Global Merkel Cell Carcinoma Treatment Market

Market Size in USD Billion

CAGR :

%

USD

3.77 Billion

USD

5.10 Billion

2025

2033

USD

3.77 Billion

USD

5.10 Billion

2025

2033

| 2026 –2033 | |

| USD 3.77 Billion | |

| USD 5.10 Billion | |

| % | |

|

Merkel Cell Carcinoma Treatment Market Size

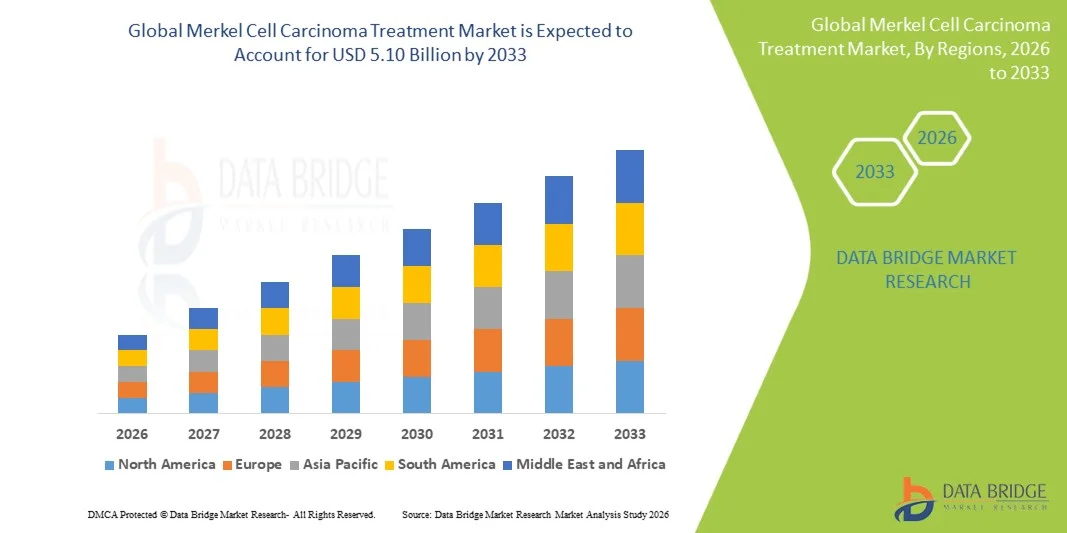

- The global Merkel Cell Carcinoma Treatment market size was valued at USD 3.77billion in 2025 and is expected to reach USD 5.10 billion by 2033, at a CAGR of 3.87% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within checkpoint immunotherapy platforms and novel targeted oncology approaches, leading to increased treatment options and improved survival outcomes in this rare and aggressive cutaneous malignancy

- Furthermore, rising demand for effective, well-tolerated, and durable treatment solutions for Merkel cell carcinoma across both localized and metastatic disease settings is establishing checkpoint inhibitor-based immunotherapy as the modern standard of oncological care. These converging factors are accelerating the uptake of Merkel Cell Carcinoma Treatment solutions, thereby significantly boosting the industry's growth

Merkel Cell Carcinoma Treatment Market Analysis

- Merkel cell carcinoma (MCC) treatments, offering immunotherapy-based and cytotoxic therapeutic options for this rare neuroendocrine skin cancer associated with Merkel cell polyomavirus (MCPyV) and UV-induced DNA mutations, are increasingly vital components of modern dermatologic and oncologic care pathways due to their improved efficacy over historical chemotherapy-based approaches and seamless alignment with the broader precision immuno-oncology paradigm

- The escalating demand for Merkel cell carcinoma treatments is primarily fueled by rising MCC incidence driven by an aging and increasingly immunocompromised global population, expanding regulatory approvals for checkpoint inhibitor therapies, and a growing preference for immunotherapy-based approaches that offer durable long-term disease control

