Global Microinsurance Market

Market Size in USD Billion

USD

101.61 Billion

USD

170.70 Billion

2025

2033

USD

101.61 Billion

USD

170.70 Billion

2025

2033

| 2026 - 2033 | |

| USD 101.61 Billion | |

| USD 170.70 Billion | |

| % | |

|

Microinsurance Market Overview

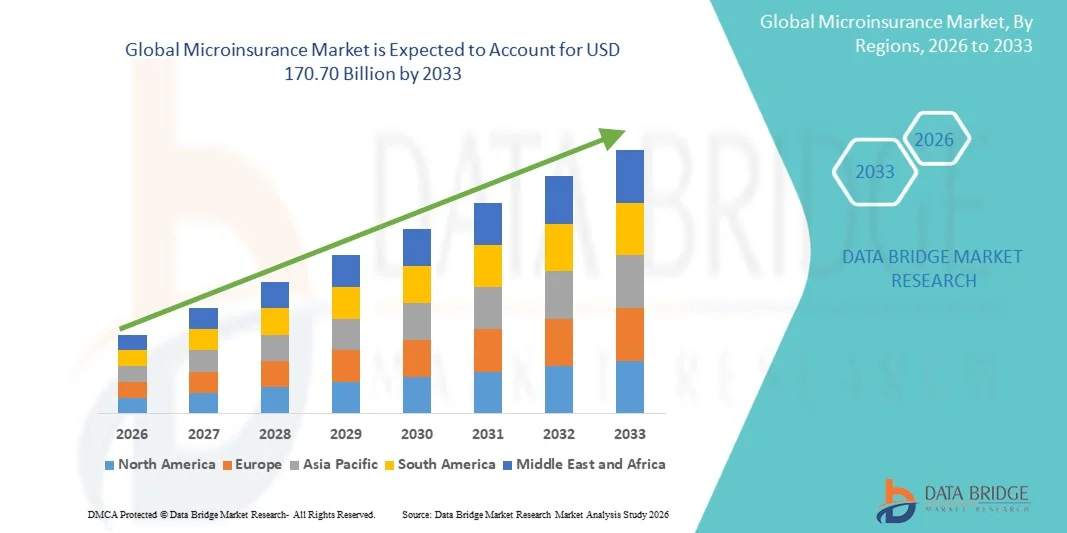

The Microinsurance Market was valued at USD 101.61 billion in 2025 and is projected to reach USD 170.70 billion by 2033, growing at a CAGR of 6.70% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for affordable financial protection among low-income populations, increasing awareness of insurance penetration in emerging economies, and expanding digital distribution channels such as mobile-based insurance platforms and fintech ecosystems. The growing vulnerability of underserved populations to health emergencies, climate-related disasters, and income instability is further accelerating adoption of microinsurance products across developing regions.

The increasing frequency of climate risks, natural disasters, and health-related expenditures, combined with limited access to traditional insurance services, is compelling governments, microfinance institutions, and insurers to promote low-cost, easy-to-access microinsurance solutions. Digital transformation in the insurance sector, including mobile wallets, AI-based underwriting, and parametric insurance models, is replacing traditional paper-based distribution systems in many markets, offering faster claim settlements, simplified enrollment processes, and highly scalable coverage options for rural and informal populations.

Key Market Trends & Insights

- North America dominated the Microinsurance Market with the largest revenue share of 34% in 2025, supported by strong digital insurance penetration, advanced fintech infrastructure, rising adoption of embedded insurance solutions, and increasing partnerships between insurers and financial technology platforms. The region also benefits from high financial literacy, widespread mobile insurance adoption, and strong regulatory frameworks supporting micro-level risk coverage products. Growing integration of AI-driven underwriting and digital distribution channels continues to strengthen North America’s leadership position in the global market.

- The Adult segment dominated the market in 2025 with a share of 66.1%, driven by high workforce participation and financial responsibility for dependents.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.9% from 2026 to 2033, fueled by rapid financial inclusion initiatives, large underinsured populations, increasing penetration of mobile-based insurance platforms, expanding fintech ecosystems, and strong government-backed social protection programs. Rising adoption of affordable microinsurance products across India, China, Indonesia, Vietnam, and other Southeast Asian countries is further accelerating regional market growth.

- The Adult age group segment dominated the market with a 61.48% share in 2025, supported by rising workforce participation, increasing financial dependency coverage needs, and growing adoption of microinsurance products among gig economy workers and informal sector populations.

Market Size & Forecast

- Global Market Value (2025): USD 101.61 Billion

- Expected Market Value (2033): USD 170.70 Billion

- Forecast CAGR (2026–2033): 6.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Microinsurance Market Segmentation

|

Attributes |

Microinsurance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Allianz SE (Germany) |

|

Market Opportunities |

· Expansion of Digital and Mobile-Based Microinsurance Platforms · Growth in Climate Risk and Agricultural Microinsurance · Increasing Government and NGO-Backed Insurance Inclusion Programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Microinsurance Market Trends

Trend: Growth in Digital and Embedded Microinsurance Solutions

Microinsurance products are increasingly being integrated into digital ecosystems such as mobile wallets, e-commerce platforms, and fintech applications. Providers are leveraging API-based insurance models to offer instant, low-cost coverage for health, life, agriculture, and asset protection. For instance, mobile network operators and fintech platforms in India, Africa, and Southeast Asia are bundling microinsurance with digital payment services, enabling instant enrollment and claims processing. The growing use of AI-driven underwriting and mobile-first distribution is significantly improving accessibility for low-income and underserved populations.

