Global Menin Inhibitor Drug Market

Market Size in USD Million

USD

618.00 Million

USD

2,747.16 Million

2025

2033

USD

618.00 Million

USD

2,747.16 Million

2025

2033

| 2026 - 2033 | |

| USD 618.00 Million | |

| USD 2,747.16 Million | |

| % | |

|

Menin Inhibitor Drug Market Overview

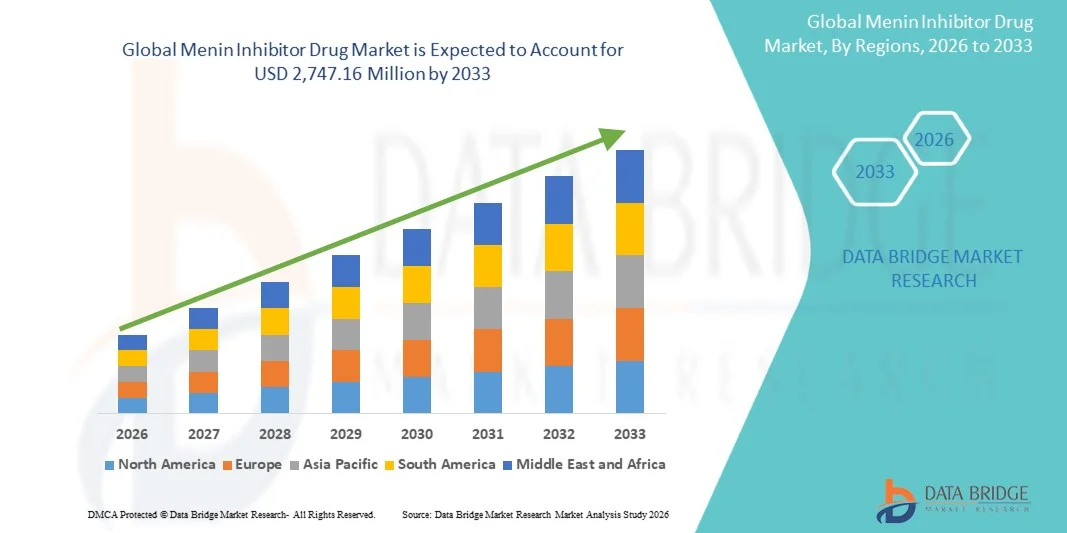

The global menin inhibitor drug market was valued at USD 618.00 million in 2025 and is projected to reach USD 2,747.16 million by 2033, growing at a CAGR of 20.50% from 2026 to 2033. The market is witnessing rapid expansion driven by increasing prevalence of acute leukemias such as AML and ALL, strong clinical pipeline activity, and growing adoption of targeted oncology therapies.

The rising burden of genetically defined hematologic malignancies, particularly KMT2A-rearranged and NPM1-mutated acute myeloid leukemia, is accelerating demand for novel precision treatments. Breakthrough advances in small-molecule drug development, combined with favorable regulatory designations such as orphan drug status and fast-track approvals, are supporting faster commercialization. In addition, expanding use of combination therapies with BCL-2 and FLT3 inhibitors is improving treatment outcomes, further driving market adoption across oncology hospitals and specialized cancer centers.

Key Market Trends & Insights

- North America dominated the global menin inhibitor drug market with the largest revenue share of 48.12% in 2025, supported by strong clinical trial activity, early regulatory approvals, and advanced oncology treatment infrastructure.

- The Single-Agent Menin Inhibitors segment led the market with a 46.28% share in 2025, driven by strong clinical progress of targeted monotherapy agents in relapsed/refractory AML and NPM1-mutated leukemia.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 18.6% from 2026 to 2033, fueled by rising leukemia incidence, expanding oncology access, and increasing clinical research participation in China, India, and Japan.

- Combination Menin Inhibitors are the fastest-growing drug type, projected to register a CAGR of 8.4%, reflecting increasing clinical evidence that combining menin inhibitors with other targeted therapies improves response depth and durability.

