Global Microdisplay Market

Market Size in USD Billion

CAGR :

%

USD

4.47 Billion

USD

35.83 Billion

2025

2033

USD

4.47 Billion

USD

35.83 Billion

2025

2033

| 2026 –2033 | |

| USD 4.47 Billion | |

| USD 35.83 Billion | |

| % | |

|

Microdisplay Market Size

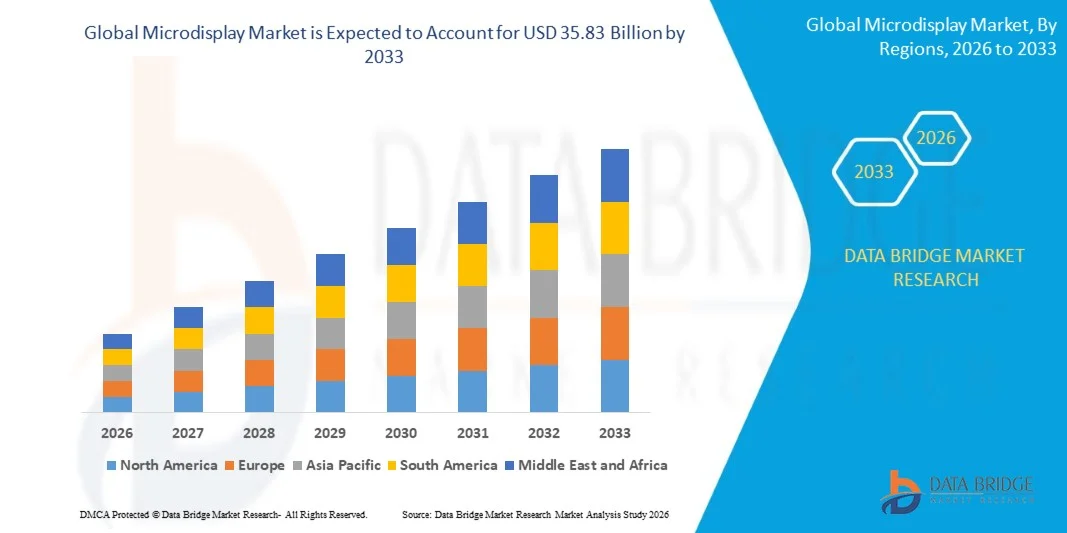

- The global microdisplay market size was valued at USD 4.47 billion in 2025 and is expected to reach USD 35.83 billion by 2033, at a CAGR of 29.70% during the forecast period

- The market growth is largely fueled by the rising adoption of AR/VR devices, automotive head-up displays (HUDs), and wearable electronics, driving demand for compact, high-resolution, and energy-efficient microdisplays

- Furthermore, increasing investments in display technologies, ongoing innovations in OLED, LCoS, and microLED solutions, and growing interest in immersive experiences for consumer, industrial, and medical applications are accelerating the uptake of microdisplay solutions, thereby significantly boosting the industry’s growth

Microdisplay Market Analysis

- Microdisplays are compact display devices used in applications such as near-to-eye (NTE) AR/VR devices, automotive HUDs, and wearable electronics. These systems offer high pixel density, low power consumption, and integration capabilities with optical systems to enhance user experience in both consumer and industrial sectors

- The escalating demand for microdisplays is primarily fueled by the growth of AR/VR adoption, increasing integration of HUDs in vehicles, rising industrial automation, and the need for high-performance, energy-efficient display solutions across multiple end-user segments

- Asia-Pacific dominated the microdisplay market with a share of 36.82% in 2025, due to increasing adoption of AR/VR devices, expanding automotive HUD integration, and a strong presence of electronics manufacturing hubs

- North America is expected to be the fastest growing region in the microdisplay market during the forecast period due to robust demand for microdisplays in AR/VR, automotive HUDs, and industrial applications

