Global Meglinitides Market

Market Size in USD Billion

USD

4.43 Billion

USD

5.61 Billion

2025

2033

USD

4.43 Billion

USD

5.61 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.43 Billion | |

| USD 5.61 Billion | |

| % | |

|

Meglinitides Market Size

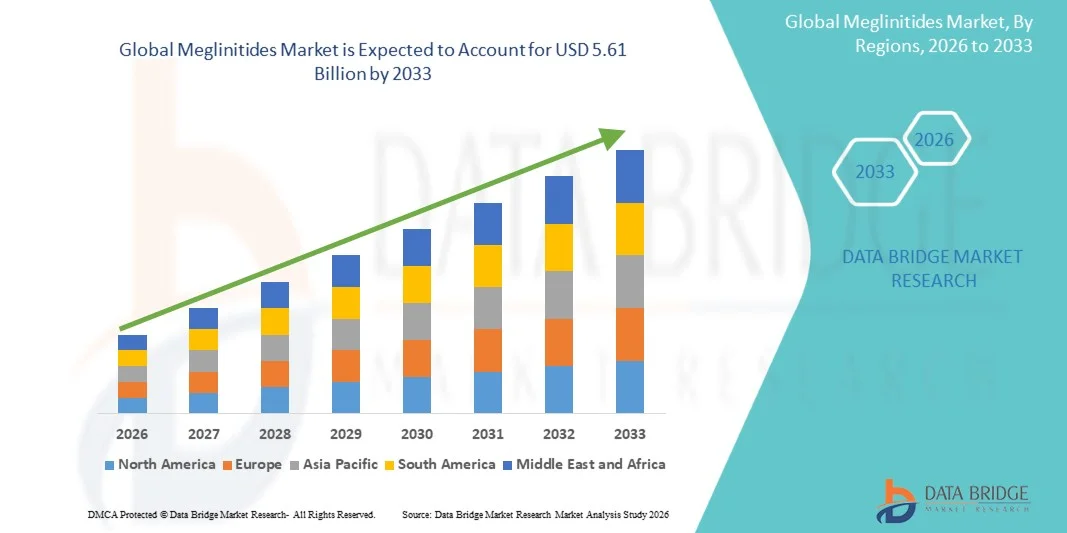

- The global Meglinitides market size was valued at USD 4.43 billion in 2025and is expected to reach USD 5.61 billion by 2033, at a CAGR of 3.00% during the forecast period

- The market growth is largely fueled by the rising global prevalence of type 2 diabetes and increasing demand for effective postprandial glucose control therapies, leading to greater adoption of meglitinides in hospitals, clinics, and outpatient care settings. Growing awareness regarding diabetes management and expansion of chronic disease treatment programs are further supporting market growth

- Furthermore, increasing preference for oral antidiabetic medications with rapid onset of action, flexible dosing schedules, and suitability for meal-time glucose regulation is establishing meglitinides as an important therapeutic option in diabetes care. These converging factors are accelerating the uptake of Meglinitides solutions, thereby significantly boosting the industry's growth

Meglinitides Market Analysis

- Meglinitides, a class of oral antidiabetic drugs used to stimulate rapid insulin secretion for postprandial glucose control in patients with type 2 diabetes, are increasingly important components of modern diabetes management due to their fast onset of action, flexible dosing schedules, and effectiveness in meal-related blood sugar regulation

- The escalating demand for meglinitides market is primarily fueled by the rising global prevalence of type 2 diabetes, increasing awareness regarding glycemic control, growing preference for oral diabetes medications, and expanding access to chronic disease treatment programs across hospitals, clinics, and retail healthcare settings

- North America dominated the meglinitides market with the largest revenue share of 36.80% in 2025, supported by advanced healthcare infrastructure, high diabetes diagnosis rates, favorable reimbursement systems, and widespread availability of branded and generic antidiabetic medications, with the U.S. witnessing steady adoption among patients requiring targeted postprandial glucose management

- Asia-Pacific is expected to be the fastest growing region in the meglinitides market during the forecast period due to rising diabetes prevalence, improving healthcare access, increasing healthcare expenditure, and growing awareness of diabetes treatment options across countries such as China, India, Japan, and South Korea

- The Oral segment accounted for the largest market revenue share of 94.2% in 2025, driven by the fact that meglinitides are primarily formulated as oral tablets for convenient diabetes management

