Global Lymphedema Praecox Meige Disease Treatment Market

Market Size in USD Million

USD

192.94 Million

USD

402.60 Million

2025

2033

USD

192.94 Million

USD

402.60 Million

2025

2033

| 2026 - 2033 | |

| USD 192.94 Million | |

| USD 402.60 Million | |

| % | |

|

Lymphedema Praecox (Meige Disease) Treatment Market Size

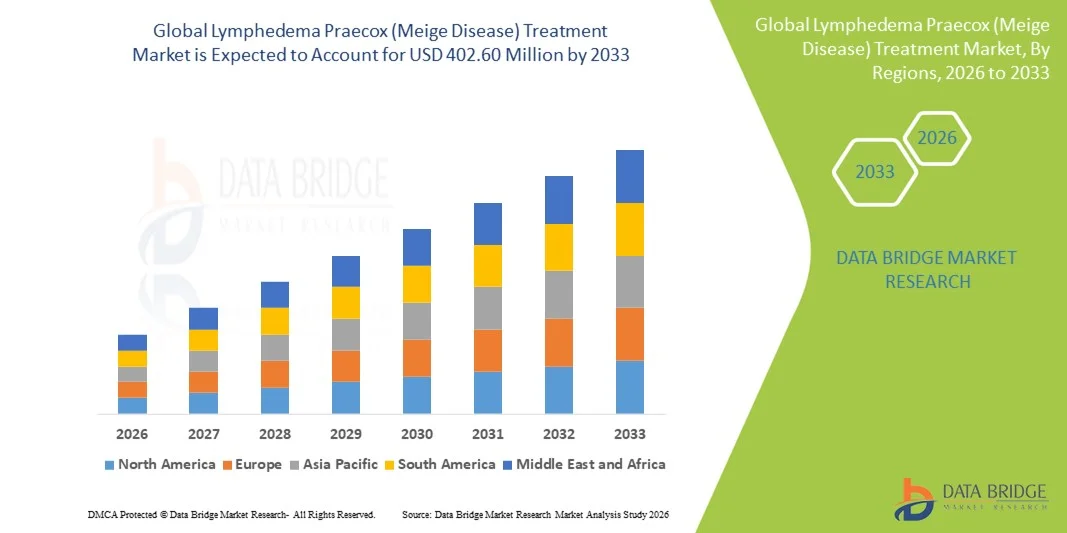

- The global Lymphedema Praecox (Meige Disease) treatment market size was valued at USD 192.94 million in 2025 and is expected to reach USD 402.60 million by 2033, at a CAGR of 9.63% during the forecast period

- The market growth is primarily driven by rising clinical awareness, increasing availability of advanced diagnostic modalities, and ongoing advancements in microsurgical procedures and compression technologies that support more effective long-term management of primary lymphedema

- Furthermore, the growing emphasis on early intervention, expanding adoption of complete decongestive therapy, and rising patient demand for safer, personalized, and outcome-oriented treatment approaches are strengthening the role of specialized lymphedema care. These converging factors are accelerating the use of therapeutic and surgical solutions for Meige disease, thereby significantly boosting overall market expansion

Lymphedema Praecox (Meige Disease) Treatment Market Analysis

- Lymphedema Praecox (Meige Disease), a primary lymphatic disorder characterized by early-onset limb swelling, is increasingly driving demand for advanced therapeutic solutions due to growing clinical awareness, improved diagnostic capabilities, and the rising availability of specialized treatment options across healthcare settings

- The rising adoption of complete decongestive therapy, advancements in compression technologies, and expanding use of microsurgical interventions such as lymphovenous anastomosis (LVA) and vascularized lymph node transfer (VLNT) are key factors fueling the growth of the Meige disease treatment landscape

- North America dominated the Lymphedema Praecox treatment market with a market share of 43.7% in 2025, supported by well-established lymphedema management centers, strong implementation of clinical guidelines, and higher patient access to advanced surgical and compression-based therapies, with the U.S. witnessing significant adoption driven by improved reimbursement policies and wider clinical availability of physiologic microsurgery

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to increasing investment in lymphatic disorder management, rising diagnostic rates, and expanding healthcare infrastructure enabling earlier detection and intervention

