Global Medical Device Cybersecurity Solutions Market

Market Size in USD Billion

USD

12.22 Billion

USD

60.39 Billion

2024

2032

USD

12.22 Billion

USD

60.39 Billion

2024

2032

| 2025 - 2032 | |

| USD 12.22 Billion | |

| USD 60.39 Billion | |

| % | |

|

Medical Device Cybersecurity Solutions Market Size

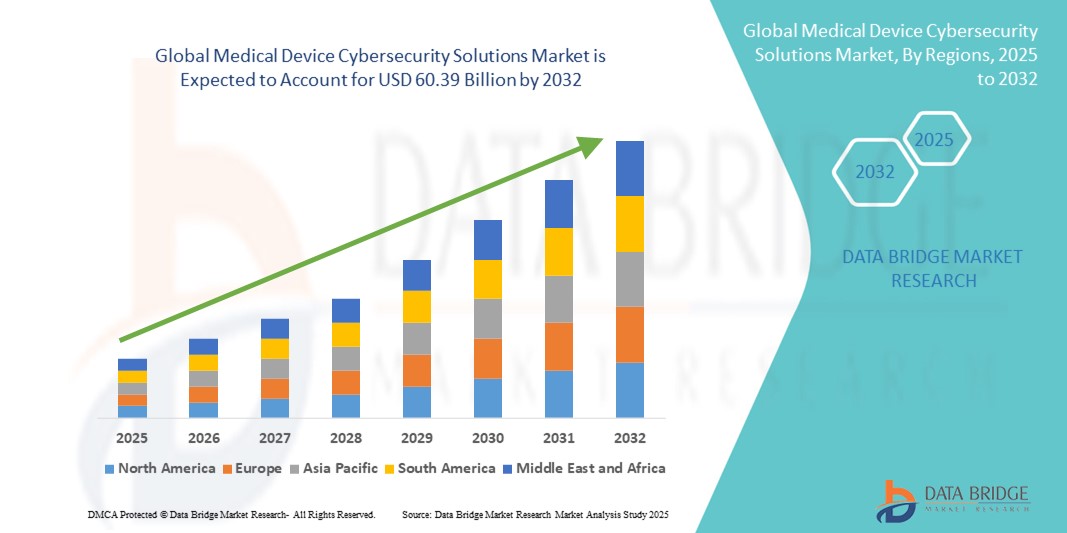

- The global medical device cybersecurity solutions market size was valued at USD 12.22 billion in 2024 and is expected to reach USD 60.39 billion by 2032, at a CAGR of 22.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of connected medical devices, digital health technologies, and telemedicine platforms, leading to higher integration of medical equipment with hospital networks and cloud-based systems. This digital transformation across healthcare is creating a strong demand for robust cybersecurity solutions to safeguard patient data and ensure device integrity

- Furthermore, rising concerns over data breaches, ransomware attacks, and unauthorized access to critical medical devices are establishing cybersecurity solutions as an essential component of modern healthcare infrastructure. These converging factors are accelerating the uptake of medical device cybersecurity solutions, thereby significantly boosting the industry’s growth

Medical Device Cybersecurity Solutions Market Analysis

- Medical device cybersecurity solutions are increasingly critical to safeguarding connected medical devices from cyber threats, ensuring patient safety, data protection, and compliance with stringent regulatory requirements. The rapid digitalization of healthcare, growing adoption of IoMT (Internet of Medical Things), and increasing sophistication of cyberattacks are driving the demand for advanced cybersecurity solutions in this market

- The rising demand for medical device cybersecurity solutions is primarily fueled by the surge in connected medical devices, heightened vulnerability to ransomware and data breaches, and stricter enforcement of compliance standards such as HIPAA, FDA guidelines, and GDPR

- North America dominated the medical device cybersecurity solutions market with the largest revenue share of 40.5% in 2024, characterized by advanced healthcare infrastructure, high adoption of digital health technologies, and a strong regulatory environment. The U.S. in particular is experiencing substantial growth due to significant investments in cybersecurity for healthcare institutions, rising awareness of cyber risks, and innovations from both established players and startups focusing on AI-driven and automated security platforms

- Asia-Pacific is expected to be the fastest growing region in the medical device cybersecurity solutions market during the forecast period, projected to grow at a CAGR of 9.5% from 2025 to 2032, driven by rapid urbanization, rising adoption of connected healthcare systems, and increasing government initiatives to strengthen medical cybersecurity. Countries such as China, India, Japan, and South Korea are witnessing accelerated investments in healthcare IT infrastructure, which is expected to significantly boost market expansion

- The hospital medical devices segment dominated the medical device cybersecurity solutions market with the largest market revenue share of 41.5% in 2024, as critical care equipment—such as ventilators, infusion pumps, imaging scanners, and surgical robots—require continuous uptime and secure operation

Report Scope and Medical Device Cybersecurity Solutions Market Segmentation

|

Attributes |

Medical Device Cybersecurity Solutions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Device Cybersecurity Solutions Market Trends

Enhanced Protection Through Regulatory Compliance and Advanced Security Integration

