Global Mandibular Osteomyelitis Treatment Market

Market Size in USD Billion

USD

89.05 Billion

USD

143.00 Billion

2025

2033

USD

89.05 Billion

USD

143.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 89.05 Billion | |

| USD 143.00 Billion | |

| % | |

|

Mandibular Osteomyelitis Treatment Market Size

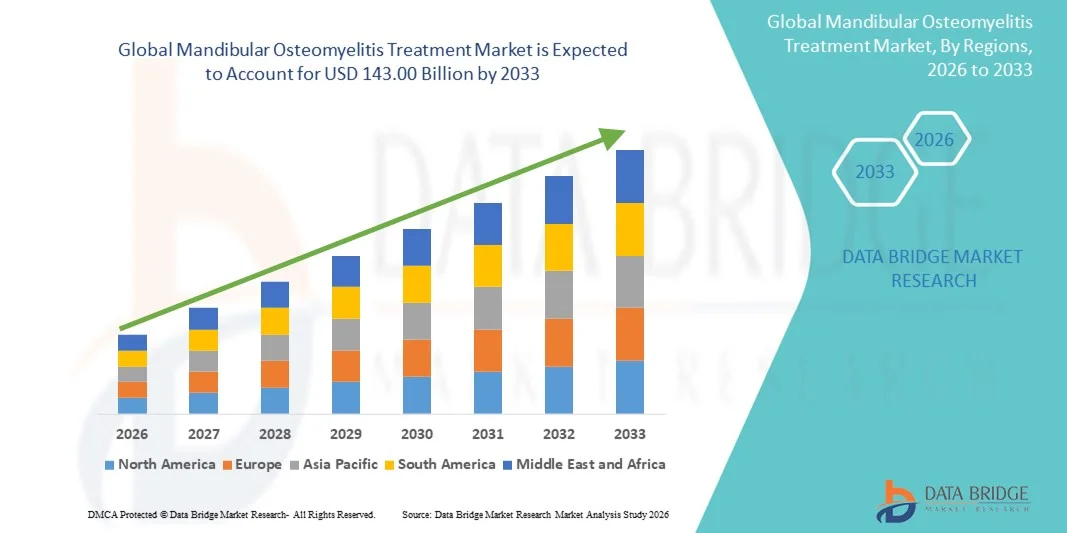

- The global mandibular osteomyelitis treatment market size was valued at USD 89.05 billion in 2025 and is expected to reach USD 143.00 billion by 2033, at a CAGR of 6.10% during the forecast period

- The market growth is largely fueled by the rising prevalence of oral infections, increasing cases of trauma-related jaw complications, and the growing demand for advanced dental and maxillofacial treatments in both hospital and clinical settings

- Furthermore, increasing awareness about early diagnosis and effective management of mandibular osteomyelitis, combined with technological advancements in imaging, surgical procedures, and antibiotic therapies, is driving the adoption of Mandibular Osteomyelitis Treatment solutions, thereby significantly boosting the industry's growth

Mandibular Osteomyelitis Treatment Market Analysis

- Mandibular Osteomyelitis Treatment, encompassing advanced surgical interventions, targeted antibiotic therapies, and supportive care, is increasingly vital in managing severe jawbone infections and related complications in both hospital and clinical settings

- The escalating demand for Mandibular Osteomyelitis Treatment is primarily fueled by the rising prevalence of oral infections, trauma cases, and an increasing focus on early diagnosis and effective treatment strategies to prevent long-term complications

- North America dominated the mandibular osteomyelitis treatment market with the largest revenue share of 43.00% in 2025, characterized by well-established healthcare infrastructure, high adoption of advanced dental and maxillofacial treatment modalities, and the strong presence of key pharmaceutical and medical device companies, with the U.S. experiencing substantial growth due to expanding clinical research, hospital-based therapies, and adoption of innovative treatment protocols

- Asia-Pacific is expected to be the fastest growing region in the mandibular osteomyelitis treatment market during the forecast period due to increasing healthcare investments, rising prevalence of oral and maxillofacial infections, expansion of specialized clinics, and improving healthcare infrastructure across emerging economies

- The Staphylococcus Bacteria segment dominated the market, accounting for 52.7% revenue in 2025, owing to its high prevalence in post-traumatic and postoperative mandibular infections

Report Scope and Mandibular Osteomyelitis Treatment Market Segmentation

|

Attributes |

Mandibular Osteomyelitis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Mandibular Osteomyelitis Treatment Market Trends

