Global Medical Electronics Market

Market Size in USD Billion

USD

8.91 Billion

USD

16.49 Billion

2025

2033

USD

8.91 Billion

USD

16.49 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.91 Billion | |

| USD 16.49 Billion | |

| % | |

|

Medical Electronics Market Overview

The Medical Electronics Market was valued at USD 8.91 billion in 2025 and is projected to reach USD 16.49 billion by 2033, growing at a CAGR of 8.00% from 2026 to 2033. The market is witnessing strong growth driven by rising adoption of advanced diagnostic and monitoring devices, increasing integration of electronics in healthcare systems, and rapid technological advancements in wearable and portable medical equipment. Growing demand for early disease detection and real-time patient monitoring is further accelerating the use of smart electronic medical devices across hospitals, clinics, and home healthcare settings.

The increasing prevalence of chronic diseases, combined with an aging global population and rising healthcare expenditure, is significantly boosting demand for medical electronics across imaging systems, patient monitoring devices, implantable electronics, and therapeutic equipment. In addition, the shift toward digital healthcare, telemedicine, and connected medical devices is encouraging healthcare providers to adopt advanced electronic systems that enhance diagnostic accuracy, improve treatment efficiency, and enable continuous remote patient care.

Key Market Trends & Insights

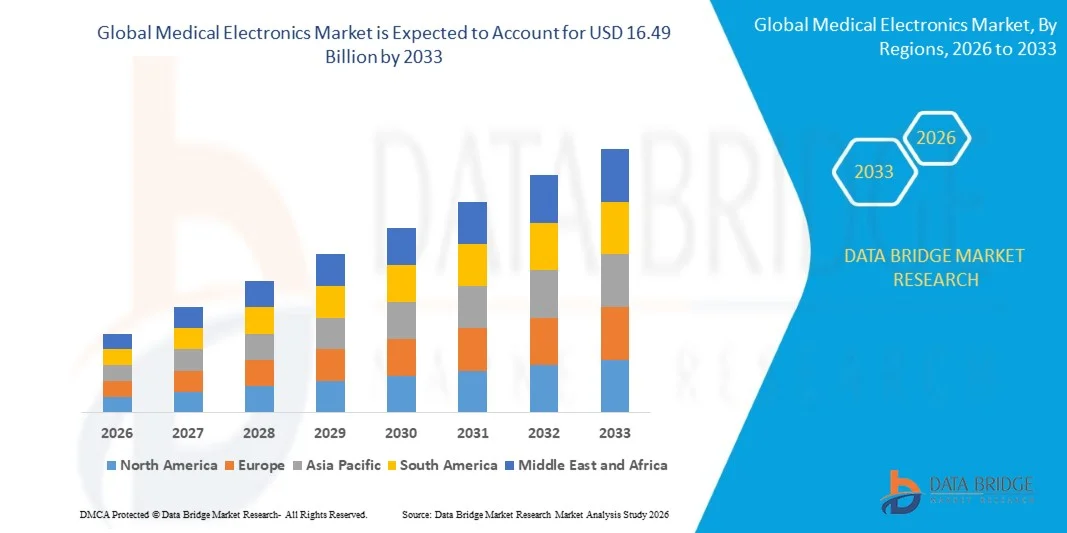

- North America dominated the medical electronics market with the largest revenue share of approximately 38.9% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of digital healthcare and remote patient monitoring technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 9.4% from 2026 to 2033. Growth is driven by expanding healthcare infrastructure, rising healthcare investments, increasing adoption of wearable medical devices, and growing government initiatives supporting healthcare digitalization across countries such as China, India, and Japan.

- The Sensors segment held the largest market revenue share of approximately 32.6% in 2025 driven by widespread usage in patient monitoring systems, diagnostic devices, and wearable medical electronics. Sensors are critical for real-time data acquisition including heart rate, blood pressure, oxygen saturation, and glucose levels, making them essential across both hospital and home healthcare environments.

- The MCUs/MPUs segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing integration of AI-enabled processing capabilities in medical devices, imaging systems, and portable diagnostic equipment. Rising adoption of smart and connected healthcare devices requiring real-time computation is further accelerating segment expansion.

- The Diagnostic and Imaging Devices segment held the largest market revenue share of approximately 38.1% in 2025 driven by strong demand for advanced imaging systems such as MRI, CT scanners, and ultrasound equipment across hospitals and diagnostic centers.

