Global Mechanistic Target Of Rapamycin Mtor Inhibitors Market

Market Size in USD Billion

CAGR :

%

USD

7.74 Billion

USD

10.19 Billion

2025

2033

USD

7.74 Billion

USD

10.19 Billion

2025

2033

| 2026 –2033 | |

| USD 7.74 Billion | |

| USD 10.19 Billion | |

| % | |

|

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Size

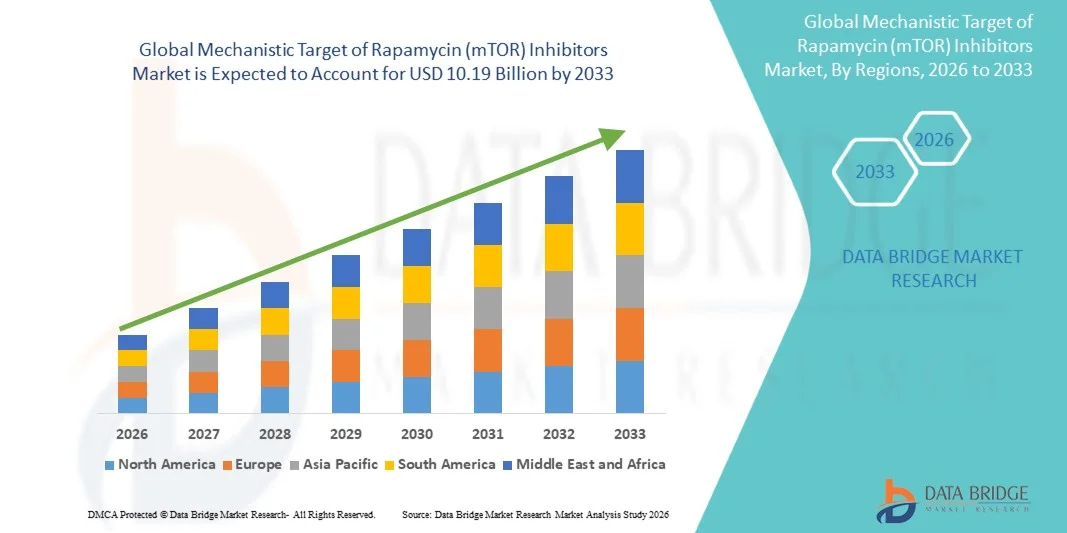

- The global Mechanistic Target of Rapamycin (mTOR) Inhibitors market size was valued at USD 7.74 billion in 2025 and is expected to reach USD 10.19 billion by 2033, at a CAGR of 3.50% during the forecast period

- The market growth is largely fueled by increasing prevalence of cancer, organ transplant procedures, and rare genetic disorders, leading to higher adoption of targeted therapies such as Mechanistic Target of Rapamycin (mTOR) inhibitors across clinical settings for improved treatment outcomes

- Furthermore, rising demand for precision medicine, along with growing research into cellular signaling pathways and immunosuppressive therapies, is establishing Mechanistic Target of Rapamycin (mTOR) inhibitors as a critical therapeutic class in oncology and transplant medicine. These converging factors are accelerating the uptake of mTOR inhibitor solutions, thereby significantly boosting the industry's growth

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Analysis

- Mechanistic Target of Rapamycin (mTOR) inhibitors are a vital class of targeted therapies widely used in oncology, organ transplantation, and rare disease management due to their ability to regulate cell growth, proliferation, and immune response through inhibition of the mTOR signaling pathway

- The escalating demand for mTOR inhibitors is primarily driven by increasing cancer prevalence, rising organ transplant procedures, and growing adoption of precision medicine approaches, along with expanding clinical research into targeted molecular therapies for improved patient outcomes

- North America dominated the mechanistic target of rapamycin (mTOR) inhibitors market with the largest revenue share of 41.8% in 2025, supported by advanced healthcare infrastructure, strong R&D investments, high adoption of novel oncology and immunosuppressive therapies, and the presence of major pharmaceutical companies

- Asia-Pacific is expected to be the fastest growing region in the mechanistic target of rapamycin (mTOR) inhibitors market during the forecast period due to increasing healthcare expenditure, rising cancer incidence, improving access to advanced therapeutics, and expansion of clinical trial activities in emerging economies

- The Oral segment dominated the largest market revenue share of 66.9% in 2025, driven by ease of administration and high patient compliance in long-term therapies

Report Scope and Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Segmentation

|

Attributes |

Mechanistic Target of Rapamycin (mTOR) Inhibitors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Trends