Report Scope and Meglinitides Market Segmentation

|

Attributes |

Meglinitides Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novo Nordisk A/S (Denmark) · Sanofi S.A. (France) · Eli Lilly and Company (U.S.) · Merck & Co., Inc. (U.S.) · AstraZeneca plc (U.K.) · Boehringer Ingelheim International GmbH (Germany) · Takeda Pharmaceutical Company Limited (Japan) · Novartis AG (Switzerland) · Pfizer Inc. (U.S.) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Teva Pharmaceutical Industries Ltd. (Israel) · Viatris Inc. (U.S.) · Lupin Limited (India) · Aurobindo Pharma Limited (India) · Glenmark Pharmaceuticals Ltd. (India) · Torrent Pharmaceuticals Ltd. (India) · Zydus Lifesciences Limited (India) · Biocon Limited (India) · Cipla Limited (India) |

|

Market Opportunities |

· Expansion in emerging markets with rising diabetes prevalence · Combination therapy and personalized diabetes management growth |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Meglinitides Market Trends

“Growing Focus on Personalized Diabetes Care and Short-Acting Glucose Control Therapies”

- A significant and accelerating trend in the global Meglinitides market is the increasing emphasis on personalized diabetes management and flexible short-acting oral therapies designed to improve postprandial glucose control in patients with Type 2 Diabetes. These therapies are gaining relevance for patients requiring meal-time glucose regulation with adaptable dosing schedules

- For instance, medications such as Repaglinide and Nateglinide are widely prescribed for patients who benefit from rapid insulin secretion stimulation before meals, particularly when post-meal hyperglycemia remains inadequately controlled with other oral agents

- Growing use of combination therapy approaches is increasing the role of meglinitides alongside metformin and other antidiabetic drugs to achieve individualized glycemic targets

- Physicians are increasingly adopting patient-centric treatment strategies that consider meal patterns, age, renal status, and hypoglycemia risk when selecting short-acting secretagogues

- Expanding diabetes care access in emerging markets is also supporting continued use of established oral therapies with proven clinical effectiveness and broad physician familiarity

- This trend toward tailored glycemic management and flexible oral treatment regimens is sustaining interest in meglinitides within the broader diabetes therapeutics landscape

Meglinitides Market Dynamics

Driver

“Rising Prevalence of Type 2 Diabetes and Demand for Effective Postprandial Glucose Management”

- The increasing global prevalence of Type 2 diabetes and growing awareness regarding the importance of controlling postprandial blood glucose levels are major drivers supporting the growth of the Meglinitides market

- For instance, endocrinologists and primary care physicians continue prescribing Repaglinide for patients who experience elevated meal-time glucose spikes or require a shorter-acting insulin secretagogue alternative to sulfonylureas

- Sedentary lifestyles, obesity, and aging populations are contributing to higher diabetes incidence, thereby increasing demand for diversified oral treatment options

- Improved screening rates and earlier diagnosis of diabetes are enabling faster treatment initiation and long-term glucose management strategies

- In addition, rising healthcare access in developing economies is expanding the patient base receiving pharmacological diabetes treatment

Restraint/Challenge

“Competition from Newer Therapies, Hypoglycemia Risk, and Frequent Dosing Requirements”

- Intense competition from newer antidiabetic drug classes such as GLP-1 receptor agonists, SGLT2 inhibitors, and DPP-4 inhibitors remains a major challenge for the Meglinitides market

- For instance, many clinicians now prefer newer agents that offer added benefits such as weight reduction, cardiovascular protection, or lower hypoglycemia risk, reducing first-line reliance on meglinitides in some markets

- Meglinitides may still cause hypoglycemia and weight gain in certain patients, particularly when meal timing is inconsistent or dosing is not properly managed

- The need for multiple daily dosing before meals can reduce adherence compared with once-daily oral therapies

- Addressing these challenges through better patient selection, combination therapy positioning, and cost-effective access strategies will be essential for sustained market growth

Meglinitides Market Scope

The market is segmented on the basis of indication, drugs, route of administration, end-users, and distribution channel.

- By Indication

On the basis of indication, the Meglinitides market is segmented into Type II Diabetes and Others. The Type II Diabetes segment dominated the largest market revenue share of 88.6% in 2025, driven by the widespread use of meglinitides in managing postprandial blood glucose levels among patients with type II diabetes mellitus. Rising global prevalence of obesity, sedentary lifestyles, and aging populations are significantly increasing the diabetic patient pool. Meglinitides are particularly preferred for patients requiring flexible mealtime glucose control. Growing awareness regarding early glycemic management is supporting prescription demand. Physicians often prescribe these agents when metformin monotherapy is insufficient or contraindicated. Increasing diagnosis rates in emerging economies are further contributing to market growth. Expanding access to oral antidiabetic medicines also supports adoption. Improved healthcare infrastructure and diabetes screening programs are boosting treatment uptake. Availability of branded and generic products strengthens accessibility. Rising incidence of metabolic syndrome further supports demand. These factors ensure dominance of the Type II Diabetes segment.

