Global Melioidosis Treatment Market

Market Size in USD Billion

USD

300.00 Billion

USD

443.23 Billion

2025

2033

USD

300.00 Billion

USD

443.23 Billion

2025

2033

| 2026 - 2033 | |

| USD 300.00 Billion | |

| USD 443.23 Billion | |

| % | |

|

What is the Melioidosis Treatment Size and Growth Rate ?

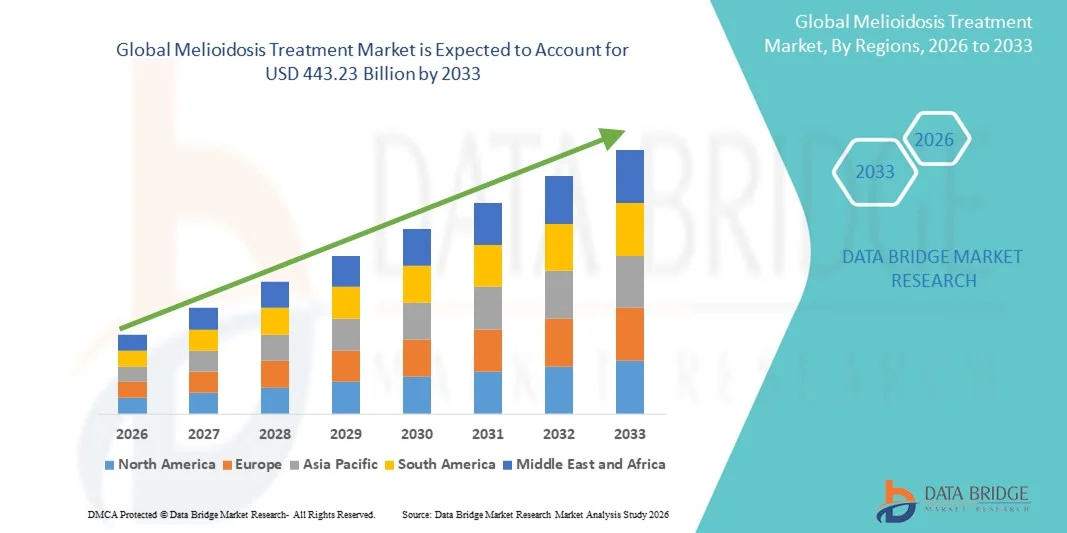

- As per Data Bridge Market Research Analysis the global Melioidosis Treatment market size was valued at USD 300.00 billion in 2025 and is expected to reach USD 443.23 billion by 2033, at a CAGR of 5.00 % during the forecast period

- The market growth is largely fueled by increasing awareness of Melioidosis, advancements in diagnostic facilities, and the expansion of healthcare infrastructure in both urban and rural areas

- Furthermore, rising demand for effective antibiotics, antitoxins, and supportive therapies for Melioidosis patients is driving the adoption of comprehensive treatment solutions. These converging factors are accelerating the uptake of Melioidosis Treatment solutions, thereby significantly boosting the industry's growth

Market Size & Forecast

- Global Market Value (2025): USD 300.00 billion in 2025

- Expected Market Value (2033): USD 443.23 billion by 2033

- Forecast CAGR (2026–2033): 5.00 %

Melioidosis Treatment Market Analysis

- Melioidosis Treatment, encompassing effective antibiotics, antitoxins, and supportive therapies, is increasingly critical in managing the disease in both endemic and non-endemic regions due to rising awareness, improved diagnostics, and the expansion of healthcare infrastructure

- The escalating demand for melioidosis treatment is primarily fueled by increasing incidence rates, growing awareness among healthcare professionals, and government initiatives to improve early detection and access to effective treatment

- North America dominated the melioidosis treatment market with the largest revenue share of 38.5% in 2025, supported by robust healthcare infrastructure, high awareness of rare infectious diseases, extensive access to antibiotics, and active research collaborations, with the U.S. leading due to specialized infectious disease centers and vaccination programs

- Asia-Pacific is expected to be the fastest-growing region in the melioidosis treatment market during the forecast period, projected to grow at a CAGR of 8.5% from 2026 to 2033, driven by increasing disease incidence, expansion of healthcare access, development of diagnostic and treatment facilities, and government initiatives for early detection and prevention in countries such as China, India, Japan, and South Korea

- The Bacterial Culture Test segment held the largest market revenue share of 48.6% in 2025, owing to its high specificity, reliability, and global acceptance as the gold standard for Melioidosis detection

Report Scope and Melioidosis Treatment Market Segmentation

|

Attributes |

Melioidosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Melioidosis Treatment?

