Global Lymphatic Filariasis Market

Market Size in USD Billion

USD

11.55 Billion

USD

25.76 Billion

2025

2033

USD

11.55 Billion

USD

25.76 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.55 Billion | |

| USD 25.76 Billion | |

| % | |

|

Lymphatic Filariasis Market Size

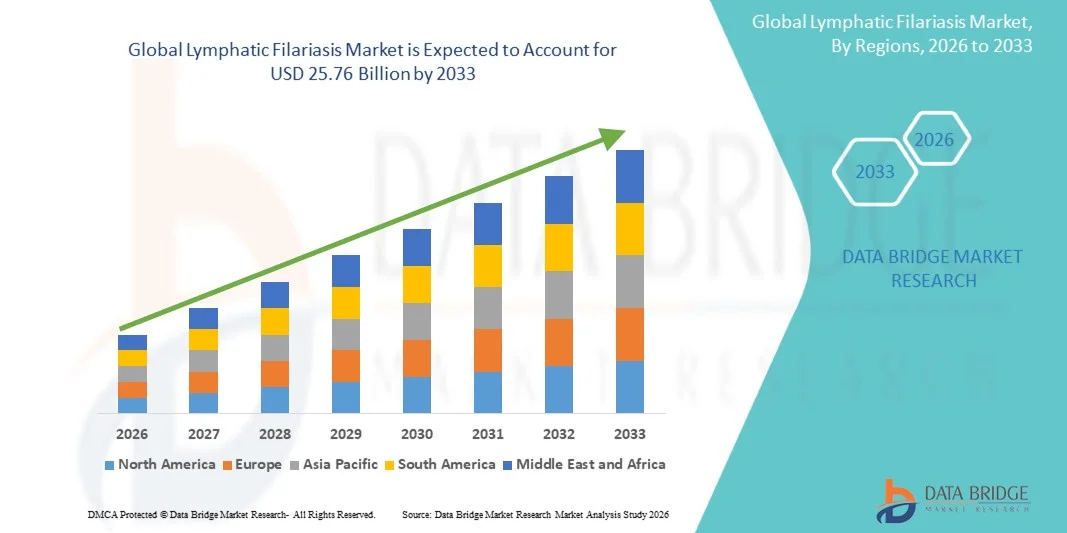

- The global Lymphatic Filariasis market size was valued at USD 11.55 billion in 2025 and is expected to reach USD 25.76 billion by 2033, at a CAGR of 10.5% during the forecast period

- The market growth is largely fueled by the increasing prevalence of lymphatic filariasis in endemic tropical and subtropical regions, along with expanding government-led mass drug administration (MDA) programs and rising global efforts toward disease elimination, leading to greater adoption of preventive and therapeutic solutions

- Furthermore, growing investments from public health organizations, improved diagnostic capabilities, and increasing access to antiparasitic treatments are establishing lymphatic filariasis management as a key focus in infectious disease control. These converging factors are accelerating the uptake of Lymphatic Filariasis solutions, thereby significantly boosting the industry’s growth

Lymphatic Filariasis Market Analysis

- Lymphatic filariasis, a neglected tropical disease caused by parasitic worms transmitted through mosquitoes, is a major public health concern in endemic regions, leading to chronic disability such as lymphedema and elephantiasis, thereby driving increased focus on preventive chemotherapy and elimination programs

- The escalating demand for lymphatic filariasis management is primarily fueled by large-scale government elimination initiatives, expanded mass drug administration (MDA) campaigns, growing awareness of neglected tropical diseases, and improving access to antiparasitic treatments and diagnostic tools

- North America dominated the Lymphatic Filariasis market with the largest revenue share of approximately 34.8% in 2025, supported by strong research funding, active involvement of global health organizations, and advanced diagnostic and surveillance capabilities despite being a non-endemic treatment and research hub

