Global Mek Inhibitors Market

Market Size in USD Billion

USD

2.79 Billion

USD

4.86 Billion

2025

2033

USD

2.79 Billion

USD

4.86 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.79 Billion | |

| USD 4.86 Billion | |

| % | |

|

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Size

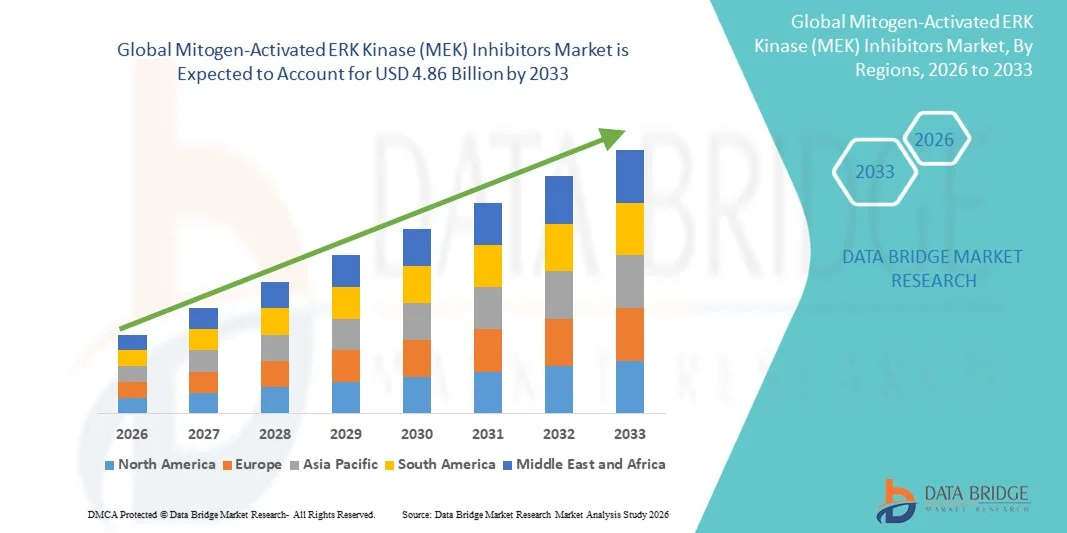

- The global Mitogen-Activated ERK Kinase (MEK) Inhibitors market size was valued at USD 2.79 billion in 2025 and is expected to reach USD 4.86 billion by 2033, at a CAGR of 7.20% during the forecast period

- The market growth is largely fueled by rapid advancements in targeted cancer therapies and increasing adoption of precision medicine, leading to higher demand for Mitogen-Activated ERK Kinase (MEK) Inhibitors in oncology treatment

- Furthermore, rising prevalence of cancers driven by MAPK/ERK pathway mutations, combined with strong investments in R&D and growing regulatory approvals for novel MEK inhibitors, is accelerating the uptake of Mitogen-Activated ERK Kinase (MEK) Inhibitors solutions, thereby significantly boosting the industry's growth

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Analysis

- Smart MEK inhibitors, offering targeted therapy for cancers driven by MAPK/ERK pathway mutations, are increasingly vital components of modern oncology treatment in both hospital and specialty clinic settings due to their high specificity, improved patient outcomes, and compatibility with combination therapies

- The escalating demand for MEK inhibitors is primarily fueled by rising prevalence of melanoma, non-small cell lung cancer, and other MAPK/ERK-driven cancers, growing awareness among oncologists, and increasing approvals of new-generation MEK inhibitors with improved safety profile

- North America dominated the mitogen-activated ERK kinase (MEK) inhibitors market with the largest revenue share of 42.5% in 2025, characterized by advanced oncology infrastructure, high healthcare expenditure, and strong presence of key pharmaceutical players, with the U.S. experiencing substantial growth in MEK inhibitor usage due to clinical adoption and supportive regulatory policies

- Asia-Pacific is expected to be the fastest-growing region in the mitogen-activated ERK kinase (MEK) Inhibitors market during the forecast period, with a projected CAGR of 9.8% from 2026 to 2033, driven by increasing cancer prevalence, growing healthcare investments, and rising patient access to targeted therapies