- Near-to-Eye (NTE) devices segment dominated the market with a market share of 48.87% in 2025, due to growing adoption in augmented reality (AR) and virtual reality (VR) applications. NTE devices are widely used in wearable electronics, offering immersive experiences for gaming, training, and industrial applications. The segment benefits from increasing consumer interest in AR/VR headsets and the rising development of lightweight, compact, and high-resolution displays

Report Scope and Microdisplay Market Segmentation

|

Attributes |

Microdisplay Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Microdisplay Market Trends

“Rising Adoption of AR/VR and Wearable Devices”

- A significant trend in the microdisplay market is the growing integration of microdisplays in augmented reality (AR), virtual reality (VR), and wearable devices, driven by increasing demand for immersive visual experiences and compact form factors. This trend is elevating microdisplays as essential components for consumer electronics, industrial AR applications, and medical wearable devices

- For instance, Sony supplies OLED microdisplays used in AR and VR headsets that deliver high pixel density and low latency, enhancing immersive visual performance in devices such as the Sony PlayStation VR2. These displays are enabling realistic graphics rendering while maintaining a compact size suitable for head-mounted devices

- The adoption of microdisplays is expanding in smart glasses and AR-assisted industrial solutions, where high-resolution and lightweight displays are critical for field operations, maintenance, and remote collaboration. This is positioning microdisplays as key enablers of hands-free visualization and real-time data overlay in professional environments

- Healthcare applications are increasingly leveraging microdisplays in wearable medical devices for patient monitoring and surgical guidance systems. High-contrast and energy-efficient microdisplays support prolonged device operation while delivering clear visuals for critical healthcare tasks

- The consumer electronics sector is witnessing a shift toward compact and high-performance display solutions for smartwatches, AR glasses, and personal wearable devices. Microdisplays are enabling smaller device footprints without compromising image quality, driving innovation in wearable design

- The market is also experiencing rising interest in automotive AR head-up displays (HUDs) and infotainment systems that use microdisplays for navigation and real-time information. This trend is reinforcing the role of microdisplays in delivering advanced, user-centric visual interfaces across various applications

Microdisplay Market Dynamics

Driver

“Growing Demand for High-Resolution and Energy-Efficient Displays”

- The rising demand for high-resolution and energy-efficient displays is driving the adoption of microdisplays, as these components deliver superior pixel density and low power consumption in compact form factors. Such attributes are critical for AR/VR headsets, wearable devices, and HUDs where display clarity and battery life are paramount

- For instance, eMagin manufactures OLED microdisplays that provide high pixel-per-inch (PPI) performance for military and industrial applications, enhancing visual clarity while reducing energy requirements. These displays support prolonged usage without overheating, benefiting wearable and head-mounted solutions

- Increasing consumer preference for immersive experiences in gaming, professional visualization, and mixed reality applications is contributing to microdisplay adoption. Microdisplays allow compact integration without sacrificing visual fidelity, meeting performance expectations in portable devices

- The integration of microdisplays in AR/VR ecosystems is accelerating due to their ability to reduce device size while maintaining high image quality. This demand is encouraging manufacturers to innovate display technologies that balance resolution, brightness, and power efficiency

- The increasing focus on sustainability and reduced energy consumption in consumer electronics is further strengthening the demand for microdisplays. Energy-efficient operation aligns with environmental goals while providing manufacturers with opportunities to differentiate their products through performance and battery longevity

Restraint/Challenge

“High Manufacturing Costs and Complex Production Processes”

- The microdisplay market faces challenges from high manufacturing costs and complex production processes required to achieve ultra-high resolution, small pixel pitch, and uniform brightness. These factors increase production difficulty and result in higher device prices, impacting market scalability

- For instance, Kopin Corporation employs sophisticated lithography and microfabrication techniques to produce high-resolution microdisplays for AR and defense applications. Such processes demand precision equipment and skilled labor, raising overall manufacturing costs

- Maintaining consistent quality and performance across large-scale production presents significant operational challenges. High defect rates in microfabrication can lead to yield loss, extended production timelines, and elevated per-unit costs

- The reliance on specialized materials such as OLED substrates, micro-lenses, and backplane technologies increases supply chain complexity and cost exposure. Manufacturers must balance performance requirements with economic feasibility to remain competitive

- Scaling microdisplay production while ensuring energy efficiency, resolution consistency, and reliability under varying environmental conditions continues to constrain market growth. These challenges require ongoing innovation in fabrication techniques and process optimization to meet rising global demand

Microdisplay Market Scope

The market is segmented on the basis of product, technology, resolution, brightness, and industry.

