Global Medical Membranes Market

Market Size in USD Billion

USD

3.94 Billion

USD

7.98 Billion

2024

2032

USD

3.94 Billion

USD

7.98 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.94 Billion | |

| USD 7.98 Billion | |

| % | |

|

Medical Membranes Market Size

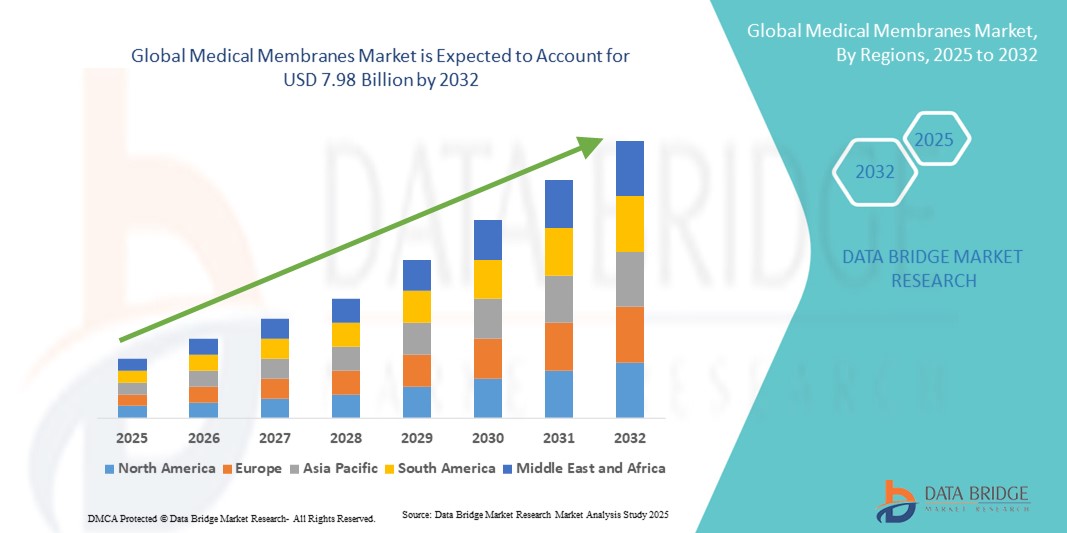

- The global medical membranes market size was valued at USD 3.94 billion in 2024 and is expected to reach USD 7.98 billion by 2032, at a CAGR of 9.20% during the forecast period

- The market growth is largely fueled by the increasing demand for advanced medical devices and biotechnology applications, leading to the adoption of high-performance medical membranes in healthcare and research sectors

- Furthermore, rising requirements for efficient filtration, separation, and purification in hospitals, laboratories, and pharmaceutical manufacturing are driving the uptake of medical membranes solutions, thereby significantly boosting the industry's growth

Medical Membranes Market Analysis

- Medical membranes, widely used in applications such as hemodialysis, drug delivery, tissue engineering, and diagnostic devices, are increasingly becoming a vital component of modern healthcare due to their ability to provide selective permeability, biocompatibility, and high filtration efficiency. Their role in supporting critical therapeutic and diagnostic processes makes them indispensable in both hospital and laboratory settings

- The escalating demand for medical membranes is primarily fueled by the rising prevalence of chronic diseases such as kidney disorders and diabetes, increasing adoption of advanced medical devices, and growing investments in biotechnology and pharmaceutical research. In addition, ongoing innovations in membrane materials, such as the development of high-performance polymeric and ceramic membranes, are enhancing durability, efficiency, and patient safety, thereby accelerating their adoption across the global healthcare sector

- North America dominated the medical membranes market with the largest revenue share of 39.5% in 2024, supported by high healthcare expenditure, advanced hospital infrastructure, and a strong presence of leading membrane technology providers. The U.S. experienced substantial growth in installations, particularly in hospitals, diagnostic centers, and specialty laboratories, driven by innovations in high-performance filtration membranes, biocompatible materials, and integration with advanced medical equipment. Strong focus on efficiency, regulatory compliance, and enhanced patient safety further reinforce the region’s leadership

- Asia-Pacific is expected to be the fastest-growing region in the medical membranes market during the forecast period, driven by rapid urbanization, rising healthcare investments, and growing demand for high-quality filtration solutions in countries such as China, India, and Japan. Expansion of hospital networks, government initiatives to improve healthcare infrastructure, and increasing adoption of advanced membrane technologies are accelerating market growth across the region