- A significant and accelerating trend in the global medical device cybersecurity solutions market is the increasing emphasis on compliance with international regulations and security frameworks such as HIPAA, GDPR, and FDA cybersecurity guidelines. Healthcare providers and device manufacturers are prioritizing robust cybersecurity protocols to avoid penalties, safeguard patient data, and ensure uninterrupted clinical operations

- For instance, leading solution providers are introducing cybersecurity platforms that embed compliance-ready frameworks, allowing hospitals and clinics to meet evolving regulatory requirements. Companies are offering solutions with real-time monitoring, encryption, and patch management to align with global cybersecurity standards, thereby enhancing adoption among healthcare institutions

- The growing interconnectedness of medical devices within the Internet of Medical Things (IoMT) ecosystem has amplified the need for secure communication channels, intrusion detection, and risk assessment tools. Advanced cybersecurity solutions now include continuous vulnerability scanning and device authentication systems to prevent unauthorized access and protect sensitive patient information

- The seamless integration of medical device cybersecurity with broader hospital IT infrastructure facilitates centralized monitoring of threats, streamlined risk management, and incident response. Through a single platform, healthcare organizations can manage both clinical data security and device functionality, ensuring reliability and patient safety

- This trend towards more regulated, secure, and interconnected medical device environments is fundamentally reshaping healthcare cybersecurity priorities. Consequently, companies such as MedCrypt and Cynerio are developing specialized solutions for real-time monitoring, zero-trust security models, and device-specific protection frameworks

- The demand for medical device cybersecurity solutions is growing rapidly across both developed and emerging healthcare markets, as hospitals, clinics, and research institutions increasingly prioritize regulatory compliance, patient safety, and resilience against cyberattacks

Medical Device Cybersecurity Solutions Market Dynamics

Driver

Growing Need Due to Rising Security Concerns in Healthcare and Rapid Digitalization

- The increasing prevalence of cyberattacks targeting healthcare providers and medical devices, coupled with the accelerating adoption of digital health ecosystems, is a significant driver for the heightened demand for medical device cybersecurity solutions

- For instance, in April 2024, the U.S. Food and Drug Administration (FDA) introduced updated cybersecurity guidance for medical device manufacturers, emphasizing stronger premarket security testing and postmarket monitoring. Such initiatives by regulators and collaborations with industry players are expected to drive the Medical Device Cybersecurity Solutions industry growth in the forecast period

- As healthcare providers become more aware of potential security threats and seek enhanced protection for patient data, advanced cybersecurity solutions offer critical features such as threat detection, data encryption, intrusion prevention, and tamper alerts—providing a compelling upgrade over traditional IT security systems

- Furthermore, the growing popularity of connected medical devices, cloud-based platforms, and AI-driven healthcare systems is making cybersecurity an integral component of healthcare IT, offering seamless integration with hospital information systems and remote patient monitoring platforms

- The convenience of centralized monitoring, compliance management, and the ability to secure sensitive data across multiple device types are key factors propelling the adoption of medical device cybersecurity solutions in both healthcare provider and manufacturer sectors. The trend toward digital health adoption and the increasing availability of user-friendly, regulatory-compliant cybersecurity options further contribute to market growth

Restraint/Challenge

Concerns Regarding Cybersecurity Vulnerabilities and High Implementation Costs

- Concerns surrounding the cybersecurity vulnerabilities of connected medical devices and healthcare IT systems pose a significant challenge to broader market penetration. As medical devices rely on network connectivity and software, they are susceptible to hacking attempts, ransomware attacks, and data breaches, raising anxieties among healthcare organizations about patient safety and compliance

- For instance, high-profile reports of ransomware attacks on hospital systems and breaches of patient health records have made some institutions hesitant to adopt advanced connected medical technologies without robust cybersecurity safeguards

- Addressing these concerns through robust encryption, secure authentication protocols, vulnerability assessments, and regular software updates is crucial for building trust among stakeholders. Companies such as IBM, Cisco, and Fortinet emphasize their advanced threat detection and compliance management capabilities in their solutions to reassure healthcare providers and device manufacturers

- In addition, the relatively high initial cost of advanced medical device cybersecurity systems compared to traditional IT security can be a barrier to adoption for smaller hospitals and healthcare facilities, particularly in developing regions with limited budgets. While cloud-based security solutions have made cybersecurity more accessible, premium features such as AI-driven analytics and advanced endpoint protection often come with a higher price tag

- While costs are gradually decreasing due to technological advancements, the perceived premium for robust cybersecurity can still hinder widespread adoption, especially for budget-conscious healthcare providers. Overcoming these challenges through enhanced regulatory frameworks, industry collaboration, and the development of more affordable medical device cybersecurity solutions will be vital for sustained market growth

Medical Device Cybersecurity Solutions Market Scope

The market is segmented on the basis of solutions, type, device type, and end-user.