- The Patient Monitoring Devices segment accounted for approximately 29.7% share in 2025, supported by increasing ICU admissions, rising chronic disease prevalence, and growing adoption of remote patient monitoring systems. The Medical Implantable Devices segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by advancements in neurostimulators, cardiac implants, and biosensors. The Ventilators and RGM Equipment segment held a moderate share supported by critical care applications and emergency healthcare infrastructure expansion.

- The Diagnostic Imaging segment held the largest market revenue share of approximately 36.5% in 2025 driven by increasing demand for early disease detection and AI-enhanced imaging systems in radiology.

- The Patient Monitoring segment accounted for approximately 33.4% share in 2025 supported by growing adoption of continuous monitoring systems in ICUs and home healthcare. The Medical Implants segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033 driven by advancements in bioelectronic implants and miniaturized medical electronics. The Endoscopy segment held a smaller but steady share driven by increasing minimally invasive surgical procedures.

- The Non-Invasive segment held the largest market revenue share of approximately 58.9% in 2025 driven by rising demand for wearable devices, external monitoring systems, and diagnostic imaging technologies that eliminate the need for surgical intervention.

- The Invasive segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing adoption of implantable medical electronics such as pacemakers, neurostimulators, and biosensors used for long-term patient care and chronic disease management.

- The Class II segment held the largest market revenue share of approximately 46.7% in 2025 driven by widespread use of moderate-risk electronic medical devices such as infusion pumps, diagnostic equipment, and patient monitoring systems.

- The Class III segment is projected to register the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by increasing adoption of high-risk implantable and life-supporting electronic devices including cardiac implants and advanced neurotechnology systems. The Class I segment held a smaller share due to its use in basic, low-risk medical instruments.

- The Hospitals segment held the largest market revenue share of approximately 54.3% in 2025 driven by high patient inflow, advanced diagnostic infrastructure, and widespread deployment of medical electronic systems across critical care and surgical departments.

- The Ambulatory Surgical Centers segment accounted for approximately 27.8% share in 2025 supported by increasing preference for outpatient surgeries and minimally invasive procedures. The Clinics segment is projected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033 driven by rising adoption of portable diagnostic devices and growing expansion of decentralized healthcare services in urban and semi-urban regions.

Market Size & Forecast

- Global Market Value (2025): USD 8.91 Billion

- Expected Market Value (2033): USD 16.49 Billion

- Forecast CAGR (2026–2033): 8.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Medical Electronics Market Segmentation

|

Attributes |

Medical Electronics Key Market Insights |

|

Segments Covered |

· By Component: Sensors, Mcus/Mpus, Displays, Memory Devices, and Batteries · By End User Products: Diagnostic and Imaging Devices, Patient Monitoring Devices, Medical Implantable Devices and Ventilators and RGM Equipment · By Application: Patient Monitoring, Diagnostic Imaging, Medical Implants, and Endoscopy · By Medical Procedure: Invasive and Non-Invasive · By Medical Device Classification: Class I, Class II, and Class III · By End User: Hospital, Ambulatory Surgical Centers, and Clinics |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Analog Devices, Inc. (U.S.) |

|

Market Opportunities |

• Expansion Of Wearable Medical Devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Medical Electronics Market Trends

Trend: Growth In Miniaturized Medical Electronics And AI Enabled Diagnostic Systems

Increasing demand for compact, high-precision, and connected medical electronic devices is driving innovation across diagnostics, monitoring, and therapeutic applications. Traditional standalone medical equipment is being replaced by integrated digital systems that offer real-time data acquisition, improved accuracy, and seamless connectivity with hospital information systems and cloud platforms.

In modern healthcare systems, manufacturers are integrating advanced medical electronics, For instance in wearable ECG monitors, continuous glucose monitoring systems, and smart infusion pumps, to enable real-time patient tracking and improve clinical decision-making. In hospital environments, AI-enabled diagnostic imaging systems are being used to enhance detection accuracy in radiology and pathology, reducing diagnostic time and improving treatment outcomes.

The rapid expansion of telemedicine and home healthcare is also increasing demand for portable and wireless medical electronics capable of remote patient monitoring and data transmission. In addition, critical care units and emergency healthcare systems are adopting advanced monitoring devices, such as multi-parameter patient monitors used in ICUs, which continuously track vital signs with high accuracy. Growing clinical validation through pilot deployments in 2025 integrating AI-based diagnostic support systems in hospitals across the U.S. and Europe has shown diagnostic accuracy improvements of approximately 15–20% in early disease detection applications

Medical Electronics Market Dynamics

Key Market Driver: Rising Demand For Chronic Disease Monitoring And Digital Healthcare Transformation

The increasing global burden of chronic diseases such as cardiovascular disorders, diabetes, and respiratory conditions is significantly driving demand for advanced medical electronics. Healthcare providers are increasingly adopting continuous monitoring systems and connected diagnostic devices to enable early detection, personalized treatment, and improved patient outcomes.

