Global Medical Image Management Market

Market Size in USD Billion

USD

5.97 Billion

USD

8.96 Billion

2024

2032

USD

5.97 Billion

USD

8.96 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.97 Billion | |

| USD 8.96 Billion | |

| % | |

|

Medical Image Management Market Size

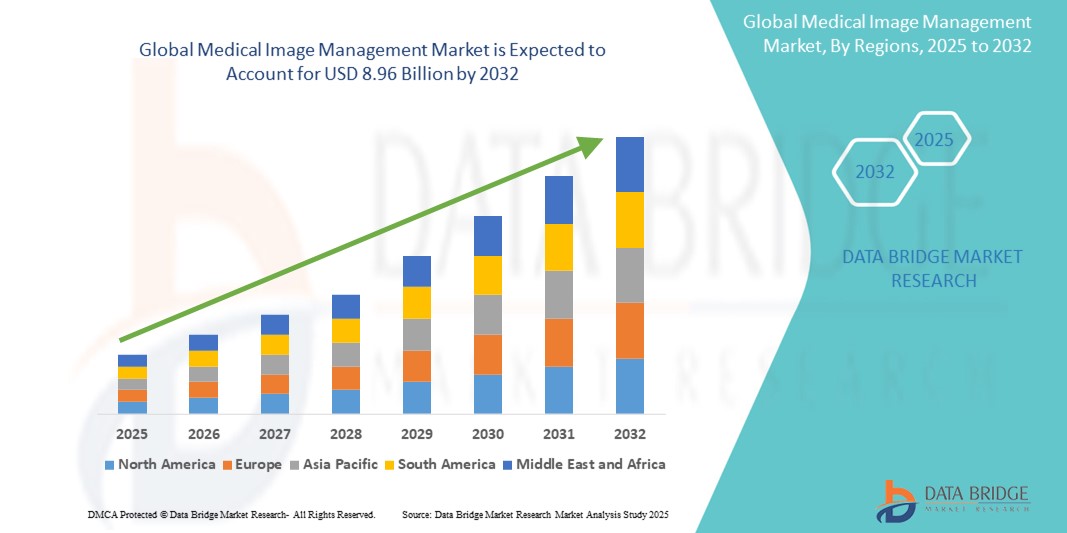

- The global medical image management market size was valued at USD 5.97 billion in 2024 and is expected to reach USD 8.96 billion by 2032, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by the growing demand for efficient and integrated solutions to handle the increasing volumes of complex imaging data, coupled with technological advancements in diagnostic imaging modalities and image management software, including the integration of AI and cloud-based platforms

- Furthermore, rising consumer demand for early disease detection, the increasing prevalence of chronic diseases, and government initiatives promoting the adoption of electronic medical records are establishing medical image management systems as crucial tools for modern healthcare delivery, thereby significantly boosting the industry's growth

Medical Image Management Market Analysis

- Medical image management systems, encompassing solutions such as picture archiving & communication systems (PACS) and vendor neutral archives (VNA), are increasingly vital in modern healthcare due to the growing volume and complexity of imaging data, the need for efficient storage and retrieval, and seamless integration with electronic health records

- The escalating demand for medical image management solutions is primarily fueled by rapid technological advancements in diagnostic imaging modalities, the rising prevalence of chronic diseases necessitating frequent imaging, and increasing investments in digital health infrastructure and IT in healthcare

- North America dominates the medical image management market with the largest revenue share of 41.5% in 2024, characterized by the region's sophisticated healthcare systems, early and widespread adoption of advanced imaging technologies, and significant government initiatives promoting digitalization and EHR implementation

- Asia-Pacific is expected to be the fastest growing region in the medical image management market during the forecast period due to increasing healthcare expenditure, a rapidly expanding patient pool, rising awareness about early disease detection, and ongoing improvements in healthcare infrastructure across emerging economies

- Picture Archiving & Communication System (PACS) segment dominates the medical image management market with a market share of 50.5% in 2024, driven by its widespread use and critical function in managing and storing medical images, particularly within radiology departments where the majority of imaging studies are handled

Report Scope and Medical Image Management Market Segmentation

|

Attributes |

Medical Image Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Image Management Market Trends

“Enhanced Diagnostics and Workflow Optimization Through AI and Deep Learning”

- A significant and accelerating trend in the global medical image management market is the deepening integration of Artificial Intelligence (AI) and its subset, deep learning, across various stages of the imaging workflow. This fusion of technologies is fundamentally transforming diagnostic capabilities, improving workflow efficiency, and enhancing patient care

- For instance, AI algorithms are now being used to analyze vast datasets of medical images (X-rays, CTs, MRIs, ultrasounds) with remarkable speed and precision, aiding in the early detection of subtle abnormalities, such as cancerous lesions, that might be missed by the human eye. Companies such as Qure.ai and Niramai are developing AI-based diagnostic tools for specific conditions, while major players such as GE HealthCare and Siemens Healthineers are embedding AI into their imaging systems and management platforms