• By Product

On the basis of product, the microdisplay market is segmented into Near-to-Eye (NTE) devices, Head-Up Displays (HUD), and others. The Near-to-Eye (NTE) devices segment dominated the largest market revenue share of 48.87% in 2025, driven by growing adoption in augmented reality (AR) and virtual reality (VR) applications. NTE devices are widely used in wearable electronics, offering immersive experiences for gaming, training, and industrial applications. The segment benefits from increasing consumer interest in AR/VR headsets and the rising development of lightweight, compact, and high-resolution displays. Integration of NTE devices in smart glasses and mixed reality solutions further fuels their market demand, supported by the focus of key players on enhancing visual quality and reducing power consumption.

The HUD segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising implementation in automotive and aviation sectors. HUDs provide critical real-time information to drivers and pilots while minimizing distraction, improving safety, and enhancing user experience. Their adoption in electric and autonomous vehicles is driving demand for advanced display technologies that combine brightness, clarity, and wide field of view. Industrial and military applications are also expected to contribute to the rapid growth of this segment, owing to increasing demand for situational awareness and operational efficiency.

• By Technology

On the basis of technology, the microdisplay market is segmented into LCD, LCoS, OLED, and DLP. The OLED segment dominated the largest market revenue share in 2025, driven by superior color reproduction, high contrast ratios, and thin form factors. OLED microdisplays are widely used in premium AR/VR devices and military applications where image quality is critical. The technology also allows for low power consumption and flexible designs, making it suitable for compact wearables and high-end headsets. Major players focus on OLED for its capability to deliver vibrant visuals in NTE applications, which strengthens its market dominance.

The LCoS segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its high resolution and ability to support optical projection systems. LCoS microdisplays are preferred in professional AR systems, projectors, and HUDs due to their excellent image sharpness and reflective technology. The growing adoption of LCoS in industrial, automotive, and simulation applications is expected to accelerate its market growth over the forecast period.

• By Resolution

On the basis of resolution, the microdisplay market is segmented into lower than HD, HD, FHD, and higher than FHD. The FHD segment dominated the largest market revenue share in 2025, driven by its balance between image clarity and affordability for AR/VR and NTE devices. FHD microdisplays are preferred for providing immersive experiences without significantly increasing power consumption or device size. The segment benefits from widespread adoption in consumer electronics, enterprise applications, and wearable devices that require high-quality visuals. Leading manufacturers focus on optimizing FHD microdisplays for enhanced frame rates and color accuracy to meet growing consumer expectations.

The higher than FHD segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for ultra-high-resolution displays in industrial, military, and medical applications. These displays enable precise imaging, improved user experience, and detailed visualization for AR/VR training, simulation, and surgical procedures. The growth is further supported by ongoing technological advancements and decreasing costs of high-resolution microdisplay production.

• By Brightness

On the basis of brightness, the microdisplay market is segmented into less than 500 nits, 500 to 1,000 nits, and more than 1,000 nits. The 500 to 1,000 nits segment dominated the largest market revenue share in 2025, driven by its suitability for most indoor and semi-outdoor applications. This range provides a balance between visibility, power efficiency, and device portability, making it ideal for AR/VR headsets, HUDs, and wearable devices. Manufacturers focus on optimizing brightness to improve user comfort, reduce eye strain, and enhance color performance across various lighting conditions. In addition, this brightness range supports integration with multiple optical systems and consumer electronics, reinforcing its market leadership.

