Global Medical X Ray 2d Radiography Equipment Market

Market Size in USD Billion

USD

5.34 Billion

USD

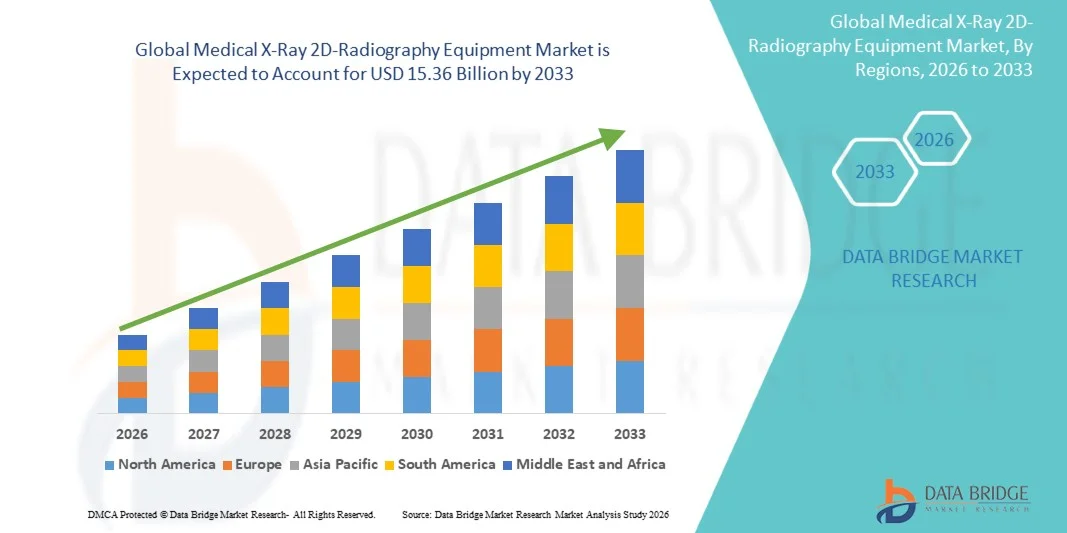

15.36 Billion

2025

2033

USD

5.34 Billion

USD

15.36 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.34 Billion | |

| USD 15.36 Billion | |

| % | |

|

Medical X-Ray 2D-Radiography Equipment Market Size

- The global medical X-Ray 2D-radiography equipment market size was valued at USD 5.34 billion in 2025 and is expected to reach USD 15.36 billion by 2033, at a CAGR of 14.12% during the forecast period

- The market growth is largely driven by the increasing adoption of advanced imaging technologies and ongoing technological advancements in diagnostic equipment, leading to enhanced digitalization across hospitals, clinics, and diagnostic centers

- Furthermore, rising demand from healthcare providers for accurate, efficient, and user-friendly diagnostic solutions is positioning Medical X-Ray 2D-Radiography Equipment as a critical tool in modern medical imaging. These converging factors are accelerating the uptake of these solutions, thereby significantly boosting the growth of the medical imaging equipment industry

Medical X-Ray 2D-Radiography Equipment Market Analysis

- Medical X‑Ray 2D‑Radiography Equipment, comprising essential diagnostic X‑ray systems used across clinical settings, remains a cornerstone of medical imaging due to its proven effectiveness, reliability, and increasingly digital and dose‑efficient capabilities that support faster and clearer diagnostics

- The escalating demand for advanced radiography solutions is primarily driven by rising healthcare expenditure, growing prevalence of chronic diseases, and the continuous shift from analog to digital imaging systems that offer superior image quality and workflow efficiency.

