Global Maritime Patrol Aircraft Market

Market Size in USD Billion

USD

10.14 Billion

USD

15.01 Billion

2025

2033

USD

10.14 Billion

USD

15.01 Billion

2025

2033

| 2026 - 2033 | |

| USD 10.14 Billion | |

| USD 15.01 Billion | |

| % | |

|

Maritime Patrol Aircraft Market Size

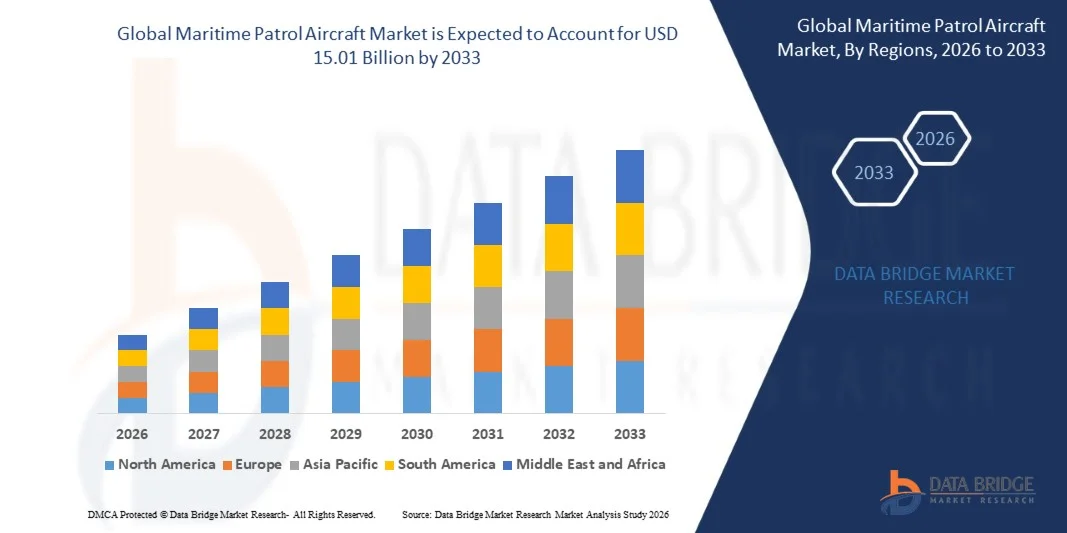

- The global maritime patrol aircraft market size was valued at USD 10.14 billion in 2025 and is expected to reach USD 15.01 billion by 2033, at a CAGR of 5.03% during the forecast period

- The market growth is largely fueled by rising defense modernization programs and the increasing need for advanced maritime surveillance, anti-submarine warfare, and reconnaissance capabilities, driving demand for technologically sophisticated patrol aircraft

- Furthermore, growing investments in long-endurance, sensor-equipped aircraft by navies and coast guards are enhancing operational readiness and multi-mission capabilities, accelerating fleet upgrades and strengthening the overall market expansion

Maritime Patrol Aircraft Market Analysis

- Maritime patrol aircraft, equipped with advanced radar, cameras, and multi-sensor systems, are becoming essential for coastal security, anti-piracy operations, and strategic maritime reconnaissance, serving both national defense and allied operations

- The escalating demand for these aircraft is primarily fueled by territorial maritime disputes, modernization of naval fleets, rising defense budgets, and the need for integrated, high-endurance surveillance solutions to maintain maritime domain awareness

- North America dominated the maritime patrol aircraft market with a share of 38.7% in 2025, due to rising defense modernization programs, strategic maritime surveillance requirements, and high defense expenditure

- Asia-Pacific is expected to be the fastest growing region in the maritime patrol aircraft market during the forecast period due to rising defense budgets, territorial maritime disputes, and modernization of naval fleets in countries such as China, India, and Japan

- Armoured segment dominated the market with a market share of 58.3% in 2025, due to its enhanced survivability in hostile maritime environments and robust protection against small arms fire and surface threats. Navies and coast guards often prioritize armoured variants for long-duration patrols and anti-submarine operations due to their reinforced airframe and onboard safety systems

Report Scope and Maritime Patrol Aircraft Market Segmentation

|

Attributes |

Maritime Patrol Aircraft Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Maritime Patrol Aircraft Market Trends

“Increasing Integration of Multi-Sensor and Long-Endurance Surveillance Systems”

- A notable trend in the maritime patrol aircraft market is the growing integration of multi-sensor suites and long-endurance surveillance capabilities, driven by the need for enhanced maritime domain awareness and persistent monitoring over vast oceanic regions. These integrated systems combine radar, electro-optical/infrared (EO/IR) sensors, magnetic anomaly detectors, and signal intelligence equipment to provide comprehensive situational awareness and intelligence gathering for naval and coast guard operations

