Global Medical Digital Imaging Systems Market

Market Size in USD Billion

USD

20.82 Billion

USD

39.60 Billion

2025

2033

USD

20.82 Billion

USD

39.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.82 Billion | |

| USD 39.60 Billion | |

| % | |

|

Medical Digital Imaging Systems Market Overview

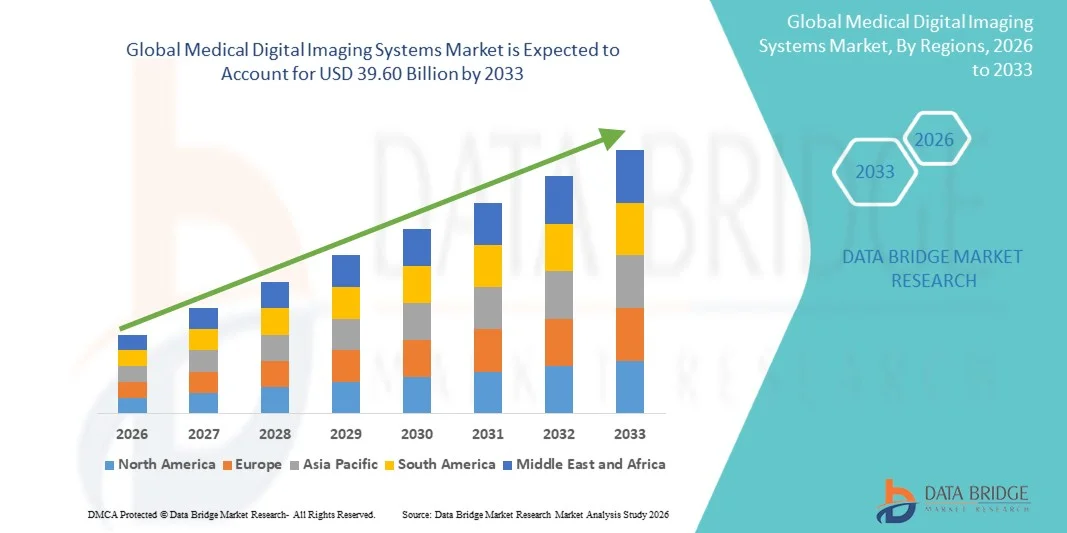

The Medical Digital Imaging Systems Market was valued at USD 20.82 billion in 2025 and is projected to reach USD 39.60 billion by 2033, growing at a CAGR of 8.37% from 2026 to 2033. The market is witnessing steady expansion driven by the rising prevalence of chronic diseases, increasing demand for early and accurate diagnosis, and continuous technological advancements in imaging modalities such as MRI, CT, X-ray, ultrasound, and hybrid imaging systems. Growing healthcare infrastructure development and digital transformation across hospitals and diagnostic centers are further supporting market adoption.

The increasing burden of cardiovascular diseases, cancer, and neurological disorders globally is accelerating the need for high-resolution, real-time imaging solutions that enable precise clinical decision-making. In addition, the integration of artificial intelligence, cloud-based imaging platforms, and advanced image processing software is enhancing workflow efficiency and diagnostic accuracy. Expanding applications in tele-radiology, minimally invasive procedures, and personalized medicine are further driving the transition from conventional imaging systems to advanced digital imaging ecosystems across both developed and emerging healthcare markets.

Key Market Trends & Insights

- North America dominated the Medical Digital Imaging Systems Market with the largest revenue share of 36.92% in 2025, supported by advanced healthcare infrastructure, high diagnostic imaging adoption, and strong presence of leading imaging technology providers.

- The MRI segment led the market with a 34.18% share in 2025, driven by its superior soft-tissue contrast and high diagnostic accuracy across complex disease conditions.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by expanding healthcare access, rising chronic disease burden, and rapid hospital infrastructure development in China, India, and Southeast Asia.

- CT are the fastest-growing type of test type, projected to register a CAGR of 7.1%, reflecting the surge in demand for rapid, high-resolution diagnostic imaging in emergency and critical care settings

- The 3D/4D segment dominated the technology category with a 56.12% revenue share in 2025, led by its advanced visualization capabilities and superior diagnostic accuracy.

- Oncology accounted for 38.45% of the market, preferred by the rising global burden of cancer and increasing reliance on imaging for diagnosis and treatment planning.

