Global Micro Invasive Glaucoma Surgery Migs Devices Market

Market Size in USD Billion

USD

1.89 Billion

USD

18.84 Billion

2025

2033

USD

1.89 Billion

USD

18.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.89 Billion | |

| USD 18.84 Billion | |

| % | |

|

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Size

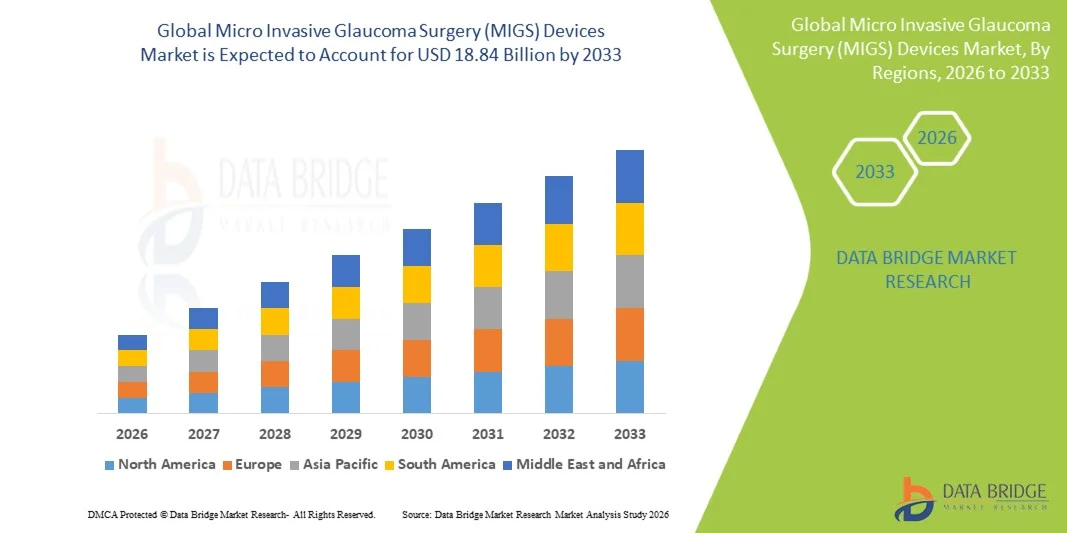

- The global Micro Invasive Glaucoma Surgery (MIGS) devices market size was valued at USD 1.89 billion in 2025and is expected to reach USD 18.84 billion by 2033, at a CAGR of 33.3% during the forecast period

- The market growth is largely fueled by the rising prevalence of glaucoma and the increasing preference for minimally invasive surgical procedures, supported by continuous technological advancements in ophthalmic devices and surgical techniques

- Furthermore, growing awareness among patients and ophthalmologists regarding early intervention, along with the demand for safer procedures with faster recovery times, is positioning MIGS devices as a preferred treatment option. These converging factors are accelerating the adoption of MIGS technologies, thereby significantly boosting the industry's growth

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Analysis

- Micro Invasive Glaucoma Surgery (MIGS) devices, designed to reduce intraocular pressure through minimally invasive procedures, are increasingly vital in modern ophthalmic care due to their improved safety profile, shorter recovery times, and ability to be combined with cataract surgeries in both early and moderate stages of glaucoma treatment

- The escalating demand for Micro Invasive Glaucoma Surgery (MIGS) devices is primarily fueled by the rising global prevalence of glaucoma, growing geriatric population, and increasing preference among surgeons and patients for less invasive surgical options with reduced complications compared to traditional glaucoma surgeries

- North America dominated the Micro Invasive Glaucoma Surgery (MIGS) devices market with the largest revenue share of 35.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative ophthalmic technologies, and a strong presence of key industry players, with the United States experiencing substantial growth in procedure volumes driven by favorable reimbursement policies and increasing awareness of early glaucoma management

- Asia-Pacific is expected to be the fastest growing region in the Micro Invasive Glaucoma Surgery (MIGS) devices market during the forecast period due to increasing healthcare expenditure, rising awareness about eye health, and a growing patient pool in countries such as China and India

