Global Machine Vision Market

Market Size in USD Billion

USD

14.56 Billion

USD

24.82 Billion

2025

2033

USD

14.56 Billion

USD

24.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.56 Billion | |

| USD 24.82 Billion | |

| % | |

|

Machine Vision Market Size

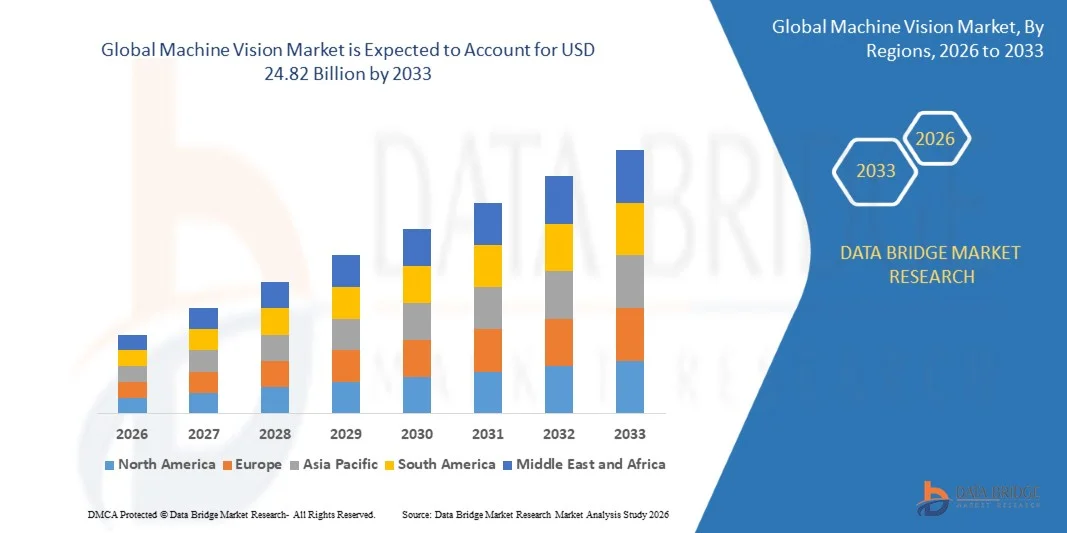

- The global machine vision market size was valued at USD 14.56 billion in 2025 and is expected to reach USD 24.82 billion by 2033, at a CAGR of 6.90% during the forecast period

- The market growth is largely fuelled by the increasing adoption of automation and Industry 4.0 practices across manufacturing sectors, where machine vision systems are widely used for quality inspection, defect detection, and process optimization. The rising demand for high-speed, accurate, and cost-efficient production systems is further accelerating market expansion across automotive, electronics, and pharmaceutical industries

- The growing integration of artificial intelligence, deep learning, and advanced imaging technologies in machine vision systems is enhancing real-time analysis capabilities and improving operational efficiency. In addition, increasing demand for robotics-based automation in smart factories is strengthening the adoption of machine vision solutions globally

Machine Vision Market Analysis

- The machine vision market is witnessing strong growth due to rapid industrial automation and the shift toward smart manufacturing ecosystems

- Expanding applications in quality control, predictive maintenance, and robotic guidance are significantly supporting market penetration across diverse industries such as automotive, food and beverage, and electronics manufacturing

- North America dominated the machine vision market with the largest revenue share in 2025, driven by strong industrial automation adoption, advanced manufacturing infrastructure, and rapid integration of AI-based inspection systems

- Asia-Pacific region is expected to witness the highest growth rate in the global machine vision market, driven by expanding manufacturing activities, strong electronics and semiconductor production, and increasing adoption of AI-enabled automation technologies across emerging economies

- The 2D Vision segment held the largest market revenue share in 2025 driven by its widespread use in industrial inspection, barcode reading, and quality control applications across manufacturing environments. 2D vision systems are widely adopted due to their cost-effectiveness, ease of integration, and strong performance in standard inspection tasks, making them the most commonly used vision technology in industrial automation. These systems are extensively deployed in production lines where high-speed inspection and surface-level defect detection are required. Increasing automation in repetitive manufacturing processes further strengthens their dominance across industries. Their compatibility with existing industrial setups also supports large-scale adoption across global manufacturing hubs

Report Scope and Machine Vision Market Segmentation

|

Attributes |

Machine Vision Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Baumer (Switzerland) |

|

Market Opportunities |

• Expansion Of Industrial Automation And Smart Manufacturing Adoption |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Machine Vision Market Trends