- The compression therapy segment dominated the Lymphedema Praecox treatment market with a market share of 57% in 2025, driven by its position as the global first-line management standard, its role across all disease stages, and its consistent demand for long-term maintenance, making it the cornerstone of lymphedema care worldwide

Report Scope and Lymphedema Praecox (Meige Disease) Treatment Market Segmentation

|

Attributes |

Lymphedema Praecox (Meige Disease) Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Lymphedema Praecox (Meige Disease) Treatment Market Trends

Advancement of Physiologic Microsurgeries and Imaging-Guided Therapies

- A significant and accelerating trend in the global Lymphedema Praecox treatment market is the expanding use of physiologic microsurgeries such as lymphovenous anastomosis (LVA) and vascularized lymph node transfer (VLNT), supported by improved imaging technologies that enable earlier detection and more targeted intervention

- For instance, leading centers globally are now using high-resolution indocyanine green (ICG) lymphography to map functional lymphatic channels, allowing clinicians to perform precision-based LVA procedures tailored to each patient’s lymphatic architecture

- Microsurgical advancements enable benefits such as improved lymphatic drainage, reduced limb volume, and better long-term outcomes, while imaging-guided techniques help identify suitable surgical candidates and optimize treatment planning; for instance, VLNT programs increasingly combine ICG mapping with intraoperative navigation to enhance graft success and reduce complications

- The seamless integration of imaging technologies with surgical planning platforms facilitates more accurate staging and personalized treatment pathways, allowing specialists to correlate lymphatic flow patterns with therapeutic responses and postoperative progress

- This trend toward more sophisticated, minimally invasive, and patient-specific treatment approaches is fundamentally reshaping expectations for primary lymphedema care

- The demand for image-guided physiologic surgeries and advanced lymphatic mapping tools is growing rapidly across specialized centers, as clinicians increasingly prioritize durable outcomes and earlier intervention for Meige disease patients

Lymphedema Praecox (Meige Disease) Treatment Market Dynamics

Driver

Growing Need Due to Rising Clinical Awareness and Advancements in Early Diagnosis

- The increasing recognition of primary lymphedema among healthcare professionals, along with the expansion of diagnostic infrastructure, is a significant driver for the heightened demand for targeted Lymphedema Praecox treatment solutions

- For instance, in recent years multiple tertiary care hospitals have expanded their lymphatic disorder programs by incorporating ICG lymphography suites and multidisciplinary care teams, enabling streamlined assessment and earlier initiation of therapy

- As clinicians become more aware of the lifelong progression risks associated with untreated Meige disease, advanced therapies such as CDT, compression systems, and physiologic microsurgeries are gaining traction as superior alternatives to basic symptomatic management

- Furthermore, the rising interest in comprehensive care pathways and the development of specialized lymphedema centers are positioning structured treatment protocols as essential components of early-stage intervention

- The convenience of standardized CDT programs, improved compression options, and the ability to manage patients through coordinated, multidisciplinary frameworks are key factors propelling adoption across clinical settings; the shift toward dedicated lymphedema clinics further contributes to market growth

Restraint/Challenge

Skin Irritation Issues and Regulatory Compliance Hurdle

- Concerns surrounding skin irritation, dermatitis, and discomfort caused by long-term compression garment use pose a significant challenge to broader adoption, particularly among patients with sensitive skin or chronic inflammation

- For instance, reports of compression-induced skin reactions in primary lymphedema patients have made some clinicians cautious in prescribing high-pressure garments without close monitoring and proper skin-care protocols

- Addressing these concerns through hypoallergenic fabrics, better moisture-control materials, and patient education on skin hygiene is crucial for improving adherence; manufacturers increasingly highlight dermatologically tested materials and improved pressure-distribution designs to build user confidence

- In addition, the relatively high cost of advanced compression systems and microsurgical procedures can be a barrier to access for patients in low-resource regions, particularly where insurance coverage for primary lymphedema remains limited or inconsistent

- While affordability is gradually improving through wider production and streamlined device designs, the perceived premium for advanced treatment options can still limit widespread clinical adoption, especially in regions lacking reimbursement pathways

- Overcoming these challenges through material innovation, expanded reimbursement support, and improved patient education on garment use will be vital for sustained market growth

Lymphedema Praecox (Meige Disease) Treatment Market Scope

The market is segmented on the basis of treatment, product, end user, and distribution channel.

