologies are such asly to enhance its penetration in the coming years.

- By Fuel Type

On the basis of fuel type, the market is segmented into Gasoline Fuel, Diesel Fuel, Aviation Fuel, and Others. The Diesel Fuel segment held the largest revenue share of 46.9% in 2024, attributed to the widespread global use of diesel engines in commercial transport, agriculture, and industrial machinery. Lubricity improvers are essential for ultra-low sulfur diesel (ULSD) to prevent pump and injector wear, ensuring engine efficiency.

The Aviation Fuel segment is projected to grow at the fastest CAGR from 2025 to 2032, driven by the rising demand for cleaner aviation fuels and the adoption of sustainable aviation fuel (SAF) blends. Continuous research to improve fuel lubricity under extreme temperature conditions enhances market growth potential in this segment.

- By End-Use Industry

Based on end-use industry, the market is segmented into Automotive, Agriculture, and Manufacturing. The Automotive segment dominated the Lubricity Improvers Market with a revenue share of 57.3% in 2024, fueled by the extensive use of lubricity additives in vehicle fuels and lubricants to minimize engine friction and wear. Increasing vehicle production and demand for efficient engines continue to drive this segment.

The Manufacturing segment is anticipated to witness the fastest CAGR from 2025 to 2032, driven by the growing requirement for high-performance lubricants in industrial machinery and equipment. The need to enhance operational efficiency, reduce downtime, and comply with emission norms encourages the use of advanced lubricity improvers in industrial lubricants and hydraulic fluids.

Which Region Holds the Largest Share of the Lubricity Improvers Market?

- Europe dominated the lubricity improvers market with the largest revenue share of 39.4% in 2024, driven by the region’s robust automotive manufacturing base and stringent fuel quality standards

- The European refining industry continues to adopt lubricity improvers to comply with environmental regulations, such as REACH and Euro VI emission norms. Growing awareness of fuel efficiency and sustainable additives is also propelling demand across diesel and biofuel applications

- The presence of leading chemical companies, continuous R&D investment, and the rising shift toward low-sulfur fuels further support market expansion. The integration of eco-friendly lubricity enhancers in automotive and industrial sectors positions Europe as the global leader in lubricity improvement solutions

Germany Lubricity Improvers Market Insight

The Germany lubricity improvers market held the largest share within Europe in 2024, accounting for 31% of regional revenue, supported by its strong automotive and industrial base. The country’s focus on energy-efficient manufacturing and emission control policies has driven the demand for fuel additives that extend engine life and improve combustion. Continuous innovation in refining technology and increasing use of ultra-low sulfur diesel (ULSD) contribute significantly to growth. In addition, German consumers’ growing preference for cleaner fuel options and sustainability-driven corporate strategies are encouraging the adoption of bio-based lubricity improvers. The ongoing shift toward renewable energy and green fuels further accelerates market development in the country.

U.K. Lubricity Improvers Market Insight

The U.K. lubricity improvers market is projected to expand steadily throughout the forecast period, driven by the increasing emphasis on reducing vehicle emissions and enhancing engine performance. With the government promoting low-emission vehicles and alternative fuels, the demand for high-performance fuel additives has risen sharply. The refining and automotive industries are investing in cleaner lubricity-enhancing solutions to meet carbon reduction goals. Moreover, the rise of hybrid and electric vehicle technologies has stimulated R&D in next-generation additives suitable for diverse fuel formulations. Growing awareness of maintenance efficiency and operational cost reduction is expected to sustain demand in both transportation and industrial sectors.

France Lubricity Improvers Market Insight

The France lubricity improvers market is expected to experience significant growth during the forecast period, propelled by the nation’s commitment to cleaner energy and renewable fuel adoption. France’s ongoing transition toward biofuels and the modernization of refinery operations are creating strong opportunities for lubricity additive manufacturers. Government-backed sustainability programs and rising adoption of biodiesel blends in transportation are major contributors to market expansion. In addition, collaborations between French energy companies and chemical producers are accelerating product innovations focused on reducing friction and wear in engines. The preference for environmentally safe, non-acidic lubricity improvers continues to strengthen the country’s market position within Europe.

Which Region is the Fastest-Growing in the Lubricity Improvers Market?

The Asia-Pacific lubricity improvers market is poised to grow at the fastest CAGR of 10.98% from 2025 to 2032, driven by rapid industrialization, expanding automotive production, and rising energy demand across China, India, and Japan. The region’s push toward cleaner fuels, coupled with government initiatives supporting biofuel adoption, is fostering significant demand for lubricity-enhancing additives. Increasing refinery modernization projects and the growing penetration of ultra-low sulfur fuels are also key growth enablers. The expansion of local manufacturing capabilities and cost-efficient additive production make APAC a global hub for lubricity improvers, offering affordable and scalable solutions to emerging economies.

China Lubricity Improvers Market Insight

The China lubricity improvers market dominated the Asia-Pacific region in 2024, capturing 44% of regional revenue, fueled by its strong refining sector and rising demand for high-quality diesel and gasoline fuels. The government’s efforts to reduce emissions and improve fuel quality have accelerated the adoption of lubricity enhancers in transportation and industrial applications. Domestic chemical manufacturers are expanding production capacity to meet both local and export demand. The increasing integration of lubricity additives in biofuel and synthetic fuel blends further supports market growth. China’s growing automotive sector and stringent fuel regulations position it as a key driver in the regional landscape.

India Lubricity Improvers Market Insight

The India lubricity improvers market is projected to grow at the fastest CAGR within Asia-Pacific, driven by the rapid shift toward low-sulfur fuels and the expanding automobile and agricultural machinery sectors. The government’s promotion of biodiesel and ethanol-blended fuels is spurring the demand for effective lubricity additives to ensure engine reliability. Rising infrastructure investments, coupled with urbanization, are boosting fuel consumption, thereby elevating additive requirements. Moreover, collaborations between global additive producers and domestic refiners are enhancing technology transfer and product availability. The growing emphasis on cost-effective, eco-friendly lubricity solutions is expected to propel sustained market growth across India.

Which are the Top Companies in Lubricity Improvers Market?

The lubricity improvers industry is primarily led by well-established companies, including:

- Afton Chemical Corporation (U.S.)

- Dow (U.S.)

- TotalEnergies SE (France)

- BASF SE (Germany)

- The Lubrizol Corporation (U.S.)

- Innospec Inc. (U.S.)

- Chevron Corporation (U.S.)

- Acpaegypt Inc. (Egypt)

- Huntsman International LLC (U.S.)

- Fuel Additive Science Technologies Limited (U.K.)

- Baker Hughes, a GE Company LLC (U.S.)

- Ecolab Inc. (U.S.)

- Dorfketal Chemicals (I) Pvt. Ltd. (India)

- SI Group, Inc. (U.S.)

- Infineum International Limited (U.K.)

- Abhitech Energycon Ltd. (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Lubricity Improvers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Lubricity Improvers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Lubricity Improvers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.