“Rising Adoption Of AI-Enabled And Deep Learning-Based Vision Systems”

• The increasing integration of artificial intelligence and deep learning technologies is significantly shaping the machine vision market, as industries demand higher accuracy, real-time decision-making, and automated defect detection. Machine vision systems are being widely adopted to improve inspection precision, reduce human error, and enhance production efficiency across manufacturing environments. This trend is strengthening their deployment in automotive, electronics, semiconductor, and pharmaceutical industries, encouraging manufacturers to develop advanced imaging and analytics solutions

• Growing adoption of Industry 4.0 and smart manufacturing practices is accelerating the demand for machine vision systems in automated production lines. Manufacturers are increasingly deploying vision-guided robotics and inspection systems to improve operational efficiency, ensure product quality, and enable predictive maintenance. This is also driving investments in connected factory ecosystems and real-time monitoring solutions

• Increasing demand for high-speed, accurate, and cost-effective quality inspection systems is influencing purchasing decisions across industrial sectors. Companies are focusing on reducing production defects and improving consistency through automated vision-based inspection, which is further supporting the replacement of traditional manual inspection processes

• For instance, in 2024, Cognex Corporation in the U.S. and Basler AG in Germany expanded their AI-powered machine vision product lines to support semiconductor and automotive inspection applications. These solutions were deployed to enhance precision inspection, improve defect detection rates, and support large-scale automated manufacturing operations across global production facilities

• While adoption is increasing, sustained market expansion depends on high implementation costs, integration complexity, and continuous advancements in imaging technologies. Manufacturers are also focusing on improving processing speed, scalability, and system interoperability to support broader industrial adoption

Machine Vision Market Dynamics

Driver

“Rising Industrial Automation And Demand For Quality Inspection”

• Increasing automation across manufacturing industries is a major driver for the machine vision market. Companies are adopting vision-based systems to improve production accuracy, reduce operational costs, and enhance quality control processes across assembly lines and production facilities

• Expanding use of robotics and automated systems in industries such as automotive, electronics, and pharmaceuticals is further driving demand for machine vision solutions. These systems enable real-time monitoring, defect detection, and process optimization, supporting higher productivity and efficiency

• Growing emphasis on reducing manufacturing errors and improving product consistency is encouraging the adoption of advanced imaging and inspection technologies. Machine vision systems are increasingly used to replace manual inspection processes and ensure higher reliability in production outcomes

• For instance, in 2023, Keyence Corporation in Japan and Omron Corporation in Japan reported increased deployment of machine vision systems in automotive and electronics manufacturing plants to enhance inspection accuracy and reduce production defects. These implementations supported higher production efficiency and improved quality assurance processes

• Although demand is rising, wider adoption depends on cost optimization, skilled workforce availability, and seamless integration with existing industrial systems. Continued investment in AI-based vision technologies and smart factory infrastructure will be critical for long-term growth

Restraint/Challenge

“High Implementation Cost And Technical Complexity”

• The high initial investment required for machine vision systems remains a key challenge, particularly for small and medium-sized manufacturers. Costs associated with advanced cameras, sensors, software, and system integration can limit adoption in price-sensitive industries

• Technical complexity in system setup, calibration, and integration with existing production lines also poses challenges for widespread deployment. Skilled professionals are required to operate and maintain these systems, which increases operational dependency and training costs

• Variability in lighting conditions, product surfaces, and production environments can impact system accuracy, requiring continuous optimization and advanced configuration. This adds to maintenance requirements and overall operational complexity

• For instance, in 2024, manufacturers in Southeast Asia and Eastern Europe reported slower adoption of machine vision systems due to high installation costs and lack of skilled technical workforce for system integration and maintenance. These challenges also led to delayed automation projects in small-scale manufacturing facilities

• Overcoming these challenges will require cost-efficient system designs, simplified integration platforms, and increased training initiatives for industrial workers. Development of plug-and-play machine vision solutions and cloud-based analytics platforms will be essential to improve accessibility and accelerate market adoption

Machine Vision Market Scope

The machine vision market is segmented into six notable segments based on type, deployment, offering, product, application, and end user.