- By Solutions

On the basis of solutions, the medical device cybersecurity solutions market is segmented into Identity and Access Management Solutions, Antivirus/Antimalware Solutions, Encryption Solutions, Data Loss Prevention Solutions, Risk and Compliance Management, Intrusion Detection Systems/Intrusion Prevention Systems, Disaster Recovery Solutions, Distributed Denial of Service Solutions, and Other Solutions. The Identity and Access Management (IAM) solutions segment dominated the largest market revenue share of 27.0% in 2024, underpinned by its critical role in enforcing secure user authentication, multi-factor authentication, and role-based access control in healthcare networks. IAM solutions are pivotal in maintaining integrity of patient data and preventing unauthorized access across interconnected device ecosystems. Integration of IAM with biometric authentication, centralized identity platforms, and real-time session monitoring further strengthens institutional trust and compliance. Regulatory mandates such as HIPAA, GDPR, and FDA cybersecurity guidance continue to drive adoption, as IAM assists in audit trails and governance. Healthcare organizations increasingly rely on IAM to manage staff, device, and third-party user access in hospitals, clinics, and telehealth platforms. Investment in IAM is being further fueled by the need for scalable and interoperable security platforms in expanding Internet of Medical Things (IoMT) deployments.

The intrusion detection systems/intrusion prevention systems (IDS/IPS) segment is anticipated to witness the fastest CAGR of 20.1% from 2025 to 2032, driven by a significant rise in cyber threats targeting medical infrastructure, including ransomware and network intrusions. IDS/IPS solutions provide hospitals and clinics with real-time monitoring, anomaly detection, and automated response capabilities, which are vital for early threat mitigation. The integration of behavioral analytics, machine learning-powered detection, and centralized threat intelligence enhances detection accuracy and lowers false positive rates. Rapid proliferation of telemedicine services, remote monitoring devices, and cloud-hosted systems increases the attack surface, necessitating advanced IDS/IPS deployment. Furthermore, regulatory expectations for proactive threat defense and incident response planning elevate the importance of these systems. Healthcare cybersecurity strategy now often begins with robust IDS/IPS layers to protect device integrity and ensure continuity of clinical services during cyber incidents.

- By Type

On the basis of type, the medical device cybersecurity solutions market is segmented into Network Security, Endpoint Security, Application Security, Cloud Security, and Other Security Types. The Network Security segment dominated the largest market revenue share of 35.3% in 2024, because healthcare organizations operate complex networks connecting imaging systems, infusion pumps, EHR platforms, and clinical workstations that require secure data transmission. Network security measures—including next-generation firewalls, secure gateways, and intrusion prevention—are integral to preventing lateral movement of threats within hospital infrastructure. The centralized network defense also streamlines compliance and monitoring for regulatory audits. As specialized medical devices often lack built-in security, network security solutions act as critical control points to detect and block malicious activity. Hospitals and healthcare IT departments favor network-level measures for their broad vehicle coverage across multiple departments and ability to intercept threats before they reach critical endpoints. Investment in secure segmentation, encrypted VPNs, and zero-trust network architecture continues to reinforce dominance of network security investments.

The cloud security segment is projected to witness the fastest CAGR of 19.9% during 2025–2032, spurred by the growing shift to cloud-based platforms for EHRs, telehealth, medical imaging archives, and remote diagnostic tools. Cloud security solutions—such as cloud access security brokers (CASBs), secure API gateways, and cloud workload protection—are increasingly essential for safeguarding healthcare data in transit and at rest. Providers are investing in cloud-native encryption, identity-based access controls, and real-time breach detection to maintain compliance, especially with cross-border data storage requirements. The rise of hybrid cloud architectures and distributed patient monitoring systems further amplifies need for dynamic cloud security. Rapid digital transformation, including AI-driven analytics and big data initiatives in healthcare, relies on secure cloud frameworks. The ability to scale cloud security rapidly makes it attractive for both large hospital systems and smaller clinics transitioning to cloud-based infrastructure.

- By Device Type

On the basis of device type, the medical device cybersecurity solutions market is segmented into Hospital Medical Devices, Wearable and External Medical Devices, and Internally Embedded Medical Devices. The Hospital Medical Devices segment dominated the largest market revenue share of 41.5% in 2024, as critical care equipment—such as ventilators, infusion pumps, imaging scanners, and surgical robots—require continuous uptime and secure operation. These devices operate within high-risk environments, making them prime targets for cyber threats that could endanger patient safety. Cybersecurity solutions tailored to hospital devices must ensure patch management, integrity checking, and secure firmware updates within clinical workflows. Hospitals allocate a significant portion of cybersecurity budgets toward safeguarding these devices due to their complexity and regulatory implications. Integration with hospital network defenses and centralized monitoring systems further enhances protection of interconnected medical infrastructure. As healthcare systems expand connected device inventories, hospital-focused cybersecurity remains foundational.

The wearable and external medical devices segment is projected to witness the fastest CAGR of 18.4% from 2025 to 2032, driven by explosive growth in consumer-facing and clinical wearable devices—including continuous glucose monitors, remote cardiac trackers, and telehealth sensors. These devices generate sensitive personal health data that must be transmitted securely to healthcare providers, amplifying demand for encryption, secure wireless protocols, and device authentication. The shift toward remote patient monitoring and home-based care, especially post-pandemic, increases reliance on wearable security. Patients demand privacy and assurance that their data is protected from interception. Device manufacturers, recognizing this, are embedding cybersecurity features at design stage, including tamper detection, secure pairing, and OTA (over-the-air) encryption. With the rise of 5G and edge computing enabling real-time monitoring, wearables must maintain strong defenses against network-based attacks—thus catalyzing growth of security solutions in this segment.