Enhanced Patient Outcomes Through Advanced Treatment Modalities

- A significant and accelerating trend in the global mandibular osteomyelitis treatment market is the increasing adoption of advanced surgical techniques, targeted antimicrobial therapies, and comprehensive post-operative care protocols. These improvements are significantly enhancing patient outcomes and reducing the morbidity associated with severe mandibular infections

- For instance, the use of hyperbaric oxygen therapy (HBOT) alongside combination antibiotic regimens enables clinicians to manage necrotic bone tissue more effectively, reducing infection recurrence and accelerating healing. Similarly, minimally invasive surgical debridement methods allow for precise removal of infected tissue while preserving healthy mandibular structures, offering patients improved recovery experiences

- Integration of imaging technologies such as 3D CT scans and MRI into treatment planning enables more accurate identification of infection extent, guiding surgical intervention and optimizing antimicrobial therapy selection

- Point-of-care microbiological testing and rapid culture analysis facilitate immediate clinical decision-making, enabling timely initiation of targeted antibiotics and reducing reliance on broad-spectrum therapies

- This trend towards more precise, timely, and integrated treatment approaches is fundamentally reshaping clinician expectations for Mandibular Osteomyelitis management. Consequently, specialized centers are adopting multidisciplinary care protocols involving maxillofacial surgeons, infectious disease specialists, and radiologists to ensure comprehensive patient care

- The demand for improved treatment protocols, early detection strategies, and multidisciplinary intervention is growing rapidly across hospitals, specialty clinics, and research institutions, as healthcare providers increasingly prioritize reducing complications and improving quality of life for affected patients

Mandibular Osteomyelitis Treatment Market Dynamics

Driver

Rising Focus on Early Diagnosis and Minimally Invasive Therapies

- The increasing emphasis on early detection of mandibular infections, combined with advancements in diagnostic imaging and laboratory techniques, is a significant trend driving improved patient management

- For instance, hospitals are increasingly adopting rapid microbiological assays and advanced imaging modalities to identify infection at earlier stages, allowing timely intervention before severe bone necrosis occurs

- Minimally invasive surgical procedures, including laser-assisted debridement and ultrasonic bone cutting, are increasingly used to limit tissue damage and improve functional outcomes

- Integration of comprehensive post-operative care, including targeted antimicrobial therapy, pain management, and nutritional support, is enhancing patient recovery and reducing hospitalization time

- These trends are supported by growing awareness among clinicians and patients regarding the importance of early intervention and the long-term benefits of optimized treatment protocols

- The adoption of standardized clinical guidelines and evidence-based treatment pathways is further shaping market growth and ensuring consistent patient outcomes

Restraint/Challenge

High Treatment Costs and Limited Access to Specialized Care

- The high cost associated with advanced surgical procedures, long-term hospitalization, and specialized antimicrobial therapies presents a significant challenge to broader market adoption, particularly in low- and middle-income regions

- Limited access to specialized maxillofacial surgeons, infectious disease experts, and modern diagnostic facilities in certain regions can delay treatment, increasing patient morbidity and healthcare burden

- For instance, in 2024, a study conducted in rural India reported delays in surgical intervention for mandibular osteomyelitis patients due to unavailability of trained maxillofacial surgeons, resulting in prolonged infection and increased complication rates

- Addressing these challenges requires development of cost-effective treatment protocols, wider distribution of diagnostic capabilities, and training of healthcare personnel to manage complex mandibular infections efficiently

- The prolonged recovery period and need for multidisciplinary intervention can also act as a barrier for patient compliance and timely management

- While government and private healthcare initiatives are gradually improving access, the gap in availability of specialized treatment options still limits market penetration in emerging economies

- Overcoming these challenges through investment in infrastructure, healthcare professional training, and affordable therapeutic solutions will be vital for sustained growth of the Mandibular Osteomyelitis Treatment market

Mandibular Osteomyelitis Treatment Market Scope

The market is segmented on the basis of types, symptoms, treatment, cause, end-users, and distribution channel.