- For instance, Boeing’s P-8A Poseidon is equipped with advanced multi-sensor suites including AN/APY-10 radar, acoustic sensors, and electronic support measures that allow extended maritime patrol and anti-submarine warfare missions. This combination of sensors enables operators to detect, track, and classify surface and subsurface targets across large operational theaters

- There is increasing adoption of long-endurance unmanned aerial vehicles (UAVs) in maritime surveillance, complementing manned patrol aircraft. UAVs such as Northrop Grumman’s MQ-4C Triton provide extended flight durations and real-time data relay, enhancing maritime reconnaissance capabilities and persistent intelligence collection

- The integration of advanced data fusion and mission management systems is improving operational efficiency by consolidating inputs from multiple sensors into actionable intelligence. This trend supports more precise decision-making in naval and coast guard missions, particularly in search and rescue, anti-piracy, and border monitoring operations

- Defense agencies are focusing on multi-role patrol aircraft that combine surveillance, anti-submarine warfare, and electronic intelligence functions. This holistic approach reduces fleet complexity, enhances mission flexibility, and increases return on investment in high-value maritime platforms

- The market is witnessing strong interest in next-generation maritime patrol platforms capable of operating in contested environments with network-centric capabilities. The emphasis on interoperability, long-range communications, and advanced surveillance systems continues to drive innovation in multi-sensor maritime patrol aircraft

Maritime Patrol Aircraft Market Dynamics

Driver

“Rising Defense Modernization Programs and Maritime Security Requirements”

- The growing emphasis on naval modernization and strengthening maritime security is driving investments in advanced patrol aircraft capable of addressing emerging threats across littoral and open-ocean environments. Governments are upgrading fleets to maintain strategic deterrence, enhance intelligence collection, and improve operational readiness

- For instance, the Indian Navy has procured Boeing P-8I Poseidon aircraft as part of its modernization program to strengthen anti-submarine warfare and maritime reconnaissance capabilities. These aircraft enhance the Navy’s ability to monitor critical sea lanes and respond effectively to regional maritime threats

- Increasing geopolitical tensions in maritime zones are prompting nations to acquire long-range, multi-role patrol platforms that can provide early warning, intelligence gathering, and surveillance capabilities. This strategic requirement underpins defense procurement decisions and fleet expansion

- Allied and regional navies are increasingly seeking interoperability with NATO and other coalition forces, requiring patrol aircraft that can operate in joint missions with advanced communication and sensor-sharing capabilities. This integration strengthens collaborative maritime security frameworks

- The rise in piracy, smuggling, and illegal fishing activities in key international waters is intensifying demand for maritime patrol aircraft. These platforms provide a persistent aerial presence, supporting law enforcement and safeguarding national maritime interests

Restraint/Challenge

“High Procurement and Operational Costs of Advanced Patrol Aircraft”

- The maritime patrol aircraft market faces challenges due to the substantial investment required for procurement, integration of sophisticated sensors, and ongoing operational expenditures. High lifecycle costs limit the ability of some countries to expand or modernize their fleets rapidly

- For instance, Boeing P-8A Poseidon aircraft involve high acquisition costs along with significant maintenance and training expenses, which can strain defense budgets and slow fleet expansion plans

- Operational costs include fuel consumption, long mission durations, crew training, and logistics support for high-endurance platforms. These factors collectively increase the total cost of ownership and influence procurement decisions

- Maintenance and upgrade programs for advanced sensors, avionics, and communication systems further add to the financial burden. Continuous investment is required to ensure platform readiness and technological relevance

- The complexity and cost associated with integrating multi-sensor suites and mission management systems act as a barrier for smaller defense forces. Balancing capability requirements with budgetary constraints remains a key challenge for maritime patrol aircraft operators

Maritime Patrol Aircraft Market Scope

The market is segmented on the basis of type, integrated sensors, aircraft type, engine type, and application.

• By Type

On the basis of type, the Maritime Patrol Aircraft market is segmented into armoured and unarmoured. The armoured segment dominated the market with the largest revenue share of 58.3% in 2025, driven by its enhanced survivability in hostile maritime environments and robust protection against small arms fire and surface threats. Navies and coast guards often prioritize armoured variants for long-duration patrols and anti-submarine operations due to their reinforced airframe and onboard safety systems. The demand for armoured maritime patrol aircraft is further supported by their ability to integrate advanced sensors and weapon systems without compromising structural integrity. Their reliability in high-risk missions ensures preference over unarmoured options for strategic maritime defense operations.

