Global Lung Cancer Surgery Market

Market Size in USD Billion

CAGR :

%

USD

1.55 Billion

USD

2.37 Billion

2025

2033

USD

1.55 Billion

USD

2.37 Billion

2025

2033

| 2026 –2033 | |

| USD 1.55 Billion | |

| USD 2.37 Billion | |

| % | |

|

Lung Cancer Surgery Market Size

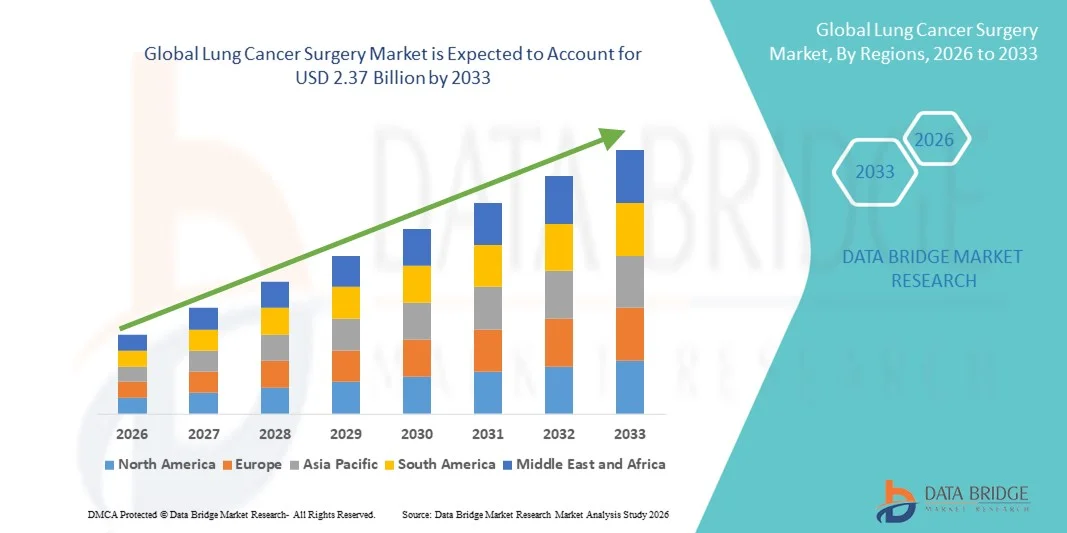

- The global lung cancer surgery market size was valued at USD 1.55 billion in 2025 and is expected to reach USD 2.37 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of lung cancer and the rising demand for advanced surgical interventions, leading to greater adoption of innovative surgical procedures in hospitals and specialized oncology centers

- Furthermore, growing advancements in minimally invasive surgical techniques and increasing healthcare investments are establishing lung cancer surgery as a critical component of modern cancer treatment. These converging factors are accelerating the uptake of Lung Cancer Surgery solutions, thereby significantly boosting the industry's growth

Lung Cancer Surgery Market Analysis

- Lung cancer surgery, involving advanced surgical procedures for the removal of cancerous lung tissues, is increasingly vital in modern oncology treatment across hospitals and specialized cancer centers due to improved surgical precision, better patient outcomes, and advancements in minimally invasive techniques

- The escalating demand for lung cancer surgery is primarily fueled by the rising global prevalence of lung cancer, increasing adoption of early diagnostic screening, and growing preference for minimally invasive surgical approaches such as video-assisted thoracoscopic surgery (VATS) and robotic-assisted surgery

- North America dominated the lung cancer surgery market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative surgical technologies, and a strong presence of leading medical device manufacturers and oncology treatment centers in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the lung cancer surgery market during the forecast period with a projected CAGR of 9.6%, due to increasing lung cancer incidence, expanding healthcare infrastructure, and rising healthcare investments in countries such as China, India, and Japan

- The male segment dominated the largest market revenue share of 58.4% in 2025, primarily due to the higher prevalence of lung cancer among men globally

Report Scope and Lung Cancer Surgery Market Segmentation

|

Attributes |

Lung Cancer Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Lung Cancer Surgery Market Trends

Growing Adoption of Minimally Invasive Surgical Techniques

- A significant and accelerating trend in the global lung cancer surgery market is the growing adoption of minimally invasive surgical techniques aimed at improving patient outcomes and reducing recovery time. Procedures such as video-assisted thoracoscopic surgery (VATS) and robotic-assisted thoracic surgery are increasingly being adopted by healthcare providers as they allow surgeons to perform complex lung cancer procedures with greater precision and smaller incisions. These techniques help reduce postoperative complications, shorten hospital stays, and enhance overall patient recovery