Hospitals and healthcare networks are deploying advanced patient monitoring systems and smart diagnostic equipment to reduce hospital readmissions and improve ICU efficiency. For instance, large hospital networks in the U.S. and Germany have implemented integrated monitoring systems across critical care units, improving patient response times by nearly 12–18% through real-time alerts and predictive analytics.

In addition, the expansion of digital healthcare ecosystems, telehealth platforms, and remote patient monitoring solutions is accelerating adoption of wearable and portable medical electronics. Government-backed healthcare digitalization programs in countries such as India and China are further supporting large-scale deployment of connected medical devices in both urban and rural healthcare systems

Key Restraint/Challenge: High Device Costs And Strict Regulatory Approval Requirements

The development and commercialization of advanced medical electronic devices involve high research and manufacturing costs due to complex sensor integration, precision engineering, and software validation requirements. These high costs limit affordability and adoption, particularly in low and middle-income healthcare systems.

In addition, stringent regulatory approval processes imposed by agencies such as the U.S. FDA and the European Medicines Agency increase time-to-market and compliance costs for manufacturers. Device certification, clinical validation, and safety testing requirements often extend product development cycles significantly.

Industry data from medical device manufacturers indicates that regulatory approval timelines for advanced diagnostic electronics can range from 12 to 36 months, depending on device complexity, increasing commercialization costs and delaying market entry for innovative solutions

Key Market Opportunity: Expansion Of Wearable Devices And AI Powered Healthcare Systems

The growing adoption of wearable medical electronics and AI-driven healthcare systems is creating significant opportunities for market expansion across preventive care, diagnostics, and chronic disease management. Increasing consumer preference for real-time health tracking is driving demand for smart wearable devices capable of continuous physiological monitoring.

Healthcare companies are increasingly investing in wearable technologies, For instance smartwatches with ECG and blood oxygen monitoring features, remote cardiac monitoring patches, and AI-enabled diagnostic assistants, to improve early disease detection and patient engagement. In hospitals, AI-powered imaging and decision-support systems are being deployed to assist clinicians in complex diagnostic procedures and reduce human error.

In addition, advancements in semiconductor miniaturization and low-power electronics are enabling next-generation implantable devices and ultra-portable diagnostic systems. Large-scale pilot programs in 2025 across Asia-Pacific hospitals integrating AI-based monitoring platforms reported up to 18–22% improvement in early intervention rates for high-risk patients, demonstrating strong potential for future market growth.

Medical Electronics Market Scope

The market is segmented on the basis of component, end user products, application, medical procedure, medical device classification, and end user.

- By Component

On the basis of component, the medical electronics market is segmented into Sensors, MCUs/MPUs, Displays, Memory Devices, and Batteries. The Sensors segment held the largest market revenue share of approximately 32.6% in 2025 driven by widespread usage in patient monitoring systems, diagnostic devices, and wearable medical electronics. Sensors are critical for real-time data acquisition including heart rate, blood pressure, oxygen saturation, and glucose levels, making them essential across both hospital and home healthcare environments.

The MCUs/MPUs segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing integration of AI-enabled processing capabilities in medical devices, imaging systems, and portable diagnostic equipment. Rising adoption of smart and connected healthcare devices requiring real-time computation is further accelerating segment expansion.

- By End User Products

On the basis of end user products, the market is segmented into Diagnostic and Imaging Devices, Patient Monitoring Devices, Medical Implantable Devices, and Ventilators and RGM Equipment. The Diagnostic and Imaging Devices segment held the largest market revenue share of approximately 38.1% in 2025 driven by strong demand for advanced imaging systems such as MRI, CT scanners, and ultrasound equipment across hospitals and diagnostic centers.

The Patient Monitoring Devices segment accounted for approximately 29.7% share in 2025, supported by increasing ICU admissions, rising chronic disease prevalence, and growing adoption of remote patient monitoring systems. The Medical Implantable Devices segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by advancements in neurostimulators, cardiac implants, and biosensors. The Ventilators and RGM Equipment segment held a moderate share supported by critical care applications and emergency healthcare infrastructure expansion.