- By Types

On the basis of types, the Mandibular Osteomyelitis Treatment market is segmented into Acute and secondary chronic osteomyelitis, and Primary chronic osteomyelitis. The Acute and secondary chronic osteomyelitis segment dominated the market with a revenue share of 47.3% in 2025, driven by its high prevalence in post-traumatic infections, dental procedures, and systemic comorbidities. This segment is characterized by rapid onset and progression of infection, necessitating immediate clinical intervention. Hospitals and clinics often prioritize early diagnosis and aggressive management through intravenous antibiotics and supportive therapies, generating substantial revenue. The widespread awareness of the complications arising from delayed treatment, such as bone necrosis and abscess formation, further reinforces segment dominance. Acute infections require frequent monitoring and often involve multiple treatment modalities, including steroids, surgery, and chemotherapeutic agents. Emerging research and diagnostic advancements, such as advanced imaging and laboratory tests, improve detection and treatment efficacy, boosting hospital utilization. The presence of high-risk patient populations, including diabetics and immunocompromised individuals, ensures sustained market demand. Insurance and government healthcare coverage for acute osteomyelitis treatment enhance adoption rates. Preventive protocols in dental and surgical procedures also contribute to early detection and revenue generation. Clinical guidelines emphasize immediate intervention, increasing the overall market share. Hospitals with well-equipped emergency and dental units continue to adopt best practices for managing acute cases. The adoption of combination therapy strategies enhances treatment outcomes and strengthens market leadership.

The Primary chronic osteomyelitis segment is expected to witness the fastest CAGR of 19.1% from 2026 to 2033, largely driven by its complex, long-term treatment requirements and increasing prevalence in aging populations. Chronic cases often require a combination of surgery, bisphosphonates, and prolonged chemotherapeutic regimens, leading to higher revenue per patient. Hospitals and specialty dental centers increasingly invest in advanced imaging technologies and surgical equipment to manage these complex cases. Early detection is facilitated by enhanced diagnostic protocols including MRI and laboratory testing. Chronic osteomyelitis cases are more frequent in patients with comorbidities, including diabetes and immune disorders, driving adoption of comprehensive treatment plans. Ongoing research in osteomyelitis pathogenesis supports the development of targeted therapies, further boosting market growth. The segment benefits from higher insurance reimbursement rates for complex cases, encouraging hospitals to expand treatment capacity. Patient awareness campaigns emphasize the importance of early intervention, improving treatment adherence. Increasing demand for home healthcare and follow-up care services also supports the segment’s rapid growth. The segment sees rising adoption of combination treatment strategies to reduce recurrence rates, enhancing clinical outcomes. Hospital and diagnostic center collaborations streamline treatment workflows, improving efficiency and revenue. The chronic nature of the condition ensures sustained demand for long-term pharmaceutical interventions. Advanced surgical interventions, including bone grafts and reconstructive procedures, contribute significantly to market expansion.

- By Symptoms

On the basis of symptoms, the market is segmented into fever, fatigue, pain, swelling, and redness over the area of infection. The pain segment dominated the market, accounting for 42.8% revenue in 2025, as pain is the most immediate and noticeable symptom prompting patients to seek clinical attention. Hospitals and clinics report high patient inflow due to localized mandibular pain, which accelerates diagnostic testing and treatment initiation. Pain management often involves analgesics, steroids, and adjunct therapies, contributing to overall market revenue. The segment benefits from heightened awareness among dentists and healthcare providers to address pain promptly to prevent progression. Chronic and acute osteomyelitis patients alike report pain, which drives repeat hospital visits and follow-ups. Early treatment of pain helps mitigate complications such as abscess formation and bone necrosis. Pain symptoms often correlate with swelling and redness, enabling faster clinical diagnosis and intervention. Treatment regimens targeting pain relief complement primary therapies like antibiotics or surgical procedures. Pain-focused therapies increase demand for pharmaceutical products and hospital services. Telehealth platforms also support early assessment of pain symptoms, accelerating patient care. Hospitals implement pain management protocols as part of comprehensive treatment plans. Patient education on symptom recognition boosts timely hospital visits. The rising prevalence of post-surgical and post-traumatic infections further reinforces segment dominance.

The swelling segment is expected to witness the fastest CAGR of 17.6% from 2026 to 2033, driven by its role as an early and visually detectable sign of infection. Swelling prompts patients to seek urgent care, accelerating the adoption of diagnostic tests and treatment interventions. Hospitals and diagnostic centers increasingly utilize advanced imaging techniques to evaluate the extent of swelling and tissue involvement. Swelling management often requires combination therapies including steroids, surgery, and antibiotics, enhancing market revenue. The segment benefits from public awareness campaigns highlighting the importance of early symptom recognition. Dental and surgical clinics emphasize prompt management of swelling to prevent systemic infection. Advanced protocols for anti-inflammatory treatment and localized intervention are being adopted in high-volume centers. Rising prevalence of comorbidities that exacerbate swelling, such as diabetes and immune disorders, fuels market growth. Swelling monitoring supports long-term follow-up care, boosting home healthcare adoption. Increasing collaborations between hospitals and specialty clinics enhance patient access to treatment. Hospitals leverage swelling symptoms to triage and prioritize care efficiently. Early recognition of swelling improves treatment outcomes and reduces recurrence. The segment is further driven by technological advancements in non-invasive imaging tools for inflammation assessment.