- The oral segment dominated the largest market revenue share of 87.5% in 2025, due to ease of administration, patient adherence, and suitability for outpatient care

Report Scope and Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Segmentation

|

Attributes |

Mitogen-Activated ERK Kinase (MEK) Inhibitors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Roche (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Trends

“Increasing Adoption of Targeted and Combination Therapies”

- A significant and accelerating trend in the global mitogen-activated ERK kinase (MEK) inhibitors market is the rising adoption of MEK inhibitors as part of targeted cancer therapy regimens and combination treatments. Researchers and pharmaceutical companies are increasingly focusing on next-generation MEK inhibitors with enhanced specificity, reduced side effects, and improved patient outcomes

- For instance, combination therapies that pair MEK inhibitors with BRAF inhibitors or immunotherapies are being actively tested in clinical trials for melanoma and non-small cell lung cancer, offering enhanced efficacy compared to monotherapies

- The growing emphasis on precision medicine and personalized oncology is driving the development of MEK inhibitor formulations tailored to individual molecular profiles. This allows clinicians to target specific pathways in tumor cells while minimizing systemic toxicity, improving both survival rates and quality of life for patients

- Furthermore, ongoing R&D into oral formulations, sustained-release versions, and combination protocols is shaping the market by improving treatment convenience, adherence, and effectiveness

- The trend towards personalized, pathway-targeted oncology treatments is fundamentally redefining the standards of care in cancer therapy, encouraging healthcare providers to integrate MEK inhibitors into broader therapeutic strategies

- The global demand for MEK inhibitors is growing rapidly as oncology treatment protocols evolve, particularly in regions with advanced healthcare infrastructure and active clinical trial networks

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Dynamics

Driver

“Growing Need Due to Rising Security Concerns and Smart Home Adoption”

- The increasing prevalence of cancers, including melanoma, non-small cell lung cancer (NSCLC), and colorectal cancer, is a primary driver for the MEK inhibitors market. Patients and healthcare providers are seeking therapies that offer higher efficacy with manageable side effect profiles

- For instance, in March 2025, AstraZeneca initiated a multi-country Phase II study investigating the efficacy of its MEK inhibitor selumetinib in combination with a PD-1 inhibitor in NSCLC patients. Early results showed enhanced tumor suppression compared to standard chemotherapy, reinforcing clinician confidence in MEK-targeted combination therapies

- Expansion of healthcare infrastructure, particularly in emerging markets, alongside rising healthcare expenditure, is facilitating greater access to MEK inhibitors. Countries like China, India, and Brazil are increasingly incorporating advanced oncology therapies into national treatment programs

- Growing awareness of precision medicine and molecular profiling is encouraging physicians to adopt MEK inhibitors as part of individualized treatment plans, particularly for patients with known BRAF or KRAS mutations

- The increasing number of ongoing clinical trials across oncology indications continues to strengthen the market pipeline, demonstrating strong potential for both monotherapy and combination treatment applications

Restraint/Challenge

“High Treatment Costs and Potential Adverse Effects”

- Despite their clinical advantages, MEK inhibitors are often associated with high treatment costs, limiting accessibility for patients in low- and middle-income regions. The cost factor can also impact reimbursement decisions, slowing adoption in certain healthcare systems

- For instance, a 2025 report by the National Cancer Institute highlighted that patients receiving combination MEK and BRAF inhibitor therapy incurred treatment costs nearly double that of standard chemotherapy, which may reduce adherence or delay therapy initiation

- MEK inhibitors may cause adverse effects such as rash, diarrhea, cardiovascular events, and ocular toxicity, requiring careful monitoring and sometimes dose adjustments. These safety concerns can limit long-term patient compliance and treatment continuation

- Regulatory hurdles, including slower approvals in emerging markets and competition from alternative therapies like immunotherapies, can also constrain market expansion

- The necessity of frequent clinical monitoring, along with the need for companion diagnostic testing, adds complexity to treatment management, which may deter adoption by both patients and healthcare providers

- Overcoming these challenges through patient support programs, innovative pricing strategies, and the development of safer, next-generation MEK inhibitors will be vital to sustaining long-term market growth

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Scope

The market is segmented on the basis of target, type, application, route of administration, end-users, and distribution channel.