- By Application

On the basis of application, the market is segmented into Patient Monitoring, Diagnostic Imaging, Medical Implants, and Endoscopy. The Diagnostic Imaging segment held the largest market revenue share of approximately 36.5% in 2025 driven by increasing demand for early disease detection and AI-enhanced imaging systems in radiology.

The Patient Monitoring segment accounted for approximately 33.4% share in 2025 supported by growing adoption of continuous monitoring systems in ICUs and home healthcare. The Medical Implants segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033 driven by advancements in bioelectronic implants and miniaturized medical electronics. The Endoscopy segment held a smaller but steady share driven by increasing minimally invasive surgical procedures.

- By Medical Procedure

On the basis of medical procedure, the market is segmented into Invasive and Non-Invasive. The Non-Invasive segment held the largest market revenue share of approximately 58.9% in 2025 driven by rising demand for wearable devices, external monitoring systems, and diagnostic imaging technologies that eliminate the need for surgical intervention.

The Invasive segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing adoption of implantable medical electronics such as pacemakers, neurostimulators, and biosensors used for long-term patient care and chronic disease management.

- By Medical Device Classification

On the basis of medical device classification, the market is segmented into Class I, Class II, and Class III. The Class II segment held the largest market revenue share of approximately 46.7% in 2025 driven by widespread use of moderate-risk electronic medical devices such as infusion pumps, diagnostic equipment, and patient monitoring systems.

The Class III segment is projected to register the fastest growth at a CAGR of 10.8% from 2026 to 2033, driven by increasing adoption of high-risk implantable and life-supporting electronic devices including cardiac implants and advanced neurotechnology systems. The Class I segment held a smaller share due to its use in basic, low-risk medical instruments.

- By End User

On the basis of end user, the market is segmented into Hospitals, Ambulatory Surgical Centers, and Clinics. The Hospitals segment held the largest market revenue share of approximately 54.3% in 2025 driven by high patient inflow, advanced diagnostic infrastructure, and widespread deployment of medical electronic systems across critical care and surgical departments.

The Ambulatory Surgical Centers segment accounted for approximately 27.8% share in 2025 supported by increasing preference for outpatient surgeries and minimally invasive procedures. The Clinics segment is projected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033 driven by rising adoption of portable diagnostic devices and growing expansion of decentralized healthcare services in urban and semi-urban regions.

Medical Electronics Market Regional Analysis

North America Medical Electronics Market Insight

North America dominated the medical electronics market with the largest revenue share of approximately 38.9% in 2025, supported by strong healthcare infrastructure, high adoption of advanced diagnostic technologies, and increasing integration of AI-enabled medical devices across hospitals and clinics. The region benefits from high healthcare expenditure, rapid digitalization of healthcare systems, and strong penetration of wearable and connected medical devices. Rising demand for real-time patient monitoring and precision diagnostics is further strengthening the adoption of advanced medical electronics across critical care and home healthcare settings.

U.S. Medical Electronics Market Insight

The U.S. medical electronics market captured the largest revenue share in North America in 2025, driven by advanced hospital infrastructure, rapid adoption of AI-powered diagnostic imaging systems, and widespread use of remote patient monitoring solutions. The country has a strong presence of leading medical device manufacturers and technology providers, enabling continuous innovation in wearable sensors, implantable devices, and smart monitoring systems. Increasing prevalence of chronic diseases such as cardiovascular disorders and diabetes is further accelerating demand for continuous monitoring and connected healthcare solutions.

Europe Medical Electronics Market Insight

The Europe medical electronics market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by rising healthcare modernization programs, stringent regulatory standards for patient safety, and increasing adoption of digital health technologies. European healthcare systems are rapidly integrating advanced monitoring devices, AI-based diagnostic platforms, and smart imaging systems to improve clinical efficiency and reduce healthcare costs. Growth is also supported by rising investments in telemedicine and home healthcare infrastructure across major economies.

U.K. Medical Electronics Market Insight

The U.K. medical electronics market is expected to witness steady growth from 2026 to 2033, driven by increasing adoption of digital healthcare solutions, expanding telemedicine services, and rising demand for advanced patient monitoring systems. The National Health Service is actively investing in healthcare digitalization initiatives, supporting integration of connected medical devices across hospitals and primary care centers. Growing focus on early diagnosis and preventive healthcare is further encouraging adoption of wearable and portable medical electronics across the country.