- For instance, several leading hospitals and cancer treatment centers are increasingly utilizing robotic-assisted thoracic surgery systems to perform lung cancer resections with improved accuracy and control. These advanced systems enable surgeons to operate with enhanced visualization and precision, resulting in improved surgical outcomes and reduced trauma to surrounding tissues

- The increasing focus on early detection and timely surgical intervention is also contributing to the growing demand for lung cancer surgeries. As screening programs and diagnostic technologies improve globally, more lung cancer cases are being diagnosed at earlier stages, when surgical treatment remains the most effective option

- Furthermore, technological advancements in surgical instruments and imaging systems are enhancing the efficiency and safety of lung cancer surgeries. Modern surgical tools allow surgeons to perform procedures with higher precision, minimizing damage to healthy tissues and improving the success rate of surgical treatments

- The expansion of specialized oncology centers and thoracic surgery departments in hospitals is also supporting the increasing adoption of advanced surgical techniques for lung cancer treatment

- As healthcare systems continue to prioritize improved surgical outcomes and patient-centered care, the demand for innovative surgical technologies and minimally invasive procedures is expected to grow significantly in the global Lung Cancer Surgery market

Lung Cancer Surgery Market Dynamics

Driver

Rising Global Incidence of Lung Cancer and Advancements in Surgical Care

- The rising global prevalence of lung cancer is one of the major drivers fueling the growth of the Lung Cancer Surgery market. Lung cancer remains one of the most commonly diagnosed cancers worldwide, leading to a growing demand for effective treatment options, including surgical intervention

- For instance, healthcare institutions across regions such as North America, Europe, and Asia-Pacific are expanding their thoracic surgery departments to manage the increasing number of lung cancer patients requiring surgical treatment. These expansions are helping improve patient access to specialized surgical procedures and advanced treatment facilities

- The growing adoption of early cancer screening programs is also increasing the number of lung cancer cases diagnosed at earlier stages, where surgery remains the most effective treatment option. Early detection significantly improves survival rates and encourages healthcare providers to recommend surgical removal of cancerous tissue

- In addition, continuous advancements in surgical equipment and operating room technologies are improving the efficiency and safety of lung cancer procedures. Modern surgical tools allow surgeons to perform more precise tumor resections while minimizing complications

- The increasing availability of skilled thoracic surgeons and specialized oncology hospitals across both developed and emerging economies is also contributing to the growth of the lung cancer surgery market

- Furthermore, rising healthcare investments and the expansion of cancer treatment infrastructure are enabling hospitals to adopt advanced surgical technologies that support improved patient outcomes

Restraint/Challenge

High Treatment Costs and Surgical Risks

- Despite significant advancements in surgical techniques, the high cost associated with lung cancer surgery remains a major challenge for market growth. Surgical procedures often require advanced equipment, specialized surgical teams, and extended postoperative care, which can increase the overall cost of treatment for patients and healthcare providers

- For instance, complex procedures such as robotic-assisted thoracic surgery require expensive surgical systems and highly trained medical professionals, making them less accessible in certain healthcare facilities, particularly in developing regions

- In addition, lung cancer surgery carries inherent clinical risks, including postoperative complications such as infections, bleeding, or respiratory difficulties. These risks may limit surgical eligibility for certain patients, particularly elderly individuals or those with advanced-stage disease

- Limited access to specialized thoracic surgery centers in some regions can also delay treatment for lung cancer patients, affecting overall patient outcomes

- Furthermore, the shortage of trained thoracic surgeons and oncology specialists in certain healthcare systems can restrict the availability of advanced surgical procedures

- Addressing these challenges through improved healthcare infrastructure, expanded surgical training programs, and the development of cost-effective surgical technologies will be essential for sustaining long-term growth in the global lung cancer surgery market