- By Treatment

On the basis of treatment, the market is segmented into complete decongestive therapy, compression therapy, pneumatic compression devices, surgical interventions, and supportive therapies. The compression therapy segment dominated the Lymphedema Praecox treatment market with a market share of 57% in 2025, owing to its position as the standard first-line management method for primary lymphedema. Compression garments and bandaging help prevent fluid buildup, stabilize swelling, and maintain daily limb volume control. Their non-invasive nature and broad availability across clinical and home-care environments strengthen adoption among patients. Increasing physician preference for compression products due to proven clinical outcomes also contributes to sustained market leadership. The segment further benefits from continuous improvements in garment materials, adjustable designs, and patient-friendly wearability. In addition, compression therapy remains widely reimbursed in several developed healthcare systems, supporting its strong market hold.

The surgical interventions segment is anticipated to witness the fastest growth during the forecast period, driven by rising adoption of advanced microsurgical procedures such as lymphaticovenous anastomosis (LVA) and vascularized lymph node transfer (VLNT). These techniques are increasingly recommended for early-onset lymphedema cases, especially Meige disease patients who respond poorly to long-term conservative therapies. Growing surgeon training programs and expanding availability of supermicrosurgery centers are accelerating uptake in developed countries. Technological advancements in operative imaging, including ICG lymphography and high-resolution lymphatic mapping, enhance procedural outcomes and patient suitability. The growing preference for long-term improvement and reduced dependence on lifelong compression also fuels patient demand. As a result, surgical interventions are emerging as a major growth catalyst within the treatment landscape.

- By Product

On the basis of product, the market is segmented into compression products, medical devices, surgical instruments & consumables, and diagnostics & monitoring systems. Compression Products held the largest market revenue share in 2025 due to their critical role in lymphedema management across all stages of the condition. Compression garments such as sleeves, stockings, wraps, and bandages help maintain limb pressure, prevent fluid accumulation, and support lymphatic flow. The segment benefits from continuous innovation in fabric technology, including breathable, hypoallergenic, and custom-fit materials enhancing patient comfort. High usage frequency and recurring replacement needs contribute to strong commercial demand. In addition, compression products remain the most accessible and affordable intervention globally, supporting widespread adoption across clinical and home settings.

Diagnostics & Monitoring Systems are expected to witness the fastest CAGR from 2026 to 2033, driven by rising emphasis on early detection of lymphatic dysfunction. Advancements in bioimpedance spectroscopy, limb volume measurement technologies, and imaging tools accelerate growth within this segment. These systems enable clinicians to identify early fluid buildup, allowing timely intervention to prevent disease progression. Growing integration of digital monitoring platforms and remote-tracking solutions supports precision care and long-term disease management. Increasing adoption of diagnostic tools in hospitals and specialty clinics further boosts segment expansion, particularly in regions prioritizing early-stage lymphedema screening.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, home healthcare providers, specialty medical suppliers, and patients. Hospitals dominated the market with the largest share in 2025 driven by their access to advanced diagnostic tools, multidisciplinary care teams, and structured treatment programs. Hospitals are often the primary point of diagnosis for lymphedema praecox, enabling early initiation of therapy and coordinated care planning. The availability of certified lymphedema therapists and surgical capabilities further strengthens their leading position. Hospitals also manage more severe or progressive cases requiring combination therapies or advanced interventions. In addition, strong reimbursement pathways across many regions support hospital-based treatment adoption.

Home Healthcare Providers are anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing preference for cost-effective and convenient long-term disease management. Home-based care enables patients to continue therapy independently through compression garments, pneumatic compression devices, and home-exercise modules. Rising adoption of telehealth platforms enhances remote monitoring and personalized treatment adjustments. The trend toward decentralizing chronic care management supports rapid expansion of home healthcare services. In addition, growing availability of portable medical devices and patient-education programs accelerates segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital procurement, retail pharmacies, medical device distributors, and e-commerce. Hospital Procurement dominated the market with the largest revenue share in 2025 due to bulk purchasing of medical devices, compression garments, and consumables directly used in treatment programs. Hospitals typically maintain long-term partnerships with approved suppliers, ensuring consistent demand through structured procurement cycles. The presence of reimbursement-driven treatment pathways further strengthens the segment’s share. Hospital procurement channels also support advanced product adoption, including diagnostic systems and surgical consumables. In addition, centralized purchasing enables cost efficiency and reliable supply availability.