- Trabecular meshwork segment dominated the Micro Invasive Glaucoma Surgery (MIGS) devices market with a market share of 45.6% in 2025, driven by their effectiveness in enhancing aqueous humor outflow and widespread adoption due to relatively straightforward surgical techniques and favorable clinical outcomes

Report Scope and Micro Invasive Glaucoma Surgery (MIGS) Devices Market Segmentation

|

Attributes |

Micro Invasive Glaucoma Surgery (MIGS) Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of Micro Invasive Glaucoma Surgery (MIGS) devices into earlier-stage glaucoma treatment · Rising adoption of next-generation MIGS implants compatible with outpatient and ambulatory surgical centers |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Trends

“Expanding Adoption of Minimally Invasive Combined Surgical Procedures”

- A significant and accelerating trend in the global Micro Invasive Glaucoma Surgery (MIGS) devices market is the increasing integration of MIGS procedures with cataract surgeries, improving clinical efficiency and patient outcomes in the management of glaucoma

- For instance, the iStent inject W is widely used in combination with cataract surgery to enhance aqueous outflow while simultaneously treating lens opacity in a single surgical session

- The adoption of next-generation MIGS devices enables surgeons to achieve better intraocular pressure control with fewer postoperative complications, while supporting faster recovery compared to traditional glaucoma surgeries

- Furthermore, advanced MIGS platforms are increasingly being designed for compatibility with minimally invasive ophthalmic operating workflows, allowing standardized implantation techniques across surgical centers

- This trend towards combination procedures and streamlined surgical approaches is reshaping clinical practice, with companies such as Glaukos Corporation and Alcon focusing on devices that simplify implantation and improve surgical reproducibility

- The demand for combined and less invasive glaucoma interventions is growing rapidly across both developed and emerging healthcare systems, as clinicians prioritize safety, efficiency, and long-term disease management

- Furthermore, rising adoption of disposable and preloaded MIGS delivery systems is improving procedural efficiency and reducing surgical variability across ophthalmic centers

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Dynamics

Driver

“Rising Prevalence of Glaucoma and Growing Demand for Early Intervention”

- The increasing prevalence of glaucoma worldwide, along with growing emphasis on early disease detection and intervention, is a significant driver for the heightened demand for Micro Invasive Glaucoma Surgery (MIGS) devices

- For instance, in March 2025, leading ophthalmic centers reported increasing utilization of MIGS procedures as a first-line surgical option for patients with mild to moderate intraocular pressure elevation

- As patients and healthcare providers seek safer alternatives to traditional trabeculectomy, MIGS devices offer reduced surgical risk, shorter recovery time, and improved long-term eye pressure control

- Furthermore, rising geriatric populations and increased awareness of vision preservation are making early surgical intervention a preferred treatment pathway in many healthcare systems

- The convenience of minimally invasive procedures, combined with improved clinical outcomes and expanding reimbursement coverage, is further accelerating adoption in hospitals and ambulatory surgical centers

- Growing integration of MIGS into standard glaucoma treatment guidelines is strengthening its role as a preferred surgical solution in ophthalmology

- In addition, increasing screening programs for eye diseases are improving early diagnosis rates, thereby expanding the pool of patients eligible for MIGS procedures

- Furthermore, rising healthcare infrastructure development in emerging economies is enhancing access to advanced ophthalmic surgical technologies, supporting overall market expansion

Restraint/Challenge

“High Procedure Cost and Limited Long-Term Clinical Evidence”

- Concerns surrounding the high cost of Micro Invasive Glaucoma Surgery (MIGS) procedures, including device pricing and surgical infrastructure requirements, pose a significant challenge to broader market penetration

- For instance, in several emerging healthcare markets, limited reimbursement coverage for MIGS procedures restricts patient access despite growing clinical demand

- While MIGS devices offer improved safety profiles, the relatively higher upfront cost compared to conventional glaucoma treatments remains a barrier for cost-sensitive healthcare systems