“Advancements in Precision Oncology and Combination Therapy Approaches”

- A significant and accelerating trend in the global mechanistic target of rapamycin (mTOR) inhibitors market is the growing adoption of precision oncology approaches and combination therapies, aimed at improving treatment efficacy and overcoming drug resistance in cancer and other chronic diseases

- For instance, mTOR inhibitors such as everolimus and temsirolimus are increasingly being studied in combination with chemotherapy, immunotherapy, and targeted agents to enhance therapeutic response in oncology indications

- The use of biomarker-driven treatment strategies is enabling clinicians to better identify patient subgroups most likely to benefit from mTOR pathway inhibition

- Pharmaceutical companies are also focusing on next-generation mTOR inhibitors that offer improved selectivity and reduced toxicity compared to earlier agents

- Increasing clinical trials exploring dual inhibition of PI3K/AKT/mTOR pathways are further expanding the therapeutic potential of this drug class

- This shift toward personalized medicine and combination regimens is significantly improving long-term disease management outcomes

- The growing pipeline of novel mTOR-targeted therapies is expected to strengthen future market expansion

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Dynamics

Driver

“Increasing Prevalence of Cancer and Expanding Use of Targeted Therapies”

- The rising global burden of cancer is a major driver of the mTOR inhibitors market, as these drugs play a crucial role in targeted cancer treatment strategies

- For instance, cancers such as renal cell carcinoma, breast cancer, and certain lymphomas have shown responsiveness to mTOR pathway inhibition, increasing clinical adoption

- Expanding awareness of targeted therapies among oncologists is further driving the integration of mTOR inhibitors into treatment protocols

- For instance, hospitals are increasingly adopting molecular diagnostics to support targeted treatment decision-making in oncology care

- Strong investment in oncology research and drug development is accelerating innovation in mTOR-based therapies

- Growing availability of biologics and targeted drugs through specialty care channels is further supporting market expansion

Restraint/Challenge

“Adverse Effects, Drug Resistance, and High Treatment Costs”

- One of the key challenges in the mTOR inhibitors market is the occurrence of significant side effects such as immunosuppression, metabolic disorders, and infections, which can limit long-term use

- For instance, patients receiving mTOR inhibitors may experience complications such as stomatitis, hyperlipidemia, and increased infection risk due to immune suppression

- Development of drug resistance over time reduces treatment effectiveness and remains a major clinical concern

- For instance, tumor cells may activate alternative signaling pathways, diminishing the long-term efficacy of mTOR inhibition therapy

- High treatment costs associated with targeted cancer therapies also pose a barrier to widespread adoption, particularly in low- and middle-income regions

- For instance, prolonged therapy with branded mTOR inhibitors can create financial burden for patients and healthcare systems

- Addressing these challenges requires development of safer formulations, improved combination strategies, and more cost-effective therapeutic options

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Scope

The market is segmented on the basis of indication, product types, route of administration, end-users, and distribution channel.

• By Indication

On the basis of indication, the Mechanistic Target of Rapamycin (mTOR) Inhibitors market is segmented into Organ Transplant, Oncology, and Others. The Oncology segment dominated the largest market revenue share of 61.8% in 2025, driven by the rising global burden of cancer and the increasing use of mTOR inhibitors in targeted cancer therapy. Drugs targeting the mTOR pathway are widely used in treating renal cell carcinoma, breast cancer, and neuroendocrine tumors. Increasing adoption of precision medicine is further supporting demand. Growing awareness regarding early cancer diagnosis boosts treatment uptake. Expanding oncology infrastructure in developed and emerging markets enhances accessibility. Strong clinical efficacy in tumor growth suppression supports physician preference. Rising healthcare expenditure globally contributes to segment growth. Continuous research and clinical trials are expanding therapeutic applications. Favorable reimbursement policies in oncology care further strengthen adoption. Increasing geriatric population also drives cancer incidence. Overall, oncology remains the dominant segment due to high disease prevalence and treatment dependency.

The Organ Transplant segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing transplant procedures worldwide. mTOR inhibitors play a critical role in preventing organ rejection, boosting their demand. Rising cases of end-stage organ failure support growth. Improvements in transplant surgery success rates are expanding adoption. Increasing donor availability in developed regions further accelerates procedures. Growing awareness of post-transplant care enhances drug usage. Advancements in immunosuppressive therapy improve patient outcomes. Expansion of transplant centers globally supports accessibility. Government initiatives promoting organ donation boost market growth. Increasing survival rates post-transplant further encourage usage. Overall, organ transplant applications are growing rapidly due to rising clinical need.

