Global Methane Emissions Monitoring In Oil And Gas Market

Market Size in USD Billion

USD

3.40 Billion

USD

16.79 Billion

2025

2033

USD

3.40 Billion

USD

16.79 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.40 Billion | |

| USD 16.79 Billion | |

| % | |

|

Methane Emissions Monitoring in Oil & Gas Market Overview

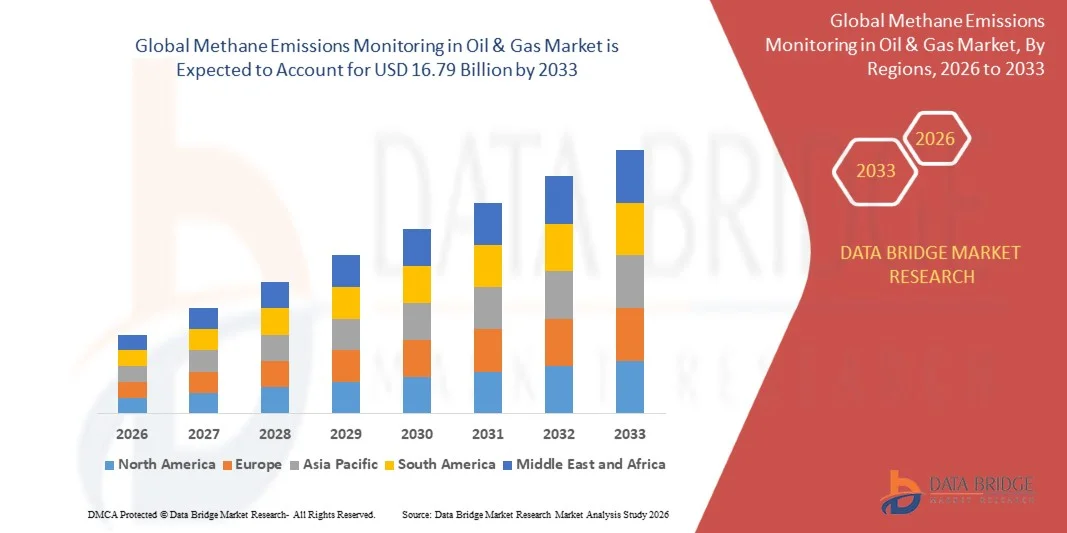

As per Data Bridge Market Research analysis The methane emissions monitoring in oil & gas market was valued at USD 3.40 billion in 2025 and is projected to reach USD 16.79 billion by 2033, growing at a CAGR of 22.10% from 2026 to 2033. The market is experiencing consistent growth driven by increasing regulatory pressure to reduce methane emissions, rapid advancements in methane detection and quantification technologies, and expanding deployment of continuous monitoring systems across upstream, midstream, and downstream oil and gas operations. The growing adoption of satellite-based monitoring, optical gas imaging, aerial surveys, and sensor-based detection platforms is further enhancing emissions transparency and operational accountability.

The increasing focus on methane mitigation globally, combined with stricter emissions reporting requirements and industry-wide decarbonization commitments, is compelling oil and gas operators to adopt advanced methane monitoring solutions. Continuous emissions monitoring systems (CEMS), drone- and aircraft-based inspections, satellite-enabled surveillance, and real-time analytics platforms are increasingly supplementing traditional leak detection and repair (LDAR) programs in many regions, offering scalable, repeatable, and cost-effective approaches for emissions detection, regulatory compliance, loss prevention, and greenhouse gas reduction.

Market Size & Forecast

- Global Market Value (2025): USD 3.40 Billion

- Expected Market Value (2033): USD 16.79 Billion

- Forecast CAGR (2026–2033): 22.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the methane emissions monitoring in oil & gas market with the largest revenue share of 38.5% in 2025, supported by stringent methane regulations, widespread deployment of leak detection and repair (LDAR) programs, and significant investments in advanced monitoring technologies across the United States and Canada.

- The continuous emissions monitoring systems (CEMS) segment led the market with a 38.4% share in 2025, driven by increasing regulatory pressure, demand for real-time emissions tracking, and widespread adoption across large upstream and midstream oil and gas facilities.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by expanding natural gas infrastructure, increasing environmental monitoring requirements, and growing methane mitigation initiatives across China, India, and Southeast Asia.