• By Target

On the basis of target, the Mitogen-Activated ERK Kinase (MEK) Inhibitors market is segmented into MEK1 and MEK2. The MEK1 segment dominated the largest market revenue share of 57.4% in 2025, primarily due to its central role in the MAPK/ERK signaling pathway, which is critical in cancer cell proliferation and survival. MEK1 inhibitors are widely used in combination with BRAF inhibitors for treating melanoma and other solid tumors, supported by numerous clinical trials and FDA-approved therapies. Their high efficacy in targeted therapies and favorable safety profiles enhance adoption across oncology centers. Hospitals and specialty clinics prefer MEK1 inhibitors due to established treatment protocols, extensive clinical evidence, and accessibility for both first-line and second-line therapies. The dominance of this segment is further reinforced by increased awareness of precision medicine and personalized oncology approaches. Continuous R&D efforts and expanding patient populations for targeted therapies drive sustained demand. MEK1 inhibitors also receive strong support from oncology guidelines for combination therapy regimens, contributing to consistent usage in clinical practice. In addition, healthcare investments and reimbursement policies favor MEK1-targeted treatments. These factors collectively maintain MEK1’s leadership in the market.

The MEK2 segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by emerging clinical evidence highlighting its complementary role in the MAPK pathway. MEK2 inhibitors are increasingly being evaluated in combination with immunotherapies and other kinase inhibitors, offering expanded treatment options for patients with resistant or metastatic cancers. Growing interest in dual MEK1/MEK2 targeting therapies supports pipeline development and accelerates market adoption. Specialty clinics and hospitals are adopting MEK2-targeted therapies for advanced-stage cancers where conventional therapies show limited efficacy. Enhanced patient outcomes and improved tolerability profiles further encourage adoption. Increasing collaborations between pharmaceutical companies and research institutions are boosting clinical trial activity for MEK2 inhibitors. As awareness of MEK2’s role in tumorigenesis spreads among oncologists, the segment is witnessing steady uptake. Digital health platforms and tele-oncology services are also contributing to increased access for patients in remote locations. Overall, MEK2 inhibitors are expected to show robust growth driven by clinical innovation and expanding indications.

• By Type

On the basis of type, the market is segmented into MEKINIST (Trametinib), COTELLIC (Cobimetinib), and MEKTOVI (Binimetinib). The MEKINIST (Trametinib) segment dominated the largest market revenue share of 46.8% in 2025, owing to its early FDA approval, well-established efficacy, and broad adoption in combination therapies for melanoma and NSCLC. Trametinib is widely prescribed due to its demonstrated survival benefits and strong safety profile. Hospitals and specialty clinics favor MEKINIST because of extensive clinical guidelines and long-term post-market data supporting its use. The dominance is also supported by significant marketing efforts, physician familiarity, and inclusion in standard treatment protocols. Its oral administration provides convenience for outpatient care and home-based therapy management. Patient adherence, insurance coverage, and growing awareness of targeted therapies further strengthen its market position. Availability across hospital and retail pharmacies ensures widespread access, while continuous post-market studies reinforce clinician confidence. Trametinib’s combination regimens with BRAF inhibitors remain standard of care in many oncology settings. Strong global presence in both developed and emerging markets maintains MEKINIST’s leadership.

The COTELLIC (Cobimetinib) segment is projected to witness the fastest CAGR of 7.5% from 2026 to 2033, driven by expanding clinical applications and combination therapy approvals. Cobimetinib is increasingly used alongside BRAF inhibitors in patients with advanced melanoma, and its clinical pipeline includes trials for other solid tumors. Growing awareness among oncologists, coupled with increased access through hospitals and specialty clinics, supports rapid adoption. Patient preference for oral therapies and improved tolerability profiles contribute to growth. COTELLIC’s uptake is further aided by regional approvals, reimbursement coverage, and expansion in emerging markets. Tele-oncology and digital health platforms are also enhancing patient reach, supporting the segment’s high CAGR.