- The hemodialysis segment dominated the medical membranes market with a market share of 45.6% in 2024. The growing prevalence of chronic kidney disease and end-stage renal failure has significantly boosted demand for advanced dialysis membranes

Report Scope and Medical Membranes Market Segmentation

|

Attributes |

Medical Membranes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Membranes Market Trends

Enhanced Performance Through Material Innovation

- A significant and accelerating trend in the global medical membranes market is the growing focus on material innovation, where advanced polymeric and ceramic membranes are being developed to improve performance, durability, and biocompatibility. This innovation is significantly enhancing the efficiency of medical membranes in applications such as hemodialysis, drug delivery, and tissue engineering

- For instance, next-generation polymeric membranes are being engineered to provide greater permeability and selectivity, enabling faster and more precise separation of toxins and biomolecules during dialysis. Similarly, ceramic-based membranes are gaining traction for their chemical stability, longer lifespan, and ability to withstand rigorous sterilization processes, making them highly suitable for critical medical applications

- Continuous R&D efforts are also leading to the development of membranes with improved antifouling properties, reducing the risk of contamination and extending operational life. This is particularly beneficial in laboratory diagnostics and therapeutic devices, where reliability and accuracy are paramount

- Medical membranes are further being tailored for specialized applications, such as controlled drug release systems, bioartificial organs, and regenerative medicine, creating new opportunities across the healthcare landscape. The incorporation of nanotechnology in membrane design is allowing for superior precision at the molecular level, further boosting their utility in advanced biomedical research and clinical care

- This trend towards high-performance, specialized, and durable medical membranes is fundamentally reshaping expectations for healthcare solutions. Consequently, major companies are investing heavily in R&D to bring innovative membranes to the market, focusing on both enhanced patient outcomes and compliance with stringent global healthcare regulations

- The demand for advanced membranes that provide higher accuracy, safety, and reliability is growing rapidly across both hospitals and research institutions, as healthcare providers increasingly prioritize efficient diagnostic and therapeutic solutions supported by robust membrane technologies

Medical Membranes Market Dynamics

Driver

Growing Need Due to Rising Demand for Advanced Healthcare Solutions

- The increasing burden of chronic diseases such as kidney disorders, liver failure, and cardiovascular conditions, coupled with the expanding adoption of advanced medical technologies, is a significant driver for the heightened demand for medical membranes

- For instance, in March 2024, Merck KGaA announced an advancement in its membrane technology portfolio with a new line of high-performance membranes designed for biopharmaceutical filtration and medical device applications. Such strategic developments by key industry players are expected to accelerate the growth of the Medical Membranes market during the forecast period

- As healthcare providers worldwide seek reliable solutions for hemodialysis, drug delivery, and bio-separation, medical membranes offer superior efficiency, high selectivity, and biocompatibility, making them a compelling choice over conventional filtration methods

- Furthermore, the growing focus on personalized medicine and regenerative therapies is creating opportunities for the integration of specialized membranes in tissue engineering and controlled drug release systems, thereby widening their clinical applications

- The rising investments in healthcare infrastructure, particularly in emerging economies, and the expansion of hospital and diagnostic networks are also contributing to the increased adoption of medical membranes. Their role in ensuring accuracy, safety, and efficiency in medical treatments positions them as an indispensable component of modern healthcare systems

Restraint/Challenge

Concerns Regarding High Costs and Stringent Regulatory Frameworks

- Despite their growing importance, the relatively high production and operational costs of advanced medical membranes pose a significant challenge to broader adoption. Membranes designed with advanced polymeric or ceramic materials, while offering superior durability and precision, often come at a premium compared to conventional alternatives, which can restrict accessibility in cost-sensitive markets

- For instance, healthcare providers in developing regions may hesitate to invest in advanced medical membrane systems due to budgetary constraints, opting instead for lower-cost but less efficient solutions

- In addition to cost barriers, the market faces challenges linked to stringent regulatory approvals. Medical membranes used in dialysis, drug delivery, and implantable devices must comply with rigorous quality and safety standards imposed by agencies such as the FDA and EMA, leading to longer product development timelines and higher compliance costs

- Manufacturers are required to invest heavily in R&D, clinical validation, and quality control, which can delay commercialization and limit the entry of smaller players

- While technological advancements and scale of production are gradually helping to reduce costs, overcoming these barriers will require innovation in cost-effective membrane design, streamlined regulatory pathways, and collaborations with healthcare institutions to promote affordability. Ensuring accessibility without compromising performance will be vital for sustained global adoption of medical membranes

Medical Membranes Market Scope

The market is segmented on the basis of chemical, technology, application, end user and distribution chanel.