Germany Medical Electronics Market Insight

The Germany medical electronics market is expected to witness strong growth from 2026 to 2033, supported by advanced healthcare infrastructure, strong medical device manufacturing capabilities, and increasing focus on precision medicine and digital health solutions. Germany’s emphasis on innovation and high-quality medical standards is driving adoption of advanced diagnostic imaging systems and AI-assisted clinical devices. Rising demand for hospital automation and smart patient monitoring systems is further strengthening market expansion across healthcare facilities.

Asia-Pacific Medical Electronics Market Insight

The Asia-Pacific medical electronics market is expected to witness the fastest growth rate from 2026 to 2033, supported by rising healthcare expenditure, rapid urbanization, and expanding access to advanced medical technologies in countries such as China, India, and Japan. The region is experiencing strong growth in hospital infrastructure development and increasing adoption of wearable and portable medical devices. Government initiatives promoting healthcare digitization and telemedicine are further accelerating demand for connected medical electronics across both urban and rural healthcare systems.

Japan Medical Electronics Market Insight

The Japan medical electronics market is expected to witness steady growth from 2026 to 2033 due to the country’s advanced healthcare system, strong technological innovation, and aging population driving demand for continuous monitoring and assisted healthcare solutions. Japan is widely adopting robotic-assisted medical devices, AI-based diagnostic imaging systems, and wearable health monitoring technologies. Increasing focus on elderly care and home healthcare services is further boosting demand for compact and user-friendly medical electronic devices.

China Medical Electronics Market Insight

The China medical electronics market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid healthcare infrastructure expansion, strong domestic manufacturing capabilities, and growing adoption of advanced medical technologies. China is one of the fastest-growing markets for smart medical devices, including patient monitoring systems, diagnostic imaging equipment, and wearable health trackers. Government support for healthcare digitalization and smart hospital initiatives is further driving large-scale deployment of advanced medical electronics across the country.

Medical Electronics Market Share

The Medical Electronics industry is primarily led by well-established companies, including:

- Analog Devices, Inc. (U.S.)

• Texas Instruments Incorporated (U.S.)

• Medtronic (Ireland)

• STMicroelectronics (Switzerland)

• Mouser Electronics, Inc. (U.S.)

• Cypress Semiconductor Corporation (U.S.)

• Semiconductor Components Industries, LLC (U.S.)

• Digi-Key Electronics (U.S.)

• Tekscan, Inc. (U.S.)

• First Sensor AG (Germany)

• TE Connectivity (Switzerland)

• Renesas Electronics Corporation (Japan)

• GENERAL ELECTRIC COMPANY (U.S.)

• Siemens (Germany)

• NXP Semiconductors (Netherlands)

• SAMSUNG (South Korea)

• Toshiba Corporation (Japan)

• Boston Scientific Corporation (U.S.)

Latest Developments in Medical Electronics Market

- In February 2026, Olympus announced the publication of the EAGLE Trial validating its cloud-based CADDIE polyp detection platform integrated within the OLYSENSE ecosystem. The FDA-cleared and CE-marked AI-assisted detection solution is designed to improve colorectal screening accuracy, support early cancer detection, and enhance clinical workflow efficiency, strengthening the adoption of AI-enabled diagnostic systems in the medical electronics market.

- In January 2026, ZEISS Medical Technology launched Collaborative Care, a browser-based application enabling real-time exchange of patient data and referrals among eye-care professionals. The platform is expected to improve clinical coordination, accelerate diagnosis and treatment planning, and enhance digital healthcare connectivity, supporting the growing demand for integrated healthcare IT and medical electronics solutions.

- In January 2026, Polymatech Electronics received CDSCO registration approval to begin domestic manufacturing of vein-finder devices under India’s Medical Devices Rules. The development is expected to strengthen local medical electronics production capabilities, reduce import dependency, and improve accessibility to advanced vascular imaging devices across hospitals and diagnostic centers in India.

- In July 2024, Fujifilm Holdings Corporation launched the APERTO Lucent 0.4T open MRI system featuring permanent magnet technology and enhanced workflow capabilities. The system is designed to improve patient comfort, optimize imaging efficiency, and reduce operational complexity for healthcare facilities, supporting broader adoption of advanced diagnostic imaging technologies in emerging and developed healthcare markets.

- In May 2024, Canon installed the first Aquilion Serve SP CT scanner in the U.S. integrated with INSTINX workflow automation technology. The advanced imaging system is intended to improve scan consistency, enhance diagnostic accuracy, and streamline radiology operations through automated workflow management, contributing to increased efficiency in medical imaging infrastructure across healthcare institutions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Medical Electronics Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Medical Electronics Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Medical Electronics Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.