- North America dominated the medical X‑Ray 2D‑radiography equipment market in 2025, capturing an estimated 40% share of global revenue, supported by well‑established healthcare infrastructure, strong adoption of digital X‑ray systems, and substantial investments in diagnostic imaging upgrades across hospitals and clinics

- Asia‑Pacific is expected to be the fastest‑growing region in the medical X‑Ray 2D‑radiography Equipment market during the forecast period, fueled by expanding healthcare infrastructure, rising disposable incomes, increasing disease burden, and government initiatives to expand access to modern diagnostic technologies across China, India, Japan, and Southeast Asia

- The digital segment dominated the market with the largest revenue share of 61.5% in 2025, driven by rapid technological advancements and the growing demand for higher image quality

Report Scope and Medical X-Ray 2D-Radiography Equipment Market Segmentation

|

Attributes |

Medical X-Ray 2D-Radiography Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Medical X-Ray 2D-Radiography Equipment Market Trends

“Advancements in Imaging Technology and Digital Workflow Integration”

- A notable trend in the global medical X-Ray 2D-radiography equipment market is the ongoing technological advancement in imaging systems, including the transition from analog to digital X-ray systems

- Digital radiography (DR) equipment is increasingly preferred due to its higher image resolution, faster processing times, and reduced radiation exposure to patients

- Integration of advanced imaging software, such as automated image enhancement, computer-aided detection (CAD), and digital archiving solutions, is enhancing diagnostic accuracy and workflow efficiency in hospitals and diagnostic centers

- For instance, in June 2023, Carestream Health launched its DRX Plus System with enhanced image processing software, enabling radiologists to quickly detect fractures and subtle pathologies with higher precision

- Portable and compact X-ray systems are gaining traction, particularly in emergency care, outpatient clinics, and rural healthcare settings, as they allow imaging at the patient’s location without the need for a dedicated radiology room

- Furthermore, innovations such as flat-panel detectors, dose-reduction technologies, and improved detector sensitivity are shaping the market by providing more precise imaging with enhanced safety for both patients and operators

- The trend toward connected healthcare ecosystems, where X-ray systems can be integrated with hospital information systems (HIS) and picture archiving and communication systems (PACS), is enabling faster reporting, remote consultations, and improved patient care

Medical X-Ray 2D-Radiography Equipment Market Dynamics

Driver

“Rising Demand for Early Disease Detection and Increasing Healthcare Expenditure

- The rising prevalence of chronic diseases, traumatic injuries, and lifestyle-related illnesses is driving the need for timely and accurate diagnostic imaging, which directly fuels the adoption of Medical X-Ray 2D-Radiography Equipment

- Increasing healthcare expenditure across both developed and developing regions is facilitating investments in advanced diagnostic imaging infrastructure, allowing hospitals and clinics to upgrade from conventional X-ray systems to digital solutions. For example, in March 2024, Siemens Healthineers launched the Luminos DR System in India, targeting both urban hospitals and rural diagnostic centers to improve early detection of musculoskeletal disorders

- Growing awareness among healthcare professionals and patients regarding the benefits of early diagnosis and preventive care is encouraging wider adoption of X-ray imaging systems

- In addition, the expansion of healthcare facilities in emerging economies, driven by government initiatives to improve healthcare access, is creating a significant demand for cost-effective and reliable radiography equipment

Restraint/Challenge

“High Equipment Costs and Regulatory Compliance Challenges”

- The relatively high cost of advanced digital X-ray systems, including flat-panel detectors and DR consoles, poses a barrier to adoption, particularly for smaller clinics or healthcare facilities in developing countries. While analog systems are less expensive, they offer limited functionality and lower efficiency

- Compliance with stringent regulatory standards regarding radiation safety, equipment certification, and clinical protocols adds complexity and increases the overall cost of implementation for healthcare providers

- For instance, in July 2023, GE Healthcare faced delays in the rollout of its Definium DR systems in Europe due to additional CE certification requirements, highlighting the regulatory challenges in major markets

- Regular maintenance, calibration, and the need for trained personnel to operate sophisticated X-ray systems are additional operational challenges that may slow market adoption

- Furthermore, concerns over equipment downtime, technical failures, and the need for continuous software updates can hinder seamless integration into hospital workflows, especially in regions with limited technical support infrastructure

- Overcoming these challenges through cost optimization, enhanced training programs, and streamlined regulatory pathways will be critical for sustained growth in the Medical X-Ray 2D-Radiography Equipment market

Medical X-Ray 2D-Radiography Equipment Market Scope

The market is segmented on the basis of type, product type, technology, portability, application, and end users.