- By End-User

On the basis of end-user, the medical device cybersecurity solutions market is segmented into Healthcare Providers, Medical Device Manufacturers, and Healthcare Payers. The Healthcare Providers segment dominated the largest market revenue share of 38.2% in 2024, given that hospitals, clinics, and ambulatory centers deploy vast arrays of connected devices integral to patient diagnosis, treatment, and data management. Providers are high-value targets for cybercriminals due to the availability of patient records, operational disruption potential, and the presence of lifesaving devices. In response, healthcare providers invest heavily in layered cybersecurity strategies, including access control, network segmentation, and incident response systems, to maintain continuity and comply with regulatory standards. Recurring ransomware threats and increasing regulatory fines for data breaches further drive spending. Collaboration with cybersecurity vendors to tailor solutions for clinical environments reinforces the dominant role of the provider segment.

The medical device manufacturers segment is expected to witness the fastest CAGR of 17.8% through 2025–2032, as manufacturers face increasing regulatory expectations (such as FDA documentation requirements and the EU’s MDR guidelines) compelling security-by-design implementations. Manufacturers embed cybersecurity through secure firmware updates, hardware encryption, and threat testing within their product development lifecycle. As supply chain attacks rise, OEMs are under pressure to secure not only device functionality but also chain-of-custody and software provenance. In addition, manufacturers engage in post-market surveillance and vulnerability disclosure programs, collaborating with cybersecurity firms to release patches and updates—making them dynamic adopters of cybersecurity platforms optimized for medical hardware. Market demand is further supported by healthcare customers requiring validated cybersecurity as a condition of procurement for their device fleets.

Medical Device Cybersecurity Solutions Market Regional Analysis

- North America dominated the medical device cybersecurity solutions market with the largest revenue share of 40.5% in 2024, characterized by advanced healthcare infrastructure, high adoption of digital health technologies, and a strong regulatory environment

- Healthcare providers and device manufacturers in the region are prioritizing cybersecurity to protect patient data and ensure regulatory compliance, particularly in light of increasing ransomware and phishing attacks on hospitals and connected devices

- The market is also supported by the presence of leading cybersecurity firms, robust cloud adoption, and continuous investments in AI-driven and automated security solutions tailored for healthcare environments

U.S. Medical Device Cybersecurity Solutions Market Insight

The U.S. medical device cybersecurity solutions market captured the largest revenue in 2024 within North America, fueled by significant investments from healthcare institutions, growing awareness of cyber risks, and supportive federal policies. The U.S. is witnessing accelerated adoption of advanced cybersecurity platforms that provide real-time threat detection, network segmentation, and compliance monitoring. Moreover, the rising number of connected medical devices, combined with FDA’s updated cybersecurity guidelines for manufacturers, is driving hospitals, clinics, and device companies to implement comprehensive security frameworks.

Europe Medical Device Cybersecurity Solutions Market Insight

The Europe medical device cybersecurity solutions market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent data protection regulations such as GDPR and the EU Medical Device Regulation (MDR). The growing digitalization of healthcare systems and the adoption of telemedicine and cloud-based platforms are increasing the need for robust cybersecurity safeguards across the region. Europe is experiencing significant demand for secure medical device connectivity, endpoint protection, and regulatory-compliant solutions to ensure both patient safety and institutional resilience against cyberattacks.

U.K. Medical Device Cybersecurity Solutions Market Insight

The U.K. medical device cybersecurity solutions market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the rapid digital transformation of the National Health Service (NHS) and increasing integration of connected devices into healthcare. Rising concerns about ransomware incidents and data breaches are compelling healthcare providers to invest in cybersecurity platforms offering encryption, intrusion detection, and compliance management. The U.K.’s strong health IT ecosystem and government-backed initiatives for digital health security are expected to further stimulate market growth.

Germany Medical Device Cybersecurity Solutions Market Insight

The Germany medical device cybersecurity solutions market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s emphasis on data protection, technological innovation, and regulatory compliance. Germany’s healthcare sector is actively adopting secure cloud-based infrastructures and advanced endpoint security to manage growing cyber risks. The demand for privacy-focused, AI-enabled security platforms is gaining traction, aligning with local consumer expectations for data safety and institutional trust. The government’s strong stance on cybersecurity compliance across critical infrastructure further reinforces market adoption.

Asia-Pacific Medical Device Cybersecurity Solutions Market Insight

The Asia-Pacific medical device cybersecurity solutions market is poised to grow at the fastest CAGR of 9.5% during the forecast period of 2025 to 2032, driven by rapid urbanization, rising adoption of connected healthcare systems, and increasing government initiatives to strengthen medical cybersecurity. Countries such as China, India, Japan, and South Korea are witnessing accelerated investments in healthcare IT infrastructure, cloud-based hospital systems, and telemedicine platforms, all of which require advanced cybersecurity safeguards. The affordability of cybersecurity solutions, coupled with growing domestic vendors and international collaborations, is expected to significantly boost market expansion across the region.

Japan Medical Device Cybersecurity Solutions Market Insight

The Japan medical device cybersecurity solutions market is gaining momentum due to the country’s high-tech healthcare infrastructure, rapid digital adoption, and strong emphasis on patient safety. Hospitals and healthcare providers in Japan are increasingly prioritizing cybersecurity as the number of connected devices and telehealth platforms continues to rise. The aging population, along with government policies promoting secure digital health systems, is further spurring demand for medical device cybersecurity solutions. The market is also witnessing growth in AI-driven, automated platforms designed to detect and mitigate sophisticated cyber threats in real time.