• By Type

On the basis of type, the machine vision market is segmented into 1D Vision, 2D Vision, and 3D Vision. The 2D Vision segment held the largest market revenue share in 2025 driven by its widespread use in industrial inspection, barcode reading, and quality control applications across manufacturing environments. 2D vision systems are widely adopted due to their cost-effectiveness, ease of integration, and strong performance in standard inspection tasks, making them the most commonly used vision technology in industrial automation. These systems are extensively deployed in production lines where high-speed inspection and surface-level defect detection are required. Increasing automation in repetitive manufacturing processes further strengthens their dominance across industries. Their compatibility with existing industrial setups also supports large-scale adoption across global manufacturing hubs.

The 3D Vision segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-precision measurement, depth sensing, and advanced robotics applications. 3D vision systems are increasingly used in complex inspection tasks, such as object recognition, volume measurement, and robotic guidance in dynamic production environments. These systems are gaining traction in industries requiring high accuracy and spatial analysis, such as automotive and electronics. Rising adoption of AI-enabled robotics is further accelerating the demand for 3D imaging solutions. Continuous advancements in stereo vision and laser-based imaging technologies are enhancing system performance and reliability.

• By Deployment

On the basis of deployment, the machine vision market is segmented into General Machine Vision System and Robotic Cell. The General Machine Vision System segment held the largest market revenue share in 2025 driven by its extensive use across standalone inspection and quality control applications in manufacturing industries. These systems are widely preferred due to their flexibility, scalability, and ability to operate independently across various production lines. They are commonly used in packaging, assembly verification, and surface inspection applications. Manufacturers prefer these systems for their ease of deployment and lower integration complexity. Their adaptability across multiple industrial environments supports consistent demand.

The Robotic Cell segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of robotics integrated with vision systems for automated material handling, assembly, and inspection. Increasing demand for smart factories and fully automated production environments is further supporting the growth of robotic vision solutions. These systems enhance precision and reduce dependency on manual labor in high-speed production processes. Integration with collaborative robots is improving operational efficiency across industries. Expanding use in logistics and warehousing automation is also boosting segment growth.

• By Offering

On the basis of offering, the machine vision market is segmented into Hardware and Software. The Hardware segment held the largest market revenue share in 2025 driven by strong demand for cameras, sensors, processors, and imaging devices used in industrial inspection systems. Hardware components form the core of machine vision systems, enabling real-time image capture and processing across manufacturing applications. Increasing installation of advanced imaging sensors in production lines is supporting market expansion. Continuous improvements in camera resolution and processing speed are enhancing system capabilities. Demand from large-scale manufacturing facilities is further reinforcing hardware dominance.

The Software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of AI-based analytics, deep learning algorithms, and advanced image processing solutions. Software advancements are enhancing system intelligence, improving defect detection accuracy, and enabling predictive maintenance capabilities. Growing integration of cloud-based vision platforms is improving scalability and remote monitoring capabilities. Rising use of machine learning models is enabling adaptive inspection systems. Continuous innovation in vision algorithms is strengthening real-time decision-making applications.

• By Product

On the basis of product, the machine vision market is segmented into PC Based and Smart Camera Based. The PC Based segment held the largest market revenue share in 2025 driven by its high processing power, flexibility, and ability to handle complex inspection tasks in industrial environments. PC-based systems are widely used in large-scale manufacturing setups requiring advanced image processing and multi-camera configurations. These systems support high-performance computing for detailed inspection tasks. Their ability to integrate with multiple peripherals enhances operational efficiency. Strong adoption in heavy industries supports continued market dominance.

The Smart Camera Based segment is expected to witness the fastest growth rate from 2026 to 2033, driven by compact design, ease of installation, and integrated processing capabilities. Smart cameras reduce system complexity and cost, making them highly suitable for small and medium-sized automation applications. Their plug-and-play functionality supports faster deployment in production lines. Increasing demand for decentralized inspection systems is boosting adoption. Advancements in embedded AI processing are further improving their capabilities.

• By Application

On the basis of application, the machine vision market is segmented into Quality Assurance and Inspection, Positioning and Guidance, Measurement, Identification, and Predictive Maintenance. The Quality Assurance and Inspection segment held the largest market revenue share in 2025 driven by the growing need for defect detection, product validation, and compliance with industrial quality standards across manufacturing industries. Machine vision systems are widely used to ensure consistency and reduce production errors. Increasing focus on zero-defect manufacturing is strengthening adoption. High-speed inspection requirements in mass production are further driving demand. Integration with automated production lines enhances efficiency and accuracy.