Increasing Focus on Early Diagnosis and Combination Therapy

- A significant and accelerating trend in the global melioidosis treatment market is the growing emphasis on early diagnosis and optimized combination therapy protocols. Healthcare providers are increasingly integrating rapid diagnostic tests with established antibiotic regimens to reduce treatment initiation time and improve patient outcomes

- For instance, in 2023, hospitals in Southeast Asia implemented standardized protocols combining ceftazidime and meropenem with supportive care, leading to faster recovery rates and reduced complications

- Clinicians are focusing on personalized treatment strategies that include antibiotics, supportive therapy, and patient monitoring to minimize morbidity and ensure complete recovery

- Rising awareness among healthcare professionals regarding the importance of early intervention has led to more systematic approaches, ensuring faster response to infection and reduced fatality rates

- Research initiatives are exploring novel adjunctive therapies, including immunomodulators, to improve treatment effectiveness and limit hospital stays

- Implementation of new clinical guidelines and treatment frameworks in endemic regions is further standardizing patient care and optimizing clinical outcomes

- Enhanced availability of treatment kits and outreach programs in rural areas are contributing to wider accessibility and more timely management of Melioidosis

Melioidosis Treatment Market Dynamics

Driver

Increasing Burden of Melioidosis and Rising Awareness in Endemic Regions

- The rising prevalence of Melioidosis in Southeast Asia, Northern Australia, and other endemic regions, combined with increasing awareness among healthcare providers, is driving the demand for effective treatment protocols

- For instance, in March 2024, the Thai Ministry of Public Health initiated a national program to provide standardized antibiotic therapy and rapid diagnostic testing in rural hospitals, significantly improving patient access and outcomes

- Growing recognition of severe complications associated with delayed treatment, including septicemia and organ failure, has prompted hospitals to adopt intensive care protocols and combination therapy strategies

- Government-funded awareness campaigns and health worker training programs are helping communities recognize early symptoms, ensuring timely medical intervention

- Rising investment in disease surveillance and reporting infrastructure further supports the implementation of targeted treatment initiatives

- Increased availability of combination antibiotic therapies such as ceftazidime, meropenem, and trimethoprim-sulfamethoxazole in local healthcare facilities is contributing to faster adoption of standardized care practices

Restraint/Challenge

Limited Healthcare Infrastructure and High Treatment Costs in Remote Areas

- A key challenge to market growth is the limited healthcare infrastructure in remote and rural endemic areas, which restricts timely diagnosis and administration of effective therapies

- For instance, delayed presentation in remote parts of Northern Australia and Southeast Asia often leads to higher complication rates, making treatment less effective

- The relatively high cost of combination therapies, prolonged hospital stays, and intravenous administration can pose barriers for patients in low-income regions

- Supply chain constraints for essential antibiotics and limited availability of rapid diagnostic kits can delay treatment initiation and reduce overall efficacy

- In addition, lack of trained healthcare personnel in endemic regions restricts the implementation of standardized protocols and patient monitoring programs

- Addressing these challenges through enhanced healthcare infrastructure, subsidized treatment programs, training initiatives, and improved access to antibiotics will be crucial for sustained market growth

Melioidosis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Melioidosis Treatment market is segmented into Oral Antimicrobial, Intravenous Antibiotic, Eradication Phase, and Surgery. The Oral Antimicrobial segment dominated the largest market revenue share of 45.8% in 2025, driven by its convenience, widespread availability, and suitability for outpatient management. Oral antibiotics such as trimethoprim-sulfamethoxazole and doxycycline allow self-administration, reduce hospital visits, and are integrated into mass eradication programs in endemic regions. The market benefits from standardized dosing guidelines, physician familiarity, and patient preference for non-invasive therapy. Community-based distribution, school screening initiatives, and awareness campaigns further support adoption. Improved formulation stability, extended shelf-life, and low cost make oral antimicrobials the preferred choice in low-resource settings. The segment’s accessibility in rural and semi-urban areas contributes to its dominance, alongside strong governmental and NGO support for supply chains.