- Asia-Pacific is expected to be the fastest growing region in the Lymphatic Filariasis market during the forecast period due to high disease burden in endemic countries, large-scale public health programs, increasing government funding, and strong WHO-backed elimination initiatives across countries like India and Indonesia

- The oral segment accounted for the largest market revenue share of 68.3% in 2025, driven by its extensive use in mass drug administration programs

Report Scope and Lymphatic Filariasis Market Segmentation

|

Attributes |

Lymphatic Filariasis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Lymphatic Filariasis Market Trends

“Enhanced Disease Surveillance and Digital Health Integration in Lymphatic Filariasis Management”

- A significant and accelerating trend in the global Lymphatic Filariasis market is the increasing use of digital health tools and data-driven surveillance systems to improve disease tracking, prevention, and elimination programs. These technologies are strengthening mass drug administration (MDA) programs and enabling more efficient monitoring of endemic regions

- For instance, national public health programs in endemic countries are increasingly adopting mobile-based reporting systems and GIS-enabled mapping tools to identify high-risk communities and track treatment coverage during elimination campaigns

- Digital surveillance systems are improving real-time reporting of infection clusters, enabling health authorities to respond more effectively with targeted intervention strategies such as vector control and community drug distribution

- Integration of centralized health databases with field-level reporting systems is enhancing coordination between healthcare workers, epidemiologists, and government health agencies. This is helping improve accuracy in prevalence estimation and program evaluation

- This shift toward technology-enabled disease monitoring is reshaping expectations in infectious disease control programs, with greater emphasis on real-time data, program efficiency, and elimination-focused strategies

- The demand for improved diagnostics, surveillance platforms, and public health intervention tools is steadily increasing as global health organizations intensify efforts toward eliminating lymphatic filariasis as a public health problem

Lymphatic Filariasis Market Dynamics

Driver

“Global Elimination Programs and Increasing Government and NGO-Led Mass Drug Administration Initiatives”

- The primary growth driver in the lymphatic filariasis market is the strong global push toward disease elimination, led by organizations such as the WHO along with national governments and non-governmental organizations. These initiatives focus on interrupting transmission through large-scale mass drug administration (MDA) programs across endemic regions

- For instance, several endemic countries across Asia and Africa are scaling up annual MDA campaigns using antiparasitic drugs such as albendazole combined with ivermectin or diethylcarbamazine. These structured campaigns aim to reduce microfilaria levels in the population and eventually eliminate transmission. Such coordinated public health efforts are expected to significantly drive market growth over the forecast period

- Increasing funding from global health agencies and partnerships between governments and pharmaceutical organizations are strengthening access to essential medications and improving the reach of treatment programs in rural and underserved populations

- In addition, rising awareness among healthcare workers and communities regarding the long-term disability burden caused by lymphatic filariasis (such as lymphedema and elephantiasis) is improving participation rates in preventive treatment campaigns

- The expansion of public health infrastructure and sustained global commitment toward elimination goals is expected to remain a key factor driving the lymphatic filariasis market

Restraint/Challenge

“Limited Healthcare Access, Poor Disease Awareness, and Challenges in Sustaining Long-Term Elimination Programs”

- A major challenge in the lymphatic filariasis market is the continued lack of adequate healthcare infrastructure in endemic rural and low-income regions, which limits early detection, treatment coverage, and consistent implementation of mass drug administration programs

- For instance, in several remote areas, logistical constraints such as inadequate healthcare workforce, poor transportation networks, and limited access to medicines reduce the effectiveness of large-scale elimination campaigns, leading to inconsistent treatment coverage

- Low awareness among affected populations about the asymptomatic nature of early-stage infection further reduces participation in preventive drug programs, making it difficult to achieve full community compliance in endemic regions

- Addressing these challenges requires strengthening primary healthcare systems, improving community engagement programs, and expanding education initiatives to increase awareness about prevention and treatment benefits

- In addition, sustaining long-term funding and maintaining high coverage rates across multiple treatment cycles remains difficult for many national programs, especially in regions with competing public health priorities

- Overcoming these barriers through stronger healthcare delivery systems, improved community participation, and sustained global funding support will be essential for achieving long-term elimination targets in the lymphatic filariasis market

Lymphatic Filariasis Market Scope

The market is segmented on the basis of diagnosis, treatment, route of administration, end-users, and distribution channel.