• By Type

On the basis of type, the Medical X-Ray 2D-Radiography Equipment market is segmented into digital and analog. The digital segment dominated the market with the largest revenue share of 61.5% in 2025, driven by rapid technological advancements and the growing demand for higher image quality. Hospitals and diagnostic centers increasingly prefer digital solutions due to their superior workflow efficiency and faster image processing compared to analog systems. Digital systems also reduce radiation exposure for patients, which is becoming a critical requirement in modern healthcare. The compatibility with PACS (Picture Archiving and Communication Systems) allows seamless integration with hospital IT infrastructure, further strengthening adoption. Rising adoption of AI-enabled digital radiography for automated detection and reporting also contributes to dominance. Moreover, government initiatives and healthcare policies supporting digitalization are boosting demand. The convenience of storage, retrieval, and remote sharing of images enhances clinical efficiency. Digital systems support multi-department usage, from orthopedics to chest imaging, increasing their utility. Their growing integration with telemedicine platforms allows remote consultations. Maintenance is simpler compared to analog systems, improving cost efficiency in the long term. As a result, the digital segment continues to dominate across developed and emerging markets.

The analog segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2033, driven primarily by its affordability and continued use in regions with limited healthcare budgets. Analog systems remain popular in small clinics, rural hospitals, and emerging markets where infrastructure or investment in IT is limited. Continuous improvements in film quality, processing speed, and image contrast enhance analog utility. Analog radiography is particularly useful for basic screening purposes where high-end imaging is not mandatory. Growing awareness about cost-effective healthcare solutions supports analog adoption. Hospitals upgrading gradually from analog to digital often rely on hybrid systems, maintaining analog relevance. Additionally, training and familiarity with analog systems among technicians drive continued usage. Analog systems have low maintenance costs, making them attractive for low-resource settings. Their robustness and reliability under challenging conditions also appeal to small diagnostic centers. Market expansion in emerging economies, along with increasing healthcare facility establishments, fuels growth. Rising adoption for educational and training purposes in medical institutions further contributes. The analog segment’s growth is gradual but steady, ensuring a significant presence globally.

• By Product Type

On the basis of product type, the market is segmented into stationary digital radiology systems and portable digital radiology systems. The stationary digital radiology systems segment held the largest revenue share of 55.8% in 2025, driven by its ability to handle high patient volumes and deliver superior image resolution for multiple diagnostic applications. Hospitals and large diagnostic centers prefer stationary systems for their integration with hospital IT networks and PACS. These systems offer advanced features such as automatic exposure control, multi-angle imaging, and large detector panels for chest, orthopedics, and cardiovascular studies. The reliability and long operational lifespan of stationary systems make them a preferred long-term investment. High throughput and multi-modality compatibility allow simultaneous imaging across departments. Their adoption is further fueled by increasing hospital infrastructure investments and rising demand for routine diagnostic screenings. Workflow efficiency, improved image quality, and the ability to support AI-assisted diagnostics enhance their utility. They also enable centralized maintenance and monitoring, reducing operational challenges. Integration with telemedicine services allows remote consultation and review. The aesthetic and ergonomic design of stationary systems improves patient comfort. Large hospitals see significant cost-benefit in high-volume operations, reinforcing dominance.