The Predictive Maintenance segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of smart manufacturing and Industry 4.0 technologies. Machine vision systems are increasingly used to detect equipment anomalies, reduce downtime, and improve operational efficiency through early fault detection. Real-time monitoring capabilities are improving maintenance planning. Rising focus on reducing unplanned shutdowns is supporting adoption. Integration with IoT-based industrial systems is further accelerating growth.

• By End User

On the basis of end user, the machine vision market is segmented into Automotive, Electronics and Semiconductor, Consumer Electronics, Glass, Metals, Wood and Paper, Pharmaceuticals, Food and Packaging, Rubber and Plastics, Printing, Machinery/Equipment, Solar Panel Manufacturing, and Textile. The Automotive segment held the largest market revenue share in 2025 driven by extensive use of machine vision systems for assembly line inspection, quality control, and robotic automation in vehicle manufacturing. Increasing vehicle production and electrification trends are further supporting demand. Machine vision ensures high precision in welding, painting, and assembly processes. Adoption of automated inspection systems is improving production efficiency. Strong investment in smart automotive factories is reinforcing market leadership.

The Electronics and Semiconductor segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for precision inspection, miniaturized components, and high-speed defect detection in semiconductor fabrication and electronics assembly processes. Increasing complexity of semiconductor devices is boosting reliance on advanced vision systems. Growing production of consumer electronics is further supporting demand. High accuracy requirements in chip manufacturing are accelerating adoption. Expansion of global semiconductor manufacturing capacity is strengthening long-term growth prospects.

Machine Vision Market Regional Analysis

• North America dominated the machine vision market with the largest revenue share in 2025, driven by strong industrial automation adoption, advanced manufacturing infrastructure, and rapid integration of AI-based inspection systems

• Manufacturers in the region highly value the accuracy, speed, and efficiency offered by machine vision systems for quality control, defect detection, and process optimization across automotive, electronics, and semiconductor industries

• This widespread adoption is further supported by high investments in smart factories, presence of leading technology providers, and growing demand for robotics-based automation, establishing machine vision as a key enabler of Industry 4.0 transformation

U.S. Machine Vision Market Insight

The U.S. machine vision market captured the largest revenue share in 2025 within North America, fueled by rapid deployment of AI-enabled inspection systems and strong demand from automotive and electronics manufacturing sectors. Companies are increasingly adopting machine vision solutions to enhance production efficiency, reduce defects, and support high-speed automated assembly lines. The presence of leading technology providers and continuous innovation in imaging hardware and software are further accelerating market growth. In addition, integration of machine vision with robotics, IoT platforms, and cloud-based analytics is significantly strengthening industrial automation across the country.

Europe Machine Vision Market Insight

The Europe machine vision market is expected to witness strong growth from 2026 to 2033, primarily driven by increasing adoption of smart manufacturing, strict quality standards, and rising demand for industrial automation. European manufacturers are increasingly integrating machine vision systems into production lines to improve precision, reduce operational errors, and enhance productivity. The region’s strong focus on sustainability and energy-efficient manufacturing is also supporting the deployment of advanced inspection technologies. Growth is further supported by widespread adoption across automotive, pharmaceutical, and electronics industries.

Germany Machine Vision Market Insight

The Germany machine vision market held the largest market share in Europe in 2025, driven by its highly developed industrial base, strong automotive manufacturing sector, and leadership in engineering innovation. Germany’s emphasis on Industry 4.0 and smart factory implementation has significantly boosted the adoption of machine vision systems across production facilities. The country’s focus on precision engineering, quality assurance, and automation integration further strengthens demand. In addition, increasing use of AI-powered inspection systems in automotive and semiconductor manufacturing is reinforcing Germany’s dominance in the regional market.

U.K. Machine Vision Market Insight

The U.K. machine vision market is expected to witness steady growth from 2026 to 2033, driven by increasing automation in manufacturing and rising adoption of advanced quality inspection systems. Industries in the U.K. are focusing on improving production efficiency and reducing defects through AI-based vision technologies. Growing investments in smart manufacturing and robotics integration are further supporting market expansion. In addition, strong demand from packaging, pharmaceuticals, and electronics sectors is contributing to the rising adoption of machine vision solutions across the country.

Asia-Pacific Machine Vision Market Insight

The Asia-Pacific machine vision market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, expanding electronics manufacturing, and increasing adoption of automation technologies. Countries such as China, Japan, and India are heavily investing in smart factories and advanced production systems. Rising demand for high-speed inspection and quality control in mass production industries is further boosting market growth. In addition, the region’s strong manufacturing base and cost-effective production capabilities are accelerating machine vision deployment across multiple industries.