China Medical Device Cybersecurity Solutions Market Insight

The China medical device cybersecurity solutions market accounted for the largest market revenue share in Asia-Pacific in 2024, supported by the country’s expanding healthcare infrastructure, strong digitalization initiatives, and rapid growth of connected medical devices. China’s push toward “smart hospitals” and government-backed data security laws are accelerating the adoption of advanced cybersecurity solutions. Local vendors, alongside global players, are contributing to competitive pricing and widespread deployment of security systems across both public and private healthcare facilities. The rising frequency of cyberattacks on healthcare institutions is further compelling hospitals and device manufacturers to integrate comprehensive cybersecurity solutions.

Medical Device Cybersecurity Solutions Market Share

The medical device cybersecurity solutions industry is primarily led by well-established companies, including:

- Cisco (U.S.)

- IBM Corporation (U.S.)

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Broadcom (U.S.)

- McAfee, LLC (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- Palo Alto Networks. (U.S.)

- ClearDATA (U.S.)

- DXC Technology Company (U.S.)

- Sophos Ltd. (U.K.)

- Fortinet, Inc. (U.S.)

- Zscaler, Inc. (U.S.)

- FireEye, Inc. (U.S.)

Latest Developments in Global Medical Device Cybersecurity Solutions Market

- In December 2022, Palo Alto Networks announced its Medical IoT Security offering — a dedicated solution to discover, segment, and protect connected medical devices in healthcare environments

- In August 2023, MedCrypt expanded its platform capabilities (including enhancements to Helm and Guardian) to provide SBOM vulnerability management, runtime protections, and product-security intelligence targeted at medical-device OEMs

- In September 2023, the U.S. Food and Drug Administration (FDA) issued final guidance titled “Cybersecurity in Medical Devices: Quality System Considerations and Content of Premarket Submissions,” clarifying expectations for embedding cybersecurity into device quality systems and premarket submissions

- In March 2024, the FDA released draft “Select Updates for the Premarket Cybersecurity Guidance: Section 524B of the FD&C Act” proposing clarifications for cyber-device definitions and premarket expectations, prompting manufacturers to accelerate compliance work

- In February 2024, a major ransomware incident involving Change Healthcare (part of UnitedHealth Group) disrupted services and highlighted systemic supply-chain exposure in healthcare IT — an event that substantially increased focus on vendor and device security

- In June 2024, a ransomware attack on Synnovis (a pathology/testing services provider) caused broad disruption to NHS services in southeast London; subsequent investigations linked the incident to critical service failures and reported at least one patient fatality related to the disruption. The incident renewed regulatory and provider urgency on operational resilience and cyber protections for critical healthcare services

- In January 2025, the FDA and CISA publicly identified cybersecurity vulnerabilities in certain patient monitors (e.g., Contec/Epsimed models), warning healthcare providers of potential unauthorized access and urging mitigations — underscoring continuing device-level risk

- In June 2025, the FDA issued an updated/replaced iteration of its premarket cybersecurity guidance (continuing the 2023–2024 regulatory momentum), further clarifying manufacturer obligations for premarket and postmarket cybersecurity controls for medical devices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET SIZE

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 TRIPOD DATA VALIDATION MODEL

2.2.4 MARKET GUIDE

2.2.5 MULTIVARIATE MODELLING

2.2.6 TOP TO BOTTOM ANALYSIS

2.2.7 CHALLENGE MATRIX

2.2.8 APPLICATION COVERAGE GRID

2.2.9 STANDARDS OF MEASUREMENT

2.2.10 VENDOR SHARE ANALYSIS

2.2.11 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.12 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET: RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHTS

5.1 PESTEL ANALYSIS

5.2 PORTER’S FIVE FORCES MODEL

5.3 SURGERIES/PROCEDURES IN VOLUMES

5.4 HOSPITALS AND UROLOGIST IN MIDDLE EAST REGION

6 INDUSTRY INSIGHTS

6.1 MICRO AND MACRO ECONOMIC FACTORS

6.2 PENETRATION AND GROWTH PROSPECT MAPPING

6.3 KEY PRICING STRATEGIES

6.4 INTERVIEWS WITH SPECIALIST

6.5 ANALYIS AND RECOMMENDATION

7 INTELLECTUAL PROPERTY (IP) PORTFOLIO

7.1 PATENT QUALITY AND STRENGTH

7.2 PATENT FAMILIES

7.3 LICENSING AND COLLABORATIONS

7.4 COMPETITIVE LANDSCAPE

7.5 IP STRATEGY AND MANAGEMENT

7.6 OTHER

8 COST ANALYSIS BREAKDOWN

9 TECHNONLOGY ROADMAP

10 INNOVATION TRACKER AND STRATEGIC ANALYSIS

10.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

10.1.1 JOINT VENTURES

10.1.2 MERGERS AND ACQUISITIONS

10.1.3 LICENSING AND PARTNERSHIP

10.1.4 TECHNOLOGY COLLABORATIONS

10.1.5 STRATEGIC DIVESTMENTS

10.2 NUMBER OF PRODUCTS IN DEVELOPMENT

10.3 STAGE OF DEVELOPMENT

10.4 TIMELINES AND MILESTONES

10.5 INNOVATION STRATEGIES AND METHODOLOGIES

10.6 RISK ASSESSMENT AND MITIGATION

10.7 FUTURE OUTLOOK

11 REGULATORY COMPLIANCE

11.1 REGULATORY AUTHORITIES

11.2 REGULATORY CLASSIFICATIONS

11.2.1 CLASS I

11.2.2 CLASS II

11.2.3 CLASS III

11.3 REGULATORY SUBMISSIONS

11.4 INTERNATIONAL HARMONIZATION

11.5 COMPLIANCE AND QUALITY MANAGEMENT SYSTEMS

11.6 REGULATORY CHALLENGES AND STRATEGIES

12 REIMBURSEMENT FRAMEWORK

13 OPPUTUNITY MAP ANALYSIS

14 INSTALLED BASE DATA

15 VALUE CHAIN ANALYSIS

16 HEALTHCARE ECONOMY

16.1 HEALTHCARE EXPENDITURE

16.2 CAPITAL EXPENDITURE

16.3 CAPEX TRENDS

16.4 CAPEX ALLOCATION

16.5 FUNDING SOURCES

16.6 INDUSTRY BENCHMARKS

16.7 GDP RATION IN OVERALL GDP

16.8 HEALTHCARE SYSTEM STRUCTURE

16.9 GOVERNMENT POLICIES

16.1 ECONOMIC DEVELOPMENT

17 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY OFFERINGS

17.1 OVERVIEW

17.2 SOLUTIONS

17.2.1 IDENTITY & ACCESS MANAGEMENT SOLUTIONS

17.2.2 ANTIVIRUS/ANTIMALWARE SOLUTIONS

17.2.3 ENCRYPTION SOLUTIONS

17.2.4 DATA LOSS PREVENTION SOLUTIONS

17.2.5 RISK & COMPLIANCE MANAGEMENT

17.2.6 INTRUSION DETECTION SYSTEMS/INTRUSION PREVENTION SYSTEMS

17.2.7 DISASTER RECOVERY SOLUTIONS

17.2.8 DISTRIBUTED DENIAL OF SERVICE SOLUTIONS

17.2.9 OTHER SOLUTIONS

17.3 SERVICES

17.3.1 MANAGED SERVICES

17.3.2 PROFESSIONAL SERVICES

18 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY TYPE

18.1 OVERVIEW

18.2 NETWORK SECURITY

18.3 ENDPOINT SECURITY

18.4 APPLICATION SECURITY

18.5 CLOUD SECURITY

18.6 OTHER SECURITY TYPES

19 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY DEPLOYMENT

19.1 OVERVIEW

19.2 CLOUD

19.2.1 PRIVATE CLOUD

19.2.2 PUBLIC CLOUD

19.2.3 HYBRID CLOUD

19.3 ON-PREMISES

20 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY DEVICES CLASS

20.1 OVERVIEW

20.2 CLASS 1

20.3 CLASS 2

20.4 CLASS 3

21 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY DEVICE THERAPEUTIC SPECIALITIES