The portable digital radiology systems segment is expected to witness the fastest CAGR of 16.7% from 2026 to 2033, driven by rising demand for bedside imaging, emergency care, and mobile healthcare services. Portable systems allow imaging at the patient’s location, reducing the need for transportation and improving care efficiency, especially in ICUs and emergency departments. They are particularly useful in disaster relief, mobile hospitals, and rural healthcare settings. Technological advancements in lightweight materials, battery efficiency, and wireless connectivity have made portable systems highly practical and reliable. Growing adoption in veterinary hospitals, military, and sports medicine also supports market growth. Remote healthcare services increasingly rely on portable X-ray systems for home-based diagnostics. Cost-effectiveness compared to large stationary systems encourages smaller hospitals and clinics to adopt portable devices. Multi-functionality, ease of use, and quick setup enhance operational efficiency. Portable systems now offer high-resolution imaging comparable to stationary systems. Integration with mobile apps and cloud storage allows instant sharing of images with specialists. Increasing healthcare awareness and government initiatives for mobile diagnostics further boost adoption. Rising geriatric and chronic disease populations drive demand for point-of-care imaging. The segment’s growth is expected to remain strong across developed and emerging regions.

• By Technology

On the basis of technology, the market is segmented into film-based radiography, computed radiography (CR), and direct radiography (DR). The direct radiography (DR) segment dominated with a revenue share of 49.3% in 2025, driven by its instant image acquisition, high-resolution output, and reduced radiation exposure. DR systems are widely adopted in modern hospitals and advanced diagnostic centers. Their efficiency enables rapid patient throughput, especially in high-volume departments such as orthopedics, chest, and cardiovascular imaging. Integration with hospital IT networks and PACS ensures seamless workflow. DR systems are increasingly used for AI-assisted diagnostics and remote image analysis. They support multi-specialty applications, enhancing versatility. DR adoption is bolstered by increasing government funding for healthcare digitization and modernization of imaging infrastructure. Reduced operating and maintenance costs compared to CR and film-based systems further strengthen market position. Hospitals prefer DR for advanced features such as dynamic imaging, 3D reconstructions, and dose optimization. Their reliability and compatibility with telemedicine platforms improve clinical reach. Continuous technological innovation, including wireless detectors and cloud connectivity, enhances DR utility. DR’s dominance reflects the global trend toward digitalization and AI integration in medical imaging.

The computed radiography (CR) segment is expected to witness the fastest CAGR of 13.9% from 2026 to 2033, as it provides a flexible transition from analog to digital systems. CR technology is widely adopted in emerging markets and smaller clinics upgrading from film-based systems. It offers moderate cost, easy integration with PACS, and improved image quality over analog. CR systems are particularly useful for hospitals balancing cost and technological advancement. Increasing demand in routine diagnostics and outpatient care drives growth. Technological enhancements in scanning speed, resolution, and software compatibility further support adoption. CR serves as a cost-effective solution for multi-departmental use, including chest, dental, and orthopedics. Training and ease of use contribute to popularity among technicians. Its compatibility with existing analog infrastructure enables gradual modernization. Healthcare facilities in rural and semi-urban areas prefer CR for affordability and reliability. Growing awareness of digital workflows and cloud-enabled diagnostics is increasing adoption. Rising hospital and diagnostic center expansion in emerging economies further fuels market growth.

• By Portability

On the basis of portability, the Medical X-Ray 2D-Radiography Equipment market is segmented into fixed and portable systems. The fixed segment accounted for the largest market revenue share of 58.6% in 2025, driven by the preference of large hospitals and multi-specialty diagnostic centers for high-throughput imaging. Fixed systems are preferred for their superior image quality, stability, and ability to support complex examinations such as chest, cardiovascular, and orthopedic imaging. These systems integrate seamlessly with hospital IT networks, PACS, and electronic health records, enabling efficient workflow management and long-term monitoring. The reliability and robustness of fixed X-ray systems ensure consistent performance and reduced downtime. Advanced features, including automated exposure control, multi-angle imaging, and large detector arrays, further enhance clinical efficiency. Hospitals rely on fixed systems for departments requiring continuous patient imaging and high patient volumes. They also offer better ergonomic designs, supporting patient comfort and technician convenience. Large-scale installation allows centralized maintenance and training programs, reducing operational costs. Government initiatives promoting hospital infrastructure modernization contribute to the dominance of fixed systems. Hospitals increasingly prefer fixed systems for AI-based diagnostics and telemedicine support. Their long lifespan and multi-modality support ensure continued high adoption. Overall, fixed systems remain the backbone of hospital-based radiography worldwide.