• By Application

On the basis of application, the market is segmented into NSCLC, Cancer (other types), and others. The NSCLC segment dominated the largest market revenue share of 52.3% in 2025, due to the high prevalence of non-small-cell lung cancer globally and the proven efficacy of MEK inhibitors in combination therapies. Hospitals and specialty clinics favor MEK inhibitors for NSCLC because of established treatment guidelines, clinical trial data, and the need for precision oncology approaches. Early detection programs, increasing lung cancer screening, and rising patient awareness contribute to the strong adoption of MEK inhibitors in NSCLC treatment. The segment’s dominance is also supported by insurance coverage, availability of oral formulations, and patient compliance with targeted therapies. Advanced hospitals and cancer centers are central to delivering combination regimens, reinforcing NSCLC’s leading share. Continuous R&D and pipeline expansions for NSCLC indications maintain robust market demand.

The other cancer types segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by expanding clinical research into melanoma, colorectal cancer, and other solid tumors. As oncologists explore novel combination therapies and precision medicine approaches, MEK inhibitors are increasingly adopted for patients with diverse tumor profiles. Growth is further supported by clinical trials, emerging approvals, and rising awareness of personalized treatment regimens. Hospitals and specialty clinics are integrating MEK inhibitors into broader oncology care pathways. Patient demand for targeted therapies, coupled with increased diagnostic capabilities, enhances adoption. The combination of MEK inhibitors with immunotherapies provides new opportunities in advanced-stage cancers, contributing to the strong projected CAGR.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral and others. The oral segment dominated the largest market revenue share of 87.5% in 2025, due to ease of administration, patient adherence, and suitability for outpatient care. Oral MEK inhibitors allow patients to manage therapy at home, reducing hospitalization costs and supporting long-term treatment regimens. Hospitals and clinics prefer oral administration for convenience and streamlined treatment protocols. Widespread insurance coverage and inclusion in standard care guidelines further reinforce oral therapy dominance. The high bioavailability and consistent therapeutic effect of oral MEK inhibitors contribute to their market leadership. Physicians and oncologists continue to recommend oral formulations for both monotherapy and combination regimens. Distribution through hospital and retail pharmacies ensures timely access. Oral therapy’s simplicity enhances patient compliance, particularly in long-term NSCLC and melanoma management. Market demand is bolstered by global initiatives promoting targeted therapy adoption and precision medicine in oncology.

The others segment is expected to witness a CAGR of 5.8% from 2026 to 2033, driven by investigational administration routes in clinical trials, including intravenous or combination delivery methods. Emerging research focuses on enhancing drug bioavailability and efficacy in challenging tumor environments. Hospitals and specialty clinics adopt alternative routes for patients with absorption issues or severe side effects. Pipeline developments, clinical trial expansions, and regulatory approvals contribute to steady growth. As therapeutic strategies diversify, these alternative administration methods support specialized treatment protocols, fueling segmental expansion.

• By Distribution Channel

On the basis of distribution channel, the MEK Inhibitors market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 54.6% in 2025, driven by the high concentration of oncology treatments and the need for controlled, prescription-based dispensing. Hospitals and specialty cancer centers serve as primary points for MEK inhibitor administration, ensuring adherence to treatment protocols and monitoring patient outcomes. Hospital pharmacies facilitate immediate access to MEK inhibitors for hospitalized patients receiving combination therapies for NSCLC and other cancers. The segment’s dominance is reinforced by centralized drug procurement, insurance coverage, and the ability to provide patient counseling on oral targeted therapies. In addition, hospital pharmacies are equipped to handle specialty medications requiring strict storage and dispensing conditions. Collaboration with oncology specialists and clinical trial sites also strengthens hospital pharmacy’s leading position. Continuous growth in hospital infrastructure and cancer treatment facilities globally supports sustained adoption of this distribution channel.

The online pharmacy segment is expected to witness the fastest CAGR of 7.3% from 2026 to 2033, fueled by the increasing demand for home-based medication delivery and telehealth integration. Patients and caregivers are increasingly using digital healthcare platforms to order MEK inhibitors, especially for oral formulations. Growth is further supported by improved logistics for cold-chain and specialty drug delivery, rising patient awareness, and convenience of doorstep delivery. E-commerce adoption in healthcare, along with regulatory approvals for online prescription fulfillment, accelerates the segment’s expansion. Online pharmacies provide access for patients in remote or underserved regions, bridging gaps in oncology care. The convenience of home delivery reduces treatment interruptions and enhances patient compliance. Rising digital literacy and smartphone penetration also contribute to adoption. Specialty online pharmacies offering counseling and tracking services are driving trust among patients and caregivers. Partnerships with hospitals and oncology clinics for prescription verification strengthen online pharmacy growth potential.