Lung Cancer Surgery Market Scope

The market is segmented on the basis of product type, surgical procedure, patient type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Lung Cancer Surgery market is segmented into surgical instruments, monitoring & visualizing system, endosurgical equipment, robotic-assisted thoracic surgery systems, and others. The surgical instruments segment dominated the largest market revenue share of 38.6% in 2025, due to the essential role of surgical tools such as forceps, retractors, staplers, and electrosurgical devices in lung cancer procedures. Hospitals and cancer treatment centers rely heavily on these instruments for performing tumor resections, biopsies, and other thoracic surgeries. The increasing number of lung cancer cases worldwide has significantly increased the demand for high-precision surgical tools. Healthcare facilities prefer advanced surgical instruments that improve procedural accuracy and reduce complications during operations. The availability of technologically advanced instruments and continuous product upgrades also support strong market demand. In addition, rising healthcare investments and expansion of surgical infrastructure across developing countries contribute to higher adoption. Surgical instruments are widely used across both open and minimally invasive surgeries, strengthening their market presence. Surgeons prioritize reliable and durable instruments to ensure successful outcomes in complex thoracic procedures. Furthermore, frequent replacement cycles of surgical instruments in hospitals create recurring demand. The presence of major medical device manufacturers continuously launching improved products also reinforces this segment’s dominance. As a result, surgical instruments remain the most widely used product category in lung cancer surgery.

The robotic-assisted thoracic surgery systems segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by the increasing adoption of robotic technologies in cancer surgery. Robotic systems enable surgeons to perform highly precise and minimally invasive procedures with improved visualization and dexterity. Hospitals are investing in robotic surgical platforms to enhance surgical accuracy and patient outcomes. These systems allow surgeons to operate with greater control and precision in delicate lung tissues. Patients undergoing robotic-assisted surgery often experience shorter hospital stays and faster recovery times. The growing demand for minimally invasive procedures further accelerates adoption of robotic systems in thoracic surgery. In addition, advancements in 3D imaging and robotic instrumentation support better surgical planning and execution. Healthcare institutions are also adopting robotic systems to strengthen their advanced surgical capabilities. Training programs for robotic surgery are increasing among thoracic surgeons worldwide. The rising number of cancer centers equipped with robotic platforms further supports market growth. Increasing healthcare expenditure and technological innovation are expected to boost adoption during the forecast period. Consequently, robotic-assisted systems are anticipated to be the fastest-growing segment in the lung cancer surgery market.

- By Surgical Procedure

On the basis of surgical procedure, the Lung Cancer Surgery market is segmented into thoracotomy and minimally invasive surgery. The thoracotomy segment dominated the largest market revenue share of 55.1% in 2025, owing to its long-established use in traditional lung cancer surgeries. Thoracotomy involves making a larger incision in the chest to access the lungs and remove tumors, which allows surgeons to directly visualize the affected area. This procedure is often preferred for advanced or complex lung cancer cases requiring extensive surgical access. Hospitals frequently rely on thoracotomy for large tumor resections and complicated thoracic operations. The technique is widely practiced in many healthcare facilities due to the familiarity of surgeons with the procedure. In regions with limited access to advanced surgical technologies, thoracotomy remains the primary treatment option. In addition, the increasing number of advanced-stage lung cancer diagnoses contributes to the demand for this procedure. Surgeons often prefer thoracotomy when complete tumor removal requires wider exposure. The availability of experienced thoracic surgeons further supports the segment’s strong presence. Clinical guidelines in several cases still recommend thoracotomy for certain lung cancer conditions. Furthermore, hospitals performing complex lung surgeries continue to depend on this established method. As a result, thoracotomy continues to hold the largest share in the lung cancer surgery market.

The minimally invasive surgery segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by the growing preference for advanced surgical techniques with smaller incisions. Procedures such as video-assisted thoracoscopic surgery (VATS) allow surgeons to remove tumors with minimal disruption to surrounding tissues. Patients undergoing minimally invasive surgery typically experience less pain and faster recovery compared to traditional open procedures. Hospitals are increasingly adopting these techniques to improve surgical outcomes and reduce hospitalization time. Technological advancements in imaging systems and surgical instruments have significantly improved the safety and efficiency of minimally invasive procedures. Surgeons are receiving specialized training to perform these advanced techniques more effectively. In addition, the rising awareness about early cancer detection supports the use of minimally invasive surgeries. Healthcare providers aim to reduce postoperative complications by using less invasive treatment methods. Many cancer centers are investing in advanced thoracoscopic and robotic equipment to expand surgical capabilities. The growing demand for improved patient comfort and faster recovery further supports this segment’s expansion. Increasing healthcare investments in advanced surgical technologies also contribute to adoption. Consequently, minimally invasive surgery is projected to experience the fastest growth during the forecast period.