The unarmoured segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising adoption for cost-effective maritime surveillance, border patrolling, and civilian applications. These aircraft offer lighter weight and improved fuel efficiency, making them ideal for extended patrol missions over large maritime zones. For instance, manufacturers such as Leonardo are increasingly providing unarmoured variants equipped with modular sensors for flexible maritime monitoring. The operational versatility, lower procurement costs, and ease of maintenance contribute to their rising popularity among emerging naval forces and coast guard fleets.

• By Integrated Sensors

On the basis of integrated sensors, the market is segmented into radar, camera, and others. The radar segment dominated the market in 2025 due to its critical role in detecting surface and subsurface threats across vast maritime regions. Advanced radar systems provide real-time situational awareness, target tracking, and early warning capabilities, enabling effective maritime domain surveillance. Navies often equip patrol aircraft with multifunctional radar for anti-submarine warfare, search-and-rescue, and surveillance missions, ensuring operational superiority. High reliability in adverse weather conditions and integration with other onboard sensor systems enhance the preference for radar-equipped aircraft. The segment’s dominance is reinforced by continuous technological upgrades, including AESA radar systems, which improve range, resolution, and threat detection accuracy.

The camera segment is projected to grow at the fastest rate during 2026–2033, driven by increased demand for high-resolution optical and infrared imaging for maritime surveillance. For instance, FLIR Systems’ electro-optical and infrared cameras are integrated into modern patrol aircraft for precise vessel monitoring and threat identification. These sensors enable covert surveillance, day-night operations, and evidence collection for maritime law enforcement. Their rising adoption is further supported by advances in miniaturization, AI-based image processing, and integration with unmanned aerial vehicles, providing operational flexibility and cost efficiency for various maritime missions.

• By Aircraft Type

On the basis of aircraft type, the market is segmented into fixed-wing and rotary-wing. The fixed-wing segment dominated the market in 2025, driven by its long-range capabilities, high endurance, and ability to cover vast maritime areas efficiently. Fixed-wing patrol aircraft are preferred for long-duration surveillance missions, anti-piracy operations, and maritime reconnaissance due to their fuel efficiency and higher payload capacity for sensors and weapons. Navies prioritize fixed-wing types for strategic monitoring of territorial waters and extended patrol missions over international waters. The ability to operate at high altitudes and integrate advanced surveillance systems reinforces the dominance of fixed-wing maritime patrol aircraft.

The rotary-wing segment is expected to witness the fastest growth during 2026–2033, fueled by increasing demand for versatile, short-range, and shipborne maritime patrol operations. For instance, Sikorsky S-70 Seahawk helicopters are deployed for anti-submarine warfare, search-and-rescue, and rapid-response missions. Their vertical takeoff and landing capabilities allow deployment from ships and offshore platforms, making them ideal for coastal and nearshore operations. Rising adoption is also driven by their ability to operate in confined spaces and perform multi-role missions, enhancing overall fleet flexibility.

• By Engine Type

On the basis of engine type, the market is segmented into turbofan and turboprop. The turboprop segment dominated the market in 2025 due to its fuel efficiency, lower operational costs, and suitability for low-speed, long-endurance maritime patrol missions. Turboprop-powered aircraft provide stability for sensor operations such as radar scanning and electro-optical surveillance, making them preferred for extended coastal monitoring. The segment benefits from compatibility with both fixed-wing and smaller rotary-wing patrol aircraft, ensuring widespread adoption across various maritime forces. Continuous improvements in engine reliability and endurance further reinforce the preference for turboprop engines in strategic maritime operations.

The turbofan segment is anticipated to witness the fastest growth from 2026 to 2033, driven by rising demand for high-speed maritime interception, rapid response, and long-range reconnaissance. For instance, Boeing P-8 Poseidon utilizes turbofan engines to achieve high operational speed while maintaining substantial sensor payloads for anti-submarine and anti-surface warfare missions. Increased adoption is also supported by the growing need for multi-mission aircraft capable of covering large maritime zones quickly and efficiently, enabling navies to respond rapidly to emerging threats.

• By Application

On the basis of application, the market is segmented into passenger ships and ferries, dry cargo vessels, tankers, dry bulk carriers, special purpose vessels, service vessels, fishing vessels, and others. The special purpose vessels segment dominated the market in 2025 due to its critical role in surveillance, anti-piracy, and fleet protection operations. These aircraft are often deployed to safeguard high-value maritime assets, conduct rescue operations, and monitor sensitive zones such as offshore oil rigs. The segment’s dominance is further driven by the integration of multi-sensor payloads and advanced communication systems, enabling real-time maritime intelligence and coordinated operations with naval fleets. Their strategic importance in ensuring maritime security reinforces continued investment by defense agencies and coast guards.