- North America dominated the merkel cell carcinoma treatment market with the largest revenue share of 44.60% in 2025, characterized by the highest absolute incidence of MCC globally, early adoption of anti-PD-1/PD-L1 checkpoint inhibitors, and a strong network of academic dermatologic oncology programs with MCC treatment expertise

- Asia-Pacific is expected to be the fastest growing region in the merkel cell carcinoma treatment market during the forecast period due to increasing MCC incidence driven by growing aging populations and rising UV radiation exposure awareness in countries such as Australia, Japan, and China

- The Parenteral segment accounted for the largest market revenue share of 62.3% in 2025, primarily due to the high usage of intravenous immunotherapies and chemotherapy drugs that require direct bloodstream administration for rapid and effective action

Report Scope and Merkel Cell Carcinoma Treatment Market Segmentation

|

Attributes |

Merkel Cell Carcinoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Merck & Co. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Merkel Cell Carcinoma Treatment Market Trends

“Neoadjuvant Immunotherapy Transforming Surgical Outcomes in Resectable MCC”

- A significant and accelerating trend in the global Merkel Cell Carcinoma Treatment market is the growing investigation and clinical adoption of neoadjuvant checkpoint inhibitor immunotherapy prior to surgery in patients with resectable localized and regional MCC. This emerging treatment strategy is significantly enhancing pathological response rates, potentially enabling organ-sparing surgical approaches and improving long-term disease control compared to surgery-first management

- For Instance, the STAMP trial investigating neoadjuvant pembrolizumab in resectable Stage I-III MCC has demonstrated pathological complete response rates exceeding 47% in MCPyV-positive tumors, providing compelling early evidence that neoadjuvant immunotherapy may fundamentally reshape the surgical management paradigm for early-stage MCC

- Neoadjuvant immunotherapy in MCC treatment enables features such as in vivo immune priming through systemic immune activation against tumor antigens, real-time assessment of tumor immunosensitivity through pathological response evaluation, and potential reduction in surgical morbidity through tumor downstaging. These mechanisms have demonstrated superior early relapse-free survival outcomes compared to historical surgery-first approaches in retrospective comparative analyses showing improvements of up to 43%

- The seamless integration of neoadjuvant immunotherapy protocols with multidisciplinary MCC treatment teams encompassing dermatologic surgeons, radiation oncologists, and medical oncologists facilitates coordinated treatment planning and delivery across all disease stages. Through integrated tumor board platforms, MCC specialists can comprehensively manage treatment sequencing, response assessment imaging, and adjuvant therapy decisions

- This trend towards perioperative immunotherapy integration is fundamentally reshaping the surgical oncology management paradigm for resectable MCC, moving beyond the traditional surgery-first approach. Consequently, companies such as Merck & Co. and Pfizer are investing in prospective clinical trial programs evaluating both neoadjuvant and adjuvant checkpoint inhibitor strategies in early-stage MCC

- The demand for MCC treatments incorporating perioperative immunotherapy frameworks is growing rapidly across academic dermatologic oncology centers globally, as multidisciplinary MCC treatment teams increasingly prioritize maximizing long-term disease control and minimizing surgical extent

Merkel Cell Carcinoma Treatment Market Dynamics

Driver

“Growing Need Due to Rising MCC Incidence and Transformative Immunotherapy Clinical Outcomes”

- The increasing global incidence of Merkel cell carcinoma, with approximately 3,000 new cases diagnosed annually in the U.S. alone and incidence rising at approximately 8% per year driven by the aging population, increasing immunosuppression prevalence, and cumulative UV radiation exposure, is a significant driver for the heightened demand for effective MCC treatment options

- For Instance, in February 2025, Pfizer reported updated 5-year long-term follow-up data from the JAVELIN Merkel 200 trial confirming durable overall survival benefit for avelumab in previously treated metastatic MCC, with 26.0% of patients alive at 5 years versus less than 5% historical expectations with chemotherapy, reinforcing the transformative long-term survival impact of immunotherapy in this aggressive malignancy. Such strategies by key companies are expected to drive the Merkel Cell Carcinoma Treatment industry growth in the forecast period