- Continuous monitoring systems (CMS) are the fastest-growing monitoring system type, projected to register a CAGR of 9.5%, reflecting the surge in deployment of distributed sensor networks and real-time emissions intelligence platforms.

- The optical gas imaging (OGI) segment dominated the detection technology category with a 33.2% revenue share in 2025, led by its widespread use in Leak Detection and Repair (LDAR) programs and its ability to visually identify methane leaks in real time.

- Fixed monitoring systems accounted for 42.6% of the market, preferred by widespread deployment across upstream production sites, refineries, and gas processing facilities requiring continuous site-level emissions tracking.

- The cloud-based monitoring segment is the fastest-growing deployment mode category, with a CAGR of 11%, driven by the increasing adoption of digital emissions management platforms and centralized data analytics solutions.

Report Scope and Methane Emissions Monitoring in Oil & Gas Market Segmentation

|

Attributes |

Methane Emissions Monitoring in Oil & Gas Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· SLB (U.S.) · Baker Hughes Company (U.S.) · Halliburton Company (U.S.) · ABB Ltd (Switzerland) · Honeywell International Inc. (U.S.) · Siemens AG (Germany) · Teledyne FLIR LLC (U.S.) · Emerson Electric Co. (U.S.) · Sensirion AG (Switzerland) · Spectra Sensors LLC (U.S.) · GHGSat Inc. (Canada) · Kayrros SAS (France) · Orbio Earth GmbH (Germany) · Momentick Ltd. (Israel) · AIRMO GmbH (Germany) · Carbon Mapper Inc. (U.S.) · Insight M (U.S.) · Blue Sky Measurements (U.S.) · EOTRAC (U.S.) · Blue Comply (U.S.) |

|

Market Opportunities |

· The growing deployment of satellite-based methane monitoring · Increasing integration of multi-platform monitoring using satellites, aircraft, drones, and advanced analytics · The rising adoption of AI and data-driven methane analytics platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Methane Emissions Monitoring in Oil & Gas Market Trends

Trend: Expansion of Satellite, Drone, and Multi-Layer Methane Monitoring Systems

The methane emissions monitoring in oil & gas market is increasingly shifting toward integrated, multi-layer detection ecosystems combining satellites, drones, aircraft, and ground-based sensors to enable continuous, high-resolution identification and quantification of methane leaks across complex upstream, midstream, and downstream infrastructure. This shift is being driven by the need for persistent emissions visibility, faster leak localization, and improved measurement accuracy across geographically dispersed oil and gas assets, where traditional periodic inspection methods are no longer sufficient for regulatory and ESG requirements.

For instance, the UN Environment Programme’s Methane Alert and Response System (MARS) leverages near-real-time satellite data to detect major methane emission events globally and alert operators and governments for rapid response, significantly improving the speed of leak identification and mitigation across oil and gas production regions. This initiative highlights the increasing importance of satellite-enabled monitoring platforms in enhancing global methane accountability, accelerating emissions reduction efforts, and supporting more effective regulatory enforcement across the oil and gas sector.

Methane Emissions Monitoring in Oil & Gas Market Dynamics

Key Market Driver: Rising Regulatory Pressure and Global Methane Reduction Commitments

The primary growth driver for the methane emissions monitoring market is the rapid strengthening of global regulatory frameworks and climate commitments targeting methane reduction as one of the most impactful near-term greenhouse gases. Governments and international bodies are increasingly enforcing stricter LDAR requirements, emissions disclosure norms, and carbon reporting obligations, compelling oil and gas operators to adopt advanced monitoring technologies that ensure compliance while minimizing emissions penalties and reputational risks.

For instance, regulatory initiatives such as the United States EPA methane rules and the European Union Methane Strategy are mandating more frequent monitoring, repair cycles, and emissions verification, which is directly accelerating the adoption of continuous emissions monitoring systems and advanced detection technologies across major oil and gas producing regions. These regulatory developments demonstrate the growing role of policy-driven compliance requirements in accelerating methane monitoring technology adoption and supporting the transition toward more transparent, measurable, and accountable emissions management practices within the oil and gas industry.