• By Diagnosis

On the basis of diagnosis, the Lymphatic Filariasis market is segmented into microscopic examination, serologic techniques, and others. The microscopic examination segment dominated the largest market revenue share of 46.8% in 2025, driven by its strong availability in primary healthcare centers across endemic regions. It remains the most widely used diagnostic method due to its simplicity and low operational cost. The technique allows direct detection of microfilariae in blood samples, ensuring reliable confirmation of infection. Increasing government-led mass screening programs are significantly boosting adoption rates. Expanding diagnostic laboratory infrastructure in rural and semi-urban regions is further supporting growth. High dependency on conventional microscopy in low-resource settings continues to strengthen demand. Healthcare workers prefer it due to quick results and minimal technical requirements. Rising disease burden in tropical regions is further increasing testing volumes. Continuous public health initiatives are enhancing awareness and diagnosis rates.

The serologic techniques segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by improved sensitivity and early-stage detection capabilities. These methods can detect antigen-antibody responses even in low parasite load conditions. Increasing adoption of ELISA-based assays and rapid diagnostic kits is boosting uptake. Growing investment in advanced immunodiagnostic technologies is enhancing accuracy. Public health elimination programs are encouraging broader screening adoption. Rising demand for early and asymptomatic detection is further supporting growth. Expanding availability of point-of-care diagnostic tools is improving accessibility. Continuous innovation in serological testing platforms is strengthening reliability. Government support for elimination of lymphatic filariasis is accelerating adoption. Integration of advanced diagnostic solutions in hospitals and labs is also supporting expansion.

• By Treatment

On the basis of treatment, the Lymphatic Filariasis market is segmented into surgery, medication, and others. The medication segment held the largest market revenue share of 52.6% in 2025, driven by large-scale mass drug administration programs across endemic countries. Antifilarial drugs such as diethylcarbamazine and ivermectin are widely distributed for both treatment and prevention. Strong support from global health organizations is ensuring widespread drug availability. Increasing government-led elimination campaigns are boosting treatment coverage. High affordability and accessibility of oral medications are further strengthening adoption. Community health programs are improving compliance in rural areas. Rising awareness regarding early-stage treatment is supporting demand. Pharmaceutical supply chain expansion is ensuring consistent availability. Preventive chemotherapy strategies are reinforcing dominance of this segment.

The surgery segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing cases of advanced lymphatic complications requiring surgical intervention. Chronic lymphedema and severe hydrocele cases often require operative management. Growing availability of specialized surgical care in tertiary hospitals is improving access. Advancements in reconstructive and microsurgical techniques are enhancing outcomes. Rising awareness about surgical correction options is supporting adoption. Increasing healthcare infrastructure development in endemic regions is boosting capacity. Higher referral rates for complicated cases are contributing to growth. Improved post-operative care facilities are increasing treatment success rates. Focus on improving quality of life in chronic patients is further driving demand.

• By Route of Administration

On the basis of route of administration, the Lymphatic Filariasis market is segmented into oral, parenteral, and others. The oral segment accounted for the largest market revenue share of 68.3% in 2025, driven by its extensive use in mass drug administration programs. Oral therapies are easy to distribute at community level in large populations. High patient compliance and non-invasive nature support widespread adoption. Governments prefer oral drugs for large-scale elimination campaigns. Availability of low-cost antifilarial tablets strengthens accessibility. Pharmaceutical companies ensure stable production of oral formulations. Rural healthcare workers can easily administer oral regimens. Strong global elimination initiatives are increasing coverage rates. Oral drugs remain the backbone of preventive chemotherapy programs.