The Intravenous Antibiotic segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, due to increasing use of IV therapy in severe acute cases requiring hospitalization. IV-administered ceftazidime, meropenem, or imipenem are critical for early-stage septicemia management and reducing mortality. Hospitals and specialized clinics are increasingly equipped to administer IV therapy under close monitoring, supported by training programs for healthcare personnel. The fast adoption is driven by higher awareness of early diagnosis benefits, enhanced hospital infrastructure, and government-supported treatment protocols. Rising investment in acute care and increasing prevalence of severe cases in endemic regions are further propelling growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Bacterial Culture Test, Latex Fixation Test, Hemagglutination Assay, Immunofluorescence Matrix-Assisted Laser Desorption, Direct Fluorescent Antibody Test, and Others. The Bacterial Culture Test segment held the largest market revenue share of 48.6% in 2025, owing to its high specificity, reliability, and global acceptance as the gold standard for Melioidosis detection. The test supports early detection, timely antibiotic administration, and better patient management. Widespread laboratory adoption, training of clinical microbiologists, and inclusion in national guidelines further strengthen dominance. Its cost-effectiveness in endemic regions and integration into routine hospital protocols also contributes to its leading position. Community-level diagnostic programs, outbreak response protocols, and public health initiatives make bacterial culture the primary choice for both urban and rural healthcare settings. Hospitals and clinics leverage this method for accurate identification of Burkholderia pseudomallei, improving patient outcomes. Additionally, research institutions utilize bacterial culture tests for epidemiological studies and monitoring antimicrobial resistance trends. Partnerships between governmental health agencies and private diagnostic providers ensure continuous supply of reagents and laboratory equipment. The robustness, reproducibility, and reliability of the test enhance confidence among clinicians and patients, further reinforcing its market dominance.

The Direct Fluorescent Antibody Test segment is expected to witness the fastest CAGR of 18.7% from 2026 to 2033, due to its rapid turnaround time, high sensitivity, and applicability in field diagnostics. Increasing adoption in rural health centers, mobile clinics, and outbreak situations allows early identification and intervention. Government-supported rapid diagnostic initiatives, NGO-led awareness campaigns, and funding for mobile laboratories are boosting adoption. Point-of-care testing capabilities reduce the need for centralized laboratories and provide immediate results, enabling faster treatment decisions. Rapid training programs for health workers ensure consistent use in endemic areas. Emerging technology improvements enhance fluorescence signal stability and detection accuracy. Early detection allows reduction of severe cases and prevents complications. The test is particularly useful during outbreaks for immediate case identification. Integration with digital reporting tools and health management systems is increasing. High sensitivity and specificity make it suitable for both clinical and surveillance purposes. Public-private collaborations in endemic regions are expanding availability. Overall, this segment is increasingly adopted due to efficiency, reliability, and adaptability across healthcare settings.

- By Route of Administration

On the basis of route of administration, the market is segmented into Intramuscular, Intravenous, and Oral. The Oral route dominated the largest market revenue share of 46.3% in 2025, driven by convenience, ease of administration, and outpatient accessibility. Oral therapy is ideal for long-term eradication phase treatment, reducing hospital dependency. Community-based treatment programs and national eradication initiatives further support adoption. Patient preference for non-invasive administration, lower costs, and availability in rural pharmacies contribute to dominance. Oral formulations of trimethoprim-sulfamethoxazole and doxycycline are widely used in endemic regions due to safety and tolerability. School and workplace-based programs facilitate treatment adherence and follow-up. Easy storage, transport, and shelf-stable formulations enhance accessibility. Widespread awareness campaigns encourage self-administration for mild or moderate cases. Integration of oral therapy into national guidelines ensures standardized treatment. Physicians in outpatient settings rely on oral antibiotics to reduce hospital burden and manage high patient volumes. Pharmaceutical manufacturers focus on child-friendly and easy-to-swallow formulations to increase adoption.