The Others segment is expected to witness the fastest growth rate of 6.9% CAGR from 2026 to 2033, driven by niche usage in secondary diabetes conditions and off-label glycemic management scenarios. Growing physician interest in personalized treatment combinations is supporting limited expansion. Increasing prevalence of steroid-induced hyperglycemia and mixed metabolic disorders contributes to demand. Better awareness of individualized diabetes care pathways is also driving adoption. Hospitals are increasingly using combination regimens for complex patients. Advancements in endocrinology treatment protocols support broader therapeutic exploration. Rising research into glucose variability management is another growth factor. Expanding specialist consultation networks in developing regions also aid market penetration. Improved patient monitoring technologies enable tailored therapy use. Although smaller in share, demand remains steadily increasing. These factors collectively make the Others segment the fastest-growing category.

- By Drugs

On the basis of drugs, the Meglinitides market is segmented into Repaglinide, Nateglinide, Mitiglinide, and Others. The Repaglinide segment held the largest market revenue share of 46.7% in 2025, driven by its strong clinical efficacy in reducing post-meal glucose spikes and broad availability across global markets. Repaglinide is widely prescribed due to rapid onset and short duration of action, allowing flexible meal-based dosing. Physicians prefer it for patients needing individualized glycemic control. Increasing type II diabetes burden is significantly supporting prescription volumes. Availability in generic form improves affordability and market penetration. Rising awareness regarding postprandial glucose management further boosts demand. Repaglinide is often used in combination with metformin or other oral agents. Strong hospital and retail pharmacy stocking supports continuous supply. Established clinical familiarity among endocrinologists reinforces dominance. Expanding diabetic populations in Asia-Pacific also aid growth. These factors maintain leadership of the Repaglinide segment.

The Mitiglinide segment is expected to witness the fastest growth rate of 8.4% CAGR from 2026 to 2033, driven by increasing adoption in Asian markets where it is widely utilized for rapid glucose control. Mitiglinide offers quick insulin secretion stimulation with reduced duration, supporting lower hypoglycemia risk. Growing demand for tailored diabetes therapy is boosting segment expansion. Rising elderly diabetic populations needing safer mealtime drugs further support adoption. Increasing physician preference for region-specific treatment protocols is another factor. Expanding healthcare expenditure in Japan and neighboring markets strengthens demand. Improved awareness of postprandial glucose complications is driving prescriptions. Ongoing clinical studies on combination therapy use also support growth. Better availability through retail and hospital channels aids access. These drivers position Mitiglinide as the fastest-growing drug segment.

- By Route of Administration

On the basis of route of administration, the Meglinitides market is segmented into Oral and Others. The Oral segment accounted for the largest market revenue share of 94.2% in 2025, driven by the fact that meglinitides are primarily formulated as oral tablets for convenient diabetes management. Oral medicines remain highly preferred due to ease of use, patient comfort, and better long-term compliance. Rising diabetic population globally is significantly boosting demand for oral antidiabetic therapies. Physicians often recommend oral agents before insulin initiation in type II diabetes. Growing awareness regarding early treatment adherence is further supporting growth. Availability through hospital, retail, and online pharmacies enhances accessibility. Generic competition keeps treatment costs relatively affordable. Patients prefer tablet regimens due to non-invasive administration. Strong outpatient treatment trends further reinforce segment leadership. Regular follow-up prescriptions support recurring revenue. These factors ensure dominance of the Oral segment.

The Others segment is expected to witness the fastest growth rate of 5.8% CAGR from 2026 to 2033, driven by research into alternative delivery systems and combination treatment technologies. Though currently limited in market share, innovation in novel formulations may create new opportunities. Increasing demand for patient-friendly drug delivery methods supports exploration. Pharmaceutical companies are investing in advanced diabetes care platforms. Growth in combination therapies may also support non-traditional routes. Better patient monitoring systems enable customized therapy delivery. Rising focus on improving adherence among elderly patients contributes to demand. Technological innovation in controlled-release systems further aids expansion. Clinical trials and pipeline development remain key drivers. These factors make Others the fastest-growing route category.