- The Acute Myeloid Leukemia (AML) segment dominated the indication type category with a 52.63% revenue share in 2025, led by strong prevalence of genetically defined subtypes such as KMT2A-rearranged AML and NPM1-mutated AML. AML represents the primary clinical focus for menin inhibitors

- Oral segment accounted for 71.84% of the market, preferred by development of orally bioavailable small molecule inhibitors such as revumenib and ziftomenib, which allow convenient outpatient administration.

- The Acute Lymphoblastic Leukemia (ALL) segment is the fastest-growing indication category, with a CAGR of 9.1%, driven by increasing exploration of menin inhibitors in KMT2A-rearranged ALL cases, particularly in pediatric and young adult populations

Market Size & Forecast

- Global Market Value (2025): USD 618.00 Million

- Expected Market Value (2033): USD 2,747.16 Million

- Forecast CAGR (2026–2033): 20.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Menin Inhibitor Drug Market Segmentation

|

Attributes |

Menin Inhibitor Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Syndax Pharmaceuticals, Inc. (U.S.) · Kura Oncology, Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Novartis AG (Switzerland) · Daiichi Sankyo Company, Limited (Japan) · Sumitomo Pharma Co., Ltd. (Japan) · Boehringer Ingelheim International GmbH (Germany) · AbbVie Inc. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · AstraZeneca (U.K.) · Amgen Inc. (U.S.) · Pfizer Inc. (U.S.) · Bristol Myers Squibb (U.S.) · Merck & Co., Inc. (U.S.) · Sanofi (France) · GSK plc (U.K.) · Jazz Pharmaceuticals plc (Ireland) · Otsuka Holdings Co., Ltd. (Japan) · Kyowa Kirin Co., Ltd. (Japan) · BeiGene, Ltd. (China) |

|

Market Opportunities |

· Expansion of menin inhibitors into genetically defined subsets beyond AML · Growing adoption of combination regimens with FLT3, IDH, and BCL-2 inhibitors · Increasing orphan drug designations and accelerated regulatory pathways |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global Menin Inhibitor Drug Market Trends

Trend: Expansion in Precision Oncology & Targeted Leukemia Therapies

The global menin inhibitor drug market is witnessing strong momentum driven by precision oncology adoption, particularly in genetically defined acute leukemias such as KMT2A-rearranged and NPM1-mutated AML. Drug developers are advancing menin-KMT2A pathway inhibitors such as revumenib (SNDX-5613, Syndax Pharmaceuticals) and ziftomenib (KO-539, Kura Oncology), which have shown promising responses in relapsed/refractory patient populations. A key milestone includes the progression of AUGMENT-101 (revumenib) clinical trial, which demonstrated clinically meaningful remission rates in heavily pretreated leukemia cases. The recent regulatory advancement of revumenib (approved as Revuforj in 2024 for KMT2A-rearranged acute leukemia) further reflects accelerating clinical validation. Increasing integration of biomarker-driven patient selection and combination strategies with chemotherapy and targeted agents is strengthening treatment precision and improving therapeutic durability.

Global Menin Inhibitor Drug Market Dynamics

Key Market Driver: Rising Prevalence of Genetically Defined Acute Leukemia Subtypes

The rising incidence of molecularly characterized leukemias, particularly KMT2A-rearranged AML and NPM1-mutant AML, is a major driver for menin inhibitor adoption. These therapies are being developed to address high unmet needs in relapsed/refractory cases where conventional regimens show limited survival benefit. For instance, revumenib (Syndax Pharmaceuticals) has been evaluated in pediatric and adult populations with KMT2A-rearranged leukemia showing measurable complete remission rates, while Kura Oncology’s ziftomenib is being studied in the KOMET-001 trial for NPM1-mutant AML. The expanding use of next-generation sequencing in routine oncology diagnostics is further enabling early identification of eligible patients, increasing clinical trial enrollment and accelerating commercial demand.