E-commerce is expected to witness the fastest CAGR from 2026 to 2033, supported by increasing patient preference for convenient access to compression garments and home-based medical devices. Online platforms offer wider product availability, size customization options, and competitive pricing, boosting adoption among younger patients and caregivers. The rapid growth of digital health marketplaces and direct-to-consumer medical brands enhances segment expansion. E-commerce also facilitates repeat purchases, especially for consumables and replacement compression products. In addition, improved logistics networks and doorstep delivery services further accelerate market penetration.

Lymphedema Praecox (Meige Disease) Treatment Market Regional Analysis

- North America dominated the Lymphedema Praecox treatment market with a market share of 43.7% in 2025, supported by well-established lymphedema management centers, strong implementation of clinical guidelines, and higher patient access to advanced surgical and compression-based therapies

- Healthcare providers in the region benefit from well-established lymphedema management protocols, enabling comprehensive treatment through multidisciplinary teams, certified lymphedema therapists, and advanced rehabilitation centers

- This strong uptake is further supported by higher healthcare spending, favorable reimbursement for compression therapy and surgical procedures, and rising emphasis on early detection of primary lymphedema using modern lymphatic mapping tools, solidifying North America as a leading market for Meige disease management

U.S. Lymphedema Praecox (Meige Disease) Treatment Market Insight

The U.S. Lymphedema Praecox treatment market captured the largest revenue share within North America in 2025, fueled by strong clinical awareness and early adoption of advanced lymphedema diagnostic tools. Patients increasingly seek specialized care, including microsurgical procedures such as LVA and VLNT, which are widely available in U.S. tertiary hospitals. The growing integration of modern imaging technologies such as ICG lymphography and bioimpedance spectroscopy further enhances diagnostic precision. Rising emphasis on early-stage intervention and multidisciplinary management is propelling demand for comprehensive treatment programs. Moreover, the presence of certified lymphedema therapists, structured rehabilitation centers, and favorable reimbursement for compression therapy is significantly contributing to market expansion.

Europe Lymphedema Praecox (Meige Disease) Treatment Market Insight

The Europe Lymphedema Praecox treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong clinical guidelines and growing prioritization of chronic lymphatic disease management. Increasing awareness of genetic and primary lymphedema conditions is fostering early diagnosis and treatment adherence across major European nations. The region’s well-established healthcare infrastructure supports widespread use of CDT, compression garments, and advanced pneumatic devices. European patients increasingly prefer evidence-based, physiotherapist-led care, strengthening demand for certified lymphedema therapy services. The rise in specialized lymphatic centers and increased access to supermicrosurgery techniques are further stimulating market growth across both public and private healthcare systems.

U.K. Lymphedema Praecox (Meige Disease) Treatment Market Insight

The U.K. Lymphedema Praecox treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by expanding clinical education initiatives and increased emphasis on chronic condition management. Rising awareness of primary lymphedema among physicians and patients is leading to earlier referrals to specialist clinics. Concerns regarding long-term swelling management and therapy adherence are encouraging adoption of compression garments and home-based CDT programs. The U.K.’s strong telehealth ecosystem and digital-first healthcare approach are supporting remote monitoring and patient-led care. In addition, improvements in clinical pathways and increased training for lymphoedema practitioners are expected to stimulate steady market growth across the country.

Germany Lymphedema Praecox (Meige Disease) Treatment Market Insight

The Germany Lymphedema Praecox treatment market is expected to expand at a considerable CAGR, fueled by high clinical standards, robust reimbursement structures, and demand for technologically advanced solutions. Germany’s strong medical infrastructure supports the adoption of modern diagnostic imaging, including lymphoscintigraphy and ICG-based lymphatic mapping. Patient preference for structured therapy programs and medical-grade compression products drives consistent utilization of long-term treatment options. The country’s emphasis on precision medicine and sustainable healthcare solutions aligns with rising investments in specialized lymphedema clinics. Integration of advanced surgical interventions and rehabilitation pathways is becoming increasingly prevalent, supporting market expansion across both outpatient and hospital settings.