- By Patient Type

On the basis of patient type, the Lung Cancer Surgery market is segmented into male and female. The male segment dominated the largest market revenue share of 58.4% in 2025, primarily due to the higher prevalence of lung cancer among men globally. Historically, smoking rates have been significantly higher among male populations, which has contributed to increased lung cancer incidence. Occupational exposure to harmful substances such as asbestos and industrial pollutants also raises lung cancer risk among men. Healthcare statistics consistently show higher diagnosis and treatment rates for male patients. Hospitals frequently perform lung cancer surgeries on male patients because of the larger patient population. Government cancer screening programs also focus heavily on high-risk male populations. Increased awareness campaigns regarding early detection further contribute to higher surgical treatment rates among men. The availability of specialized thoracic surgery units supports treatment access for male patients. In addition, clinical research and treatment guidelines often address the higher incidence of lung cancer among men. Surgeons regularly perform tumor resections and other thoracic procedures for male patients diagnosed with early-stage cancer. Growing healthcare infrastructure also improves access to surgical treatment. As a result, the male segment remains the dominant patient category in the lung cancer surgery market.

The female segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by the rising incidence of lung cancer among women. Changing lifestyle habits, including increasing smoking rates in certain regions, have contributed to the growing number of female lung cancer cases. Environmental factors such as air pollution and secondhand smoke exposure also increase risk among women. Healthcare awareness programs encourage early diagnosis and screening among female populations. Early detection improves the chances of surgical treatment for lung cancer patients. Hospitals and cancer centers are increasingly focusing on gender-specific treatment strategies. Improved diagnostic technologies allow doctors to identify lung cancer in women at earlier stages. In addition, expanding healthcare infrastructure improves surgical access for female patients worldwide. Awareness campaigns highlighting lung cancer risks among women also contribute to rising treatment rates. Advancements in minimally invasive procedures make surgery more acceptable and accessible for female patients. Medical research focused on women’s lung cancer treatment is also expanding. These factors collectively support the rapid growth of the female segment in the coming years.

- By End User

On the basis of end user, the Lung Cancer Surgery market is segmented into hospitals, ambulatory surgical centres, academic & research laboratories, speciality cancer care centres, and others. The hospitals segment dominated the largest market revenue share of 46.7% in 2025, driven by the availability of advanced surgical infrastructure and specialized thoracic surgeons. Hospitals serve as primary treatment centers for lung cancer diagnosis and surgical procedures. They are equipped with operating rooms, intensive care units, and comprehensive oncology departments. Patients undergoing lung cancer surgery often require extensive preoperative evaluation and postoperative monitoring, which hospitals can provide. Large hospitals also invest heavily in advanced surgical technologies, including robotic systems and imaging equipment. The presence of multidisciplinary medical teams ensures comprehensive patient care. Hospitals perform a high volume of lung cancer surgeries due to referrals from smaller clinics and healthcare providers. Government funding and healthcare infrastructure development further strengthen hospital capabilities. Insurance coverage and reimbursement policies often support hospital-based procedures. In addition, hospitals participate in clinical research and advanced treatment programs. The availability of experienced surgeons and specialized facilities reinforces their dominance. Consequently, hospitals remain the leading end-user segment in the lung cancer surgery market.

The speciality cancer care centres segment is expected to witness the fastest CAGR of 8.2% from 2026 to 2033, driven by the increasing demand for specialized oncology treatment facilities. These centers focus exclusively on cancer diagnosis, treatment, and research. Patients often prefer specialized centers due to the availability of expert oncologists and advanced treatment technologies. Many cancer care centers are equipped with advanced surgical systems and precision diagnostic tools. These facilities emphasize personalized treatment plans and multidisciplinary care approaches. Governments and private healthcare providers are investing in the expansion of dedicated cancer hospitals. The rising incidence of cancer worldwide also increases demand for specialized treatment centers. Patients benefit from focused care pathways and shorter waiting times in these facilities. In addition, many specialty centers collaborate with research institutions to develop innovative cancer treatments. The presence of experienced oncology specialists improves surgical outcomes. Increasing awareness about specialized cancer care services further boosts patient preference. As a result, specialty cancer care centers are expected to witness rapid growth during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Lung Cancer Surgery market is segmented into direct tender, retail sales, online sales, and others. The direct tender segment dominated the largest market revenue share of 49.5% in 2025, driven by the procurement practices of hospitals and healthcare institutions. Medical devices and surgical equipment used in lung cancer surgery are commonly purchased through large-scale contracts with manufacturers. Government hospitals and major healthcare systems frequently rely on tender-based procurement processes. This approach allows healthcare institutions to obtain equipment at competitive prices. Direct tenders also ensure consistent supply of surgical tools and devices required for lung cancer operations. Manufacturers often prefer this channel due to long-term agreements with healthcare organizations. Hospitals benefit from technical support and service contracts included in tender agreements. Increasing healthcare investments in hospital infrastructure further strengthen demand through direct tenders. In addition, large procurement volumes support cost efficiency for healthcare providers. Tender-based purchasing also ensures regulatory compliance and product quality standards. As a result, direct tender remains the dominant distribution channel for lung cancer surgery equipment.