- By Treatment

On the basis of treatment, the market is segmented into steroids, chemotherapeutic agents, bisphosphonates, and surgery. The steroids segment dominated the market, with 48.1% revenue in 2025, due to their effectiveness in reducing inflammation and alleviating pain in both acute and chronic mandibular osteomyelitis cases. Steroids are frequently prescribed in conjunction with antibiotics and surgical interventions, increasing market revenue. Hospitals and clinics rely on steroid therapy to manage inflammation, prevent tissue damage, and improve patient comfort. Clinical guidelines emphasize early steroid administration to complement antimicrobial therapy. The segment benefits from continuous development of novel formulations and delivery mechanisms. Steroids are widely available across hospital pharmacies, retail outlets, and online channels, supporting broad adoption. Reimbursement policies for hospital-administered steroids enhance utilization. Steroids’ rapid symptom relief encourages adherence, improving patient outcomes. Specialist dental clinics and maxillofacial centers routinely incorporate steroids into treatment regimens. Hospitals invest in training programs for physicians and nurses to optimize steroid therapy. Public awareness regarding inflammatory management boosts demand. Emerging research on steroid combination therapies enhances efficacy. Hospitals and pharmacies benefit from bulk procurement, contributing to segment dominance.

The surgery segment is expected to witness the fastest CAGR of 18.4% from 2026 to 2033, driven by increasing incidence of severe osteomyelitis requiring debridement or reconstructive procedures. Surgical intervention is often the definitive therapy for chronic or refractory cases, resulting in high hospital revenue. Hospitals and specialized surgical centers invest in advanced operative equipment and training to improve patient outcomes. The segment benefits from the growing number of dental and maxillofacial surgeries worldwide. Insurance coverage and reimbursement for complex surgeries support adoption. Ongoing research into minimally invasive and reconstructive techniques drives faster procedural adoption. Surgical intervention ensures long-term management and reduces recurrence, increasing follow-up care revenue. Hospitals integrate surgery with adjunct therapies like steroids and antibiotics for comprehensive care. Rising patient awareness about the risks of untreated osteomyelitis fuels demand for early surgical intervention. Collaborations between hospitals and diagnostic centers facilitate pre-surgical planning and accurate assessment. Telehealth consultations help in triaging surgical cases efficiently. Training programs and continuing education for surgeons support growth. Technological advancements, such as 3D imaging and surgical navigation, further enhance segment adoption.

- By Cause

On the basis of cause, the market is segmented into Staphylococcus Bacteria. The Staphylococcus Bacteria segment dominated the market, accounting for 52.7% revenue in 2025, owing to its high prevalence in post-traumatic and postoperative mandibular infections. Hospitals and clinics often perform culture tests and sensitivity analyses to guide targeted antibiotic therapy, enhancing market expenditure. The segment benefits from widespread awareness and diagnostic capabilities to identify Staphylococcus-related infections promptly. Treatment often involves combination therapy, including antibiotics, steroids, and surgical intervention. Ongoing research into Staphylococcus virulence factors supports development of advanced therapeutic strategies. Hospitals’ infection control protocols prioritize management of Staphylococcus infections. Public health campaigns emphasize hygiene and post-surgical care to reduce bacterial spread. Laboratory testing and imaging integration support accurate diagnosis and effective management. Hospital pharmacy procurement of antibiotics targeting Staphylococcus enhances revenue. The segment is further strengthened by increasing resistance trends, necessitating advanced treatment options. Awareness programs for dentists and maxillofacial surgeons contribute to rapid recognition. Hospitals adopt early intervention protocols to minimize complications and recurrence.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, diagnostic centres, home healthcare, and others. The hospitals segment dominated the market, with 50.3% revenue in 2025, due to their capability to provide comprehensive care including diagnosis, surgery, and post-operative management. Hospitals are equipped with advanced imaging, laboratory, and surgical facilities, ensuring effective treatment. Combination therapy protocols and intensive care support enhance hospital revenue. Hospitals are primary treatment centers for acute and severe chronic cases. Insurance reimbursement policies favor hospital care, increasing adoption. Hospitals maintain high patient inflow due to emergency admissions and referral networks. Rising prevalence of comorbidities ensures consistent demand. Hospitals’ adoption of technological advancements, such as imaging and surgical navigation, supports growth. Specialized departments handle complex mandibular osteomyelitis cases efficiently. Hospitals’ integration with diagnostic centers improves treatment outcomes. Government programs and clinical guidelines reinforce hospital dominance. Hospitals’ centralized care and multidisciplinary approach sustain market leadership.