The fishing vessels segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand for maritime patrol aircraft in fisheries monitoring, illegal fishing detection, and environmental surveillance. For instance, Saab’s surveillance systems are integrated into patrol aircraft for real-time tracking of fishing activities and vessel compliance monitoring. The rising focus on sustainable fishing practices, monitoring of maritime resources, and enforcement of regulations supports the growing adoption of these aircraft in fisheries management operations. Their operational efficiency and adaptability for multiple applications contribute to rapid market growth.

Maritime Patrol Aircraft Market Regional Analysis

- North America dominated the maritime patrol aircraft market with the largest revenue share of 38.7% in 2025, driven by rising defense modernization programs, strategic maritime surveillance requirements, and high defense expenditure

- The U.S. and Canada prioritize advanced maritime patrol aircraft for anti-submarine warfare, border protection, and search-and-rescue operations, ensuring robust fleet upgrades and sensor integration

- Widespread adoption is further supported by advanced aerospace infrastructure, high defense budgets, and government initiatives for naval security, positioning North America as a key market for both domestic production and procurement of Maritime Patrol Aircraft

U.S. Maritime Patrol Aircraft Market Insight

The U.S. Maritime Patrol Aircraft market captured the largest revenue share in 2025 within North America, fueled by ongoing fleet modernization and procurement of advanced fixed-wing and rotary-wing patrol aircraft. Rising demand for multi-mission platforms capable of anti-submarine warfare, maritime reconnaissance, and surveillance operations drives the market. The U.S. Navy’s focus on long-endurance, sensor-rich aircraft such as the P-8 Poseidon and unmanned aerial systems further propels growth. In addition, investments in state-of-the-art radar, electro-optical, and infrared sensor systems enhance operational capabilities, supporting both national security and allied maritime missions.

Europe Maritime Patrol Aircraft Market Insight

The Europe Maritime Patrol Aircraft market is projected to grow at a steady CAGR during the forecast period, primarily driven by increasing naval modernization programs and the need to safeguard extensive coastal zones. Countries such as France, Italy, and Norway are investing in advanced maritime patrol aircraft with multi-sensor integration for enhanced situational awareness. Rising focus on counter-piracy operations, search-and-rescue missions, and environmental monitoring supports the adoption of fixed-wing and rotary-wing platforms. In addition, strong defense infrastructure, government contracts, and regional cooperation in NATO contribute to consistent market growth.

U.K. Maritime Patrol Aircraft Market Insight

The U.K. Maritime Patrol Aircraft market is expected to witness notable growth during the forecast period, fueled by the Royal Navy’s focus on fleet modernization and maritime security enhancement. The adoption of multi-role patrol aircraft equipped with advanced radar and surveillance sensors is being prioritized to address emerging threats in territorial waters and the North Atlantic region. Increasing investments in sensor upgrades, interoperability with allied forces, and procurement of unmanned aerial vehicles further bolster market expansion. The U.K.’s defense strategy emphasizes both operational readiness and technological superiority, driving sustained demand for Maritime Patrol Aircraft.

Germany Maritime Patrol Aircraft Market Insight

The Germany Maritime Patrol Aircraft market is anticipated to grow at a considerable CAGR during the forecast period, driven by rising naval modernization programs and strategic maritime surveillance initiatives. Germany emphasizes sensor-rich aircraft for anti-submarine and reconnaissance missions, alongside investments in long-endurance platforms for coastal security. Strong defense budgets, government procurement policies, and integration of advanced radar and imaging systems promote adoption. The country’s focus on eco-efficient, technologically advanced solutions further supports the market, especially for fleet replacement and multi-role operational capabilities.

Asia-Pacific Maritime Patrol Aircraft Market Insight

The Asia-Pacific Maritime Patrol Aircraft market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising defense budgets, territorial maritime disputes, and modernization of naval fleets in countries such as China, India, and Japan. Growing focus on anti-piracy operations, surveillance of exclusive economic zones, and disaster response is fueling demand for both fixed-wing and rotary-wing patrol aircraft. Governments are investing in indigenous production and acquisition of advanced platforms to enhance maritime security. Increasing collaborations with global aerospace manufacturers and adoption of multi-sensor, long-endurance aircraft further accelerate market growth.