- The cardiology segment is the fastest-growing application category, with a CAGR of 7.3%, driven by the increasing prevalence of cardiovascular diseases globally.

Market Size & Forecast

- Global Market Value (2025): USD 20.82 Billion

- Expected Market Value (2033): USD 39.60 Billion

- Forecast CAGR (2026–2033): 8.37%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Medical Digital Imaging Systems Market Segmentation

|

Attributes |

Medical Digital Imaging Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Siemens Healthineers AG (Germany) · GE HealthCare (U.S.) · Koninklijke Philips N.V. (Netherlands) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · FUJIFILM Holdings Corporation (Japan) · Samsung Medison Co., Ltd. (South Korea) · Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China) · Shimadzu Corporation (Japan) · Carestream Health, Inc. (U.S.) · Hologic, Inc. (U.S.) · Agfa-Gevaert N.V. (Belgium) · Esaote S.p.A. (Italy) · United Imaging Healthcare Co., Ltd. (China) · Ziehm Imaging GmbH (Germany) · Planmed Oy (Finland) · Konica Minolta Healthcare Americas, Inc. (U.S.) · Delphinus Medical Technologies, Inc. (U.S.) · Ziehm Imaging GmbH (Germany) · Trivitron Healthcare Pvt. Ltd. (India) · Allengers Medical Systems Limited (India) |

|

Market Opportunities |

· Rapid integration of AI-powered radiology platforms · Expansion of tele-radiology and cloud-based imaging services · Growing demand for hybrid and multi-modality imaging systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Medical Digital Imaging Systems Market Trends

Trend: Growth in AI-Assisted Diagnostic Imaging and Clinical Workflow Automation

Hospitals and diagnostic centers are increasingly adopting AI-integrated imaging systems to enhance diagnostic precision, reduce interpretation time, and support radiologists in detecting early-stage diseases such as cancer, cardiovascular abnormalities, and neurological disorders. Advanced algorithms enable automated image reconstruction, anomaly detection, and quantitative analysis across CT, MRI, and ultrasound modalities. Cloud-based imaging platforms are also being deployed to enable real-time collaboration between radiologists across different geographies, improving access to specialist care while reducing reporting delays. For instance, AI-enabled radiology platforms integrated into hospital PACS systems are streamlining imaging workflows and improving diagnostic consistency.

Medical Digital Imaging Systems Market Dynamics

Key Market Driver: Rising Burden of Chronic Diseases and Demand for Early Diagnosis

The increasing global prevalence of chronic conditions such as cancer, cardiovascular diseases, and neurological disorders is driving strong demand for advanced diagnostic imaging systems that enable early detection and accurate disease characterization. Healthcare providers are increasingly relying on high-resolution imaging modalities such as MRI, CT, and PET-CT to support clinical decision-making and treatment planning. Growing investments in hospital infrastructure and diagnostic center expansion are further accelerating adoption across both developed and emerging markets. For instance, large hospital networks are upgrading from analog to fully digital imaging suites to improve diagnostic speed and patient outcomes.

Key Restraint/Challenge: High Cost of Advanced Imaging Equipment and Maintenance

A major challenge in the Medical Digital Imaging Systems Market is the high acquisition cost of advanced imaging modalities, along with significant expenses related to installation, maintenance, and skilled operator requirements. Small and mid-sized healthcare facilities often face difficulties in adopting high-end systems such as MRI and PET-CT due to budget constraints and infrastructure limitations. In addition, recurring costs associated with software upgrades, service contracts, and regulatory compliance further increase the total cost of ownership. For instance, advanced multi-modality imaging systems require continuous calibration and specialized technical support, limiting widespread adoption in cost-sensitive healthcare settings.

Key Market Opportunity: Expansion of AI-Driven Cloud Imaging and Remote Diagnostics

The integration of AI and cloud computing in medical imaging presents a major growth opportunity by enabling scalable, remote, and real-time diagnostic services across healthcare networks. Cloud-based imaging platforms allow secure storage, sharing, and analysis of large imaging datasets, improving collaboration between radiologists and specialists across regions. AI-powered tools further enhance diagnostic accuracy by supporting automated image interpretation and predictive analytics for early disease detection. For instance, cloud-based teleradiology networks are enabling remote reporting of CT and MRI scans from centralized expert hubs to rural hospitals and diagnostic centers.

Medical Digital Imaging Systems Market Scope

The medical digital imaging systems market is segmented on the basis of type of test, technology, application, and end use.