The home healthcare segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, driven by growing patient preference for at-home follow-up care and post-surgical monitoring. Remote monitoring, telehealth consultations, and home delivery of medications accelerate adoption. Home healthcare ensures convenience, reduces hospital visits, and improves treatment adherence. Rising awareness among patients about the benefits of home-based care supports segment growth. Integration of home healthcare with hospital and diagnostic services enhances continuity of care. Advanced monitoring devices enable timely detection of complications. Insurance coverage for home healthcare services facilitates adoption. Patients with mobility constraints particularly benefit from home-based follow-up and treatment. Telemedicine adoption promotes early symptom reporting and management. Home healthcare providers collaborate with clinics for medication management. Education programs for caregivers improve service quality. Growth in chronic osteomyelitis cases fuels demand for home-based interventions. Home healthcare reduces hospital burden while maintaining high-quality patient care.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market, with 48.9% revenue in 2025, due to immediate availability of critical medications such as antibiotics, steroids, and adjunct therapy agents. Hospital pharmacies ensure uninterrupted supply during emergency treatments. Bulk procurement and centralized inventory management enhance segment dominance. Policies supporting drug availability for high-risk patients reinforce adoption. Hospital pharmacy integration with clinical departments ensures timely treatment delivery. Hospitals maintain strategic partnerships with pharmaceutical companies for consistent drug supply. Advanced pharmacy systems support accurate inventory tracking and dispensing. Insurance and government healthcare coverage promote hospital pharmacy utilization. Hospital pharmacies provide combination therapies in a controlled setting, improving outcomes. Staff training ensures correct dispensing and patient safety. Hospitals leverage in-house pharmacies for cost control and quality assurance. Emergency preparedness protocols emphasize hospital pharmacy readiness. Hospital pharmacies remain the primary channel for critical medication access.

The online pharmacy segment is expected to witness the fastest CAGR of 20.7% from 2026 to 2033, driven by the increasing adoption of e-prescriptions, telehealth consultations, and home delivery of medications. Online platforms enhance accessibility, particularly for patients in remote or underserved regions. Integration with hospital and diagnostic systems ensures timely fulfillment of prescribed treatments. Digital tools, such as mobile apps and reminders, improve adherence to therapy. Online pharmacies expand geographic reach, providing access to specialty drugs not available locally. Subscription services and repeat delivery options support patient convenience. Cold-chain logistics and advanced packaging enhance drug safety. Online pharmacies collaborate with clinics and hospitals for seamless medication management. Patient awareness campaigns highlight online convenience, driving adoption. Insurance and reimbursement policies gradually accommodate online medication delivery. Rapid delivery and home convenience appeal to chronic care patients. E-commerce growth and internet penetration accelerate market expansion. Online pharmacies’ ability to deliver critical drugs efficiently ensures sustained growth.

Mandibular Osteomyelitis Treatment Market Regional Analysis

- North America dominated the mandibular osteomyelitis treatment market with the largest revenue share of 43.00% in 2025

- Supported by a well-established healthcare infrastructure, high adoption of advanced dental and maxillofacial treatment modalities, and a strong presence of key pharmaceutical and medical device companies

- The market leads the regional market due to expanding clinical research initiatives, hospital-based therapies, and the adoption of innovative treatment protocols, including combination antibiotic therapy and surgical debridement techniques

U.S. Mandibular Osteomyelitis Treatment Market Insight

The U.S. mandibular osteomyelitis treatment market captured the largest revenue share within North America in 2025, driven by extensive clinical trials, high healthcare expenditure, and the adoption of advanced diagnostic imaging such as CT scans and MRI. Hospitals and specialized clinics are increasingly implementing combination therapies, personalized treatment plans, and postoperative care protocols to improve recovery rates. Government support for oral health research and strong collaboration between medical institutions and pharmaceutical companies further propel market growth.