• By Product Types

On the basis of product types, the mTOR Inhibitors market is segmented into Afinitor, Rapamune, Torisel, Zortress, and Others. The Afinitor segment dominated the largest market revenue share of 38.6% in 2025, driven by its strong clinical efficacy and wide approval across multiple oncology indications. It is extensively used in treating advanced cancers such as breast cancer and renal cell carcinoma. Strong physician preference and established clinical guidelines support its dominance. Increasing global cancer burden further boosts demand. High adoption in both developed and emerging markets strengthens market share. Continuous R&D and label expansions enhance usage scope. Strong brand recognition and marketing support further contribute to leadership. Availability across hospital pharmacies ensures wide accessibility. Rising healthcare spending improves affordability. Growing patient dependency on long-term therapy supports consistent revenue. Overall, Afinitor remains the leading product type due to its broad therapeutic application.

The Rapamune segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by its strong role in organ transplant immunosuppression. Increasing number of kidney transplant procedures supports demand. Growing awareness regarding post-transplant rejection prevention enhances usage. Expanding transplant centers improve accessibility. Physicians prefer Rapamune for long-term maintenance therapy. Rising survival rates post-transplant support continued drug use. Increasing healthcare infrastructure in emerging economies drives adoption. Favorable reimbursement policies further support growth. Advancements in immunosuppressive therapy improve outcomes. Expanding generic availability boosts affordability. Overall, Rapamune is growing steadily due to transplant-related applications.

• By Route of Administration

On the basis of route of administration, the mTOR Inhibitors market is segmented into Oral, Parenteral, and Others. The Oral segment dominated the largest market revenue share of 66.9% in 2025, driven by ease of administration and high patient compliance in long-term therapies. Oral mTOR inhibitors are widely preferred for chronic cancer and transplant management. Increasing availability of tablet formulations supports adoption. Patients prefer non-invasive treatment options. Physicians frequently prescribe oral drugs for outpatient care. Strong accessibility through retail and hospital pharmacies boosts usage. Growing cancer and transplant patient populations support demand. Improved drug formulations enhance efficacy and safety. Rising awareness of long-term treatment adherence strengthens uptake. Cost-effectiveness compared to injectable forms further drives preference. Expanding healthcare access in emerging markets supports growth. Overall, oral administration dominates due to convenience and effectiveness.

The Parenteral segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing use in hospital-based acute care settings. Injectable mTOR inhibitors are used in severe and advanced cases requiring immediate action. Rising hospital admissions for cancer treatment support growth. Advancements in infusion technologies improve safety and efficiency. Increasing physician preference for controlled dosing enhances adoption. Growing availability of specialty oncology centers boosts access. Rising healthcare expenditure supports advanced treatment options. Expanding clinical research in targeted therapies drives innovation. Improved patient monitoring enhances outcomes. Increasing prevalence of complex cases contributes to demand. Overall, parenteral route is gaining traction in critical care settings.

• By End-Users

On the basis of end-users, the mTOR Inhibitors market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 58.4% in 2025, driven by high patient inflow for cancer and transplant treatments. Hospitals provide advanced infrastructure for drug administration and monitoring. Strong presence of oncology and transplant departments supports demand. Increasing number of surgical procedures boosts usage. Insurance coverage enhances affordability in hospital settings. Rising prevalence of chronic diseases increases hospital visits. Availability of skilled healthcare professionals improves outcomes. Hospitals also serve as primary centers for clinical trials. Government investments strengthen hospital infrastructure. Growing adoption of advanced therapies further supports demand. Patient trust in institutional care drives preference. Overall, hospitals remain the dominant end-user segment.

The Specialty Clinics segment is expected to witness the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing demand for focused oncology and transplant care. These clinics offer specialized treatment with improved patient experience. Rising preference for outpatient care supports growth. Expansion of ambulatory care centers boosts accessibility. Increasing physician specialization enhances treatment efficiency. Growing awareness about personalized care drives adoption. Improved infrastructure in urban regions supports expansion. Rising healthcare affordability in private clinics boosts demand. Integration of advanced therapies enhances outcomes. Expanding referral networks support patient inflow. Overall, specialty clinics are emerging as a fast-growing segment.