The online sales segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, supported by the rapid digitalization of healthcare procurement systems. Healthcare providers are increasingly using online platforms to purchase medical devices and surgical equipment. Digital procurement systems allow hospitals and clinics to compare products and pricing more efficiently. Online platforms also provide easier access to a wide range of surgical tools and medical supplies. Smaller hospitals and clinics particularly benefit from convenient online ordering systems. Manufacturers are increasingly developing digital marketplaces to expand their customer reach. The COVID-19 pandemic accelerated the adoption of online purchasing solutions in the healthcare sector. Secure payment systems and improved logistics networks further support online sales growth. Digital platforms also offer detailed product information and technical specifications. Healthcare institutions can streamline procurement processes through online systems. In addition, rapid advancements in e-commerce technology improve the reliability of online medical equipment distribution. These factors are expected to drive strong growth of the online sales segment during the forecast period.

Lung Cancer Surgery Market Regional Analysis

- North America dominated the lung cancer surgery market with the largest revenue share of 38.9% in 2025, supported by the region’s highly developed healthcare infrastructure, strong adoption of advanced surgical technologies, and the presence of leading medical device manufacturers and oncology treatment centers

- The region benefits from widespread availability of specialized thoracic surgeons, advanced hospital facilities, and early adoption of minimally invasive surgical techniques such as video-assisted thoracoscopic surgery (VATS) and robotic-assisted thoracic surgery

- In addition, strong healthcare expenditure, favorable reimbursement policies, and increased awareness regarding early diagnosis and treatment of lung cancer are contributing to the market’s growth. The rising prevalence of lung cancer and continuous investments in surgical innovation are further strengthening the region’s leadership in the global Lung Cancer Surgery market

U.S. Lung Cancer Surgery Market Insight

The U.S. lung cancer surgery market captured the largest revenue share within North America in 2025, driven by the country’s advanced healthcare ecosystem and strong focus on oncology research and treatment. The presence of major cancer research institutes, leading hospitals, and a high adoption rate of cutting-edge surgical technologies significantly supports market expansion. Surgeons in the U.S. increasingly utilize minimally invasive procedures, including robotic-assisted surgeries, which offer improved surgical precision, shorter recovery times, and reduced postoperative complications. In addition, rising lung cancer screening programs, growing healthcare spending, and strong government and private sector investments in cancer treatment infrastructure continue to accelerate the demand for lung cancer surgical procedures across the country.

Europe Lung Cancer Surgery Market Insight

The Europe lung cancer surgery market is projected to expand at a considerable CAGR during the forecast period, supported by increasing awareness of early cancer diagnosis and improved access to advanced surgical treatments. The region benefits from well-established healthcare systems, strong government healthcare initiatives, and increasing investments in cancer treatment technologies. Countries across Europe are adopting minimally invasive and robotic-assisted thoracic surgical procedures to improve patient outcomes and reduce hospital stays. In addition, the rising incidence of lung cancer, aging populations, and the expansion of specialized oncology treatment centers are key factors driving the growth of the Lung Cancer Surgery market in Europe.

U.K. Lung Cancer Surgery Market Insight

The U.K. lung cancer surgery market is anticipated to grow steadily during the forecast period, primarily due to the increasing prevalence of lung cancer and growing emphasis on early detection and treatment. National healthcare initiatives, including screening programs and cancer awareness campaigns, are encouraging early diagnosis and timely surgical intervention. The availability of advanced surgical technologies and specialized thoracic surgeons further supports the adoption of modern lung cancer surgical procedures. Moreover, government investments aimed at improving oncology care and expanding hospital infrastructure are expected to contribute to the long-term development of the Lung Cancer Surgery market in the U.K.

Germany Lung Cancer Surgery Market Insight

The Germany lung cancer surgery market is expected to expand at a significant CAGR throughout the forecast period, driven by the country’s strong healthcare infrastructure and leadership in medical technology innovation. Germany has a high concentration of advanced hospitals and cancer treatment centers that regularly adopt new surgical technologies, including robotic-assisted systems and minimally invasive thoracic procedures. The increasing focus on precision medicine, along with continuous investments in cancer treatment facilities, is supporting the growth of lung cancer surgical procedures. In addition, the presence of skilled surgeons, strong reimbursement frameworks, and ongoing research in oncology treatment are contributing to the expansion of the Lung Cancer Surgery market in Germany.