Key Restraint/Challenge: Clinical Complexity and Safety Profile Uncertainty

A significant challenge in this market is the complexity of validating long-term safety, resistance patterns, and optimal dosing strategies in transcriptional regulation-targeting agents. Menin inhibitors such as revumenib and ziftomenib have shown promising efficacy, but clinical trials have also reported adverse events such as differentiation syndrome and QT prolongation, requiring careful monitoring. In addition, the relatively small patient pool for genetically defined subtypes limits large-scale randomized studies, as seen in early-phase trials such as AUGMENT-101 and KOMET-001, leading to extended development timelines and higher R&D costs. Resistance mutations emerging in the menin-binding pathway further complicate long-term treatment durability and sequencing strategies.

Key Market Opportunity: Expansion into Combination Therapies and Broader Hematologic Indications

The major opportunity lies in expanding menin inhibitors into combination regimens to improve remission depth and delay resistance. Ongoing studies are evaluating revumenib combined with venetoclax (BCL-2 inhibitor) and FLT3 inhibitors in relapsed AML settings, aiming to enhance synergistic anti-leukemic effects. Similarly, ziftomenib is being explored in combination with standard induction chemotherapy to improve first-line outcomes in NPM1-mutated AML. Beyond AML, research is also expanding into other transcriptionally driven hematologic malignancies, including mixed-lineage leukemias. The use of adaptive trial designs and accelerated regulatory pathways, supported by breakthrough designations for drugs such as revumenib, is expected to further broaden clinical applications and market penetration.

Global Menin Inhibitor Drug Market Scope

The menin inhibitor drug market is segmented on the basis of drug type, indication, route of administration, and end user.

- By Drug Type

On the basis of drug type, the global menin inhibitor drug market is segmented into single-agent menin inhibitors, combination menin inhibitors, small molecule inhibitors, and biologics. The Single-Agent Menin Inhibitors segment dominated the market with a 46.28% share in 2025, driven by strong clinical progress of targeted monotherapy agents such as revumenib (Syndax Pharmaceuticals) and ziftomenib (Kura Oncology) in relapsed/refractory AML and NPM1-mutated leukemia. These therapies are specifically designed to disrupt the menin-KMT2A interaction pathway, which plays a central role in leukemogenesis. Their dominance is supported by early clinical success in achieving measurable remission in heavily pretreated patient populations. Regulatory momentum, including accelerated approval pathways for first-in-class agents, has further strengthened adoption. Simpler treatment protocols and clearer biomarker-based patient selection also support their widespread clinical use. However, resistance development and limited durability of response continue to encourage future shift toward combination strategies.

The Combination Menin Inhibitors segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by increasing clinical evidence that combining menin inhibitors with other targeted therapies improves response depth and durability. Ongoing studies evaluating revumenib + venetoclax (BCL-2 inhibitor) and ziftomenib + FLT3 inhibitors in AML are showing promising synergistic effects in overcoming resistance mechanisms. Combination approaches are particularly important in relapsed/refractory cases where monotherapy response duration is limited. Pharmaceutical companies are increasingly investing in adaptive trial designs to optimize combination regimens. Rising adoption of precision medicine frameworks is enabling more personalized therapy selection. Expanding pipeline collaborations between biotech firms and large oncology players is further accelerating development in this segment.

- By Indication

On the basis of indication, the global menin inhibitor drug market is segmented into acute myeloid leukemia (AML), acute lymphoblastic leukemia (ALL), other hematologic malignancies, and solid tumors. The Acute Myeloid Leukemia (AML) segment dominated the market with a 52.63% share in 2025, driven by strong prevalence of genetically defined subtypes such as KMT2A-rearranged AML and NPM1-mutated AML. AML represents the primary clinical focus for menin inhibitors, with drugs such as revumenib and ziftomenib showing significant efficacy in relapsed/refractory cases. High unmet need in AML due to poor survival outcomes with conventional chemotherapy is a major growth driver. Increasing adoption of genomic profiling is enabling earlier identification of eligible patients for targeted therapy. Regulatory breakthroughs and fast-track designations for AML treatments are further accelerating commercialization. Continuous clinical trial expansion in AML populations reinforces its dominance in this segment.