- As dermatologists and oncologists become increasingly aware of the MCC incidence trajectory and the available immunotherapy treatment options, MCC therapeutics offer historically unprecedented durable response rates, long-term survival benefits, and a manageable safety profile that dramatically outperforms conventional chemotherapy

- Furthermore, the growing diagnostic awareness of MCC among dermatologists and pathologists, combined with improved access to specialized immunohistochemistry and MCPyV serology testing, is reducing diagnostic delays and enabling earlier initiation of effective immunotherapy treatment in newly diagnosed patients

- The relative accessibility of checkpoint inhibitor treatment for MCC patients through established reimbursement pathways for approved indications, combined with increasing clinical guideline recognition of immunotherapy as first-line standard of care, is driving consistent adoption growth across both academic and community oncology settings

Restraint/Challenge

“Rare Disease Diagnosis Delays and Limited Treatment Access in Emerging Markets”

- The significant diagnostic challenge posed by MCC's rarity, clinical mimicry of more common skin tumors, and requirement for specialized pathological confirmation creates diagnostic delays averaging three to six months in non-specialist settings, limiting timely treatment initiation. In addition, restricted access to approved checkpoint inhibitor therapies in many emerging and lower-income healthcare markets represents a substantial challenge to equitable global treatment access

- For Instance, avelumab and pembrolizumab are approved for MCC treatment in fewer than 30 countries globally, with reimbursement coverage secured in an even more limited subset of markets, meaning that the majority of the global MCC patient population lacks formal access to immunotherapy that has transformed outcomes in approved markets

- Addressing these access and awareness challenges through dermatologist education programs, pathology training initiatives, and targeted health technology assessment submissions in additional markets is crucial for expanding global access to effective MCC immunotherapy. Companies such as Merck & Co. and Pfizer have established dedicated MCC patient support programs and physician education initiatives to improve diagnostic recognition and treatment access

- In addition, the rarity of MCC significantly constrains clinical trial recruitment, limiting the scope and power of clinical evidence generation required to support regulatory approvals for novel therapeutic modalities beyond checkpoint inhibitors, creating a challenging regulatory pathway for emerging MCC treatment candidates

- Overcoming these challenges through enhanced diagnostic educational programs, expanded orphan drug designation strategies, and novel clinical trial designs optimized for rare oncology indications will be vital for sustained market growth

Merkel Cell Carcinoma Treatment Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

• By Treatment Type

On the basis of treatment type, the Merkel Cell Carcinoma Treatment market is segmented into Immunotherapy, Chemotherapy, and Others. The Immunotherapy segment dominated the largest market revenue share of around 48.6% in 2025, driven by the strong clinical efficacy of immune checkpoint inhibitors such as PD-1/PD-L1 inhibitors in improving survival outcomes in advanced Merkel cell carcinoma. Rising preference for targeted immune modulation therapies over conventional cytotoxic drugs has significantly strengthened adoption across oncology centers. Increasing regulatory approvals and inclusion in treatment guidelines further support segment dominance. Growing awareness among clinicians regarding durable response rates and reduced relapse risk also contributes to uptake. Expansion of biologics manufacturing capabilities and oncology drug pipelines has enhanced treatment accessibility. Pharmaceutical companies are investing heavily in next-generation immuno-oncology combinations, further reinforcing market leadership. Favorable reimbursement policies in developed regions are also accelerating adoption. Overall, Immunotherapy held the highest share due to improved patient outcomes and precision targeting.