The Intravenous route is expected to witness the fastest CAGR of 17.9% from 2026 to 2033, as IV administration is preferred for acute severe cases requiring hospital supervision. Improved infusion infrastructure, training, and inclusion of IV protocols in hospitals are driving growth. Rising prevalence of severe Melioidosis and adoption of standardized hospital protocols further support expansion. Hospitals and clinics provide critical care for septicemic patients using IV ceftazidime or meropenem. Continuous infusion techniques reduce complications and improve survival rates. Government health programs are funding IV treatment expansion in endemic zones. Adoption is further accelerated by clinical guidelines emphasizing early aggressive therapy. Advanced infusion devices and monitoring technologies ensure safe administration. Enhanced hospital capacities and ICU setups are enabling broader use. Training programs for nurses and clinicians reduce administration errors. Early IV therapy prevents complications, shortening hospitalization duration. Collaboration with pharmaceutical companies ensures availability of IV formulations in high-risk regions.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. Hospitals dominated the largest market revenue share of 55.1% in 2025, due to the availability of trained staff, intensive care facilities, IV therapy, and access to diagnostic services. Hospitals support acute and severe case management, eradication phase monitoring, and integration with national treatment programs. Centralized patient care, standardized guidelines, and inclusion in disease surveillance initiatives strengthen hospital dominance. Advanced diagnostic laboratories, antimicrobial stewardship programs, and specialized infection units contribute to hospitals’ market leadership. The presence of multidisciplinary teams ensures comprehensive patient management. Hospitals also participate in research and epidemiological studies, further consolidating their role. National health authorities often partner with hospitals to implement eradication and vaccination programs. Access to a wide range of therapeutic options enhances patient outcomes. Hospitals provide patient education and follow-up support. They also ensure availability of both oral and intravenous therapies. Well-established supply chains and bulk procurement capabilities enhance reliability. Hospitals play a key role in reducing mortality and morbidity associated with Melioidosis.

The Clinics segment is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, driven by expansion of outpatient care, follow-up programs, and community-level interventions. Clinics are increasingly offering oral antimicrobial therapy, screening services, and patient education, supporting early treatment and adherence. Community outreach, mobile health programs, and telemedicine support further drive adoption. Clinics enable early detection and preventive care in endemic regions. Partnerships with public health programs increase treatment coverage. Clinics facilitate rapid prescription refills and monitoring for adherence. Staff training ensures proper administration of medications. Focus on child and adult care enhances market penetration. Integration with local pharmacies improves treatment accessibility. Health education initiatives increase patient compliance. Clinics provide affordable and convenient treatment alternatives. Expansion into semi-urban and rural areas drives segment growth. Enhanced connectivity with hospitals ensures continuity of care and follow-up.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Retail Pharmacy segment dominated the largest market revenue share of 47.9% in 2025, owing to accessibility, patient familiarity, and consistent supply of antibiotics. Retail pharmacies support adherence through regular refills, counseling, and local availability. Widespread presence in both urban and semi-urban areas strengthens adoption. Continuous supply of first-line and second-line antibiotics ensures treatment continuity. Pharmacies often educate patients on correct dosage and adherence. Proximity to communities allows timely initiation of therapy. Collaboration with clinics and hospitals enhances distribution efficiency. Bulk procurement ensures availability in endemic regions. Retail pharmacies participate in public health campaigns. Trust in pharmacy staff reinforces patient confidence. Seasonal stock management ensures uninterrupted access. Availability of generic and branded drugs supports affordability. Retail pharmacies remain the preferred channel for outpatient therapy.

The Online Pharmacy segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by digital health adoption, home delivery services, and increasing patient preference for remote access, particularly in underserved or remote endemic regions. Enhanced e-commerce penetration, mobile applications, and telemedicine integrations contribute to fast adoption. Online platforms provide timely delivery, easy reordering, and adherence monitoring. Integration with patient health records ensures continuity of care. Expanding internet penetration and smartphone adoption enable wider reach. Teleconsultation services linked to online pharmacies enhance convenience. Emerging digital payment solutions facilitate seamless transactions. Direct-to-patient delivery reduces travel and associated costs. Awareness campaigns increase trust in online medicine procurement. Partnerships with logistics providers ensure prompt distribution. User-friendly platforms encourage repeat usage. Online pharmacies also expand access to rare or specialty medications.

Melioidosis Treatment Market Regional Analysis

- North America dominated the melioidosis treatment market with the largest revenue share of 38.5% in 2025

- Supported by robust healthcare infrastructure, high awareness of rare infectious diseases, extensive access to antibiotics, and active research collaborations

- The market leads the region due to specialized infectious disease centers, widespread vaccination programs, and the availability of advanced diagnostic and treatment facilities, ensuring timely and effective management of melioidosis cases

U.S. Melioidosis Treatment Market Insight

The U.S. Melioidosis Treatment market captured the largest revenue share in 2025 within North America, driven by well-established healthcare systems, increased patient awareness, and access to advanced antimicrobial therapies. The presence of specialized infectious disease centers, ongoing clinical research, and government-supported vaccination and awareness programs significantly bolster the market. Additionally, continuous investment in rapid diagnostic technologies and eradication-phase treatments contributes to the region’s dominance.