• By Distribution Channel

On the basis of distribution channel, the mTOR Inhibitors market is segmented into Hospital Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated the largest market revenue share of 55.7% in 2025, driven by high dependency on hospital-based cancer and transplant treatments. Most mTOR inhibitors are dispensed in controlled clinical environments. Strong supply chain integration supports availability. Increasing hospital admissions drive demand. Physician-led prescriptions ensure consistent usage. Government procurement programs support distribution. Rising prevalence of oncology cases boosts consumption. Availability of specialty drug storage ensures safety. Insurance coverage enhances affordability in hospitals. Growing number of tertiary care centers supports expansion. Clinical monitoring requirements reinforce hospital pharmacy dominance. Overall, hospital pharmacies remain the primary distribution channel.

The Retail Pharmacy segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing accessibility of maintenance therapies. Growing availability of generic drugs supports expansion. Rising outpatient treatments boost demand. Patients prefer convenient pharmacy access. Expansion of pharmacy chains improves reach. Increasing awareness of chronic disease management supports growth. Digital prescription integration enhances convenience. Growing healthcare infrastructure in emerging regions drives adoption. Improved affordability encourages purchases. Expanding insurance coverage supports retail sales. Overall, retail pharmacies are steadily expanding as a key distribution channel.

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Regional Analysis

- North America dominated the mechanistic target of rapamycin (mTOR) inhibitors market with the largest revenue share of 41.8% in 2025, supported by advanced healthcare infrastructure, strong R&D investments, high adoption of novel oncology and immunosuppressive therapies, and the presence of major pharmaceutical companies. The region also benefits from early access to innovative biologics and a well-established clinical research ecosystem, which accelerates the adoption of mTOR-targeted therapies across multiple indications

- Healthcare providers and patients in the region increasingly rely on advanced targeted therapies and immunosuppressive treatment regimens, with strong integration of precision medicine approaches in oncology and transplant care

- This dominance is further supported by favorable reimbursement frameworks, robust regulatory pathways for orphan and oncology drugs, and continuous innovation by leading pharmaceutical companies, strengthening North America’s position as a key revenue contributor in the global mTOR inhibitors market

U.S. Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The U.S. mechanistic target of rapamycin (mTOR) inhibitors market captured the largest revenue share within North America in 2025, driven by strong uptake of targeted oncology therapies and widespread use of immunosuppressive agents in transplant medicine. The country benefits from a highly developed healthcare system, rapid adoption of precision medicine, and extensive availability of FDA-approved mTOR inhibitors such as everolimus and temsirolimus. For instance, leading cancer centers in the U.S. are increasingly integrating mTOR pathway inhibitors into combination treatment protocols for renal cell carcinoma and breast cancer. In addition, strong pharmaceutical R&D activity and ongoing clinical trials for next-generation mTOR inhibitors are further accelerating market expansion.

Europe Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The Europe mechanistic target of rapamycin (mTOR) inhibitors market is projected to expand at a steady CAGR during the forecast period, supported by increasing incidence of cancer and autoimmune disorders, along with strong public healthcare systems. For instance, European oncology networks are actively promoting early diagnosis and standardized treatment protocols that include targeted therapies such as mTOR inhibitors. The region also benefits from strong regulatory support for orphan drugs and increasing reimbursement coverage for advanced biologics. Growing adoption of precision medicine and biomarker-based treatment approaches is further supporting market expansion across major European economies.

U.K. Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The U.K. mechanistic target of rapamycin (mTOR) inhibitors market is anticipated to grow at a notable CAGR during the forecast period, driven by rising cancer prevalence and increasing use of immunosuppressive therapies in organ transplantation. For instance, the National Health Service (NHS) is increasingly adopting targeted oncology treatments, including mTOR inhibitors, as part of standardized care pathways. The country’s strong clinical research infrastructure and growing participation in international drug trials are further supporting innovation and adoption of advanced therapies.

Germany Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The Germany mechanistic target of rapamycin (mTOR) inhibitors market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high awareness of targeted therapies, and increasing demand for advanced oncology treatments. For instance, German hospitals are integrating mTOR inhibitors into combination regimens for cancer management, particularly in renal and breast cancer cases. The country’s emphasis on precision medicine, coupled with strong pharmaceutical manufacturing capabilities, is further driving market growth.

Asia-Pacific Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The Asia-Pacific mechanistic target of rapamycin (mTOR) inhibitors market is poised to grow at the fastest CAGR during the forecast period due to rising healthcare expenditure, increasing cancer incidence, improving access to advanced therapeutics, and expansion of clinical trial activities in emerging economies such as China, India, and South Korea. For instance, governments across the region are investing in oncology infrastructure and expanding reimbursement coverage for life-saving targeted therapies. Rapid urbanization and growing awareness of precision medicine are further accelerating adoption of mTOR inhibitors across both public and private healthcare systems.