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Regional Analysis

North America dominated the mitogen-activated ERK kinase (MEK) inhibitors market with the largest revenue share of 42.5% in 2025. This strong market position is characterized by a well-established oncology infrastructure, substantial healthcare expenditure, and the presence of leading pharmaceutical companies actively developing and commercializing MEK inhibitors. The U.S., in particular, has witnessed substantial growth in MEK inhibitor usage, driven by clinical adoption, supportive regulatory policies, and increasing availability of targeted therapies for cancers such as melanoma, non-small cell lung cancer (NSCLC), and colorectal cancer. In addition, the region benefits from extensive clinical trial networks, high patient awareness of personalized medicine, and robust research and development pipelines, which collectively accelerate the adoption of MEK-targeted therapies.

U.S. Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

The U.S. mitogen-activated ERK kinase (MEK) inhibitors market captured the largest revenue share of the region in 2025, reflecting rapid uptake across oncology centers and hospitals. Clinicians are increasingly adopting MEK inhibitors as part of combination therapies, particularly alongside BRAF inhibitors or immune checkpoint inhibitors, to improve treatment efficacy. For instance, in 2024, Novartis reported positive Phase III results combining binimetinib with a BRAF inhibitor in advanced melanoma patients, demonstrating improved progression-free survival over monotherapy. Rising awareness among patients about targeted therapies, alongside enhanced diagnostic capabilities and molecular profiling, further supports the country’s strong market performance.

Europe Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

The Europe mitogen-activated ERK kinase (MEK) inhibitors market is projected to expand at a substantial CAGR during the forecast period, propelled by increasing cancer incidence, stringent healthcare regulations, and a growing emphasis on precision oncology. Countries such as Germany, France, and Italy are witnessing heightened adoption due to expanding access to targeted therapies and supportive reimbursement policies. In addition, the proliferation of clinical trials in combination therapies and collaborative research initiatives across European institutions is driving awareness and confidence in MEK inhibitor treatment regimens. The region’s increasing focus on personalized medicine and healthcare digitalization is further contributing to market growth.

U.K. Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

The U.K. MEK inhibitors market is anticipated to grow at a notable rate over the forecast period, driven by rising cancer prevalence, national healthcare initiatives, and strong adoption of targeted therapies. The National Health Service (NHS) has increasingly incorporated MEK inhibitors into treatment protocols for cancers such as BRAF-mutant melanoma, expanding patient access. Ongoing clinical studies evaluating MEK inhibitor combination therapies and improved patient outcomes are further encouraging adoption, while increased patient education about personalized cancer treatments supports steady market expansion.

Germany Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

Germany’s mitogen-activated ERK kinase (MEK) inhibitors market is expected to expand at a significant CAGR during the forecast period. The country’s advanced healthcare system, strong research and development ecosystem, and increasing availability of targeted cancer therapies are key growth drivers. Regulatory support and early access programs for innovative oncology drugs allow patients to benefit from novel MEK inhibitor therapies. In addition, ongoing collaborations between pharmaceutical companies and academic institutions are accelerating clinical research and adoption of these therapies across hospitals and oncology centers.

Asia-Pacific Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

The Asia-Pacific mitogen-activated ERK kinase (MEK) inhibitors market is poised to be the fastest-growing region during the forecast period, with a projected CAGR of 9.8% from 2026 to 2033. The growth is primarily driven by increasing cancer prevalence, rising healthcare investments, and expanding patient access to targeted therapies in countries such as China, India, and Japan. Improved healthcare infrastructure, government initiatives promoting cancer care, and growing awareness of precision oncology among clinicians and patients are driving adoption. Moreover, increasing participation in clinical trials for MEK inhibitors and rising production capacities by domestic manufacturers are enhancing the region’s market accessibility.