- AI integration in medical image management enables features such as automated image segmentation and reconstruction, improved image quality through noise reduction, and intelligent triage systems that prioritize critical cases for radiologists, significantly reducing their workload. Natural Language Processing (NLP) is also being utilized to extract relevant information from unstructured clinical notes and radiology reports, further streamlining data management and decision support

- The seamless integration of AI-powered tools with Picture archiving and communication systems (PACS) and vendor neutral archives (VNA) facilitates a more centralized and intelligent approach to managing complex imaging data. This creates a unified and automated environment for image acquisition, analysis, storage, and reporting, leading to faster turnaround times and more consistent diagnoses

- This trend towards more intelligent, intuitive, and interconnected medical imaging systems is fundamentally reshaping expectations for diagnostic accuracy and efficiency in healthcare. Consequently, companies are focusing on developing AI-enabled solutions that offer enhanced diagnostic support, automated tasks, and predictive analytics capabilities

- The demand for medical image management solutions that offer seamless AI and deep learning integration is growing rapidly across hospitals, diagnostic centers, and research institutions, as healthcare providers increasingly prioritize improved patient outcomes, reduced costs, and optimized operational workflows

Medical Image Management Market Dynamics

Driver

“Increasing Volume of Medical Images and Rising Prevalence of Chronic Diseases”

- The escalating volume of medical images generated from advanced diagnostic modalities, coupled with the rising global prevalence of chronic diseases, is a significant driver for the heightened demand for medical image management solutions

- For instance, the continuous innovation in imaging technologies such as MRI, CT scans, and PET scans, alongside the growing use of 3D and 4D imaging, results in massive datasets that require sophisticated systems for efficient storage, retrieval, and analysis. This surge in data necessitates robust image management systems to ensure data integrity and accessibility

- As the global population ages, there's a corresponding increase in the incidence of chronic conditions such as cancer, cardiovascular diseases, and neurological disorders, all of which heavily rely on diagnostic imaging for early detection, diagnosis, and ongoing monitoring. This demographic shift directly translates to a greater demand for imaging procedures and, consequently, for comprehensive medical image management solutions

- Furthermore, government initiatives promoting the adoption of electronic medical records (EMRs) and the digitalization of healthcare data worldwide are making medical image management systems an indispensable part of modern healthcare infrastructure. These systems facilitate seamless integration with EMRs, improving patient care coordination and streamlining clinical workflows

- The critical need for accurate and timely diagnoses, coupled with the desire for efficient workflows and improved patient outcomes, are key factors propelling the adoption of medical image management solutions in hospitals, diagnostic centers, and other healthcare facilities. The growing awareness among healthcare providers about the benefits of centralized and accessible imaging data further contributes to market growth

Restraint/Challenge

“Data Security & Privacy Concerns and High Implementation & Interoperability Costs”

- Concerns surrounding the cybersecurity vulnerabilities of healthcare IT systems, including medical image management solutions, pose a significant challenge to broader market penetration. As these systems rely on network connectivity and software to manage sensitive patient data, they are susceptible to hacking attempts and data breaches, raising anxieties among healthcare providers and patients about the security and privacy of their information

- For instance, high-profile reports of ransomware attacks and data breaches targeting healthcare organizations have made some providers hesitant to invest in or fully integrate advanced digital image management solutions. The potential for disruption to patient care and the severe financial and legal repercussions associated with such incidents further amplify these concerns

- ·Addressing these cybersecurity concerns through robust encryption, secure authentication protocols, regular software updates, and adherence to stringent regulatory frameworks is crucial for building trust among healthcare institutions. Companies in the medical image management space, such such as Sectra and Philips, emphasize their advanced security features and compliance certifications in their offerings to reassure potential buyers. In addition, the relatively high initial cost of some comprehensive medical image management systems, compared to maintaining older, disparate systems, can be a barrier to adoption for budget-sensitive healthcare providers, particularly in developing regions or for smaller clinics

- While prices are gradually decreasing due to technological advancements and competitive pressure, the perceived premium for advanced medical image management technology can still hinder widespread adoption, especially for those who do not immediately see the compelling return on investment or the necessity for the full suite of advanced features offered

- Overcoming these challenges through enhanced cybersecurity measures, clear demonstrations of ROI, comprehensive training on data security best practices, and the development of more scalable and affordable medical image management options will be vital for sustained market growth

Medical Image Management Market Scope

The market is segmented on the basis of product, delivery model, specialty, end user, and distribution channel

- By Product

On the basis of product, the medical image management market is segmented into Picture Archiving & Communication system (PACS), vendor neutral archives (VNA), application-independent clinical archive (AICA), and enterprise viewers/universal viewers. The picture archiving & communication system (PACS) segment dominates the largest market revenue share of 50.5% in 2024, driven by its long-standing adoption and critical role in storing, retrieving, and distributing medical images, especially within radiology departments. PACS remains foundational for efficient image workflow and diagnostic reporting in healthcare facilities globally.