The Acute Lymphoblastic Leukemia (ALL) segment is expected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing exploration of menin inhibitors in KMT2A-rearranged ALL cases, particularly in pediatric and young adult populations. Early-stage clinical studies are investigating revumenib for relapsed/refractory ALL patients showing encouraging response signals. ALL presents a strong opportunity due to the high incidence of aggressive genetic subtypes with limited treatment options. Expanding use of next-generation sequencing in pediatric oncology is improving early detection rates. Growing interest in combination regimens with chemotherapy backbones is further enhancing therapeutic potential. Increased regulatory focus on rare pediatric leukemias is also supporting faster clinical development in this segment.

- By Route Of Administration

On the basis of route of administration, the global menin inhibitor drug market is segmented into oral and intravenous formulations. The Oral segment dominated the market with a 71.84% share in 2025, largely due to the development of orally bioavailable small molecule inhibitors such as revumenib and ziftomenib, which allow convenient outpatient administration. Oral therapy significantly improves patient compliance, especially in long-term treatment settings for AML maintenance and relapse management. It reduces hospitalization requirements and lowers overall treatment burden on healthcare systems. Pharmaceutical developers are prioritizing oral formulations to support chronic administration strategies in hematologic cancers. Increasing shift toward home-based cancer care and outpatient oncology models is further strengthening this segment.

The Intravenous segment is projected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by early-phase clinical studies of combination regimens and biologic-enhanced delivery approaches requiring controlled infusion settings. IV administration is often preferred in initial dose-escalation phases to ensure safety monitoring in high-risk patients. Hospital-based oncology centers are increasingly adopting IV protocols for combination therapies involving menin inhibitors and chemotherapy agents. Advanced infusion technologies and improved supportive care infrastructure are supporting this segment’s expansion. In addition, IV formulations are being explored for future next-generation menin-targeting biologics with enhanced pharmacokinetic control.

- By End User

On the basis of end user, the global menin inhibitor drug market is segmented into hospitals & oncology centers, specialty clinics, research & academic institutes, and pharmacies & specialty distributors. The Hospitals & Oncology Centers segment dominated the market with a 58.92% share in 2025, driven by high patient inflow for acute leukemia diagnosis and treatment. These centers serve as primary hubs for administering menin inhibitors such as revumenib and ziftomenib, especially in relapsed/refractory AML cases requiring intensive monitoring. Availability of advanced diagnostic infrastructure, including genomic sequencing and molecular profiling, supports early patient identification. Hospitals also play a key role in clinical trial enrollment and post-approval treatment adoption. Increasing integration of precision oncology departments within tertiary care hospitals is further strengthening dominance.

The Research & Academic Institutes segment is expected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033, driven by expanding clinical trials, translational research, and drug discovery programs focused on epigenetic and transcription factor-targeting therapies. Institutions such as leading cancer research centers are heavily involved in evaluating menin inhibitors in early-phase studies and combination regimens. Increasing government and private funding for hematologic cancer research is supporting innovation. Academic collaborations with biotech firms are accelerating biomarker discovery and patient stratification techniques. Growing focus on rare genetic leukemia subtypes is also expanding research activity. These institutes are critical for advancing next-generation therapeutic strategies and expanding clinical indications beyond AML.

Global Menin Inhibitor Drug Market Regional Analysis

North America dominated the global menin inhibitor drug market with the largest revenue share of 48.12% in 2025, supported by strong clinical trial activity, early regulatory approvals, and advanced oncology treatment infrastructure.The region benefits from early adoption of precision medicine, widespread use of next-generation sequencing for leukemia diagnosis, and rapid integration of targeted therapies in clinical practice. Strong regulatory support from agencies such as the U.S. FDA, including breakthrough therapy designations and accelerated approval pathways, has further accelerated market entry of menin inhibitors. High prevalence of acute myeloid leukemia (AML) and well-established clinical trial networks continue to drive strong patient enrollment and therapy uptake. Increasing investment in hematologic cancer R&D and combination therapy studies is further strengthening North America’s leadership position in the global market.