The more than 1,000 nits segment is expected to witness the fastest CAGR from 2026 to 2033, driven by growing adoption in automotive HUDs, outdoor AR devices, and industrial applications. High-brightness microdisplays ensure readability in bright environments and are critical for military, aerospace, and outdoor sports applications. Technological improvements in backlighting and energy efficiency are further accelerating growth in this segment.

• By Industry

On the basis of industry, the microdisplay market is segmented into consumer, industrial and enterprise, automotive, military, defense and aerospace, sports and entertainment, retail and hospitality, medical, education, and others. The consumer segment dominated the largest market revenue share in 2025, driven by increasing adoption of AR/VR headsets for gaming, entertainment, and lifestyle applications. Consumers are seeking immersive experiences and portable devices, encouraging manufacturers to focus on lightweight, high-resolution, and energy-efficient displays. Growth is further supported by rising investments in AR/VR content creation, wearable technology, and enhanced consumer electronics ecosystems.

The automotive segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing integration of HUDs and driver-assistance systems in electric and autonomous vehicles. Automotive microdisplays enhance safety, provide real-time navigation, and support advanced infotainment systems. Regulatory initiatives promoting driver safety, combined with consumer demand for connected and intelligent vehicles, are driving the rapid adoption of microdisplay technology in this sector.

Microdisplay Market Regional Analysis

- Asia-Pacific dominated the microdisplay market with the largest revenue share of 36.82% in 2025, driven by increasing adoption of AR/VR devices, expanding automotive HUD integration, and a strong presence of electronics manufacturing hubs

- The region’s cost-effective production landscape, rising investments in consumer electronics, and growing exports of microdisplay components are accelerating market expansion

- The availability of skilled labor, supportive government policies, and rapid technological adoption across developing economies are contributing to increased consumption of microdisplays in both consumer and industrial applications

China Microdisplay Market Insight

China held the largest share in the Asia-Pacific microdisplay market in 2025, owing to its leadership in electronics manufacturing, AR/VR device production, and automotive component supply. The country's strong industrial base, favorable government initiatives supporting advanced display technologies, and extensive export capabilities for microdisplay modules are major growth drivers. Demand is further bolstered by rapid development of wearable electronics and HUD systems for automotive and industrial applications.

India Microdisplay Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rising adoption of AR/VR technology, increasing production of consumer electronics, and growing investments in display manufacturing infrastructure. Government initiatives supporting electronics manufacturing and a focus on digital transformation in enterprises are strengthening market demand. In addition, expanding automotive and industrial sectors and growing R&D capabilities for microdisplay technologies are contributing to robust market expansion.

Europe Microdisplay Market Insight

The Europe microdisplay market is expanding steadily, supported by rising adoption of AR/VR devices in consumer, healthcare, and industrial sectors, as well as investments in high-precision automotive HUDs. The region emphasizes product quality, environmental compliance, and innovation in display technologies, particularly for premium consumer electronics and aerospace applications. Increasing collaboration between academic research institutions and technology companies is further enhancing market growth.

Germany Microdisplay Market Insight

Germany’s microdisplay market is driven by its strong automotive and industrial electronics sectors, high precision manufacturing capabilities, and focus on innovation in display technologies. The country has established R&D networks and partnerships between universities and technology manufacturers, fostering continuous advancement in microdisplay solutions. Demand is particularly strong for automotive HUDs, AR/VR devices, and aerospace applications requiring high-resolution, reliable displays.

U.K. Microdisplay Market Insight

The U.K. market is supported by a mature consumer electronics and aerospace industry, growing investments in AR/VR technology, and increasing focus on local manufacturing of high-end display solutions. Rising R&D activities, academic-industry collaborations, and production of niche microdisplay modules are supporting steady market growth. The country continues to play a significant role in high-value microdisplay applications for military, industrial, and medical sectors.