Japan Machine Vision Market Insight

The Japan machine vision market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced robotics ecosystem, high automation levels, and strong focus on precision manufacturing. Japanese industries widely adopt machine vision systems for electronics, automotive, and semiconductor production to ensure high accuracy and defect-free output. The integration of AI and robotics with vision systems is further enhancing productivity and operational efficiency. In addition, Japan’s aging workforce is increasing reliance on automated inspection systems across industrial applications.

China Machine Vision Market Insight

The China machine vision market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrial expansion, strong manufacturing output, and widespread adoption of smart factory technologies. China is a global hub for electronics and automotive production, driving significant demand for machine vision systems in quality inspection and automation processes. Government initiatives supporting industrial modernization and smart manufacturing are further boosting market growth. The presence of strong domestic manufacturers and cost-effective solutions is also enhancing market penetration across various industries.

Machine Vision Market Share

The machine vision industry is primarily led by well-established companies, including:

• Baumer (Switzerland)

• MVTEC SOFTWARE GMBH (Germany)

• Tordivel AS (Norway)

• JAI A/S (Denmark)

• Intel Corporation (U.S.)

• Sony Corporation (Japan)

• KEYENCE CORPORATION (Japan)

• COGNEX CORPORATION (U.S.)

• Inuitive (Israel)

• Teledyne FLIR LLC (U.S.)

• Qualitas Technologies (India)

• Sick AG (Germany)

• Basler AG (Germany)

• ISRA VISION AG (Germany)

• Cadence Design Systems, Inc. (U.S.)

• CEVA, Inc. (U.S.)

• OMRON Corporation (Japan)

• Texas Instruments Incorporated (U.S.)

• Allied Vision Technologies GmbH (Germany)

• Teledyne Technologies Incorporated (U.S.)

Latest Developments in Global Machine Vision Market

- In July 2024, OMRON Corporation introduced a software update for its FH Vision System and FHV7 Smart Camera, integrating advanced digital watermark decoding technology to enable high-speed and precise product identification in packaging lines. This development enhances inspection accuracy at speeds exceeding 2,000 parts per minute while improving traceability and quality assurance for consumer goods manufacturers. The update strengthens OMRON’s position in AI-enabled inspection systems and supports the growing demand for high-efficiency automated quality control, positively impacting the machine vision market through improved operational performance and scalability

- In June 2024, SICK AG launched the Inspector83x 2D vision sensor, a standalone AI-enabled inspection solution designed for defect detection, sorting, and OCR/OCV applications. The system processes up to 15 inspections per second and allows quick AI training directly on the device, improving ease of deployment and operational flexibility. This innovation enhances inspection efficiency, reduces setup time, and supports smart manufacturing adoption, driving increased demand for compact and intelligent vision sensors across industrial applications

- In April 2024, Cognex Corporation introduced the In-Sight L38 3D Vision System, an AI-powered solution combining 2D and 3D vision technologies for advanced inspection in manufacturing automation. The system simplifies deployment and improves detection of complex features not visible with traditional imaging, enabling faster and more reliable inspections. This launch strengthens Cognex’s product portfolio and accelerates the adoption of AI-driven 3D vision systems, contributing to higher accuracy and productivity in industrial operations

- In March 2024, Cognex Corporation expanded its product portfolio with an advanced vision tunnel integrated with the DataMan 380 barcode reader, designed to enhance traceability and high-throughput inspection in logistics and manufacturing environments. The system improves barcode reading accuracy and supports large-scale automated operations, enabling efficient tracking and quality control. This development boosts demand for integrated vision solutions and supports the expansion of smart logistics and automated production systems

- In January 2024, CGI Inc. launched its AI-driven machine vision solution designed to extract data from IoT sensors using deep neural network technologies. The solution enables businesses to optimize processes, improve operational efficiency, and reduce costs through advanced analytics and real-time insights. This innovation supports the growing integration of AI and IoT in industrial environments, strengthening the role of intelligent vision systems in digital transformation initiatives

- In 2024, KEYENCE Corporation introduced multiple advanced sensing and inspection solutions including a 3D laser snapshot sensor and portable 3D scanning systems, designed for high-precision measurement and inspection across complex industrial applications. These systems improve flexibility, accuracy, and portability in inspection processes while supporting non-contact measurement capabilities. The developments enhance productivity and quality assurance, reinforcing the adoption of advanced machine vision technologies across manufacturing industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.