- By Type of Test

On the basis of type of test, the Medical Digital Imaging Systems Market is segmented into X-Ray, MRI, Ultrasound, CT, and Nuclear Imaging. The MRI segment dominated the market with a 34.18% share in 2025, owing to its superior soft-tissue contrast and high diagnostic accuracy across complex disease conditions. These systems are widely used in neurology, oncology, and musculoskeletal imaging where detailed anatomical visualization is critical. Increasing prevalence of neurological disorders and cancer is significantly driving demand for MRI-based diagnostics. Continuous advancements in high-field MRI systems and functional imaging are enhancing image resolution and clinical utility. Hospitals and advanced diagnostic centers are rapidly upgrading to digital MRI platforms for improved workflow efficiency. Its non-invasive nature and broad clinical applicability continue to reinforce its dominance across healthcare systems globally.

The CT segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by rising demand for rapid, high-resolution diagnostic imaging in emergency and critical care settings. CT scanners are extensively used in trauma diagnosis, oncology staging, and cardiovascular imaging due to their speed and accuracy. Increasing global incidence of accidents and chronic diseases is further boosting adoption. Technological advancements such as low-dose CT and AI-assisted image reconstruction are improving patient safety and diagnostic precision. Expanding deployment in preventive screening programs is also accelerating market growth. Strong adoption in emerging healthcare infrastructures is further supporting segment expansion.

- By Technology

On the basis of technology, the Medical Digital Imaging Systems Market is segmented into 2D and 3D/4D imaging systems. The 3D/4D imaging segment dominated the market with a 56.21% share in 2025, driven by its advanced visualization capabilities and superior diagnostic accuracy. These systems enable detailed anatomical reconstruction, allowing precise evaluation of complex diseases such as cancer, cardiovascular disorders, and neurological abnormalities. They are widely used in hospitals and specialty diagnostic centers for high-end clinical applications. Integration with AI-based reconstruction and image enhancement tools is improving diagnostic efficiency. Increasing adoption in surgical planning and interventional procedures is further strengthening demand. Continuous technological innovation is consolidating its position as the leading imaging technology segment globally.

The 2D imaging segment is expected to grow at a CAGR of 6.8% from 2026 to 2033, driven by its affordability and widespread use in primary healthcare settings. It remains essential for routine diagnostics, basic screening, and initial patient evaluation. Increasing deployment in rural hospitals and low-resource settings is supporting adoption. Technological upgrades are improving image quality even in cost-sensitive systems. Rising demand for point-of-care diagnostics is further accelerating growth. Its accessibility and low operational cost continue to drive strong penetration in emerging healthcare markets.

- By Application

On the basis of application, the market is segmented into cardiology, oncology, neurology, urology, gynecology, and others. The oncology segment dominated the market with a 38.45% share in 2025, driven by the rising global burden of cancer and increasing reliance on imaging for diagnosis and treatment planning. Advanced imaging modalities such as CT, MRI, and PET-CT are widely used for tumor detection, staging, and therapy monitoring. Growing adoption of precision oncology is further increasing demand for high-resolution imaging systems. Hospitals are heavily investing in oncology-focused diagnostic infrastructure. Hybrid imaging technologies are improving early detection accuracy and clinical outcomes. Expanding cancer screening initiatives continue to reinforce this segment’s dominance.

The cardiology segment is expected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by the increasing prevalence of cardiovascular diseases globally. Imaging systems are increasingly used for early detection of heart conditions, vascular abnormalities, and structural disorders. Technologies such as CT angiography and cardiac MRI are gaining rapid clinical adoption. Rising demand for non-invasive and precise diagnostic methods is further supporting growth. Integration of AI in cardiac imaging analysis is enhancing diagnostic speed and accuracy. Expanding preventive cardiology programs are accelerating market expansion worldwide.

- By End Use

On the basis of end use, the market is segmented into hospitals, diagnostic imaging centers, and others. The hospitals segment dominated the market with a 44.83% share in 2025, driven by high patient inflow and availability of advanced imaging infrastructure. Hospitals extensively use MRI, CT, X-ray, and ultrasound systems for comprehensive diagnostic and treatment planning. Increasing investment in digital healthcare transformation is further strengthening adoption. Integration with PACS and hospital information systems is improving workflow efficiency and data management. Growing demand for multi-specialty clinical services is expanding imaging utilization. Continuous upgrades in hospital-based diagnostic capabilities are reinforcing segment leadership globally.