Microinsurance Market Dynamics

Key Market Driver: Rising Financial Inclusion and Expanding Low-Income Population Coverage

The increasing global focus on financial inclusion is driving strong demand for microinsurance products, particularly in emerging economies. Governments and financial institutions are actively promoting affordable insurance schemes to protect vulnerable populations against health emergencies, crop failure, natural disasters, and income loss.

For instance, government-supported microinsurance programs in India and Africa are expanding coverage to rural and informal sector workers, while digital insurers are using mobile platforms to reduce distribution costs and improve penetration in underserved regions. The rising gig economy workforce is also contributing to demand for flexible, low-premium insurance products.

Key Restraint/Challenge: Low Awareness and High Claim Settlement Complexity

A major challenge in the Microinsurance Market is the low level of awareness among target populations regarding insurance benefits and policy structures. In many developing regions, consumers still lack trust in insurance systems due to limited financial literacy and previous negative experiences.

In addition, fragmented regulatory frameworks and inefficient claim settlement processes increase operational complexity for insurers. Limited digital infrastructure in rural areas also restricts smooth onboarding and policy servicing, slowing down large-scale adoption.

Key Market Opportunity: Expansion of Digital Ecosystems and Insurtech Innovation

The integration of insurtech platforms, mobile banking, and AI-based risk assessment tools is creating significant growth opportunities in the microinsurance market. Digital insurers are increasingly using data analytics and machine learning to design personalized micro-level coverage products and improve risk prediction.

For instance, parametric insurance models are being used in agriculture to automatically trigger payouts based on weather data, reducing claim settlement time from weeks to days. Expansion of smartphone penetration across Asia-Pacific and Africa, along with government-led digital financial programs, is expected to further accelerate adoption of microinsurance solutions globally.

Microinsurance Market Scope

The Microinsurance market is segmented on the basis of type, age group, service provider, model type, and distribution channel.

- By Type

On the basis of type, the Microinsurance Market is segmented into Lifetime Coverage and Term Insurance. The Term Insurance segment dominated the market in 2025 with a share of 59.4%, driven by its low premium structure, simplified underwriting, and strong alignment with low-income population needs. It is widely preferred in emerging economies due to its affordability and easy renewal cycles. Government-backed financial inclusion programs further strengthened adoption across rural and semi-urban populations. Microfinance institutions also play a key role in distributing term-based microinsurance products. Digital onboarding and mobile-first insurance platforms have significantly reduced acquisition friction. In addition, increasing awareness of risk protection among informal workers has supported demand. The segment benefits from short-term financial commitment, making it accessible to first-time insurance buyers. Rising penetration of health-linked term covers has further expanded usage. Overall, its scalability and cost efficiency continue to reinforce market leadership globally.

The Lifetime Coverage segment is projected to witness the fastest growth with a CAGR of 8.2% from 2026 to 2033, supported by rising long-term financial planning awareness. Increasing income levels among lower-middle-class populations are enabling adoption of extended protection plans. Digital insurance ecosystems are making lifetime microinsurance products more accessible and transparent. Integration of savings, health, and life benefits is enhancing product attractiveness. Insurance providers are increasingly bundling long-term wellness benefits with coverage plans. Growing urbanization is improving customer awareness of lifelong risk protection. Governments are also promoting sustained insurance participation through subsidy-linked programs. Fintech-driven personalization is improving product affordability and retention. Expansion of AI-based risk assessment is enabling better pricing accuracy. These factors collectively are accelerating demand for lifetime microinsurance products.

- By Age Group

On the basis of age group, the market is segmented into Minor, Adult, and Senior Citizens. The Adult segment dominated the market in 2025 with a share of 66.1%, driven by high workforce participation and financial responsibility for dependents. Adults form the primary income-earning population, making them the key target for insurers. Employer-linked microinsurance schemes have further increased adoption among working individuals. Financial institutions actively cross-sell insurance with credit and savings products. Government social protection programs also prioritize adult beneficiaries. Rising awareness of health and life risks is strengthening penetration. Digital insurance platforms are improving accessibility in urban and rural markets. Increased mobile penetration is enabling easier premium payments. Adults are more responsive to income protection and hospitalization coverage products. This segment continues to remain the backbone of microinsurance demand globally.