Key Restraint/Challenge: High Deployment Cost and Technical Complexity of Advanced Monitoring Systems

Despite strong technological progress, the market faces significant barriers due to the high capital intensity and operational complexity associated with deploying advanced methane monitoring systems that integrate satellites, drones, aircraft surveillance, and dense sensor networks into a unified emissions intelligence framework. These systems require substantial upfront investment, continuous calibration, skilled technical personnel, and advanced data processing infrastructure, making adoption particularly challenging for small and mid-scale operators.

For instance, a research study published in Atmospheric Chemistry and Physics highlighted that accurately quantifying methane emissions from oil and gas operations requires combining multiple measurement approaches, including ground-based observations, aerial surveys, and atmospheric modeling. The study emphasized that differences in measurement techniques, data processing requirements, and uncertainty management increase the complexity and cost of developing reliable methane monitoring frameworks at large scales.

Key Market Opportunity: Integration of AI with Satellite and Multi-Platform Methane Analytics

A major emerging opportunity in the methane emissions monitoring market lies in the integration of artificial intelligence and machine learning algorithms with multi-source monitoring systems, including satellite imagery, drone-based sensing, and ground-level IoT sensors, enabling automated methane detection, predictive analytics, and real-time emissions intelligence. This convergence is transforming methane monitoring from a reactive compliance tool into a proactive operational optimization system that enhances leak prevention, maintenance efficiency, and emissions forecasting capabilities.

For instance, research published in Atmospheric Chemistry and Physics demonstrated that machine-learning approaches applied to TROPOMI satellite observations can automate methane plume detection and improve identification of methane emission sources. Similarly, Sentinel-2-based deep learning models such as CH4Net have shown potential for scalable monitoring of methane super-emitters, reducing dependence on manual satellite image analysis. These advancements highlight the growing role of AI-driven remote sensing in improving methane emissions visibility, enabling faster leak identification, and supporting more efficient large-scale monitoring across oil and gas operations.

Methane Emissions Monitoring in Oil & Gas Market Scope

The methane emissions monitoring in oil & gas market is segmented on the basis of monitoring system, detection technology, deployment mode, and end user

-

By Monitoring System

On the basis of monitoring system, the methane emissions monitoring in oil & gas market is segmented into continuous monitoring systems (CMS), periodic monitoring, continuous emissions monitoring systems (CEMS), and portable & handheld systems. the continuous emissions monitoring systems (CEMS) segment dominated the market with an estimated 38.4% share in 2025, driven by increasing regulatory pressure, demand for real-time emissions tracking, and widespread adoption across large upstream and midstream oil and gas facilities. These systems enable uninterrupted measurement of methane concentrations, allowing operators to detect leaks at an early stage and improve compliance with tightening environmental regulations. They are widely integrated with fixed sensor networks and facility-level monitoring infrastructure, particularly in high-emission production sites. Rising emphasis on continuous compliance reporting under methane abatement frameworks further strengthens adoption. Their ability to reduce dependence on manual inspections and periodic surveys also enhances operational efficiency.

The continuous monitoring systems (CMS) segment is projected to be the fastest growing, with an estimated CAGR of 9.5% from 2026 to 2033, driven by increasing deployment of distributed sensor networks and real-time emissions intelligence platforms. CMS solutions are gaining traction due to their ability to provide high-frequency emissions data across multiple assets simultaneously. Advancements in IoT-enabled sensors, wireless communication, and cloud-based analytics are significantly improving system scalability. Oil and gas operators are increasingly shifting toward CMS to move from reactive to proactive emissions management. Integration with AI-based anomaly detection is further accelerating adoption. Growing regulatory push for continuous methane reporting is a key growth catalyst.

-

By Detection Technology

On the basis of detection technology, the market is segmented into optical gas imaging (OGI), tunable diode laser absorption spectroscopy (TDLAS), cavity ring-down spectroscopy (CRDS), LiDAR, infrared cameras, and laser spectroscopy. The optical gas imaging (OGI) segment dominated the market with an estimated 33.2% share in 2025, owing to its widespread use in Leak Detection and Repair (LDAR) programs and its ability to visually identify methane leaks in real time. OGI cameras are extensively deployed in upstream oil and gas facilities for routine inspections due to their portability and fast deployment capability. They are also favored for regulatory compliance inspections because they provide direct visual confirmation of leaks. Continuous improvements in infrared sensor sensitivity are enhancing detection accuracy. Their relatively lower operational complexity compared to advanced laser-based systems supports widespread adoption.