- Furthermore, limited long-term clinical outcome data compared to traditional glaucoma surgeries creates hesitation among some ophthalmic surgeons regarding widespread first-line adoption

- Companies such as Glaukos Corporation and Ivantis (AbbVie) are investing in long-term clinical studies to strengthen evidence supporting sustained intraocular pressure reduction and device durability

- Overcoming these challenges through improved reimbursement frameworks, cost optimization, and expanded long-term clinical validation will be vital for sustained Micro Invasive Glaucoma Surgery (MIGS) devices market growth

- In addition, variability in surgeon training and learning curves for newer MIGS techniques can limit consistent procedural outcomes across different healthcare settings

- Furthermore, stringent regulatory approval processes for ophthalmic implantable devices can delay product commercialization and slow market entry for innovative MIGS solutions

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Scope

The market is segmented on the basis of product, target, surgery type, end user, and distribution channel.

- By Product

On the basis of product, the Micro Invasive Glaucoma Surgery (MIGS) devices market is segmented into MIGS stents, MIGS shunts, and others. The MIGS stents segment dominated the market with the largest revenue share of 50% in 2025, driven by their minimally invasive design, strong clinical efficacy in reducing intraocular pressure, and widespread adoption in early to moderate glaucoma management. MIGS stents such as trabecular micro-bypass implants are frequently used due to their predictable outcomes and compatibility with cataract surgery. Their minimally traumatic insertion technique and favorable safety profile further strengthen their dominance in clinical practice. In addition, increasing surgeon familiarity and regulatory approvals have contributed to their strong market penetration. The segment also benefits from continuous product innovations improving implant durability and fluid outflow efficiency.

The MIGS shunts segment is expected to witness the fastest growth rate of 12% from 2026 to 2033, driven by their superior effectiveness in refractory glaucoma cases and ability to provide sustained intraocular pressure reduction. MIGS shunts are increasingly preferred for patients with moderate to severe disease progression where conventional stents may be insufficient. Their ability to divert aqueous humor to alternative outflow pathways enhances long-term pressure control. Rising clinical adoption of minimally invasive drainage implants is further supporting segment expansion. Furthermore, ongoing technological advancements in biocompatible materials and micro-scale device engineering are improving safety and reducing postoperative complications, accelerating adoption globally.

- By Target

On the basis of target, the Micro Invasive Glaucoma Surgery (MIGS) devices market is segmented into trabecular meshwork, suprachoroidal space, subconjunctival filtration, and reducing aqueous production. The trabecular meshwork segment dominated the market with the largest revenue share of 45.6% in 2025, driven by its physiological relevance as the primary drainage pathway for aqueous humor and high clinical success rates. Devices targeting this pathway are widely used in early-stage glaucoma due to their safety and minimally disruptive mechanism. Surgeons prefer trabecular-based MIGS procedures because they maintain natural outflow physiology while effectively lowering intraocular pressure. In addition, strong clinical evidence and guideline inclusion have reinforced their dominance. Growing adoption in combination cataract-glaucoma surgeries further strengthens segment leadership.

The suprachoroidal space segment is expected to witness the fastest growth rate of 13% from 2026 to 2033, driven by its enhanced pressure-lowering potential and innovative bypass mechanism. This target pathway allows alternative aqueous drainage, offering benefits in patients with inadequate trabecular outflow response. Increasing focus on next-generation implantable devices leveraging suprachoroidal access is accelerating adoption. Furthermore, advancements in micro-scale implant design are improving long-term safety and reducing hypotony risks. Rising clinical interest in alternative outflow pathways for resistant glaucoma cases is further fueling segment growth globally.