- By Chemical

On the basis of chemical, the Medical Membranes market is segmented into modified acrylics, polyethylene, polytetrafluoroethylene (PTFE), Polyvinylidene Fluoride (PVDF), and Polysulfone. The Polyvinylidene Fluoride (PVDF) segment dominated the market with the largest revenue share of 38.5% in 2024. PVDF membranes are widely used in medical and pharmaceutical applications due to their outstanding thermal stability, excellent resistance to chemicals, and high mechanical strength. They play a crucial role in sterile filtration, intravenous infusion filters, and drug delivery, where precision and safety are critical. Moreover, their compatibility with various sterilization techniques, such as autoclaving and gamma radiation, makes them reliable for repeated use. Increasing adoption in high-purity filtration processes has reinforced their position as the leading chemical type in the market.

The Polysulfone segment is projected to grow at the fastest CAGR of 20.3% from 2025 to 2032. Polysulfone membranes are gaining popularity due to their superior biocompatibility, durability, and excellent permeability to water and solutes. They are increasingly utilized in hemodialysis, where the need for membranes that can withstand frequent use without compromising performance is paramount. The rising global burden of chronic kidney disease and end-stage renal disease has directly fueled demand for polysulfone-based dialysis membranes. Additionally, ongoing advancements in drug delivery and protein separation are expanding the use of polysulfone, positioning it as the fastest-growing chemical category.

- By Technology

On the basis of technology, the medical membranes market is segmented into reverse osmosis, microfiltration, ultrafiltration, and nanofiltration. The ultrafiltration segment dominated the market with a revenue share of 41.7% in 2024. Ultrafiltration membranes are preferred because of their ability to retain bacteria, viruses, and high-molecular-weight particles while allowing smaller molecules and water to pass through. They are extensively used in pharmaceutical filtration, protein purification, and sterile filtration in hospitals and laboratories. The high throughput, coupled with their reliability in ensuring product purity and patient safety, makes ultrafiltration indispensable in medical applications. Growing demand for precise separation in intravenous infusion and biopharmaceutical production has further cemented their leadership in the market.

The Nanofiltration segment is expected to register the fastest CAGR of 19.8% from 2025 to 2032. Nanofiltration membranes are increasingly being adopted in applications requiring selective removal of small solutes, such as drug delivery and water purification in healthcare facilities. Their ability to filter at a molecular level, while maintaining high energy efficiency, gives them a unique advantage over traditional filtration technologies. With increasing focus on sterile environments, stringent regulatory guidelines, and rising biopharmaceutical manufacturing, nanofiltration is emerging as the technology of choice for applications demanding ultra-precise separation. The rapid pace of innovation in advanced nanomaterials is also expected to accelerate adoption in the coming years.

- By Application

On the basis of application, the medical membranes market is segmented into hemodialysis, drug delivery, pharmaceutical filtration, intravenous infusion filters and sterile filtration, water filtration in the medical industry, protein purification and cell separation, and blood micro filters. The hemodialysis segment accounted for the largest market share of 45.6% in 2024. The growing prevalence of chronic kidney disease and end-stage renal failure has significantly boosted demand for advanced dialysis membranes. Hemodialysis membranes, especially those made of biocompatible polymers such as polysulfone and PVDF, provide high permeability, selective clearance of toxins, and reduced side effects for patients. The expansion of dialysis centers worldwide and government initiatives supporting affordable treatment options have further supported market dominance. Rising patient preference for high-quality dialysis services continues to make this segment the backbone of the medical membranes market.

The pharmaceutical filtration segment is forecasted to grow at the fastest CAGR of 21.1% from 2025 to 2032. Pharmaceutical companies rely heavily on membranes for critical processes such as sterile filtration, drug formulation, and protein purification. Increasing demand for biologics, vaccines, and advanced therapeutics has placed filtration as a cornerstone of drug production. Stricter global regulatory requirements on drug purity and safety have accelerated the adoption of advanced membranes. Furthermore, the rise in R&D investments across biopharma and expansion of manufacturing facilities in emerging markets are creating lucrative opportunities for this segment, solidifying its role as the fastest-growing application area.

- By End Users

On the basis of end users, the medical membranes market is segmented into hospitals, ambulatory centers, clinics, community healthcare, and others. The hospitals segment dominated the market with the largest revenue share of 52.8% in 2024. Hospitals are the primary users of medical membranes due to their extensive use in hemodialysis, intravenous infusion, blood purification, and sterile filtration. Large-scale procurement of high-performance membranes through government and institutional tenders ensures consistent supply and standardization of patient care. Hospitals also have the infrastructure to support advanced dialysis technologies, making them the most reliable setting for patients requiring frequent treatment. The rising global demand for quality hospital-based care continues to sustain this dominance.