The laser spectroscopy segment is projected to be the fastest growing, with an estimated CAGR of 10.2% from 2026 to 2033, driven by its high precision, long-range detection capability, and suitability for continuous monitoring applications. Laser-based systems such as TDLAS and CRDS enable highly sensitive methane concentration measurements even at low emission levels. These technologies are increasingly deployed in fixed monitoring networks and airborne surveillance systems. Integration with satellite and drone-based platforms is expanding their use in large-scale emissions mapping. Their ability to provide quantitative data rather than qualitative imaging is a key advantage. Increasing demand for high-accuracy emissions verification is accelerating adoption.

-

By Deployment Mode

On the basis of deployment mode, the market is segmented into fixed monitoring systems, portable/handheld systems, cloud-based monitoring, and on-premises monitoring. The fixed monitoring systems segment dominated the market with an estimated 42.6% share in 2025, driven by widespread deployment across upstream production sites, refineries, and gas processing facilities requiring continuous site-level emissions tracking. These systems provide stable, long-term monitoring capabilities and are often integrated into facility safety and environmental compliance frameworks. Their ability to deliver uninterrupted emissions data makes them highly suitable for regulatory reporting. Fixed systems are also increasingly integrated with SCADA and industrial IoT platforms. Growing emphasis on facility-wide emissions transparency further supports dominance.

The cloud-based monitoring segment is projected to be the fastest growing, with an estimated CAGR of 11% from 2026 to 2033, driven by increasing adoption of digital emissions management platforms and centralized data analytics solutions. Cloud-based systems enable real-time aggregation of emissions data from multiple sites and assets, improving decision-making and regulatory reporting efficiency. These platforms support AI-driven analytics, predictive leak detection, and automated reporting workflows. Oil and gas operators are increasingly adopting cloud architectures to reduce infrastructure costs and improve scalability. Remote accessibility and cross-border monitoring capabilities further enhance demand. Integration with satellite and IoT systems is accelerating adoption.

-

By End User

On the basis of end user, the market is segmented into oil & gas operators, national oil companies (NOCs), independent producers, and oilfield service providers. The oil & gas operators segment dominated the market with an estimated 45.1% share in 2025, driven by large-scale upstream and midstream infrastructure ownership and strong regulatory obligations for methane emissions monitoring. These operators are the primary adopters of continuous monitoring systems due to their high emission intensity and compliance requirements. They are increasingly investing in integrated emissions intelligence platforms combining satellite, sensor, and aerial data. Strong ESG reporting requirements are further reinforcing adoption. Their ability to deploy large-scale monitoring infrastructure gives them a dominant position in the market.

The national oil companies (NOCs) segment is projected to be the fastest growing, with an estimated CAGR of 9.8% from 2026 to 2033, driven by rising government-led decarbonization programs and international climate commitments. NOCs are increasingly modernizing their emissions monitoring infrastructure to align with global methane reduction targets. Large-scale upstream assets in emerging economies are being equipped with advanced monitoring technologies. Partnerships with global technology providers are accelerating deployment of satellite and AI-based monitoring systems. Increasing regulatory alignment with international frameworks is also supporting growth. Focus on sustainability reporting and emissions transparency is a key driver.

Methane Emissions Monitoring in Oil & Gas Market Regional Analysis

North America dominated the methane emissions monitoring in oil & gas market with the largest revenue share of 38.5% in 2025, supported by stringent methane regulations, widespread deployment of leak detection and repair (LDAR) programs, and significant investments in advanced monitoring technologies across the United States and Canada. The region also benefits from strong regulatory frameworks such as EPA methane standards, increasing investment in continuous emissions monitoring systems, and widespread integration of digital oilfield technologies. Growing deployment of AI-enabled emissions analytics, IoT-based sensor networks, and real-time methane detection platforms is accelerating market development. Increasing focus on decarbonization, ESG compliance, and methane intensity reduction continues to strengthen North America’s leadership position in the global market.