The vendor neutral archives (VNA) segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing need for centralized, vendor-agnostic storage solutions that address interoperability challenges and reduce data silos. VNAs offer healthcare organizations greater flexibility, easier data migration, and a unified view of patient imaging data across multiple specialties and departments, contributing to enhanced data governance and long-term cost savings

- By Delivery Mode

On the basis of delivery model, the medical image management market is segmented into hybrid, web/cloud based, and on premises. The on-premises segment held the largest market revenue share in 2024, driven by the traditional preference of large hospitals and healthcare systems for maintaining direct control over their data security and infrastructure. On-premise solutions offer maximum customization and data sovereignty, appealing to organizations with stringent security policies and significant IT resources.

The web/cloud based segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its benefits of scalability, lower upfront costs, remote accessibility, and reduced IT maintenance burden. Cloud-based solutions facilitate teleradiology, enable easier data sharing across geographically dispersed facilities, and support the growing trend of remote work for healthcare professionals, making them increasingly attractive to a wide range of providers.

- By Specialty

On the basis of specialty, the medical image management market is segmented into surgery, oncology, dental, and others. The oncology segment held a significant market share in 2024, largely due to the high incidence and increasing prevalence of cancer worldwide, which necessitates extensive diagnostic imaging for screening, diagnosis, staging, and treatment monitoring. The complex nature of cancer care often requires multi-modal imaging and long-term image archiving, driving the demand for specialized management solutions

The orthopedics segment is anticipated to witness substantial growth. This is due to the high demand for imaging in diagnosing musculoskeletal conditions, such fractures, arthritis, and joint replacements, often requiring detailed image analysis and longitudinal tracking for treatment and recovery.

- By End User

On the basis of end user, the medical image management market is segmented into hospitals, radiology chains/centers, ambulatory surgery center, and others. The hospitals segment dominates the largest market revenue share in 2024, accounting for 58% of the revenue. This dominance stems from their comprehensive range of imaging modalities, large patient volumes, and the critical need for integrated systems to manage vast amounts of medical data generated from diverse departments. Hospitals serve as primary centers for a wide array of diagnostic imaging procedures.

The radiology chains/centers segment is expected to witness significant growth during the forecast period, driven by their specialization in diagnostic imaging services, increasing patient referrals from private practitioners, and their focus on efficiency and cost-effectiveness through optimized image management workflows. These centers often leverage advanced image management systems to handle high throughput and deliver rapid diagnostic reports.

- By Distribution Channel

On the basis of distribution channel, the medical image management market is segmented into direct tenders, third-party administrators, and others. The direct tenders segment held a prominent market share in 2024, as large hospitals and integrated delivery networks often prefer direct procurement from major vendors through tenders to ensure comprehensive solutions, long-term support, and customized integration with their existing IT infrastructure

The third-party administrators segment is expected to witness the fastest growth rate from 2025 to 2032. This growth is fueled by the increasing demand for managed services, outsourcing of IT operations, and the desire for specialized expertise in data management and cybersecurity without the burden of in-house infrastructure. Third-party administrators offer scalable and cost-effective solutions, appealing particularly to smaller and mid-sized healthcare facilities

Medical Image Management Market Regional Analysis

- North America dominates the medical image management market with the largest revenue share of 41.5% in 2024, driven by the region's sophisticated healthcare systems, early and widespread adoption of advanced imaging technologies, and significant government initiatives promoting digitalization and EHR implementation

- Consumers and healthcare providers in the region highly value integrated solutions for managing complex imaging data efficiently and securely

- This widespread adoption is further supported by favorable reimbursement policies, a strong focus on improving patient outcomes, and the presence of numerous key industry players, establishing advanced medical image management systems as a crucial component of healthcare delivery in the region

U.S. Medical Image Management Market Insight

The U.S. medical image management market accounted the largest revenue share of 76.6% in 2024 of the North America, driven by the rapid adoption of digital health records and advanced imaging technologies. Healthcare facilities are increasingly prioritizing the integration of Picture archiving and communication systems (PACS) and vendor neutral archives (VNA) to manage the growing volume and complexity of medical images. The robust demand for AI-powered analytics and cloud-based platforms, along with significant government and private investments in healthcare IT, further propels the market.