Asia-Pacific Lymphedema Praecox (Meige Disease) Treatment Market Insight

The Asia-Pacific Lymphedema Praecox treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare access, rising awareness of hereditary lymphedema, and expanding diagnostic capabilities in countries such as China, Japan, and India. Urbanization and growing healthcare expenditure are enabling broader adoption of compression therapy and CDT programs. Government-led efforts to strengthen chronic disease management and lymphatic disorder awareness are accelerating early diagnosis. APAC’s emergence as a manufacturing hub for compression garments and pneumatic devices is improving affordability and accessibility. The availability of lower-cost therapeutic solutions is further expanding treatment uptake across a large patient population.

Japan Lymphedema Praecox (Meige Disease) Treatment Market Insight

The Japan Lymphedema Praecox treatment market is gaining momentum due to the country’s advanced healthcare infrastructure, emphasis on precision diagnostics, and rising patient awareness of primary lymphedema. Japan places strong importance on early detection and uses high-tech imaging modalities to assess lymphatic dysfunction. Adoption of supermicrosurgical techniques such as LVA is rapidly expanding, supported by skilled surgeons and specialized medical centers. Growing integration of digital home-care tools for symptom monitoring is fueling treatment adherence. Moreover, Japan’s aging population and preference for minimally invasive, long-term management solutions are such asly to spur rising demand across both hospital and community-care settings.

India Lymphedema Praecox (Meige Disease) Treatment Market Insight

The India Lymphedema Praecox treatment market accounted for one of the largest revenue shares within Asia Pacific in 2025, attributed to rising awareness of lymphatic disorders, rapid urbanization, and improvements in healthcare infrastructure. India has a large population requiring long-term compression therapy, supporting strong demand for affordable garments and CDT services. The growing presence of domestic manufacturers is making compression products and pneumatic devices more accessible to patients. Increasing adoption of telemedicine and community-based rehabilitation is enhancing outreach for early diagnosis. Government initiatives promoting chronic disease management and medical training are further helping expand lymphedema treatment availability across urban and semi-urban regions.

Lymphedema Praecox (Meige Disease) Treatment Market Share

The Lymphedema Praecox (Meige Disease) Treatment industry is primarily led by well-established companies, including:

- BIO COMPRESSION SYSTEMS (U.S.)

- Tactile Medical (U.S.)

- medi GmbH & Co. KG (Germany)

- SIGVARIS Group (Switzerland)

- 3M (U.S.)

- BSN Medical (Sweden)

- DJO Global, Inc. (U.S.)

- Lohmann & Rauscher GmbH & Co. KG (Germany)

- Bauerfeind AG (Germany)

- Paul Hartmann AG (Germany)

- Julius Zorn GmbH (Germany)

- Devon Medical Products (U.S.)

- ArjoHuntleigh (Sweden)

- Sanyleg S.r.l. (Italy)

- Therafirm (U.S.)

- Bösl Medizintechnik GmbH (Germany)

- ConvaTec plc (U.K.)

- Cardinal Health. (U.S.)

- Medline Industries, Inc. (U.S.)

- Mego Afek (Israel)

What are the Recent Developments in Global Lymphedema Praecox (Meige Disease) Treatment Market?

- In February 2025, Tactile Medical expanded the commercial availability of Nimbl to include lower-extremity lymphedema, making it an at-home therapy option for a broader group of chronic edema and lymphedema patients

- In October 2024, Tactile Medical launched its next-generation pneumatic compression platform Nimbl, now commercially available in the U.S. for treatment of upper-extremity lymphedema. The device is notably 68% lighter, 40% smaller than prior-generation PCDs, and is designed for home-based use

- In October 2024, Lymphatica Medtech closed a €17.9 million Series B funding round to advance its implantable lymphatic-drainage device LymphoDrain, aimed at treating chronic lymphedema by restoring lymphatic circulation via an implantable pump a potentially paradigm-shifting move beyond external compression

- In April 2024, A new device category non-pneumatic compression device (NPCD) developed by Koya Medical was described in literature to provide static and gradient compression using shape-memory materials, mimicking manual lymphatic drainage (MLD) effects. This represents a technological innovation in compression therapy for chronic lymphedema and offers an alternative to traditional gradient pneumatic devices

- In January 2024, Lymphatica Medtech was awarded U.S. Food and Drug Administration (FDA) “Breakthrough Device Designation” for LymphoDrain, formally recognizing its potential to offer a novel therapeutic option for long-term lymphedema management a significant regulatory milestone for implantable lymphatic technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.