U.S. Methane Emissions Monitoring in Oil & Gas Market Insight

The United States dominates the methane emissions monitoring in oil & gas market, driven by strict federal methane regulations, large-scale shale oil and gas production, and rapid deployment of advanced detection technologies such as satellites, aircraft-based sensing, drones, and continuous emissions monitoring systems. The country is also a global leader in LDAR programs and digital oilfield adoption, where operators increasingly rely on AI-driven analytics and IoT-enabled sensor networks to improve emissions visibility and regulatory compliance. Strong ESG reporting requirements and methane intensity reduction targets continue to accelerate investment in real-time monitoring infrastructure across upstream and midstream assets. For instance, the U.S. Environmental Protection Agency (EPA) methane rulemakings (OOOOb/OOOOc standards) require oil and gas operators to implement stricter emissions detection, frequent leak monitoring, and repair programs, significantly increasing deployment of continuous monitoring and detection technologies across production facilities. In addition, peer-reviewed studies using satellite inversion methods show that U.S. oil and gas methane emissions, particularly in the Permian Basin, are significantly underestimated in bottom-up inventories, highlighting the importance of satellite-based monitoring for accurate emissions accounting.

Europe Methane Emissions Monitoring in Oil & Gas Market Insight

Europe holds a significant position in the methane emissions monitoring market, driven by strict regulatory frameworks under the EU Methane Strategy, strong decarbonization commitments, and advanced adoption of satellite-based emissions monitoring technologies across industrial and energy sectors. The region emphasizes emissions transparency, measurement accuracy, and regulatory verification across the entire oil and gas value chain. Increasing integration of optical gas imaging, laser spectroscopy, and AI-powered emissions analytics is further strengthening monitoring capabilities across upstream and downstream operations. For instance, the EU Methane Strategy (2020) requires systematic measurement, reporting, and verification of methane emissions across energy infrastructure, accelerating the adoption of continuous monitoring systems and advanced leak detection technologies across member states. In addition, satellite-based research using Sentinel-5P (TROPOMI) has enabled high-resolution tracking of methane plumes across industrial regions in Europe, improving detection of previously unreported emission sources.

United Kingdom Methane Emissions Monitoring in Oil & Gas Market Insight

The United Kingdom market is driven by offshore North Sea oil and gas production, stringent environmental compliance requirements, and increasing adoption of satellite and digital monitoring technologies for methane emissions tracking. The region is focusing on improving offshore emissions transparency through advanced monitoring systems and real-time analytics platforms integrated into energy infrastructure operations. For instance, the North Sea Transition Authority (NSTA) enforces emissions reduction and monitoring requirements across offshore oil and gas facilities, promoting adoption of advanced leak detection and continuous emissions monitoring technologies. In addition, satellite-based methane monitoring using Copernicus Sentinel-5P (TROPOMI) has been widely used to track emissions over offshore North Sea infrastructure, improving detection of episodic methane leaks from energy production systems.

Germany Methane Emissions Monitoring in Oil & Gas Market Insight

Germany plays a key role in the methane emissions monitoring ecosystem due to strong industrial decarbonization policies, advanced environmental engineering capabilities, and adoption of high-precision emissions monitoring technologies across industrial infrastructure. Although upstream oil and gas production is limited, Germany is a key adopter of emissions monitoring systems for industrial and energy applications. For instance, enforcement of the EU Industrial Emissions Directive (IED) requires strict methane and greenhouse gas monitoring across industrial facilities, encouraging deployment of optical gas imaging, laser spectroscopy, and continuous emissions monitoring systems. Satellite-based research using Sentinel-5P data is also widely applied across Germany and Europe to monitor methane concentration anomalies and industrial emission sources at high spatial resolution.

Asia-Pacific Methane Emissions Monitoring in Oil & Gas Market Insight

Asia-Pacific is the fastest-growing region in methane emissions monitoring due to rapid industrialization, expanding oil and gas infrastructure, and increasing adoption of satellite-based and AI-enabled methane detection systems across China, India, and Southeast Asia. Governments in the region are strengthening environmental monitoring frameworks and integrating digital technologies to improve emissions tracking and regulatory compliance. For instance, China’s integration into global methane monitoring initiatives using satellite-based detection systems is improving identification of large-scale methane emissions from energy infrastructure and industrial facilities. Another instance is UNEP’s global Methane Alert and Response System (MARS), which actively monitors methane emissions across Asia-Pacific oil and gas operations using satellite-based detection and rapid alert mechanisms.