21.1 OVERVIEW

21.2 ORTHOPEDICS

21.3 CARDIOVASCULAR

21.4 WOUND CARE & DERMATOLOGY

21.5 GENERAL & PLASTIC SURGERY

21.6 SPINE

21.7 BIOLOGICS & COMBINATION PRODUCTS

21.8 NEUROLOGY & NEUROSURGERY

21.9 IMAGING

21.1 DENTAL

21.11 DIGITAL HEALTH

21.12 IN-VITRO DIAGNOSTICS

21.13 ANESTHESIA

21.14 OTHERS

22 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY DEVICE TYPE

22.1 OVERVIEW

22.2 HOSPITAL MEDICAL DEVICES

22.2.1 VITAL SIGNS MONITORING DEVICES

22.2.1.1. BLOOD GLUCOSE MONITORS

22.2.1.2. ECGS/HEART RATE MONITORS

22.2.1.3. BLOOD PRESSURE MONITORS

22.2.1.4. MULTIPARAMETER MONITORS

22.2.1.5. OTHERS

22.2.2 IMAGING SYSTEMS

22.2.3 SMART INFUSION PUMP

22.2.4 FETAL MONITORING DEVICES

22.2.5 OTHERS

22.3 WEARABLE AND EXTERNAL MEDICAL DEVICES

22.3.1 DIABETES CARE

22.3.2 FITNESS MONITORING

22.3.3 SLEEP TRACKING

22.3.4 OTHERS

22.4 INTERNALLY EMBEDDED MEDICAL DEVICES

22.4.1 PACEMAKER

22.4.2 IMPLANTABLE CARDIAC MONITORS

22.4.3 NEUROLOGICAL DEVICES

22.4.4 HEARING DEVICES

22.4.5 OTHERS

22.5 OTHERS

23 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY ENTERPRIZE SIZE

23.1 OVERVIEW

23.2 LARGE ENTERPRIZE

23.3 MID SIZE ENTERPRIZE

23.4 SMALL SIZE ENTERPRIZE

24 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY END-USER

24.1 OVERVIEW

24.2 CONTRACT RESEARCH ORGANIZATION

24.3 COMPONENTS MANUFACTURERS

24.4 OEMS

24.5 MEDICAL DEVICE MANUFACTURERS

24.6 HEALTHCARE PAYERS

24.7 OTHERS

25 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, COMPANY LANDSCAPE

25.1 COMPANY SHARE ANALYSIS: GLOBAL

25.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

25.3 COMPANY SHARE ANALYSIS: EUROPE

25.4 COMPANY SHARE ANALYSIS: ASIA PACIFIC

25.5 MERGERS & ACQUISITIONS

25.6 NEW PRODUCT DEVELOPMENT & APPROVALS

25.7 EXPANSIONS

25.8 REGULATORY CHANGES

25.9 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

26 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, BY GEOGRAPHY

GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

26.1 NORTH AMERICA

26.1.1 U.S.

26.1.2 CANADA

26.1.3 MEXICO

26.2 EUROPE

26.2.1 GERMANY

26.2.2 FRANCE

26.2.3 U.K.

26.2.4 HUNGARY

26.2.5 LITHUANIA

26.2.6 AUSTRIA

26.2.7 IRELAND

26.2.8 NORWAY

26.2.9 POLAND

26.2.10 ITALY

26.2.11 SPAIN

26.2.12 RUSSIA

26.2.13 TURKEY

26.2.14 NETHERLANDS

26.2.15 SWITZERLAND

26.2.16 REST OF EUROPE

26.3 ASIA-PACIFIC

26.3.1 JAPAN

26.3.2 CHINA

26.3.3 SOUTH KOREA

26.3.4 INDIA

26.3.5 AUSTRALIA

26.3.6 SINGAPORE

26.3.7 THAILAND

26.3.8 MALAYSIA

26.3.9 INDONESIA

26.3.10 PHILIPPINES

26.3.11 VIETNAM

26.3.12 REST OF ASIA-PACIFIC

26.4 SOUTH AMERICA

26.4.1 BRAZIL

26.4.2 ARGENTINA

26.4.3 PERU

26.4.4 COLOMBIA

26.4.5 VENEZUELA

26.4.6 REST OF SOUTH AMERICA

26.5 MIDDLE EAST AND AFRICA

26.5.1 SOUTH AFRICA

26.5.2 SAUDI ARABIA

26.5.3 UAE

26.5.4 EGYPT

26.5.5 KUWAIT

26.5.6 ISRAEL

26.5.7 REST OF MIDDLE EAST AND AFRICA

26.6 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

27 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, SWOT AND DBMR ANALYSIS

28 GLOBAL MEDICAL DEVICE CYBERSECURITY SOLUTIONS MARKET, COMPANY PROFILE

29 COMPANY PROFILE FOR WIRELESS TECHNOLOGY BASED DEVICES

29.1 ORDR

29.1.1 COMPANY OVERVIEW

29.1.2 REVENUE ANALYSIS

29.1.3 GEOGRAPHIC PRESENCE

29.1.4 PRODUCT PORTFOLIO

29.1.5 RECENT DEVELOPMENTS

29.2 TRIMEDX.

29.2.1 COMPANY OVERVIEW

29.2.2 REVENUE ANALYSIS

29.2.3 GEOGRAPHIC PRESENCE

29.2.4 PRODUCT PORTFOLIO

29.2.5 RECENT DEVELOPMENTS

29.3 DXC TECHNOLOGY COMPANY

29.3.1 COMPANY OVERVIEW

29.3.2 REVENUE ANALYSIS

29.3.3 GEOGRAPHIC PRESENCE

29.3.4 PRODUCT PORTFOLIO

29.3.5 RECENT DEVELOPMENTS

29.4 ASIMILY

29.4.1 COMPANY OVERVIEW