The ambulatory centers segment is anticipated to grow at the fastest CAGR of 18.6% from 2025 to 2032. With healthcare moving toward decentralized and outpatient care, ambulatory centers are increasingly adopting medical membranes for dialysis, infusion, and filtration services. These centers offer cost-effective and accessible alternatives to hospital-based treatments, especially for chronic disease management. The trend toward home-based care and short-duration outpatient procedures is also boosting demand in this segment. The combination of affordability, convenience, and advanced medical technologies positions ambulatory centers as the fastest-expanding end-user category.

- By Distribution Channel

On the basis of distribution channel, the medical membranes market is segmented into retail and direct tenders. The direct tenders segment held the largest market revenue share of 64.3% in 2024. Direct tenders remain the preferred procurement route for hospitals, large clinics, and government healthcare organizations. They enable bulk purchasing, which reduces costs while ensuring supply chain efficiency and quality assurance. Manufacturers also prefer this channel as it establishes long-term contracts and provides predictable demand for membranes. The dominance of this channel is further supported by government policies favoring centralized procurement for essential medical products.

The retail segment is forecasted to record the fastest CAGR of 17.9% from 2025 to 2032. Retail channels are gaining traction as smaller healthcare providers, ambulatory centers, and home healthcare users increasingly purchase medical membranes through distributors and e-commerce platforms. The growing preference for flexible and on-demand procurement, coupled with improved online availability, is driving the popularity of this channel. Retail distribution also caters to niche requirements and smaller-volume purchases, making it a vital growth driver in decentralized healthcare ecosystems.

Medical Membranes Market Regional Analysis

- North America dominated the medical membranes market with the largest revenue share of 39.5% in 2024, supported by high healthcare expenditure, advanced hospital infrastructure, and the presence of leading membrane manufacturers

- The region benefits from stringent quality standards, frequent audits, and well-established healthcare networks that emphasize the need for reliable and high-performance medical membranes

- Continuous innovations in membrane materials and filtration technologies further reinforce the region’s leadership in this market

U.S. Medical Membranes Market Insight

The U.S. medical membranes market captured the largest revenue share of 69% in 2024 within North America, fueled by the rising demand for high-performance membranes across hospitals, specialty clinics, and pharmaceutical manufacturing facilities. Increased adoption of advanced filtration systems, coupled with growing investments in healthcare infrastructure and research, is propelling the market. Key applications include hemodialysis, tissue engineering, and biopharmaceutical processing, which require membranes with precise permeability, durability, and biocompatibility. Ongoing technological innovations in polymeric, ceramic, and composite membranes are further enhancing efficiency and performance, contributing to substantial market growth.

Europe Medical Membranes Market Insight

The Europe medical membranes market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory requirements, growing investments in healthcare, and the rising need for high-quality medical filtration solutions. Hospitals, diagnostic centers, and biopharmaceutical facilities are increasingly integrating advanced membranes for dialysis, drug delivery, and separation processes. Rising awareness of patient safety, coupled with a focus on sustainable and energy-efficient membrane technologies, is further fostering growth. The region is witnessing significant expansion in both clinical and industrial applications, supported by ongoing R&D activities and collaborations between local manufacturers and healthcare providers.

U.K. Medical Membranes Market Insight

The U.K. medical membranes market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investments in healthcare infrastructure and the adoption of advanced medical and biopharmaceutical technologies. Hospitals and research institutions are prioritizing high-performance membranes for critical applications, such as dialysis, controlled drug release, and bioprocessing. Stringent regulatory oversight, rising patient volumes, and the push for efficient and sustainable medical filtration systems are expected to continue stimulating market growth. Furthermore, the strong presence of membrane manufacturers and distributors in the U.K. supports widespread adoption and innovation in medical membrane technologies.

Germany Medical Membranes Market Insight

The Germany medical membranes market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing demand for technologically advanced, eco-conscious solutions in healthcare and pharmaceutical industries. Germany’s emphasis on research, innovation, and sustainability is promoting the adoption of high-performance membranes in hospitals, diagnostic labs, and biopharmaceutical facilities. The integration of membranes in critical medical applications, such as hemodialysis, sterile filtration, and regenerative medicine, is becoming increasingly prevalent. Additionally, strong regulatory frameworks, advanced manufacturing infrastructure, and high standards of patient safety further reinforce the country’s leading market position.