North America Microdisplay Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by robust demand for microdisplays in AR/VR, automotive HUDs, and industrial applications. A strong focus on technological innovation, material advancements, and high-resolution display solutions is boosting adoption. In addition, increasing investments by key electronics and tech players, along with growing reshoring of display manufacturing, are supporting market expansion.

U.S. Microdisplay Market Insight

The U.S. accounted for the largest share in the North America microdisplay market in 2025, underpinned by its leadership in consumer electronics, automotive technology, and aerospace applications. The country’s strong R&D infrastructure, investments in high-resolution and energy-efficient displays, and focus on innovation are encouraging adoption in AR/VR headsets, HUDs, and industrial solutions. Presence of major technology companies and a mature supply chain further solidify the U.S.'s leading position in the region.

Microdisplay Market Share

The microdisplay industry is primarily led by well-established companies, including:

- Sony Corporation (Japan)

- Semiconductor Solutions (Japan)

- Seiko Epson Corporation (Japan)

- eMagin Corporation (U.S.)

- Kopin Corporation (U.S.)

- Yunnan OLiGHTEK Opto-Electronic Technology Co., Ltd. (China)

- Syndiant Inc. (U.S.)

- LG Display (South Korea)

- Himax Technologies, Inc. (Taiwan)

- MicroVision, Inc. (U.S.)

- AU Optronics Corp. (Taiwan)

- Micron Technology, Inc. (U.S.)

- Universal Display Corporation (U.S.)

- Microtips Technology, Inc. (China)

- WiseChip Semiconductor (Taiwan)

- LG Display (South Korea)

Latest Developments in Global Microdisplay Market

- In August 2025, Haylo Labs acquired Plessey Semiconductors through a USD 100 million debt-backed financing, gaining access to monolithic microLED IP and the Plymouth fabrication site. This strategic acquisition strengthens Haylo Labs’ position in the high-performance microLED segment, enabling faster commercialization of microLED displays for AR, automotive, and industrial applications. The move is expected to accelerate product development cycles, enhance manufacturing capabilities, and contribute to market expansion by providing integrated microLED solutions for next-generation display devices

- In June 2025, Jade Bird Display raised RMB 1 billion (USD 140 million) to expand its 8-inch microLED production line to 50,000 wafers per year and accelerate full-color RGB development. This investment reinforces the company’s capacity to meet the growing demand for high-resolution microLED displays in AR/VR, wearable electronics, and advanced consumer devices. By scaling up production and focusing on full-color microLED technology, Jade Bird Display is positioned to capture a larger share of the rapidly expanding microdisplay market while enabling cost efficiencies and technological advancements

- In March 2025, BOE unveiled a 0.39-inch 1080p OLED microdisplay with an ultra-high pixel density of 4,032 ppi during SID Display Week, targeting sub-500 milliwatt AR glasses. This development demonstrates BOE’s focus on energy-efficient, high-resolution microdisplays for wearable AR devices. The innovation is expected to drive adoption of AR glasses in consumer and industrial sectors by delivering superior visual performance and extended battery life, reinforcing BOE’s competitive position in the microdisplay market

- In January 2024, Kopin Corporation and MICLEDI Microdisplays announced a collaborative initiative to develop advanced micro-LED displays for immersive AR experiences under high-brightness conditions. The partnership combines MICLEDI’s expertise in CMOS manufacturing with Kopin’s advanced backplane control and driving technologies to create high-performance microLED solutions. This collaboration is expected to accelerate innovation in AR applications, improve visibility in bright environments, and expand the market for microLED-enabled wearable devices and industrial AR solutions

- In June 2024, LG Display began mass production of the world’s first 13-inch Tandem OLED panel for laptops. Leveraging the superior performance and reduced power consumption of Tandem OLED technology, LG Display aims to strengthen its position in the OLED market. The launch is expected to drive adoption of high-efficiency OLED displays in laptops and portable devices, enhance user experience, and support the growing demand for energy-efficient, high-quality display technologies in the consumer electronics sector

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Microdisplay Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Microdisplay Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Microdisplay Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.