- By End-Users

On the basis of end-users, the Meglinitides market is segmented into Hospitals, Homecare, Speciality Centres, and Others. The Homecare segment dominated the largest market revenue share of 48.9% in 2025, driven by the chronic and long-term nature of diabetes treatment, where most patients manage therapy outside institutional settings. Oral meglinitides are highly suitable for home-based daily use. Increasing preference for self-management of diabetes is significantly supporting growth. Availability of glucose monitoring devices enables better treatment compliance at home. Rising awareness regarding diet, exercise, and medication adherence further boosts segment demand. Aging populations prefer convenient home treatment rather than repeated hospital visits. Telemedicine and digital diabetes coaching programs are also supporting adoption. Growing pharmacy delivery networks strengthen accessibility. Recurring prescription refill demand supports revenue growth. These factors ensure Homecare remains the dominant end-user segment.

The Speciality Centres segment is expected to witness the fastest growth rate of 7.6% CAGR from 2026 to 2033, driven by increasing number of diabetes clinics and endocrinology-focused treatment centers globally. Patients seek specialist consultation for uncontrolled blood sugar and combination therapy optimization. Rising prevalence of complex metabolic disorders is boosting specialist visits. Advanced diagnostic and counseling services improve treatment outcomes. Urbanization and growing healthcare awareness support expansion of specialty centers. Physicians in these centers increasingly prescribe tailored meglinitide regimens. Better access in emerging economies is further aiding growth. Preventive diabetes management programs also support demand. Higher referral rates from general practitioners contribute significantly. These factors position Speciality Centres as the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the Meglinitides market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Retail Pharmacy segment held the largest market revenue share of 52.3% in 2025, driven by routine monthly refills of oral diabetes medications through local pharmacy networks. Retail pharmacies remain the most accessible source of chronic care medicines globally. Patients prefer nearby stores for convenience and pharmacist guidance. Strong availability of branded and generic meglinitides supports demand. Increasing diabetic population significantly boosts recurring prescription volumes. Retail chains often provide discounts and adherence programs. Expansion of pharmacy networks in emerging countries further strengthens growth. Walk-in accessibility and trusted service reinforce consumer preference. Physician prescriptions are commonly fulfilled through retail outlets. These factors ensure Retail Pharmacy remains dominant.

The Online Pharmacy segment is expected to witness the fastest growth rate of 10.2% CAGR from 2026 to 2033, driven by rapid digitalization of healthcare and growing preference for doorstep medicine delivery. Chronic diabetic patients increasingly use subscription refill services for convenience. Competitive pricing and discounts are attracting price-sensitive consumers. Smartphone penetration and e-commerce trust are accelerating adoption globally. Integration with telemedicine platforms supports seamless prescription fulfillment. Wider reach in semi-urban and remote regions enhances access. Automated reminders improve treatment adherence. Secure payment systems and faster logistics further strengthen demand. Younger patient populations are especially driving online purchases. These factors collectively make Online Pharmacy the fastest-growing distribution channel segment.

Meglinitides Market Regional Analysis

- North America dominated the meglinitides market with the largest revenue share of 36.80% in 2025, supported by advanced healthcare infrastructure, high diabetes diagnosis rates, favorable reimbursement systems, and widespread availability of branded and generic antidiabetic medications

- The region benefits from strong physician awareness, established diabetes management programs, and increasing focus on personalized glycemic control strategies

- Patients and healthcare providers in the region highly value the rapid onset of action and flexible dosing profile offered by meglinitides for controlling postprandial blood glucose levels. These therapies are particularly utilized among patients requiring meal-time glucose management and individualized treatment approaches

U.S. Meglinitides Market Insight

The U.S. meglinitides market captured the largest revenue share within North America in 2025, driven by steady adoption among patients requiring targeted postprandial glucose management. The country benefits from strong diabetes screening rates, broad access to endocrinology care, and availability of both branded and generic formulations. Healthcare providers are increasingly incorporating meglinitides into treatment regimens for suitable patients who require flexible meal-time dosing or additional glycemic control alongside other oral therapies. Rising prevalence of obesity and type 2 diabetes continues to support market demand in the U.S.

Europe Meglinitides Market Insight

The Europe meglinitides market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing diabetes prevalence, aging populations, and growing focus on effective outpatient disease management. The region is witnessing rising demand for oral antidiabetic therapies that offer flexible glucose control and can be integrated into combination treatment regimens. Favorable healthcare systems and increasing awareness of early diabetes intervention are contributing to market growth across Europe.