U.S. Menin Inhibitor Drug Market Insight

The U.S. menin inhibitor drug market is witnessing strong growth due to the country’s leadership in hematologic oncology research, high prevalence of acute myeloid leukemia (AML), and rapid adoption of precision medicine approaches. The presence of major biotech developers such as Syndax Pharmaceuticals (revumenib) and Kura Oncology (ziftomenib) is accelerating clinical advancement and commercialization of first-in-class menin-targeting therapies. Strong FDA support through breakthrough therapy designations and accelerated approval pathways is significantly reducing time-to-market for innovative drugs. In addition, widespread use of next-generation sequencing in routine cancer diagnostics is improving early identification of KMT2A-rearranged and NPM1-mutated leukemia patients. Extensive clinical trial infrastructure and high investment in combination therapy research are further strengthening market expansion across the country.

Europe Menin Inhibitor Drug Market Insight

The Europe menin inhibitor drug market remains a major contributor to global growth, driven by strong academic research networks, advanced oncology infrastructure, and increasing focus on precision medicine. Countries such as Germany, France, and the U.K. are actively participating in clinical trials evaluating menin inhibitors for AML and ALL. Regulatory frameworks under the European Medicines Agency (EMA) are increasingly supporting orphan drug designations and accelerated pathways for rare hematologic cancers. High adoption of genomic profiling in leukemia diagnosis is improving patient stratification and treatment access. Growing collaborations between pharmaceutical companies and academic institutions are further accelerating clinical development and regional market penetration.

U.K. Menin Inhibitor Drug Market Insight

The U.K. menin inhibitor drug market is expanding steadily due to strong clinical research capabilities, NHS-supported cancer care infrastructure, and active participation in early-phase oncology trials. Leading research centers are contributing significantly to studies evaluating menin inhibitors such as revumenib in relapsed/refractory leukemia cases. The country’s focus on precision medicine and widespread use of genomic testing is enabling faster identification of eligible patients. Supportive regulatory pathways through the Medicines and Healthcare products Regulatory Agency (MHRA) are facilitating clinical development. In addition, collaborations between biotech firms and academic institutes are strengthening innovation in epigenetic and transcription-targeted therapies.

Germany Menin Inhibitor Drug Market Insight

The Germany menin inhibitor drug market is growing steadily, supported by a strong pharmaceutical manufacturing base, advanced cancer research institutions, and increasing adoption of targeted oncology therapies. Major university hospitals are actively involved in clinical trials for menin inhibitors in AML and other hematologic malignancies. The country’s well-developed healthcare system and emphasis on precision diagnostics are improving early disease detection and treatment access. Strong government funding for oncology research and participation in EU-wide clinical networks are further supporting market expansion. Increasing focus on combination therapies and translational research is strengthening Germany’s position in the European market.

Asia-Pacific Menin Inhibitor Drug Market Insight

The Asia-Pacific menin inhibitor drug market is expected to witness rapid growth due to rising cancer burden, expanding healthcare infrastructure, and increasing adoption of precision medicine. Countries such as China, Japan, and India are investing heavily in genomic diagnostics and advanced oncology research. Growing participation in global clinical trials for AML therapies is improving access to novel drugs in the region. Pharmaceutical companies are increasingly collaborating with regional research institutions to accelerate development of targeted therapies. However, limited early access to advanced diagnostics in some emerging economies remains a challenge.

Japan Menin Inhibitor Drug Market Insight

The Japan menin inhibitor drug market is witnessing steady growth driven by strong clinical research capabilities, high adoption of advanced cancer diagnostics, and government support for innovative drug development. Japanese oncology centers are actively participating in global trials evaluating menin inhibitors for AML and ALL. The country’s focus on precision medicine and integration of next-generation sequencing in routine practice is improving patient identification. Regulatory efficiency under the Pharmaceuticals and Medical Devices Agency (PMDA) is supporting faster approval of novel therapies. Increasing collaboration between domestic pharmaceutical firms and global biotech companies is further enhancing market development.

China Menin Inhibitor Drug Market Insight

The China menin inhibitor drug market is growing rapidly due to increasing incidence of leukemia, expanding biotechnology sector, and strong government support for innovative drug development. Domestic pharmaceutical companies are increasingly collaborating with global players to advance clinical research on menin-KMT2A targeted therapies. Rapid expansion of genomic testing capabilities is improving early detection of AML and NPM1-mutated cases. Government initiatives supporting oncology innovation and accelerated approval pathways are further boosting market growth. In addition, rising investment in hospital infrastructure and clinical trial networks is positioning China as a key emerging market for menin inhibitor therapies globally.