Asia-Pacific Medical Membranes Market Insight

The Asia-Pacific medical membranes market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rapid urbanization, rising healthcare investments, and growing demand for advanced medical and biopharmaceutical technologies in countries such as China, Japan, and India. The expansion of hospital networks, establishment of new dialysis centers, and rising production of biopharmaceuticals are accelerating market growth. Increasing government initiatives to enhance healthcare infrastructure, coupled with the availability of cost-effective membranes, are expanding adoption across the region. Furthermore, the emergence of APAC as a manufacturing hub for medical membrane components ensures wide accessibility and affordability.

Japan Medical Membranes Market Insight

The Japan medical membranes market is gaining momentum due to the country’s high-tech healthcare ecosystem, rapid urbanization, and increasing demand for efficient medical and biopharmaceutical filtration solutions. The market emphasizes membranes for dialysis, drug delivery systems, and sterile filtration applications. Growing investments in hospital infrastructure, aging population requiring specialized medical care, and focus on precision medicine are driving demand. Additionally, ongoing innovations in membrane materials, coupled with integration in research hospitals and biotech facilities, support sustained market growth.

China Medical Membranes Market Insight

The China medical membranes market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid expansion of hospital networks, increasing investments in healthcare infrastructure, and rising demand for advanced medical and biopharmaceutical applications. China’s growing middle class, rising awareness of healthcare quality, and focus on cost-effective solutions are fueling adoption. The push towards modern hospitals, advanced dialysis centers, and bio-manufacturing facilities, alongside strong domestic membrane manufacturers, are key factors propelling market growth. Continuous innovation in membrane technology, including polymeric and ceramic variants, further supports China’s position as a rapidly expanding market within the region.

Medical Membranes Market Share

The medical membranes industry is primarily led by well-established companies, including:

- 3M (U.S.)

- NIPRO (Japan)

- Merck KGaA (Germany)

- Koch Membrane Systems, Inc. (U.S.)

- Sartorius AG (Germany)

- Abbott (U.S.)

- Aethlon Medical, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Pall Corporation (U.S.)

- Medtronic (Ireland)

- Kimberly-Clark (U.S.)

- W. L. Gore & Associates, Inc. (U.S.)

- Cantel Medical (U.S.)

- B. Braun SE (Germany)

- BD (U.S.)

- Baxter (U.S.)

- Asahi Kasei Corporation (Japan)

- Amniox Medical, Inc. (U.S.)

Latest Developments in Global Medical Membranes Market

- In June 2021, 3M Health Care launched the 3M Harvest RC clarifier, leveraging its proprietary fibrous chromatography media to deliver a single-stage purification solution for recombinant protein therapeutic manufacturing. This innovation aims to streamline upstream processes, enhancing efficiency and scalability in biopharmaceutical production

- In May 2022, Merck KGaA announced an investment exceeding EUR 440 million to expand its membrane and filtration manufacturing capabilities in Ireland. This strategic move is designed to meet the growing demand for high-quality filtration solutions in the biopharmaceutical industry, reinforcing Merck's commitment to supporting global healthcare advancements

- In April 2022, Nipro Corporation introduced the Elisio HX, a novel super high flux sharp cut-off membrane made with polyethersulfone. This membrane offers a larger pore size and specific geometry, allowing higher performance compared to standard high-flux membranes, particularly in hemodialysis applications

- In December 2021, Merck KGaA was awarded a EUR 121 million contract by the U.S. Department of Defense to construct a lateral flow membrane production facility in Sheboygan, Wisconsin. This facility aims to produce diagnostic-grade membranes, enhancing supply security and reducing lead times for global customers, thereby strengthening Merck's position in the medical membranes market

- In July 2023, Sartorius announced significant growth in its Life Science division, attributed to increased demand for its membrane filtration products. This growth underscores the rising importance of membrane technologies in various applications, including biopharmaceutical manufacturing and laboratory research

- In March 2024, Merck KGaA forecasted a return to modest operating earnings growth, adjusted for currency impacts, due to a gradual increase in demand for specialty materials used in biotech drugs and semiconductors. The Life Science division is expected to see increased orders from drugmakers in the first half of 2024, highlighting the ongoing need for advanced filtration solutions

- In May 2024, Sartorius continued its profitable growth path, with significant increases in sales revenue and profitability in the first half of the fiscal year. This performance reflects the strong demand for its membrane filtration products, particularly in the biopharmaceutical sector

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.