Japan Maritime Patrol Aircraft Market Insight

The Japan Maritime Patrol Aircraft market is witnessing steady growth due to increasing maritime security concerns, technological advancements, and modernization of the Japan Maritime Self-Defense Force. The rising need for long-range patrol and anti-submarine capabilities drives procurement of sensor-equipped fixed-wing aircraft. Integration with other defense systems, such as coastal radar networks and unmanned platforms, enhances operational efficiency. Japan’s focus on multi-role capabilities and domestic production supports market expansion in both national and regional maritime security initiatives.

China Maritime Patrol Aircraft Market Insight

The China Maritime Patrol Aircraft market accounted for the largest revenue share in Asia-Pacific in 2025, driven by the country’s strategic focus on protecting its maritime boundaries and expanding naval capabilities. Rising investments in both fixed-wing and rotary-wing platforms equipped with advanced radar, cameras, and electronic surveillance systems enhance operational reach. China is actively expanding its domestic manufacturing capacity for patrol aircraft, supported by defense modernization programs and regional security priorities. The increasing deployment of these aircraft for anti-submarine warfare, resource protection, and maritime domain awareness is propelling market growth.

Maritime Patrol Aircraft Market Share

The maritime patrol aircraft industry is primarily led by well-established companies, including:

- AVIC (China)

- Airbus S.A.S (France)

- RUAG Group (Switzerland)

- Boeing (U.S.)

- Textron Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Leonardo S.p.A (Italy)

- Dassault Aviation (France)

- Saab AB (Sweden)

- Kawasaki Heavy Industries, Ltd (Japan)

- BAE Systems plc (U.K.)

- Thales Group (France)

- Embraer S.A. (Brazil)

- Harbin Aircraft Industry Co., Ltd (China)

Latest Developments in Global Maritime Patrol Aircraft Market

- In November 2025, Boeing announced a new contract with Australian company AW Bell for castings supporting the 737 and 777 programs, including derivatives such as the P-8 Poseidon. This development strengthens Boeing’s position in the Maritime Patrol Aircraft market by enhancing its global supply chain and supporting high-tech job creation in Australia. The partnership under the Australian Government’s Global Supply Chain Program also enables small and medium-sized enterprises to participate in high-value defense manufacturing, reinforcing Boeing’s strategic footprint following the Royal Australian Air Force’s receipt of its thirteenth P-8 maritime patrol aircraft

- In October 2025, the U.S. Navy inducted the first upgraded P-8A Poseidon aircraft under a contract awarded in September 2024 to support 139 P-8A platforms. The contract, executed by L3Harris, includes structural refurbishment, avionics upgrades, systems testing, and component overhauls, with nine aircraft planned for overhaul in the first year through 2029. The July 2025 delivery of the first overhauled aircraft marks a significant milestone in depot-level MRO for the P-8 fleet, enhancing operational readiness and extending aircraft lifecycle, which positively impacts the Maritime Patrol Aircraft market by demonstrating the value of upgrade and sustainment programs

- In October 2025, the Indian Ministry of Defense issued a Request for Proposal to the Tata Advanced Systems-Airbus joint venture for 15 C-295 maritime patrol aircraft valued at USD 3.5 billion. The RFP specifies nine aircraft in Medium-Range Maritime Reconnaissance configuration for the Navy and six Multi-Mission Maritime Aircraft for the Coast Guard, with manufacturing largely at the Vadodara Final Assembly Line under the Make in India initiative. This development is expected to accelerate the market in India by increasing indigenous production capabilities, promoting local defense manufacturing, and expanding operational maritime surveillance capabilities

- In August 2025, Terma and Boeing signed a Memorandum of Understanding to explore Maintenance, Repair, and Overhaul (MRO) support for P-8 maritime patrol aircraft in Denmark. Announced at DALO Industry Days, the agreement aims to evaluate establishing a dedicated P-8 MRO capability, supporting national defense readiness while creating opportunities for industrial collaboration. This initiative is likely to strengthen the European Maritime Patrol Aircraft market by ensuring long-term sustainment solutions, increasing operational availability, and encouraging industrial partnerships for defense support services

- In August 2025, India received the final C-295 military transport aircraft from Spain on August 2, two months ahead of schedule, marking a key milestone in enhancing India’s defense capabilities. Out of 56 aircraft ordered under a USD 2.5 billion deal, 16 were delivered from Spain while the remaining 40 are to be manufactured domestically by Tata Advanced Systems under the Make in India program. This early delivery and localization of production highlight India’s growing self-reliance in defense aircraft manufacturing and is expected to stimulate the domestic market for maritime patrol aircraft while supporting fleet expansion and modernization initiatives

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.