29.4.2 REVENUE ANALYSIS

29.4.3 GEOGRAPHIC PRESENCE

29.4.4 PRODUCT PORTFOLIO

29.4.5 RECENT DEVELOPMENTS

29.5 FORESCOUT

29.5.1 COMPANY OVERVIEW

29.5.2 REVENUE ANALYSIS

29.5.3 GEOGRAPHIC PRESENCE

29.5.4 PRODUCT PORTFOLIO

29.5.5 RECENT DEVELOPMENTS

29.6 TÜV RHEINLAND

29.6.1 COMPANY OVERVIEW

29.6.2 REVENUE ANALYSIS

29.6.3 GEOGRAPHIC PRESENCE

29.6.4 PRODUCT PORTFOLIO

29.6.5 RECENT DEVELOPMENTS

29.7 ATOS SE

29.7.1 COMPANY OVERVIEW

29.7.2 REVENUE ANALYSIS

29.7.3 GEOGRAPHIC PRESENCE

29.7.4 PRODUCT PORTFOLIO

29.7.5 RECENT DEVELOPMENTS

29.8 BROADCOM

29.8.1 COMPANY OVERVIEW

29.8.2 REVENUE ANALYSIS

29.8.3 GEOGRAPHIC PRESENCE

29.8.4 PRODUCT PORTFOLIO

29.8.5 RECENT DEVELOPMENTS

29.9 AT&T INTELLECTUAL PROPERTY.

29.9.1 COMPANY OVERVIEW

29.9.2 REVENUE ANALYSIS

29.9.3 GEOGRAPHIC PRESENCE

29.9.4 PRODUCT PORTFOLIO

29.9.5 RECENT DEVELOPMENTS

29.1 SOPHOS LTD.

29.10.1 COMPANY OVERVIEW

29.10.2 REVENUE ANALYSIS

29.10.3 GEOGRAPHIC PRESENCE

29.10.4 PRODUCT PORTFOLIO

29.10.5 RECENT DEVELOPMENTS

29.11 CLOUDWAVE SENSATO CYBERSECURITY

29.11.1 COMPANY OVERVIEW

29.11.2 REVENUE ANALYSIS

29.11.3 GEOGRAPHIC PRESENCE

29.11.4 PRODUCT PORTFOLIO

29.11.5 RECENT DEVELOPMENTS

29.12 BOOZ ALLEN HAMILTON INC.

29.12.1 COMPANY OVERVIEW

29.12.2 REVENUE ANALYSIS

29.12.3 GEOGRAPHIC PRESENCE

29.12.4 PRODUCT PORTFOLIO

29.12.5 RECENT DEVELOPMENTS

29.13 IBM CORPORATION

29.13.1 COMPANY OVERVIEW

29.13.2 REVENUE ANALYSIS

29.13.3 GEOGRAPHIC PRESENCE

29.13.4 PRODUCT PORTFOLIO

29.13.5 RECENT DEVELOPMENTS

29.14 CROWDSTRIKE HOLDINGS, INC

29.14.1 COMPANY OVERVIEW

29.14.2 REVENUE ANALYSIS

29.14.3 GEOGRAPHIC PRESENCE

29.14.4 PRODUCT PORTFOLIO

29.14.5 RECENT DEVELOPMENTS

29.15 IMPRIVATA, INC.

29.15.1 COMPANY OVERVIEW

29.15.2 REVENUE ANALYSIS

29.15.3 GEOGRAPHIC PRESENCE

29.15.4 PRODUCT PORTFOLIO

29.15.5 RECENT DEVELOPMENTS

29.16 PALO ALTO NETWORKS

29.16.1 COMPANY OVERVIEW

29.16.2 REVENUE ANALYSIS

29.16.3 GEOGRAPHIC PRESENCE

29.16.4 PRODUCT PORTFOLIO

29.16.5 RECENT DEVELOPMENTS

29.17 IMPERVA

29.17.1 COMPANY OVERVIEW

29.17.2 REVENUE ANALYSIS

29.17.3 GEOGRAPHIC PRESENCE

29.17.4 PRODUCT PORTFOLIO

29.17.5 RECENT DEVELOPMENTS

29.18 CISCO SYSTEMS, INC

29.18.1 COMPANY OVERVIEW

29.18.2 REVENUE ANALYSIS

29.18.3 GEOGRAPHIC PRESENCE

29.18.4 PRODUCT PORTFOLIO

29.18.5 RECENT DEVELOPMENTS

29.19 ABSOLUTE SOFTWARE CORPORATION

29.19.1 COMPANY OVERVIEW

29.19.2 REVENUE ANALYSIS

29.19.3 GEOGRAPHIC PRESENCE

29.19.4 PRODUCT PORTFOLIO

29.19.5 RECENT DEVELOPMENTS

29.2 FORTRA, LLC

29.20.1 COMPANY OVERVIEW

29.20.2 REVENUE ANALYSIS

29.20.3 GEOGRAPHIC PRESENCE

29.20.4 PRODUCT PORTFOLIO

29.20.5 RECENT DEVELOPMENTS

29.21 ALLCLEAR ID.

29.21.1 COMPANY OVERVIEW

29.21.2 REVENUE ANALYSIS

29.21.3 GEOGRAPHIC PRESENCE

29.21.4 PRODUCT PORTFOLIO

29.21.5 RECENT DEVELOPMENTS

29.22 ARMIS INC

29.22.1 COMPANY OVERVIEW

29.22.2 REVENUE ANALYSIS

29.22.3 GEOGRAPHIC PRESENCE

29.22.4 PRODUCT PORTFOLIO

29.22.5 RECENT DEVELOPMENTS

29.23 CLAROTY

29.23.1 COMPANY OVERVIEW

29.23.2 REVENUE ANALYSIS

29.23.3 GEOGRAPHIC PRESENCE

29.23.4 PRODUCT PORTFOLIO

29.23.5 RECENT DEVELOPMENTS

29.24 TREND MICRO INCORPORATED

29.24.1 COMPANY OVERVIEW

29.24.2 REVENUE ANALYSIS

29.24.3 GEOGRAPHIC PRESENCE

29.24.4 PRODUCT PORTFOLIO

29.24.5 RECENT DEVELOPMENTS

29.25 GE HEALTHCARE

29.25.1 COMPANY OVERVIEW

29.25.2 REVENUE ANALYSIS

29.25.3 GEOGRAPHIC PRESENCE

29.25.4 PRODUCT PORTFOLIO

29.25.5 RECENT DEVELOPMENTS

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

30 RELATED REPORTS

31 QUESTIONNAIRE

32 ABOUT DATA BRIDGE MARKET RESEARCH

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.