- By Surgery Type

On the basis of surgery type, the Micro Invasive Glaucoma Surgery (MIGS) devices market is segmented into glaucoma in conjunction with cataract surgery and stand-alone glaucoma surgery. The glaucoma in conjunction with cataract surgery segment dominated the market with the largest revenue share of 60% in 2025, driven by high procedural efficiency, improved patient outcomes, and cost-effectiveness of performing dual interventions in a single session. This approach significantly reduces recovery time and surgical risk while addressing both vision impairment and intraocular pressure simultaneously. Increasing global cataract surgery volumes strongly support this segment’s dominance. Surgeons also prefer combined procedures due to streamlined workflow and reduced hospital burden. In addition, reimbursement structures in developed healthcare systems favor combined surgeries, further strengthening market leadership.

The stand-alone glaucoma surgery segment is expected to witness the fastest growth rate of 11% from 2026 to 2033, driven by increasing diagnosis of early-stage glaucoma independent of cataract presence. Growing awareness of preventive glaucoma treatment is expanding demand for standalone MIGS procedures. These surgeries are increasingly adopted in younger patient populations where cataract surgery is not yet required. Technological advancements enabling safer and more effective standalone MIGS implantation are also supporting growth. Furthermore, expanding outpatient surgical settings and improved reimbursement coverage are accelerating procedural adoption globally.

- By End User

On the basis of end user, the Micro Invasive Glaucoma Surgery (MIGS) devices market is segmented into hospital outpatient departments (HOPD), ophthalmology clinics, ambulatory surgery centers (ASCs), and others. The hospital outpatient departments (HOPD) segment dominated the market with the largest revenue share of 42% in 2025, driven by strong infrastructure availability, skilled ophthalmic surgeons, and high patient inflow for advanced glaucoma treatments. HOPDs are preferred for complex MIGS procedures due to their access to comprehensive diagnostic and surgical facilities. In addition, reimbursement support and integration with hospital-based ophthalmology departments strengthen segment dominance. The presence of multidisciplinary care teams also enhances procedural outcomes.

The ambulatory surgery centers (ASCs) segment is expected to witness the fastest growth rate of 14% from 2026 to 2033, driven by increasing demand for cost-effective, same-day surgical procedures with faster recovery times. ASCs offer efficient outpatient MIGS procedures with reduced hospital stay and lower procedural costs. Rising preference for minimally invasive ophthalmic surgeries in decentralized care settings is accelerating adoption. Furthermore, advancements in portable surgical technologies and improved reimbursement frameworks are supporting ASC expansion globally.

- By Distribution Channel

On the basis of distribution channel, the Micro Invasive Glaucoma Surgery (MIGS) devices market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest revenue share of 75% in 2025, driven by bulk procurement by hospitals, government healthcare systems, and large ophthalmology centers. Direct tender agreements ensure cost efficiency, long-term supply contracts, and standardized device availability across healthcare institutions. Strong involvement of manufacturers in institutional partnerships further strengthens this segment. In addition, regulatory procurement systems in public healthcare facilities favor direct purchasing models.

The retail sales segment is expected to witness the fastest growth rate of 12% from 2026 to 2033, driven by increasing penetration of private ophthalmology clinics and ambulatory surgical centers. Retail distribution allows faster access to MIGS devices for smaller healthcare providers. Rising decentralization of eye care services and expansion of specialty clinics are further supporting growth. In addition, improved distributor networks and digital procurement platforms are enhancing accessibility and availability of advanced MIGS technologies globally.

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Regional Analysis

- North America dominated the Micro Invasive Glaucoma Surgery (MIGS) devices market with the largest revenue share of 35.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative ophthalmic technologies, and a strong presence of key industry players

- The region benefits from a well-established healthcare infrastructure, high procedure volumes, and early adoption of minimally invasive ophthalmic surgeries, making MIGS a standard treatment option in many clinical settings

- Consumers and healthcare providers in the region highly value the clinical benefits of MIGS devices, including improved intraocular pressure control, reduced surgical complications, and faster recovery compared to traditional glaucoma surgeries

U.S. Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The U.S. Micro Invasive Glaucoma Surgery (MIGS) devices market captured the largest share within North America in 2025, driven by strong healthcare infrastructure and rapid adoption of advanced ophthalmic surgical technologies. The country has a high burden of glaucoma cases, which is increasing demand for minimally invasive and effective treatment options. U.S. ophthalmologists widely prefer MIGS procedures due to their safety, reduced recovery time, and compatibility with cataract surgery. Strong reimbursement support and favorable insurance coverage further encourage procedure adoption across hospitals and ambulatory surgical centers. The presence of leading global ophthalmic device manufacturers and continuous product innovation are also key growth drivers. In addition, increasing awareness of early glaucoma diagnosis and expanding outpatient eye care services are significantly strengthening market penetration across the country.