The parenteral segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing use in severe and complicated clinical cases. Injectable therapies are required in advanced lymphatic damage conditions. Rising hospital admissions for chronic complications are supporting demand. Improved access to hospital-based care in developing countries is boosting usage. Advances in injectable drug formulations are enhancing treatment safety. Greater clinical preference for controlled dosing is supporting adoption. Expanding emergency and tertiary care facilities are improving availability. Increased awareness of advanced treatment protocols is driving usage.

• By End-Users

On the basis of end-users, the Lymphatic Filariasis market is segmented into hospitals, homecare, speciality centres, and others. The hospitals segment dominated the largest market revenue share of 55.9% in 2025, driven by availability of advanced diagnostic and treatment infrastructure. Hospitals serve as primary treatment centers for moderate to severe cases. Increasing institutional healthcare visits in endemic regions are supporting demand. Presence of skilled healthcare professionals improves clinical outcomes. Government funding for hospital-based elimination programs is strengthening adoption. Availability of both diagnostic and surgical facilities supports dominance. Rising awareness of complications is increasing hospital dependency. Expanding tertiary care infrastructure is further boosting access.

The speciality centres segment is expected to witness the fastest CAGR of 10.6% from 2026 to 2033, driven by growing focus on targeted and long-term management of lymphatic complications. These centres provide specialized care for chronic filariasis patients. Increasing establishment of tropical disease clinics is supporting growth. Improved access to expert care is boosting patient preference. Rising awareness about chronic disease management is driving demand. Expansion of dedicated lymphatic care units is strengthening infrastructure. Government initiatives for neglected tropical diseases are supporting development.

• By Distribution Channel

On the basis of distribution channel, the Lymphatic Filariasis market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment held the largest market revenue share of 48.1% in 2025, driven by high dependency on hospital-based treatment and government-supported drug distribution programs. Hospital pharmacies ensure direct and controlled drug dispensing. Strong integration with mass drug administration initiatives supports dominance. Availability of essential antifilarial drugs in hospitals enhances access. Physicians prefer hospital dispensing for better monitoring. Rising inpatient treatment cases are increasing demand. Government procurement programs strengthen supply chain efficiency. Hospitals remain the primary distribution hub in endemic regions.

The online pharmacy segment is expected to witness the fastest CAGR of 12.7% from 2026 to 2033, driven by rapid digitalization of healthcare services. Increasing penetration of e-pharmacy platforms is improving medicine accessibility. Home delivery convenience is encouraging patient adoption. Rising telemedicine consultations are boosting digital prescriptions. Growing smartphone and internet usage in developing regions is supporting expansion. Competitive pricing and discount availability are increasing preference. Integration with digital health systems is strengthening adoption. Awareness of online healthcare services is rising steadily.

Lymphatic Filariasis Market Regional Analysis

- North America dominated the Lymphatic Filariasis market with the largest revenue share of approximately 34.8% in 2025

- Supported by strong research funding, active involvement of global health organizations

- Advanced diagnostic and surveillance capabilities despite being a non-endemic treatment and research hub

U.S. Lymphatic Filariasis Market Insight

The U.S. Lymphatic Filariasis market captured the largest revenue share within North America in 2025, driven primarily by its role as a major center for research, surveillance, and global disease monitoring rather than endemic transmission. Strong funding from public health agencies, collaborations with international health organizations, and advanced diagnostic research infrastructure contribute to market growth. The country also plays a key role in developing treatment strategies and supporting global elimination programs.

Europe Lymphatic Filariasis Market Insight

The Europe Lymphatic Filariasis market is projected to expand at a substantial CAGR throughout the forecast period, supported by strong participation in global eradication initiatives, well-funded research institutions, and active collaboration with international health organizations. Increasing focus on neglected tropical diseases (NTDs) and improved diagnostic capabilities is strengthening the region’s contribution to surveillance, research, and treatment development.