The portable segment is expected to witness the fastest CAGR of 17.2% from 2026 to 2033, fueled by rising demand for bedside imaging, emergency care, and mobile diagnostic services. Portable systems allow imaging at the patient’s location, minimizing patient movement and improving care efficiency, especially in ICUs, emergency rooms, and field hospitals. Lightweight designs, improved battery life, and wireless connectivity have significantly enhanced portability and ease of use. Portable systems are widely adopted in rural and semi-urban healthcare facilities where fixed installations are not feasible. Mobile imaging services, disaster response, and home healthcare contribute to growth. These systems support rapid deployment, immediate diagnostics, and remote consultations through cloud-based image transfer. Veterinary, sports medicine, and military applications also drive demand. Portable systems offer high-resolution imaging comparable to stationary setups, making them versatile. Hospitals and diagnostic centers benefit from reduced operational cost and space requirements. Increasing awareness of point-of-care imaging solutions encourages adoption. Continuous technological advancements, such as AI-assisted analysis, expand their utility. Government and NGO initiatives promoting healthcare accessibility in remote regions further support growth. Portable systems’ flexibility ensures they capture a growing share in emerging markets.

• By Application

On the basis of application, the Medical X-Ray 2D-Radiography Equipment market is segmented into dental, veterinary, mammography, chest, cardiovascular, orthopaedics, and others. The chest segment dominated with a revenue share of 35.4% in 2025, driven by the high prevalence of respiratory diseases, tuberculosis screening programs, and routine hospital chest imaging. Chest X-rays are one of the most commonly performed diagnostic procedures, spanning hospitals, diagnostic centers, and outpatient facilities. Government initiatives and awareness programs for early detection of lung diseases boost adoption. Hospitals require high-quality imaging for accurate diagnosis of pneumonia, chronic obstructive pulmonary disease (COPD), and other respiratory conditions. Integration with digital systems allows instant reporting, remote consultation, and automated archiving. Chest imaging is widely used for pre-operative assessments and routine health checkups. High throughput of chest X-rays contributes to dominance in high-volume centers. Advanced DR and CR systems offer enhanced image clarity, dose reduction, and AI-assisted detection. Multi-specialty hospitals rely on chest imaging for comprehensive diagnostic coverage. The segment’s dominance is also supported by continuous upgrades in hospital infrastructure and preventive care programs. Overall, chest radiography remains a primary driver of 2D X-ray market demand globally.

The orthopaedics segment is expected to witness the fastest CAGR of 15.8% from 2026 to 2033, driven by rising musculoskeletal disorders, sports injuries, and an aging population. Orthopedic imaging requires high-resolution systems for fracture detection, joint replacement planning, and post-operative monitoring. Hospitals and specialty orthopedic centers increasingly adopt portable and DR systems for accurate diagnosis and patient convenience. The growth of orthopedic surgeries, trauma care facilities, and rehabilitation programs contributes to increased demand. Portable imaging systems allow bedside diagnostics for immobile patients. Rising prevalence of osteoporosis, arthritis, and sports injuries globally boosts orthopedics imaging adoption. Technological advancements in digital detectors, AI-based fracture detection, and 3D reconstruction enhance diagnostic efficiency. Integration with hospital IT and PACS ensures rapid reporting and improved clinical workflow. Orthopedic applications benefit from multi-modality imaging capabilities. Expansion of orthopedic clinics and specialty centers in emerging markets drives growth. Insurance coverage and healthcare awareness programs further encourage adoption. Orthopedic imaging’s versatility across age groups ensures sustained demand.