The diagnostic imaging centers segment is projected to grow at a CAGR of 7.5% from 2026 to 2033, driven by increasing demand for standalone, specialized diagnostic services. These centers offer faster turnaround times and cost-effective imaging solutions compared to hospitals. Rising outsourcing of diagnostic imaging services is boosting market expansion. Growth of private diagnostic chains in emerging economies is further accelerating adoption. Technological advancements in compact, high-performance imaging systems are enabling scalability. Increasing patient preference for accessible and efficient diagnostics is driving strong global growth.

Medical Digital Imaging Systems Market Regional Analysis

North America dominated the Medical Digital Imaging Systems Market with the largest revenue share of 36.92% in 2025, supported by advanced healthcare infrastructure, high diagnostic imaging adoption, and strong presence of leading imaging technology providers. The region benefits from a high prevalence of chronic diseases such as cancer and cardiovascular disorders, driving continuous demand for advanced diagnostic imaging solutions. Strong reimbursement frameworks, early adoption of AI-enabled imaging systems, and widespread integration of digital healthcare platforms further strengthen market growth. Increasing investments in hospital modernization and diagnostic center expansion continue to reinforce North America’s leadership position in the global market.

U.S. Medical Digital Imaging Systems Market Insight

The U.S. medical digital imaging systems market is witnessing strong growth due to rising prevalence of chronic diseases, advanced healthcare infrastructure, and high adoption of AI-enabled diagnostic technologies. The country’s well-established hospital network, strong reimbursement policies, and presence of leading imaging equipment manufacturers are driving demand across MRI, CT, X-ray, and ultrasound systems. Increasing investments in precision medicine, early disease detection programs, and hospital digital transformation initiatives are further supporting market expansion across clinical and research applications. Growing integration of cloud-based imaging platforms and AI-assisted diagnostics continues to strengthen efficiency and clinical outcomes in the U.S. healthcare system.

Europe Medical Digital Imaging Systems Market Insight

The Europe medical digital imaging systems market remains a major contributor to global revenue, driven by strong healthcare systems, stringent regulatory standards, and high demand for advanced diagnostic imaging solutions. Widespread use of MRI, CT, and hybrid imaging technologies in oncology, cardiology, and neurology is supporting market expansion across the region. Government initiatives promoting early disease detection and digital healthcare adoption are further strengthening demand. Increasing investments in hospital modernization and AI-powered imaging platforms, along with a strong focus on clinical accuracy and patient safety, continue to enhance adoption of advanced imaging systems throughout Europe.

U.K. Medical Digital Imaging Systems Market Insight

The U.K. medical digital imaging systems market is experiencing steady growth, supported by increasing adoption of advanced diagnostic imaging technologies within the National Health Service (NHS) and private healthcare sector. Rising demand for early diagnosis of cancer, cardiovascular diseases, and neurological disorders is driving uptake of MRI, CT, and ultrasound systems. Investments in digital health transformation and AI-based radiology tools are improving diagnostic efficiency and workflow management. In addition, growing focus on reducing diagnostic waiting times and enhancing patient outcomes is further accelerating the adoption of modern imaging infrastructure across the U.K. healthcare system.

Germany Medical Digital Imaging Systems Market Insight

The Germany medical digital imaging systems market is expanding steadily due to its strong healthcare infrastructure, advanced medical technology base, and increasing demand for high-precision diagnostic solutions. German hospitals and diagnostic centers are widely adopting MRI, CT, and 3D/4D imaging systems for complex disease diagnosis and treatment planning. Strong emphasis on medical innovation, research, and engineering excellence is supporting continuous technological advancements in imaging systems. In addition, government focus on digital healthcare integration and rising incidence of chronic diseases are further driving adoption across clinical and research applications in Germany.

Asia-Pacific Medical Digital Imaging Systems Market Insight

The Asia-Pacific medical digital imaging systems market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising chronic disease burden, and increasing access to diagnostic services across developing economies. Countries such as China, India, and Japan are investing heavily in hospital expansion and advanced imaging technologies. Growing awareness of early disease detection, coupled with rising adoption of AI-enabled and cost-effective imaging systems, is supporting regional market expansion. In addition, increasing medical tourism and growing private healthcare investments are accelerating demand for MRI, CT, and ultrasound systems across the region.