Japan Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

Japan’s mitogen-activated ERK kinase (MEK) inhibitors market is gaining momentum due to the country’s advanced oncology ecosystem, high patient awareness, and strong government support for targeted cancer therapies. The integration of MEK inhibitors into combination therapy protocols, particularly for melanoma and NSCLC, is becoming increasingly common. Japan’s aging population, which has a higher risk of cancer incidence, is further boosting demand for effective targeted therapies. In addition, continuous investments in clinical research and development of next-generation inhibitors are enhancing the market’s growth prospects.

China Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Insight

China mitogen-activated ERK kinase (MEK) inhibitors market accounted for the largest revenue share in the Asia-Pacific MEK inhibitors market in 2025. Rapid urbanization, rising healthcare expenditure, and growing cancer incidence are fueling demand. The country’s expanding middle class and increasing patient awareness of precision medicine are supporting adoption, while government initiatives promoting oncology care and the availability of domestically manufactured MEK inhibitors are improving accessibility. Large-scale clinical studies and strategic partnerships between local and multinational pharmaceutical companies are further accelerating market expansion.

Mitogen-Activated ERK Kinase (MEK) Inhibitors Market Share

The Mitogen-Activated ERK Kinase (MEK) Inhibitors industry is primarily led by well-established companies, including:

• Roche (Switzerland)

• Novartis (Switzerland)

• Pfizer (U.S.)

• GlaxoSmithKline (U.K.)

• Merck & Co. (U.S.)

• AstraZeneca (U.K.)

• Array BioPharma (U.S.)

• Pierre Fabre (France)

• Amgen (U.S.)

• Bristol-Myers Squibb (U.S.)

• Bayer (Germany)

• Daiichi Sankyo (Japan)

• Takeda Pharmaceutical (Japan)

• Servier (France)

• BeiGene (China)

• Incyte Corporation (U.S.)

• AbbVie (U.S.)

• Johnson & Johnson (U.S.)

• Sun Pharma (India)

• Sanofi (France

Latest Developments in Global Mitogen-Activated ERK Kinase (MEK) Inhibitors Market

- In October 2021, ResearchAndMarkets.com published a comprehensive report on the Global MEK Inhibitors Market to 2026, highlighting that four MEK inhibitors were already marketed and several pipeline candidates (e.g., AZD8330, NX‑179, HL‑085, E6201, Mirdametinib, Refametinib) were expected to enter the market in coming years, expanding indications beyond melanoma into cancers like NSCLC, thyroid, breast, and ovarian cancers

- In March 2023, the U.S. FDA approved the combination of Tafinlar (dabrafenib) with Mekinist (trametinib) to treat pediatric patients aged ≥1 year with low‑grade glioma that has a BRAF V600E mutation, expanding the patient population for MEK inhibitor‑based therapy

- In October 2023, the FDA approved the combination of BRAFTOVI (encorafenib) and MEKTOVI (binimetinib) for adult patients with metastatic non‑small cell lung cancer (NSCLC) harboring the BRAF V600E mutation – a significant regulatory milestone linking MEK inhibition to broader solid tumor indications

- In March 2024, tunlametinib (HL‑085), a MEK inhibitor, was approved in China for the treatment of NRAS‑mutated advanced melanoma in patients previously treated with PD‑1/PD‑L1 inhibitors, marking a first‑in‑region approval for the drug

- In February 2025, the U.S. FDA granted priority review for the new drug application (NDA) of mirdametinib—a novel MEK inhibitor—for patients with NF1 (neurofibromatosis type 1) with symptomatic inoperable plexiform neurofibromas, with a PDUFA action date set for 28 February 2025

- In February 2025, Merck KGaA agreed to acquire SpringWorks Therapeutics for approx. USD 3.9 billion, a strategic move that strengthens Merck’s oncology portfolio with MEK inhibitor assets such as mirdametinib, reflecting industry consolidation around MEK‑focused therapies

- In November 2025, selumetinib was approved in the United States for adult patients with neurofibromatosis type 1 (NF1) who have symptomatic, inoperable plexiform neurofibromas, broadening the clinical use of this MEK inhibitor in rare disease indications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.