The Chemotherapy segment is expected to witness the fastest growth rate of 15.9% CAGR from 2026 to 2033, driven by its continued role in combination regimens and treatment of advanced or refractory cases. Despite the rise of immunotherapy, chemotherapy remains essential in cost-sensitive healthcare systems where affordability is a key factor. Its widespread availability in hospital oncology settings ensures steady utilization across developing regions. Increasing use in combination with immunotherapy is improving therapeutic effectiveness and driving renewed clinical relevance. Ongoing research in dose optimization and reduced toxicity formulations is enhancing patient tolerance. Rising cancer burden globally is further increasing demand for conventional treatment options. Hospitals continue to rely on chemotherapy as a first-line or adjunct therapy in multiple cases. Expanding generic drug availability is also supporting market growth. Overall, chemotherapy growth is sustained by accessibility and combination-based treatment strategies.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, and Others. The Parenteral segment accounted for the largest market revenue share of 62.3% in 2025, primarily due to the high usage of intravenous immunotherapies and chemotherapy drugs that require direct bloodstream administration for rapid and effective action. Hospital-based oncology treatments strongly favor injectable administration for controlled dosing and immediate therapeutic response. The increasing number of hospital admissions for advanced-stage cancer patients further supports segment dominance. Parenteral drugs offer higher bioavailability, making them more effective in aggressive cancer management. The complexity of Merkel cell carcinoma cases also necessitates physician-supervised administration. Expansion of oncology infusion centers has strengthened infrastructure support. Pharmaceutical innovations in long-acting injectables also contribute to sustained adoption. Overall, parenteral delivery remains the clinical standard for advanced treatment protocols.

The Oral segment is projected to witness the fastest CAGR of 13.4% from 2026 to 2033, driven by growing demand for patient-friendly and home-based treatment options. Oral targeted therapies and supportive drugs are increasingly being developed to reduce hospital dependency. Rising preference for outpatient cancer care is significantly supporting segment expansion. Improved formulation technologies are enhancing drug stability and absorption efficiency. Patients benefit from greater convenience and reduced treatment costs compared to injectable therapies. Increasing adoption in maintenance therapy phases is also accelerating growth. Pharmaceutical companies are focusing on oral immunomodulators and kinase inhibitors. Expansion of homecare oncology services is further driving adoption. Overall, oral administration is growing due to convenience and evolving treatment paradigms.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Centres, and Others. The Hospitals segment held the largest market revenue share of 55.8% in 2025, driven by the availability of advanced oncology infrastructure, skilled oncologists, and immediate access to emergency cancer care. Most immunotherapy and chemotherapy treatments are administered in hospital settings due to their complexity and need for monitoring. Rising cancer hospitalization rates continue to strengthen hospital dominance. Integrated diagnostic and therapeutic services improve treatment efficiency. Government funding and insurance coverage further support hospital-based care. Increasing adoption of combination therapies also favors institutional treatment settings. Hospitals remain the primary point of care for advanced-stage patients. Strong referral networks from primary care centers enhance patient inflow. Overall, hospitals dominate due to comprehensive cancer care capabilities.

The Specialty Centres segment is expected to witness the fastest CAGR of 14.7% from 2026 to 2033, driven by increasing demand for focused oncology care and personalized treatment approaches. These centers provide advanced immunotherapy and targeted therapy under specialized supervision. Growing patient preference for expert-driven care is boosting adoption. Availability of advanced diagnostic tools enhances treatment precision. Rising investments in dedicated cancer institutes are strengthening infrastructure. Specialty centres often provide shorter waiting times and improved patient experience. Increasing clinical trial activity in specialized oncology centers is further driving growth. Expansion in urban healthcare facilities supports accessibility. Overall, specialty centres are emerging as high-growth treatment hubs.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Hospital Pharmacy segment accounted for the largest market revenue share of 68.1% in 2025, driven by the direct dispensing of oncology drugs during inpatient and outpatient treatment cycles. Most Merkel cell carcinoma therapies, especially injectable immunotherapies, are administered under hospital supervision. Strict regulatory control over oncology drug distribution further reinforces hospital pharmacy dominance. Integration with hospital treatment protocols ensures seamless drug availability. Rising patient dependency on institutional care supports steady demand. Hospital pharmacies also manage high-cost biologics and specialty drugs efficiently. Increasing cancer treatment complexity strengthens centralized dispensing systems. Insurance reimbursement structures favor hospital-based procurement. Overall, hospital pharmacies remain the primary distribution channel.