Europe Medical Image Management Market Insight

The Europe medical image management market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare expenditure, a rising geriatric population, and growing awareness regarding early disease detection. Stringent regulatory frameworks for data privacy and security also push for the adoption of sophisticated image management solutions. The region is experiencing significant growth in the integration of AI into imaging workflows and the transition towards more interoperable systems, aiming to enhance diagnostic efficiency across hospitals and clinics.

U.K. Medical Image Management Market Insight

The U.K. medical image management market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the National Health Service's (NHS) ongoing digitalization initiatives and a strong emphasis on improving patient care pathways. The escalating demand for efficient image sharing, coupled with significant investments in AI for radiology and the adoption of Electronic Health Records (EHRs), is encouraging healthcare providers to implement advanced image management solutions. The UK's focus on technological advancements and streamlined healthcare processes is expected to continue stimulating market growth.

Germany Medical Image Management Market Insight

The Germany medical image management market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digital health solutions, robust healthcare infrastructure, and a strong emphasis on technological innovation. Germany's well-developed healthcare system, combined with its focus on high-quality patient care and advanced diagnostic capabilities, promotes the adoption of sophisticated image management systems. The integration of AI and cloud computing within medical imaging workflows is also becoming increasingly prevalent, aligning with local preferences for secure and efficient healthcare IT.

Asia-Pacific Medical Image Management Market Insight

The Asia-Pacific medical image management market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, rapid expansion of healthcare infrastructure, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards digital healthcare, supported by government initiatives promoting digitalization and accessible healthcare, is driving the adoption of medical image management solutions. Furthermore, the rising prevalence of chronic diseases and a large patient pool further accelerate market expansion across APAC.

Japan Medical Image Management Market Insight

The Japan medical image management market is gaining momentum due to the country’s high-tech culture, rapid aging population, and increasing demand for advanced diagnostic capabilities. The Japanese market places a significant emphasis on precision in medical diagnosis, and the adoption of medical image management is driven by the increasing need for efficient handling of complex imaging data. The integration of AI into medical imaging and the government's push for digital health transformation are fueling growth, as healthcare providers seek to enhance diagnostic accuracy and workflow efficiency.

India Medical Image Management Market Insight

The India medical image management market accounted for a significant market revenue share in Asia-Pacific in 2024, attributed to the country's expanding healthcare sector, rapid digitalization, and a rising patient burden from chronic diseases. India's increasing investments in healthcare infrastructure and the growing adoption of electronic health records are making advanced image management solutions increasingly popular in both public and private hospitals. The government's push towards digital health initiatives and the availability of cost-effective solutions from domestic and international players are key factors propelling the market in India.

Medical Image Management Market Share

The medical image management industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- FUJIFILM Holdings Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Agfa-Gevaert Group (Belgium)

- Carestream Health (U.S.)

- Sectra AB (Sweden)

- Konica Minolta, Inc. (Japan)

- Merative (U.S.)

- INFINITT Healthcare Co., Ltd. (South Korea)

- Change Healthcare (U.S.)

- Mach7 Technologies (Australia)

- Intelerad (Canada)

- Ambra Health (U.S.)

- TeraRecon (U.S.)

- Visage Imaging, Inc. (U.S.)

- Novarad (U.S.)

- RamSoft, Inc. (Canada)

- Dell Inc. (U.S.)

Latest Developments in Global Medical Image Management Market

- In November 2024, GE HealthCare and RadNet announced a strategic collaboration aimed at transforming imaging systems and accelerating the adoption of Artificial Intelligence (AI) in medical imaging, particularly focusing on enhancing breast cancer screening

- In January 2024, Royal Philips showcased its comprehensive suite of AI-driven enterprise imaging portfolio, including next-generation Ultrasound, MRI, and CT systems, at the 76th Annual Conference of the Indian Radiological and Imaging Association (IRIA) 2024

- In January 2024, FUJIFILM Diosynth Biotechnologies and SHL Medical announced a strategic partnership aimed at addressing the increasing market demand for auto-injector medicines. This collaboration, integrated into SHL’s Alliance Management Program, seeks to optimize processes and enhance efficiency for pharmaceutical and biotech firms offering finished self-injection device services, primarily leveraging SHL’s leading auto-injector platform, Molly

- In January 2024, Royal Philips, a global leader in health technology, showcased its robust portfolio of AI-driven enterprise imaging solutions at the 76th Annual Conference of the Indian Radiological and Imaging Association (IRIA) 2024. During this event in Vijayawada, Philips highlighted its next-generation Ultrasound, MRI, and CT systems, and also introduced its new state-of-the-art Compact Ultrasound System 5000 series, emphasizing performance and portability derived from its premium ultrasound capabilities. This demonstrates Philips' commitment to advancing diagnostic imaging through integrated AI

- In June 2024, Apollo released enhanced multidisciplinary medical image management capabilities of its arcc platform at SIIM24

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.