• By End Users

On the basis of end users, the Medical X-Ray 2D-Radiography Equipment market is segmented into hospitals, diagnostic centres, and others. The hospitals segment dominated with a revenue share of 62.7% in 2025, driven by multi-specialty departments, high patient volume, and demand for advanced diagnostic services. Hospitals invest heavily in DR, CR, and digital radiography systems to improve workflow, patient throughput, and image management. The integration of hospital IT systems, PACS, and electronic health records enables seamless reporting and centralized monitoring. Large hospitals prefer fixed systems for continuous high-volume imaging, while portable systems support emergency care and ICU diagnostics. Government funding for hospital infrastructure expansion and modernization contributes to dominance. Hospitals also utilize X-ray systems across multiple applications, including chest, orthopedics, cardiovascular, and dental imaging. AI-assisted diagnostics, telemedicine integration, and cloud connectivity further enhance hospital adoption. Hospitals value long-term reliability, advanced features, and high throughput offered by modern X-ray systems. Multi-departmental usage ensures maximum utility and return on investment. Hospitals’ purchasing power and technological capabilities reinforce dominance. Continuous training and support programs improve system utilization and adoption. Overall, hospitals remain the largest end-user segment in the global 2D radiography market.

The diagnostic centres segment is expected to witness the fastest CAGR of 14.9% from 2026 to 2033, driven by the rapid expansion of standalone imaging facilities, outpatient centers, and specialty clinics. Diagnostic centers benefit from compact, high-efficiency X-ray systems that allow multiple examinations with minimal operational costs. Increasing outsourcing of imaging services by hospitals and healthcare providers further boosts adoption. Portable systems are particularly valuable for diagnostic centers with limited space. Rising outpatient diagnostics and preventive healthcare checkups drive consistent demand. Integration with cloud-based image storage, telemedicine platforms, and mobile apps enhances operational efficiency. Diagnostic centers prioritize cost-effective, versatile, and easy-to-maintain systems. Technological advancements in DR and CR systems improve imaging speed, quality, and workflow. Government initiatives and private investments in diagnostic infrastructure expand the market. Growth in medical tourism and health screening programs contributes to adoption. Diagnostic centers serve multiple specialties, increasing utilization of multi-functional X-ray equipment. Overall, diagnostic centers are emerging as a rapidly growing segment worldwide.

Medical X-Ray 2D-Radiography Equipment Market Regional Analysis

- North America dominated the medical X‑Ray 2D‑radiography equipment market in 2025, capturing an estimated 40% share of global revenue

- The market growth is driven by a well‑established healthcare infrastructure, strong adoption of digital X‑ray systems

- Substantial investments in diagnostic imaging upgrades across hospitals and clinics

U.S. Medical X‑Ray 2D‑Radiography Equipment Market Insight

The U.S. medical X‑Ray 2D‑radiography equipment market captured the largest revenue share in North America in 2025, fueled by the modernization of hospital and clinic imaging facilities, the adoption of advanced 2D radiography systems, and increasing demand for high-quality diagnostic solutions. Government initiatives supporting the upgrade of diagnostic equipment and private sector investments are further contributing to market expansion.

Europe Medical X‑Ray 2D‑Radiography Equipment Market Insight

The Europe medical X‑Ray 2D‑radiography equipment market is expected to grow steadily during the forecast period, supported by increasing healthcare expenditure, stringent regulatory standards, and the replacement of outdated radiography systems with advanced digital equipment. The region is witnessing strong adoption in hospitals, private clinics, and diagnostic centers.

U.K. Medical X‑Ray 2D‑Radiography Equipment Market Insight

The U.K. medical X‑Ray 2D‑radiography equipment market is anticipated to grow at a noteworthy CAGR, driven by the adoption of modern imaging systems and government programs aimed at improving diagnostic capabilities. Rising demand for early disease detection and preventive care is encouraging hospitals and clinics to upgrade their X‑ray equipment.