Asia-Pacific Lung Cancer Surgery Market Insight

The Asia-Pacific lung cancer surgery market is expected to grow at the fastest CAGR of 9.6% during the forecast period, driven by the rising incidence of lung cancer and significant improvements in healthcare infrastructure across the region. Rapid urbanization, increasing exposure to air pollution and tobacco consumption, and the growing aging population are contributing to the increasing burden of lung cancer in countries such as China, India, and Japan. Governments across the region are expanding healthcare investments, strengthening hospital infrastructure, and improving access to advanced cancer treatment technologies. In addition, the increasing number of specialized oncology centers and the rising adoption of minimally invasive surgical techniques are accelerating the demand for lung cancer surgery procedures across the Asia-Pacific region.

Japan Lung Cancer Surgery Market Insight

The Japan lung cancer surgery market is gaining considerable momentum due to the country’s advanced healthcare system and strong focus on early cancer detection and treatment. Japan has one of the highest life expectancies globally, which contributes to a larger aging population and a higher demand for effective cancer treatment solutions. Hospitals in Japan are increasingly adopting minimally invasive surgical approaches, including robotic-assisted thoracic surgery, to improve surgical accuracy and patient recovery outcomes. In addition, continuous advancements in medical technologies, strong government healthcare policies, and widespread cancer screening programs are further supporting the growth of the Lung Cancer Surgery market in Japan.

China Lung Cancer Surgery Market Insight

The China lung cancer surgery market accounted for the largest revenue share in the Asia-Pacific region in 2025, driven by the country’s large patient population and rapidly expanding healthcare infrastructure. Increasing awareness of early cancer diagnosis, along with government-led initiatives to strengthen cancer treatment facilities, is significantly supporting market growth. China is also witnessing growing investments in advanced surgical technologies and hospital modernization programs. The rising adoption of minimally invasive and robotic-assisted surgical procedures in major hospitals, combined with the expansion of specialized oncology centers, is expected to continue driving the demand for lung cancer surgical treatments across the country.

Lung Cancer Surgery Market Share

The Lung Cancer Surgery industry is primarily led by well-established companies, including:

- Intuitive Surgical, Inc. (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson (U.S.)

- Stryker (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- CONMED Corporation (U.S.)

- Smith & Nephew plc (U.K.)

- B. Braun SE (Germany)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Fujifilm Holdings Corporation (Japan)

- Canon Medical Systems Corporation (Japan)

- Teleflex Incorporated (U.S.)

- Applied Medical Resources Corporation (U.S.)

- Peter Lazic GmbH (Germany)

- Surgnova Healthcare Technologies (India)

- Stapleline Medizintechnik GmbH (Germany)

- Reach Surgical, Inc. (China)

- Mindray Medical International Limited (China)

Latest Developments in Global Lung Cancer Surgery Market

- In September 2021, Quantum Surgical received CE marking for its Epione robotic platform for tumor ablation procedures, enabling its use in minimally invasive cancer treatments in Europe. The robotic system supports image-guided tumor targeting and ablation, allowing physicians to treat tumors with high precision while minimizing damage to surrounding tissue. This development highlighted the increasing integration of robotic technologies in minimally invasive cancer surgeries, including procedures targeting lung tumors

- In November 2022, Quantum Surgical’s Epione robotic platform received the Prix Galien USA award for innovative medical technology, recognizing its role in advancing robotic-assisted tumor ablation for cancer treatment. The system supports highly precise percutaneous interventions for tumor removal and reflects the growing adoption of advanced robotic platforms in oncology surgical procedures

- In September 2023, Quantum Surgical obtained CE certification extending the use of its Epione robotic-assisted platform to lung tumors, enabling physicians in Europe to perform robot-guided ablation procedures for pulmonary tumors. This expansion marked a significant milestone in the adoption of robotics for minimally invasive lung cancer surgery and interventional oncology

- In October 2025, surgeons at UK HealthCare began performing thoracic procedures using the da Vinci SP robotic surgical system after receiving FDA approval for thoracic surgery applications. The single-port robotic platform enables surgeons to perform complex lung cancer surgeries through a single small incision, improving surgical precision while reducing recovery time for patients

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.