U.K. Meglinitides Market Insight

The U.K. meglinitides market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising burden of type 2 diabetes and increasing emphasis on preventive and long-term metabolic care. Healthcare providers are focusing on individualized treatment strategies, creating opportunities for meglinitides in selected patient populations. Expanding access to diabetes education and routine monitoring is expected to further stimulate market growth in the U.K.

Germany Meglinitides Market Insight

The Germany meglinitides market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high awareness of chronic disease management, and demand for effective glucose-lowering therapies. Germany’s established pharmaceutical market and emphasis on evidence-based diabetes treatment are promoting adoption of meglinitides, particularly in outpatient and specialty care settings. Increasing elderly population levels are also supporting market expansion.

Asia-Pacific Meglinitides Market Insight

The Asia-Pacific meglinitides market is poised to grow at the fastest CAGR during the forecast period due to rising diabetes prevalence, improving healthcare access, increasing healthcare expenditure, and growing awareness of diabetes treatment options across countries such as China, India, Japan, and South Korea. Rapid urbanization, changing dietary habits, and sedentary lifestyles are significantly increasing the diabetic population in the region. Expanding healthcare coverage and broader access to affordable medications are further accelerating market growth across Asia-Pacific.

Japan Meglinitides Market Insight

The Japan meglinitides market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong focus on chronic disease control. Japanese physicians increasingly emphasize precise postprandial glucose management, supporting demand for meglinitides in selected treatment plans. Availability of advanced monitoring systems and strong patient compliance programs are further aiding market growth.

China Meglinitides Market Insight

The China meglinitides market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large diabetic population, expanding middle class, and improving healthcare accessibility. China is witnessing growing adoption of oral antidiabetic drugs through hospital and retail pharmacy channels. Government efforts to strengthen chronic disease management, along with increasing availability of affordable generic therapies, are key factors propelling the meglinitides market in the country.

Meglinitides Market Share

The Meglinitides industry is primarily led by well-established companies, including:

- Novo Nordisk A/S (Denmark)

- Sanofi S.A. (France)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Viatris Inc. (U.S.)

- Lupin Limited (India)

- Aurobindo Pharma Limited (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Torrent Pharmaceuticals Ltd. (India)

- Zydus Lifesciences Limited (India)

- Biocon Limited (India)

- Cipla Limited (India)

Latest Developments in Global Meglinitides Market

- In September 2021, several generic pharmaceutical manufacturers expanded global supply of repaglinide tablets following increased demand for affordable oral antidiabetic medicines in emerging markets. The move strengthened availability of meglinitide therapies through retail and hospital pharmacy channels worldwide

- In August 2022, updated global diabetes treatment reviews highlighted repaglinide as a useful therapy for patients with irregular meal schedules and elderly populations needing short-acting insulin secretagogues, reinforcing physician interest in meglinitides for personalized treatment approaches

- In November 2022, pharmaceutical companies in Asia-Pacific markets increased production and commercialization of repaglinide and nateglinide generics as governments promoted lower-cost diabetes medications to address rising Type 2 diabetes prevalence

- In May 2023, multiple manufacturers introduced new fixed-dose combination products containing repaglinide with other glucose-lowering agents in select markets, aiming to improve patient adherence, reduce pill burden, and enhance post-meal glycemic control. This development reflected renewed innovation within mature meglinitide therapies

- In October 2023, healthcare providers reported continued use of repaglinide in combination therapy regimens for patients unable to tolerate metformin or sulfonylureas, supporting sustained prescription demand for meglinitides despite increasing competition from newer diabetes drug classes

- In March 2024, pharmaceutical distributors expanded online and retail pharmacy availability of generic repaglinide products across several international markets, improving access to affordable oral diabetes medicines and supporting broader outpatient treatment continuity

- In July 2024, clinical reviews emphasized repaglinide’s lower risk of prolonged hypoglycemia compared with longer-acting insulin secretagogues, encouraging continued use in selected elderly and renal-impaired patient groups under physician supervision

- In January 2025, market participants reported continued investment in repaglinide formulation improvements, including enhanced tablet stability, packaging innovations, and patient-friendly dosing formats designed to maintain competitiveness in the global oral antidiabetic market

- In June 2025, global healthcare systems in cost-sensitive regions continued favoring generic meglinitides such as repaglinide and nateglinide as economical adjunct therapies for Type 2 diabetes, particularly where access to premium GLP-1 and SGLT2 therapies remains limited

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.