Germany Medical X‑Ray 2D‑Radiography Equipment Market Insight

Germany’s medical X‑Ray 2D‑radiography equipment market is expected to expand steadily, supported by advanced healthcare infrastructure, growing awareness of digital diagnostic solutions, and initiatives to modernize medical imaging facilities. The integration of efficient, eco-conscious X‑ray systems in hospitals and diagnostic centers is further fueling growth.

Asia‑Pacific Medical X‑Ray 2D‑Radiography Equipment Market Insight

Asia‑Pacific medical X‑Ray 2D‑radiography equipment market is expected to be the fastest-growing region in the Medical X‑Ray 2D‑Radiography Equipment market during the forecast period, driven by expanding healthcare infrastructure, rising disposable incomes, and increasing prevalence of chronic and lifestyle-related diseases. Government initiatives to enhance access to modern diagnostic technologies across China, India, Japan, and Southeast Asia are also contributing to rapid adoption.

China Medical X‑Ray 2D‑Radiography Equipment Market Insight

China medical X‑Ray 2D‑radiography equipment market accounted for the largest revenue share in Asia‑Pacific in 2025, attributed to rapid urbanization, an expanding middle class, and strong domestic manufacturing of radiography equipment. The government’s focus on improving diagnostic capacity and hospital modernization is significantly boosting market growth.

Japan Medical X‑Ray 2D‑Radiography Equipment Market Insight

Japan’s medical X‑Ray 2D‑radiography equipment market is gaining momentum due to the country’s high-tech healthcare ecosystem, growing number of private clinics, and rising adoption of digital radiography solutions. The emphasis on preventive care and hospital modernization is driving demand for 2D X‑ray systems.

Medical X-Ray 2D-Radiography Equipment Market Share

The Medical X-Ray 2D-Radiography Equipment industry is primarily led by well-established companies, including:

- GE Healthcare (U.S.)

- Siemens Healthineers (Germany)

- Canon Medical Systems (Japan)

- Philips Healthcare (Netherlands)

- Fujifilm Holdings Corporation (Japan)

- Shimadzu Corporation (Japan)

- Carestream Health (U.S.)

- Planmed Oy (Finland)

- Hitachi Medical Systems (Japan)

- Neusoft Medical Systems (China)

- United Imaging Healthcare (China)

- MinFound Medical Systems (China)

- Hologic, Inc. (U.S.)

- Allengers Medical Systems (India)

- Varex Imaging Corporation (U.S.)

- Konica Minolta Healthcare (Japan)

- Delft Imaging Systems (Netherlands)

- Radcal Corporation (U.S.)

Latest Developments in Global Medical X-Ray 2D-Radiography Equipment Market

- In September 2021, GE Healthcare launched the AMX Navigate, a new portable digital X‑ray system designed to improve maneuverability and ease of use in busy clinical settings, featuring a power‑assisted free motion column to reduce technologist fatigue and enhance workflow efficiency. This launch reflects the ongoing trend toward portable, user‑focused radiography solutions

- In July 2023, Canon Medical Systems introduced the Zexira i9 Digital X‑ray RF System, a versatile digital X‑ray solution offering high image quality, low radiation dose, and a compact design to improve clinical efficiency across various healthcare environments

- In September 2023, Carestream Health launched an advanced line of digital X‑ray film processing devices that integrate enhanced imaging algorithms to deliver improved diagnostic image quality and faster processing times, aimed at optimizing clinical workflows in medical diagnostics

- In November 2023, Carestream also introduced the Horizon Digital X‑ray system, a cost‑effective and efficient solution designed for diverse healthcare facilities, expanding access to high‑quality digital radiography without compromising diagnostic performance

- In January 2024, Carestream Health launched the DRX‑Excel Plus X‑ray System, a two‑in‑one digital radiography solution featuring automatic grid parking, automatic filter control, and a touchscreen interface, while introducing dose‑limiting technologies to enhance both image quality and patient safety

- In July 2024, Siemens Healthineers began local manufacturing of its Multix Impact E digital radiography X‑ray machine in India, marking a strategic step to improve regional access to advanced imaging technology with intuitive operation and low‑dose capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.