Japan Medical Digital Imaging Systems Market Insight

The Japan medical digital imaging systems market is witnessing consistent growth due to advanced healthcare infrastructure, aging population, and strong focus on early and accurate disease diagnosis. High adoption of MRI, CT, and hybrid imaging systems is driven by the need for precise diagnostics in oncology, neurology, and cardiology. Continuous technological innovation, including integration of AI and high-resolution imaging systems, is enhancing diagnostic accuracy and workflow efficiency. In addition, Japan’s emphasis on preventive healthcare and minimally invasive diagnostic techniques is further supporting steady market expansion across hospitals and diagnostic centers.

China Medical Digital Imaging Systems Market Insight

The China medical digital imaging systems market is growing rapidly, driven by increasing healthcare investments, expanding hospital infrastructure, and rising burden of chronic diseases. Strong government initiatives to improve healthcare access and diagnostic capabilities are boosting adoption of advanced imaging systems such as CT, MRI, and ultrasound. Rapid urbanization and growing demand for early disease detection are further supporting market expansion. In addition, increasing integration of AI-based imaging technologies and domestic manufacturing capabilities are positioning China as one of the fastest-growing markets for medical digital imaging systems globally.

Medical Digital Imaging Systems Market Share

The medical digital imaging systems industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Samsung Medison Co., Ltd. (South Korea)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Shimadzu Corporation (Japan)

- Carestream Health, Inc. (U.S.)

- Hologic, Inc. (U.S.)

- Agfa-Gevaert N.V. (Belgium)

- Esaote S.p.A. (Italy)

- United Imaging Healthcare Co., Ltd. (China)

- Ziehm Imaging GmbH (Germany)

- Planmed Oy (Finland)

- Konica Minolta Healthcare Americas, Inc. (U.S.)

- Delphinus Medical Technologies, Inc. (U.S.)

- Ziehm Imaging GmbH (Germany)

- Trivitron Healthcare Pvt. Ltd. (India)

- Allengers Medical Systems Limited (India)

Latest Developments in Medical Digital Imaging Systems Market

- In March 2024, Philips announced the launch of its Spectral CT 7500 system, a next-generation spectral computed tomography platform designed to enhance diagnostic confidence through advanced material decomposition and improved tissue characterization. The system enables faster scanning with improved image quality and reduced motion artifacts, supporting applications in cardiology, oncology, and emergency care. It also integrates workflow automation to improve efficiency in high-volume clinical settings. This launch represents a significant advancement in spectral imaging technology

- In March 2023, GE HealthCare expanded its ultrasound portfolio with enhancements to its LOGIQ E10 Series, incorporating advanced AI-driven imaging features to improve diagnostic precision in radiology, cardiology, and obstetrics applications. The upgraded system focuses on automation, enhanced image resolution, and improved workflow integration for clinicians. It supports faster and more consistent imaging outcomes across diverse clinical environments. This development reflects GE’s growing emphasis on AI-enabled diagnostic imaging solutions

- In March 2022, GE HealthCare introduced the Revolution Apex CT system, an advanced computed tomography platform designed to improve image clarity, speed, and workflow efficiency across emergency, cardiac, and oncology imaging applications. The system integrates AI-based reconstruction tools to enhance diagnostic accuracy while reducing scan times and radiation dose. It was developed to support high-volume clinical environments with improved operational efficiency. This launch highlighted GE’s continued innovation in precision CT imaging and patient-centered diagnostic solutions

- In November 2021, Philips announced the launch of its next-generation MR 7700 MRI system, designed to deliver high-performance neuro and whole-body imaging with improved gradient strength and advanced AI-enabled reconstruction capabilities. The system was developed to support demanding clinical and research applications, particularly in neurology and oncology. It also enhanced workflow efficiency through faster scan times and improved patient comfort features. This launch reinforced Philips’ focus on innovation in high-field MRI systems and digital imaging transformation

- In September 2021, Siemens Healthineers announced the FDA clearance and launch of its Naeotom Alpha photon-counting CT system, marking a major breakthrough in computed tomography imaging by enabling ultra-high resolution, spectral imaging, and improved dose efficiency for cardiovascular and oncology diagnostics. The system introduced a new detector technology that significantly enhances image quality while reducing radiation exposure, making it a milestone innovation in next-generation CT imaging. This development strengthened Siemens’ leadership in advanced diagnostic imaging and precision medicine applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.