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The Europe Micro Invasive Glaucoma Surgery (MIGS) devices market is projected to grow at a substantial CAGR during the forecast period, driven by increasing glaucoma prevalence, aging population, and strong demand for minimally invasive ophthalmic procedures. Healthcare systems across Europe are increasingly adopting MIGS technologies due to their clinical benefits, including reduced surgical risks and improved long-term outcomes. The region is also witnessing rising integration of MIGS procedures in combination cataract-glaucoma surgeries, supported by well-established hospital infrastructure and expanding outpatient surgical centers. Growing investments in ophthalmic care and increasing awareness of early diagnosis and treatment are further accelerating adoption. In addition, regulatory support for innovative medical devices and increasing clinical research activity are strengthening market expansion across major European countries.

U.K. Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The U.K. Micro Invasive Glaucoma Surgery (MIGS) devices market is expected to grow at a notable CAGR, driven by rising glaucoma cases and increasing preference for minimally invasive surgical solutions. The country is witnessing strong adoption of MIGS devices due to their ability to provide effective intraocular pressure control with reduced recovery time and fewer complications. The healthcare system is increasingly focusing on early intervention and preventive eye care, further supporting market growth. Expansion of ophthalmology services within both NHS and private healthcare facilities, along with rising awareness among patients regarding advanced treatment options, is contributing to higher procedural uptake. In addition, increasing use of combination cataract and glaucoma surgeries is further strengthening demand for MIGS devices in the region.

Germany Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The Germany Micro Invasive Glaucoma Surgery (MIGS) devices market is anticipated to expand at a considerable CAGR, supported by advanced healthcare infrastructure and strong emphasis on innovation-driven ophthalmic care. Rising prevalence of glaucoma, particularly among the elderly population, is increasing demand for minimally invasive treatment options. German healthcare providers prioritize precision, safety, and long-term clinical effectiveness, making MIGS devices an attractive option for glaucoma management. The market is also benefiting from growing adoption of outpatient surgical procedures and integration of advanced medical technologies in hospital systems. In addition, increasing preference for patient-centric and technologically advanced eye care solutions is further supporting market expansion.

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) devices market is expected to grow at the fastest CAGR of 14% during 2026 to 2033, driven by rising glaucoma prevalence, improving healthcare infrastructure, and increasing awareness of eye health. Countries such as China, Japan, India, and the U.S. expatriate-linked medical hubs in APAC are witnessing rapid adoption of minimally invasive ophthalmic procedures supported by expanding hospital networks and growing access to advanced surgical technologies. Increasing healthcare expenditure and government initiatives promoting eye care are further boosting market growth. The availability of cost-effective MIGS devices and expansion of outpatient surgical centers are also contributing to wider adoption across the region. In addition, growing investments by global medical device companies in Asia-Pacific are enhancing product accessibility and strengthening market penetration.

Japan Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The Japan Micro Invasive Glaucoma Surgery (MIGS) devices market is gaining momentum due to its advanced healthcare system, aging population, and strong focus on precision-based ophthalmic treatments. Rising cases of glaucoma are driving demand for minimally invasive surgical solutions that offer improved safety and faster recovery. The country’s high-tech medical ecosystem supports integration of MIGS devices with advanced surgical platforms, enhancing procedural efficiency. Healthcare providers strongly emphasize patient comfort and long-term treatment outcomes, further encouraging adoption. In addition, increasing use of combination surgeries and growing investment in ophthalmic innovation are supporting market expansion.

India Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The India Micro Invasive Glaucoma Surgery (MIGS) devices market accounted for a significant share in Asia-Pacific in 2025, driven by rapid urbanization, expanding middle-class population, and increasing awareness of glaucoma management. Rising healthcare infrastructure development and growing number of ophthalmology clinics are improving access to advanced surgical treatments. The availability of affordable MIGS devices is further accelerating adoption across urban and semi-urban regions. Government initiatives aimed at strengthening eye care services and expanding surgical outreach programs are also supporting market growth. In addition, increasing preference for minimally invasive procedures among both patients and surgeons is significantly contributing to rising adoption of MIGS technologies in the country.

Micro Invasive Glaucoma Surgery (MIGS) Devices Market Share

The Micro Invasive Glaucoma Surgery (MIGS) Devices industry is primarily led by well-established companies, including:

- Glaukos Corporation (U.S.)

- Alcon Inc. (Switzerland)

- Santen Pharmaceutical Co., Ltd. (Japan)

- AbbVie Inc. (Ireland)

- Bausch + Lomb (Canada)

- Sight Sciences, Inc. (U.S.)

- New World Medical, Inc. (U.S.)

- iSTAR Medical (Belgium)

- Nova Eye Medical Limited (Australia)

- Ellex Medical Lasers Ltd. (Australia)

- BVI Medical (U.S.)

- Carl Zeiss Meditec AG (Germany)

- Topcon Corporation (Japan)

- Nidek Co., Ltd. (Japan)

- Hoya Corporation (Japan)

- MicroSurgical Technology, Inc. (U.S.)

- D.O.R.C. Dutch Ophthalmic Research Center (Netherlands)

- Ophtec B.V. (Netherlands)

- Lumenis Ltd. (Israel)

What are the Recent Developments in Global Micro Invasive Glaucoma Surgery (MIGS) Devices Market?

- In February 2026, ophthalmology conferences highlighted continued expansion of MIGS innovation pipelines, with new investigational devices targeting multiple aqueous outflow pathways including trabecular, suprachoroidal, and subconjunctival spaces for better management of glaucoma. Experts reported growing surgeon adoption of next-generation MIGS systems and increasing integration into earlier-stage treatment strategies. This reflects a broader industry shift toward minimally invasive, anatomy-specific glaucoma interventions supported by ongoing clinical trials and regulatory advancements

- In January 2026, Glaukos Corporation announced the FDA approval of a supplemental New Drug Application for its iDose TR implant, enabling re-administration of the device for long-term management of glaucoma. The approval was based on accumulated clinical evidence supporting repeat use safety and sustained intraocular pressure control in patients. This development strengthens the role of implantable MIGS-related therapies as long-term procedural alternatives to topical medications and reinforces the shift toward sustained drug-device combination approaches in glaucoma care

- In February 2023, ophthalmology clinical updates highlighted growing real-world adoption of MIGS procedures as first-line surgical interventions for mild-to-moderate glaucoma. Surgeons reported increasing preference for trabecular bypass and stent-based MIGS devices due to their safety profile and compatibility with cataract surgery. This shift indicates a strong transition away from traditional invasive glaucoma surgeries toward minimally invasive alternatives

- In October 2022, Glaukos Corporation announced continued clinical advancement and expanded global adoption of its iStent inject W device, one of the most widely used MIGS stents for treating open-angle glaucoma. The device demonstrated improved intraocular pressure control and reduced medication dependence in patients undergoing minimally invasive glaucoma surgery. This development reflects increasing global acceptance of MIGS procedures as a standard treatment option in early-stage glaucoma management

- In November 2021, Alcon announced the acquisition of Ivantis, a key developer of MIGS technologies, strengthening its surgical glaucoma portfolio with the Hydrus Microstent device designed to reduce intraocular pressure in patients with glaucoma. The Hydrus Microstent is a minimally invasive implant that enhances aqueous humor outflow and has shown sustained clinical efficacy in long-term studies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.