U.K. Lymphatic Filariasis Market Insight

The U.K. Lymphatic Filariasis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong public health research funding, academic involvement in tropical disease studies, and participation in global elimination programs. Institutions in the country contribute significantly to epidemiological research, drug development studies, and international health policy support.

Germany Lymphatic Filariasis Market Insight

The Germany Lymphatic Filariasis market is expected to expand at a considerable CAGR during the forecast period, fueled by strong biomedical research capabilities, government-backed health initiatives, and participation in global disease surveillance efforts. The country’s advanced laboratory infrastructure supports diagnostic innovation and research into vector-borne and parasitic diseases.

Asia-Pacific Lymphatic Filariasis Market Insight

The Asia-Pacific Lymphatic Filariasis market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by high endemic disease prevalence, large-scale mass drug administration (MDA) programs, increasing government healthcare spending, and strong support from WHO-led elimination initiatives. Expanding rural healthcare access and improved disease mapping are further accelerating regional progress toward elimination goals.

Japan Lymphatic Filariasis Market Insight

The Japan Lymphatic Filariasis market is witnessing steady growth, primarily supported by advanced research capabilities, strong public health infrastructure, and contribution to global infectious disease control programs. Although not an endemic country, Japan plays a significant role in research, surveillance technology development, and international collaboration for lymphatic filariasis elimination.

China Lymphatic Filariasis Market Insight

The China Lymphatic Filariasis market accounted for a significant share in Asia Pacific in 2025 due to ongoing public health surveillance, historical disease burden management, and strong government-led infectious disease control initiatives. Continued investment in vector control programs, healthcare infrastructure, and international collaboration is supporting progress toward sustained elimination and monitoring efforts.

Lymphatic Filariasis Market Share

The Lymphatic Filariasis industry is primarily led by well-established companies, including:

- GlaxoSmithKline plc (U.K.)

- Merck & Co., Inc. (U.S.)

- Sanofi S.A. (France)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- Abbott Laboratories (U.S.)

- AstraZeneca plc (U.K.)

- Eisai Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Zydus Lifesciences Ltd. (India)

- Alkem Laboratories Ltd. (India)

- Incepta Pharmaceuticals Ltd. (Bangladesh)

- Gilead Sciences, Inc. (U.S.)

- Mylan N.V. (Viatris) (U.S.)

- Becton, Dickinson and Company (BD) (U.S.)

Latest Developments in Global Lymphatic Filariasis Market

- In March 2021, the World Health Organization (WHO) expanded implementation guidance for the Global Programme to Eliminate Lymphatic Filariasis (GPELF), strengthening the use of Mass Drug Administration (MDA) strategies using ivermectin, diethylcarbamazine (DEC), and albendazole to accelerate elimination in endemic countries. This reinforced global elimination timelines and treatment scale-up programs

- In June 2022, WHO and partner countries significantly increased deployment of triple-drug therapy (IDA: ivermectin + DEC + albendazole) in endemic regions, improving microfilariae clearance rates and accelerating interruption of transmission in high-burden districts

- In February 2023, national elimination programs in Africa and Asia expanded community-wide MDA coverage, targeting over 900 million people globally at risk, reinforcing WHO’s elimination roadmap toward 2030

- In January 2024, new clinical evidence supported broader adoption of IDA-MDA (triple-drug therapy) as a faster elimination strategy in non–co-endemic regions, demonstrating higher efficacy compared to traditional two-drug regimens

- In March 2024, updated WHO-based programmatic reviews highlighted improved outcomes in elimination campaigns across Southeast Asia and Africa, where intensified MDA rounds reduced lymphatic filariasis prevalence significantly and moved several districts closer to elimination validation thresholds

- In January 2025, the European Medicines Agency (EMA) issued a positive scientific opinion for ivermectin + albendazole combination therapy, including its use for lymphatic filariasis treatment, supporting regulatory validation of combination antiparasitic therapy in Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.