The Online Pharmacy segment is projected to witness the fastest CAGR of 16.2% from 2026 to 2033, driven by growing digitalization of healthcare services and rising demand for home delivery of supportive cancer medications. Patients are increasingly adopting e-pharmacy platforms for convenience and cost savings. Expansion of tele-oncology services is supporting remote prescriptions. Improved logistics and cold-chain capabilities are enhancing drug availability. Growing smartphone penetration is further accelerating online adoption. Online pharmacies are particularly gaining traction for oral supportive therapies and follow-up medications. Regulatory frameworks supporting digital healthcare are expanding market access. Increasing patient awareness of digital health platforms is driving usage. Overall, online pharmacies are rapidly emerging as a convenient distribution channel.

Merkel Cell Carcinoma Treatment Market Regional Analysis

- North America dominated the merkel cell carcinoma treatment market with the largest revenue share of approximately 44.60% in 2025, driven by the highest absolute incidence of Merkel Cell Carcinoma (MCC) globally, early adoption of anti-PD-1/PD-L1 immune checkpoint inhibitors, and the strong presence of specialized dermatologic oncology centers. The region also benefits from well-established cancer care infrastructure and advanced treatment protocols, enabling rapid clinical adoption of innovative immunotherapies

- Clinicians and patients in the region increasingly rely on immune checkpoint inhibitors as first-line and advanced-line therapies, supported by strong clinical trial activity and guideline-driven treatment pathways. The presence of leading academic medical institutions with dedicated MCC expertise further enhances early diagnosis and optimized patient management

- This widespread adoption is further supported by robust healthcare systems, high awareness of rare skin cancers, and strong integration of immuno-oncology into standard treatment practice, establishing North America as a global leader in Merkel Cell Carcinoma treatment innovation

U.S. Merkel Cell Carcinoma Treatment Market Insight

The U.S. merkel cell carcinoma treatment market captured the largest revenue share in 2025 within North America, driven by rapid adoption of advanced immunotherapies and strong clinical research activity in oncology. The country has been at the forefront of checkpoint inhibitor therapies, particularly PD-1 and PD-L1 inhibitors, which have significantly improved survival outcomes in MCC patients. Increasing collaboration between academic research institutions, pharmaceutical companies, and cancer centers is accelerating drug development and expanding access to novel therapies. In addition, high diagnostic awareness and early detection rates contribute to timely treatment initiation and improved clinical outcomes.

Europe Merkel Cell Carcinoma Treatment Market Insight

The Europe merkel cell carcinoma treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of rare skin cancers, expanding access to immuno-oncology treatments, and growing adoption of evidence-based oncology care. Strengthened healthcare systems and cancer screening initiatives are supporting earlier diagnosis and treatment. European countries are increasingly incorporating immune checkpoint inhibitors into standardized MCC treatment protocols. Furthermore, rising participation in multinational clinical trials and supportive regulatory frameworks are improving access to innovative therapies across oncology centers.

U.K. Merkel Cell Carcinoma Treatment Market Insight

The U.K. merkel cell carcinoma treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by strong oncology care networks and increasing use of immunotherapy-based treatment approaches. National healthcare programs and specialist cancer centers play a key role in improving MCC diagnosis and treatment outcomes. The growing adoption of PD-1/PD-L1 inhibitors, along with structured treatment pathways and improved access to dermatologic oncology expertise, is contributing to steady market expansion. Ongoing clinical research further supports innovation in treatment strategies.

Germany Merkel Cell Carcinoma Treatment Market Insight

The Germany merkel cell carcinoma treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare infrastructure, high oncology awareness, and increasing use of advanced immunotherapies. The country emphasizes precision oncology and guideline-based cancer care, which supports effective MCC management. German oncology centers are increasingly integrating immune checkpoint inhibitors into treatment regimens, supported by robust reimbursement systems and access to specialized cancer care facilities. Continuous clinical research activity is further strengthening treatment advancements.