Japan Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The Japan mechanistic target of rapamycin (mTOR) inhibitors market is gaining traction due to its advanced healthcare system, strong focus on oncology innovation, and high adoption of immunosuppressive therapies in transplant care. For instance, Japanese hospitals are increasingly utilizing mTOR inhibitors in post-transplant management to improve graft survival outcomes. The country’s aging population and strong emphasis on advanced biomedical research are further supporting steady market growth.

China Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Insight

The China mechanistic target of rapamycin (mTOR) inhibitors market accounted for the largest revenue share in Asia Pacific in 2025, driven by rising cancer burden, expanding healthcare infrastructure, and increasing adoption of targeted oncology therapies. For instance, major urban hospitals are increasingly incorporating mTOR inhibitors into standard cancer treatment protocols, particularly for renal cell carcinoma. Strong domestic pharmaceutical manufacturing capabilities, along with government support for oncology drug development, are further strengthening market expansion across the country.

Mechanistic Target of Rapamycin (mTOR) Inhibitors Market Share

The Mechanistic Target of Rapamycin (mTOR) Inhibitors industry is primarily led by well-established companies, including:

- Novartis (Switzerland)

- Pfizer (U.S.)

- Roche (Switzerland)

- Merck & Co. (U.S.)

- Bristol Myers Squibb (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson (U.S.)

- AbbVie (U.S.)

- Amgen (U.S.)

- Takeda Pharmaceutical (Japan)

- Astellas Pharma (Japan)

- Bayer (Germany)

- Sanofi (France)

- GSK (U.K.)

- Eli Lilly and Company (U.S.)

- CSL Limited (Australia)

- Eisai Co., Ltd. (Japan)

- Daiichi Sankyo (Japan)

- Ipsen (France)

- Sandoz (Switzerland)

Latest Developments in Global Mechanistic Target of Rapamycin (mTOR) Inhibitors Market

- In March 2021, Novartis announced updated clinical data for everolimus (Afinitor), highlighting improved progression-free survival in patients with advanced neuroendocrine tumors, reinforcing its role as a key mTOR inhibitor in oncology treatment. This update strengthened everolimus’ position as a widely used rapalog in cancer therapy

- In June 2021, Aadi Bioscience advanced its nab-sirolimus (ABI-009) program for soft tissue sarcoma, reporting encouraging Phase II results and progressing toward regulatory discussions with the U.S. FDA, marking a significant step for albumin-bound mTOR inhibitor formulations

- In February 2022, Pfizer continued expansion of its oncology portfolio with updated real-world evidence supporting the use of temsirolimus (Torisel) in renal cell carcinoma, reinforcing its clinical relevance as an mTOR pathway inhibitor in difficult-to-treat cancers

- In September 2022, Novartis presented new long-term data for everolimus in breast cancer and tuberous sclerosis complex (TSC)-associated tumors at a major oncology conference, demonstrating sustained efficacy and manageable safety profile in extended treatment settings

- In May 2023, the U.S. FDA expanded the approval label for everolimus (Afinitor) in additional rare tumor indications, including certain advanced neuroendocrine tumors, strengthening its therapeutic scope within mTOR inhibition-based oncology care

- In October 2023, Takeda and partner companies continued development of next-generation selective mTOR pathway inhibitors, focusing on improved specificity and reduced immunosuppression compared to first-generation rapalogs, with early-stage pipeline compounds entering preclinical evaluation

- In January 2024, Aadi Bioscience reported additional clinical updates for nab-sirolimus in advanced malignant PEComa, showing durable response rates and supporting continued regulatory engagement for expanded therapeutic use

- In August 2024, Novartis announced ongoing lifecycle management studies for everolimus across oncology and transplant indications, focusing on combination therapies with immunotherapy agents to enhance mTOR pathway targeting efficiency

- In April 2025, several biotechnology firms expanded research into next-generation ATP-competitive mTOR inhibitors, targeting both mTORC1 and mTORC2 complexes to overcome resistance seen with first-generation rapalogs, with multiple compounds entering Phase I trials

- In July 2025, emerging clinical research programs highlighted improved outcomes from combination regimens involving mTOR inhibitors and immune checkpoint inhibitors in solid tumors, indicating a growing trend toward combination therapy approaches in oncology.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.