Japan Methane Emissions Monitoring in Oil & Gas Market Insight

Japan’s market is driven by LNG import infrastructure monitoring, energy security priorities, and increasing adoption of advanced emissions tracking technologies across industrial energy systems. Although domestic oil and gas production is limited, Japan plays a critical role in methane emissions monitoring through LNG supply chain transparency and international climate cooperation. For instance, Japan’s participation in international methane reduction initiatives supported by the IEA is strengthening emissions tracking across LNG terminals and energy infrastructure systems. In addition, satellite-based methane detection using Sentinel-5P (TROPOMI) supports regional monitoring of methane concentration patterns across East Asia, including Japan’s industrial zones.

China Methane Emissions Monitoring in Oil & Gas Market Insight

China is one of the largest and fastest-growing markets for methane emissions monitoring due to massive oil and gas infrastructure expansion, rising environmental enforcement, and strong investment in satellite-based monitoring systems and AI-enabled emissions analytics. Government focus on carbon neutrality and air quality improvement is accelerating deployment of continuous emissions monitoring systems across industrial sectors. For instance, China’s participation in global satellite methane observation systems and increasing use of TROPOMI-based detection platforms is improving identification of large-scale methane emissions across energy infrastructure. Another instance is China’s alignment with UNEP and IEA methane reduction frameworks, which is driving adoption of continuous emissions monitoring systems and advanced leak detection technologies across oil and gas operations.

Methane Emissions Monitoring in Oil & Gas Market Share

The methane emissions monitoring in oil & gas industry is primarily led by well-established companies, including:

- SLB (U.S.)

- Baker Hughes Company (U.S.)

- Halliburton Company (U.S.)

- ABB Ltd (Switzerland)

- Honeywell International Inc. (U.S.)

- Siemens AG (Germany)

- Teledyne FLIR LLC (U.S.)

- Emerson Electric Co. (U.S.)

- Sensirion AG (Switzerland)

- Spectra Sensors LLC (U.S.)

- GHGSat Inc. (Canada)

- Kayrros SAS (France)

- Orbio Earth GmbH (Germany)

- Momentick Ltd. (Israel)

- AIRMO GmbH (Germany)

- Carbon Mapper Inc. (U.S.)

- Insight M (U.S.)

- Blue Sky Measurements (U.S.)

- EOTRAC (U.S.)

- Blue Comply (U.S.)

Latest Developments in Methane Emissions Monitoring in Oil & Gas Market

- In August 2024, NASA-supported Carbon Mapper Coalition launched the Tanager-1 satellite aboard SpaceX Transporter-11, marking a major advancement in high-resolution methane monitoring from space capable of identifying individual emission sources such as oil and gas infrastructure and refineries. The mission is designed to provide publicly accessible methane plume data and significantly improve global detection of high-emission sites, supporting faster mitigation of methane leaks

- In January 2024, UNEP officially launched the full operational phase of its Methane Alert and Response System (MARS), enabling global satellite-based detection and notification of large methane emission events across the oil and gas sector, allowing governments and operators to respond rapidly to “super-emitter” events using multi-satellite data integration. MARS aggregates data from more than 30 satellite instruments and is designed to improve global methane accountability through near-real-time alerts and verification mechanisms for emission mitigation

- In December 2023, the United States Environmental Protection Agency finalized updated methane regulations for the oil and gas sector under the Clean Air Act, introducing stricter requirements for leak detection, repair, and expanded monitoring of emissions from both new and existing sources nationwide. The rule significantly strengthens regulatory pressure on oil and gas operators, accelerating deployment of continuous monitoring systems, LDAR technologies, and advanced emissions detection solutions across production facilities

- In November 2023, the European Union reached agreement on its Methane Regulation framework, introducing mandatory measurement, reporting, and verification (MRV) requirements across the entire oil and gas supply chain, including imported fossil fuels. The regulation accelerates adoption of satellite monitoring, optical gas imaging, and laser-based methane detection technologies to ensure compliance with strict emissions transparency standards across Europe’s energy sector

- In January 2021, the International Energy Agency (IEA) launched the Global Methane Tracker, establishing a comprehensive global framework that integrates satellite observations, scientific models, and industry data to estimate methane emissions from oil and gas operations worldwide. This initiative has become a global benchmark tool for methane emissions assessment and is widely used in policy formulation and regulatory planning for methane reduction strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.