Europe Mandibular Osteomyelitis Treatment Market Insight

The Europe mandibular osteomyelitis treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing incidence of dental and maxillofacial infections, rising awareness regarding early diagnosis, and the availability of advanced therapeutic solutions. Countries such as Germany, the U.K., and France are witnessing significant adoption of surgical interventions, hyperbaric oxygen therapy, and combination drug regimens. The growth is also supported by government initiatives promoting oral health, modern hospital infrastructure, and enhanced access to specialized care centers.

U.K. Mandibular Osteomyelitis Treatment Market Insight

The U.K. mandibular osteomyelitis treatment market is anticipated to grow at a notable CAGR during the forecast period, fueled by rising cases of oral infections, increasing dental awareness, and growing adoption of intravenous antibiotics and surgical treatments. Expansion of specialized clinics, investment in healthcare infrastructure, and the integration of advanced diagnostic imaging are supporting enhanced treatment outcomes and higher patient access to quality care.

Germany Mandibular Osteomyelitis Treatment Market Insight

The Germany mandibular osteomyelitis treatment market is expected to expand significantly during the forecast period, driven by high healthcare standards, rising awareness of maxillofacial infections, and the adoption of novel treatment protocols including bisphosphonates and surgical interventions. The presence of advanced hospitals and research institutions, coupled with initiatives to improve early diagnosis and intervention strategies, is further strengthening market growth across clinical and hospital settings.

Asia-Pacific Mandibular Osteomyelitis Treatment Market Insight

The Asia-Pacific mandibular osteomyelitis treatment market is expected to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, rising prevalence of oral and maxillofacial infections, expansion of specialized clinics, and improving healthcare infrastructure across emerging economies such as China, India, and Japan. The region benefits from the growing adoption of advanced diagnostic and treatment modalities, coupled with an increasing focus on patient-centric care and early intervention.

Japan Mandibular Osteomyelitis Treatment Market Insight

The Japan mandibular osteomyelitis treatment market is witnessing steady growth due to high awareness of oral and maxillofacial health, rising cases of mandibular infections, and advanced treatment facilities. The country’s well-established healthcare system supports the adoption of combination antibiotic therapy, surgical interventions, and postoperative monitoring, enhancing patient outcomes in both clinical and hospital settings.

China Mandibular Osteomyelitis Treatment Market Insight

The China mandibular osteomyelitis treatment market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising healthcare expenditure, growing incidence of oral and maxillofacial infections, and expansion of specialized hospitals and clinics. Increased availability of advanced diagnostic techniques, combination drug therapies, and surgical interventions, along with government initiatives to strengthen healthcare infrastructure, is driving market growth in China.

Mandibular Osteomyelitis Treatment Market Share

The Mandibular Osteomyelitis Treatment industry is primarily led by well-established companies, including:

- Pfizer (U.S.)

- Novartis (Switzerland)

- Roche (Switzerland)

- Johnson & Johnson (U.S.)

- GlaxoSmithKline (U.K.)

- AstraZeneca (U.K.)

- Merck & Co. (U.S.)

- Bayer AG (Germany)

- Sanofi (France)

- Amgen (U.S.)

- Celgene (U.S.)

- Teva Pharmaceutical Industries (Israel)

- Boehringer Ingelheim (Germany)

- Eli Lilly and Company (U.S.)

- Fresenius Kabi (Germany)

- AbbVie (U.S.)

- Biocon (India)

- Dr. Reddy’s Laboratories (India)

- Cipla (India)

- Hikma Pharmaceuticals (U.K.)

Latest Developments in Global Mandibular Osteomyelitis Treatment Market

- In April 2021, researchers published on strontium‑releasing mesoporous bioactive glasses with antibacterial and bone-regenerative properties, potentially relevant to treating bone infections, including mandibular osteomyelitis. This development highlights the advancement of biomaterials aimed at improving healing and reducing infection recurrence

- In August 2024, nanoparticle-based drug delivery systems were reported to drive growth in the global osteomyelitis market, offering more targeted therapies for bone infections. These technologies enable precise delivery of antibiotics to infected sites, potentially improving outcomes and reducing systemic side effects

- In September 2024, Hikma Pharmaceuticals introduced a clindamycin intravenous injection (with 5% dextrose) for severe infections, including bone infections. This launch reflects the increasing demand for effective antimicrobial therapies to manage complex osteomyelitis cases

- In March 2024, BiomX Inc. acquired Adaptive Phage Therapeutics to advance phage therapy for chronic osteomyelitis. The acquisition aims to develop bacteriophage-based treatments capable of targeting antibiotic-resistant bacterial strains, offering a novel therapeutic option for patients with persistent bone infections

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.