Europe Melioidosis Treatment Market Insight

The Europe melioidosis treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by strong healthcare infrastructure, increasing awareness of rare infectious diseases, and adoption of advanced antimicrobial and eradication therapies. Rising government initiatives, research collaborations, and increasing investment in infectious disease control are also contributing to growth. The market shows significant adoption across hospitals, clinics, and specialized treatment centers.

U.K. Melioidosis Treatment Market Insight

The U.K. melioidosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising awareness of infectious diseases, government health programs, and the availability of advanced treatment protocols. Increased patient access to clinics and hospitals equipped with diagnostic and therapeutic facilities further accelerates market growth. Public health campaigns and research initiatives focused on early detection and prevention are also key drivers.

Germany Melioidosis Treatment Market Insight

The Germany melioidosis treatment market is expected to expand at a considerable CAGR during the forecast period, supported by well-developed healthcare infrastructure, availability of specialized treatment centers, and increasing investments in research for rare infectious diseases. Government programs promoting early diagnosis and comprehensive antimicrobial therapy adoption further strengthen market growth. Hospitals and clinics are increasingly focusing on advanced intravenous and oral antimicrobial treatments, driving regional adoption.

Asia-Pacific Melioidosis Treatment Market Insight

The Asia-Pacific melioidosis treatment market is poised to grow at the fastest CAGR of 8.5% during the forecast period of 2026 to 2033, driven by rising disease incidence, expanding healthcare access, and government initiatives for early detection and prevention. Countries such as China, India, Japan, and South Korea are investing in diagnostic facilities, antimicrobial therapies, and vaccination programs to combat melioidosis. Increasing patient awareness and development of specialized infectious disease centers are further boosting market growth.

Japan Melioidosis Treatment Market Insight

The Japan melioidosis treatment market is witnessing growth due to improved healthcare infrastructure, rising awareness of melioidosis, and the increasing adoption of advanced antimicrobial therapies. Government health initiatives and specialized infectious disease centers enhance early detection and treatment, supporting market expansion. An aging population and urbanized regions are driving demand for hospital-based treatment facilities and eradication-phase therapies.

China Melioidosis Treatment Market Insight

The China melioidosis treatment market accounted for the largest revenue share in Asia-Pacific in 2025, owing to the country’s growing healthcare infrastructure, rising awareness of rare infectious diseases, and expanding access to antibiotics and specialized treatment centers. Government-led programs for early detection, increased patient awareness, and growing investment in diagnostic and therapeutic facilities are key factors propelling market growth.

Which are the Top Companies in Melioidosis Treatment?

The Melioidosis Treatment industry is primarily led by well-established companies, including:

- Cipla (India)

- Sun Pharmaceutical (India)

- Novartis (Switzerland)

- Pfizer (U.S.)

- Gilead Sciences (U.S.)

- Roche (Switzerland)

- GlaxoSmithKline (U.K.)

- AstraZeneca (U.K.)

- Bayer (Germany)

- Sanofi (France)

- Janssen Pharmaceuticals (Belgium)

- Abbott (U.S.)

- Chemo Group (Australia)

- Takeda Pharmaceutical (Japan)

- Biocon (India)

- Fresenius Kabi (Germany)

- Amgen (U.S.)

- Hikma Pharmaceuticals (Jordan)

- Cadila Healthcare (India)

Latest Developments in Global Melioidosis Treatment Market

- In December 2024, researchers funded by the National Institute of Allergy and Infectious Diseases (NIAID) developed a new rapid diagnostic test for melioidosis that delivers results in about 15 minutes from just a drop of blood or serum. The immunochromatographic “Rapid Melioidosis” test detects antibodies to the Hcp1 antigen of B. pseudomallei, and is commercially available in parts of Southeast Asia under a licensed name

- In May 2025, a severe melioidosis outbreak was reported in northeastern Queensland, Australia, linked to extreme flooding. Medscape reported over 200 cases and dozens of deaths, highlighting how climate events are driving surges in infection risk and stressing health systems

- In October 2025, the WHO released a major report highlighting that despite global antimicrobial‑resistance (AMR) challenges, the pipeline of new antibacterial agents—including those potentially relevant to melioidosis—is dwindling. The report calls for greater investment in both novel antibiotics and diagnostics

- In September 2025, a case report was published (European Society of Medicine) about a melioidosis patient in Western Europe, bringing attention to the fact that melioidosis is increasingly recognized outside traditional tropical regions. This underscores the need for better clinical awareness and diagnostic capacity globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.