Asia-Pacific Merkel Cell Carcinoma Treatment Market Insight

The Asia-Pacific Merkel Cell Carcinoma Treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing incidence of MCC linked to aging populations and rising awareness of ultraviolet (UV) radiation exposure risks. Improvements in healthcare infrastructure and expanding oncology services are further supporting market growth. Countries such as Australia, Japan, and China are witnessing greater adoption of immuno-oncology therapies alongside improving diagnostic capabilities. Rising healthcare investments and enhanced access to advanced cancer treatments are accelerating regional market expansion.

Japan Merkel Cell Carcinoma Treatment Market Insight

The Japan merkel cell carcinoma treatment market is gaining momentum due to its aging population, advanced healthcare system, and increasing adoption of immunotherapy-based cancer treatments. Greater awareness of rare skin cancers is also contributing to improved diagnosis rates. Japan is witnessing expanding use of PD-1/PD-L1 inhibitors in MCC treatment, supported by strong oncology research and clinical expertise. Integration of precision medicine approaches is further enhancing treatment effectiveness and patient outcomes.

China Merkel Cell Carcinoma Treatment Market Insight

The China merkel cell carcinoma treatment market accounted for the largest market revenue share in Asia Pacific in 2025, driven by improving healthcare infrastructure, rising cancer awareness, and increasing access to advanced oncology therapies. Growing urbanization and enhanced diagnostic capabilities are supporting earlier detection of MCC cases. China is also experiencing increased adoption of immuno-oncology therapies, supported by expanding domestic pharmaceutical innovation and growing participation in oncology clinical trials. Continued healthcare system development is further strengthening treatment accessibility across major hospitals and cancer centers.

Merkel Cell Carcinoma Treatment Market Share

The Merkel Cell Carcinoma Treatment industry is primarily led by well-established companies, including:

• Merck & Co. (U.S.)

• Bristol Myers Squibb (U.S.)

• Roche (Switzerland)

• Novartis (Switzerland)

• Pfizer (U.S.)

• AstraZeneca (U.K.)

• Eli Lilly and Company (U.S.)

• Amgen (U.S.)

• Sanofi (France)

• Johnson & Johnson (U.S.)

• Regeneron Pharmaceuticals (U.S.)

• Gilead Sciences (U.S.)

• AbbVie (U.S.)

• Seagen (U.S.)

• Genentech (U.S.)

• BeiGene (China)

• Takeda Pharmaceutical (Japan)

• Eisai (Japan)

• Ipsen (France)

• Teva Pharmaceutical Industries (Israel)

Latest Developments in Global Merkel Cell Carcinoma Treatment Market

- In February 2025, Pfizer presented updated 5-year long-term follow-up data from the JAVELIN Merkel 200 trial at the AACR Annual Meeting, confirming sustained durable overall survival benefit for avelumab, with 26.0% of patients in the previously treated cohort remaining alive at 5 years, establishing avelumab's long-term clinical value in metastatic MCC

- In January 2025, Merck & Co. initiated the STAMP-II trial evaluating neoadjuvant pembrolizumab followed by surgery versus surgery alone in Stage I-III resectable MCC, representing the first large-scale randomized controlled trial specifically designed to evaluate the survival benefit of neoadjuvant immunotherapy in early-stage MCC

- In November 2024, Iovance Biotherapeutics announced plans to initiate a Phase II study of lifileucel, its tumor-infiltrating lymphocyte (TIL) therapy, in checkpoint inhibitor-refractory metastatic MCC, marking an important milestone in the development of cellular immunotherapy approaches for MCC beyond current checkpoint inhibitor options

- In August 2024, Incyte Corporation reported Phase I/II results for its novel PD-1/LAG-3 bispecific antibody INCB123667 in previously treated metastatic MCC, demonstrating preliminary anti-tumor activity with an objective response rate of 38% in a cohort that included patients who had progressed on prior checkpoint inhibitor therapy

- In May 2024, AstraZeneca and Regeneron announced a collaborative clinical program evaluating the combination of durvalumab and fianlimab (LAG-3 inhibitor) in advanced MCC, exploring dual checkpoint blockade as a strategy to improve response rates beyond single-agent PD-1/PD-L1 inhibition

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.