Global Menin Inhibitor Drug Market Share

The Menin Inhibitor Drug industry is primarily led by well-established companies, including:

- Syndax Pharmaceuticals, Inc. (U.S.)

- Kura Oncology, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Novartis AG (Switzerland)

- Daiichi Sankyo Company, Limited (Japan)

- Sumitomo Pharma Co., Ltd. (Japan)

- Boehringer Ingelheim International GmbH (Germany)

- AbbVie Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- AstraZeneca (U.K.)

- Amgen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Jazz Pharmaceuticals plc (Ireland)

- Otsuka Holdings Co., Ltd. (Japan)

- Kyowa Kirin Co., Ltd. (Japan)

- BeiGene, Ltd. (China)

Latest Developments in Global Menin Inhibitor Drug Market

- In November 2025, the U.S. Food and Drug Administration (FDA) approved ziftomenib (Komzifti, Kura Oncology) for adult patients with relapsed or refractory acute myeloid leukemia (AML) with a susceptible NPM1 mutation, marking it as a second major menin inhibitor approval in this indication. The approval was supported by the KOMET-001 clinical trial, which demonstrated clinically meaningful response rates in heavily pretreated patients. This milestone significantly expanded the commercial presence of menin inhibitors in precision oncology and strengthened competition within the AML treatment landscape. The therapy is administered orally once daily, improving outpatient cancer care accessibility and reinforcing the shift toward targeted epigenetic therapies in hematologic malignancies

- In November 2025, Kura Oncology announced the FDA approval of ziftomenib following Priority Review for relapsed/refractory NPM1-mutated AML patients, based on results from the Phase 2 KOMET-001 trial. The study demonstrated approximately 20–23% complete remission rates and strong minimal residual disease (MRD) negativity among responders, highlighting significant clinical efficacy in genetically defined AML. This development positioned ziftomenib as a key competitive therapy alongside revumenib in the growing menin inhibitor class. It also validated NPM1 mutation targeting as a clinically actionable pathway in AML treatment strategies

- In October 2025, the FDA expanded approval of revumenib (Revuforj, Syndax Pharmaceuticals) to include relapsed or refractory AML patients with NPM1 mutations, following its earlier approval in 2024 for KMT2A-rearranged acute leukemia. This expansion marked a major advancement in broadening the eligible patient population for menin-targeted therapy, covering a significantly larger subset of AML cases. The decision was supported by clinical data from the AUGMENT-101 trial demonstrating durable responses in genetically defined leukemia subtypes. This development reinforced revumenib as the first-in-class menin inhibitor with multiple approved indications in acute leukemia treatment

- In November 2024, the FDA granted initial approval to revumenib (Revuforj, Syndax Pharmaceuticals) for the treatment of relapsed or refractory acute leukemia with KMT2A translocation in adult and pediatric patients aged one year and older. This marked the first-ever regulatory approval of a menin inhibitor, establishing a new targeted drug class in hematologic oncology. The approval was based on clinical trial evidence showing meaningful remission rates in heavily pretreated leukemia patients. This event represented a breakthrough in epigenetic targeting therapies and opened the pathway for rapid development of additional menin inhibitors across AML and ALL indications

- In November 2024, early clinical breakthroughs and regulatory progress established menin inhibitors as a transformative oncology class, with revumenib achieving first-in-class approval and multiple pipeline candidates such as ziftomenib, bleximenib, and enzomenib advancing into late-stage clinical trials. These developments were supported by increasing evidence of strong anti-leukemic activity in KMT2A-rearranged and NPM1-mutated AML patients. The period marked a rapid acceleration of research investment, clinical trial expansion, and pharmaceutical collaborations focused on epigenetic targeting mechanisms in leukemia therapy. This phase laid the foundation for subsequent multi-indication approvals in 2025

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.