The Senior Citizens segment is expected to register the fastest CAGR of 9.1% from 2026 to 2033, driven by rising global aging populations. Increasing healthcare costs are pushing demand for affordable senior protection plans. Governments are expanding pension-linked and health subsidy insurance programs. Digital health ecosystems are improving accessibility for elderly customers. Simplified claim processes are enhancing adoption among senior users. Insurance providers are designing age-specific microcoverage products. Family-driven insurance purchases are also supporting segment growth. Rising prevalence of chronic diseases is increasing demand for continuous coverage. Telemedicine integration with insurance plans is further strengthening adoption. These factors collectively are accelerating rapid growth in senior-focused microinsurance solutions.

- By Service Provider

On the basis of service provider, the market is segmented into Microinsurance (Commercially Viable) and Microinsurance Through Aid/Government Support. The Commercially Viable segment dominated the market in 2025 with a share of 63.8%, supported by strong participation from private insurers and fintech platforms. Scalability of digital distribution has significantly improved profitability. Mobile-based insurance ecosystems are enabling mass-market penetration. Microfinance institutions are acting as key distribution partners. Private insurers are focusing on low-ticket bundled insurance products. Data analytics is improving underwriting efficiency and reducing risk. Increasing financial inclusion is expanding customer base. Cross-selling through banking and telecom channels is accelerating adoption. Strong ROI from digital microinsurance products is attracting investments. This segment continues to lead due to commercial sustainability and high outreach efficiency.

The Microinsurance Through Aid/Government Support segment is projected to grow at a CAGR of 7.6% from 2026 to 2033, driven by increasing global financial inclusion initiatives. Governments are expanding subsidized insurance coverage for vulnerable populations. International aid organizations are funding insurance penetration programs in low-income regions. Public-private partnerships are strengthening delivery frameworks. Rural outreach programs are improving awareness and accessibility. Digital identity systems are enabling seamless beneficiary enrollment. Governments are integrating insurance with welfare schemes. Health crisis preparedness programs are boosting adoption. Donor-backed insurance pools are expanding risk coverage capacity. These factors are driving steady expansion of supported microinsurance ecosystems.

- By Model Type

On the basis of model type, the market is segmented into Partner Agent Model, Full-Service Model, Provider Driven Model, Community-Based/Mutual Model, and Others. The Partner Agent Model dominated the market in 2025 with a share of 41.7%, due to its ability to leverage existing distribution networks such as banks and MFIs. It reduces operational costs for insurers while expanding rural penetration. Telecom operators are increasingly partnering to distribute microinsurance. The model benefits from strong trust in local agents. Financial institutions provide bundled insurance with loans and savings products. Insurance penetration improves through established customer relationships. Digital platforms are enhancing agent productivity and reach. Regulatory support for bancassurance is further strengthening adoption. It enables rapid scalability in emerging markets. This model remains the most efficient distribution structure in microinsurance.

The Community-Based/Mutual Model is expected to register the fastest CAGR of 8.4% from 2026 to 2033, driven by rising trust-based financial systems. Local communities are increasingly forming cooperative insurance pools. Shared risk structures are improving affordability and acceptance. Digital platforms are enabling better coordination of mutual schemes. NGOs are supporting community insurance awareness programs. This model is highly effective in rural and informal economies. Peer-based trust significantly improves participation rates. Mobile payment systems are simplifying premium collection. Government support for cooperative insurance structures is expanding. These factors are driving strong adoption of community-led insurance ecosystems.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Sales, Financial Institutions, E-commerce, Hospitals, Clinics, and Others. The Financial Institutions segment dominated the market in 2025 with a share of 36.5%, driven by strong integration with banking and microfinance systems. Banks offer bundled insurance with savings and credit products. MFIs play a critical role in rural distribution. Strong trust in financial institutions enhances customer acquisition. Digital banking platforms are improving insurance accessibility. Government-backed financial inclusion schemes are expanding reach. Cross-selling strategies are increasing penetration rates. Insurance awareness campaigns through banks are boosting adoption. Integrated digital wallets are further supporting payments. This channel remains the most dominant due to institutional trust and scale efficiency.

The E-commerce segment is projected to register the fastest CAGR of 9.3% from 2026 to 2033, driven by rising digital adoption and mobile-first consumers. Online platforms are simplifying insurance purchase journeys. Insurtech integration with e-commerce ecosystems is expanding reach. Subscription-based insurance offerings are gaining popularity. AI-driven recommendation engines are improving conversion rates. Seamless digital onboarding is reducing customer drop-off. Partnerships between insurers and e-commerce platforms are increasing visibility. Mobile payment penetration is enabling micro-premium collections. Younger populations are driving digital insurance demand. These factors are accelerating rapid growth of e-commerce-based microinsurance distribution.

Microinsurance Market Regional Analysis

North America dominated the Microinsurance market and accounted for the largest revenue share of 34% in 2025, supported by strong digital insurance penetration, advanced fintech infrastructure, rising adoption of embedded insurance solutions, and increasing partnerships between insurers and financial technology platforms. The region also benefits from high financial literacy, widespread mobile insurance adoption, and strong regulatory frameworks supporting micro-level risk coverage products. Growing integration of AI-driven underwriting, automated claims processing, and digital distribution channels continues to strengthen North America’s leadership position in the global market.

U.S. Microinsurance Market Insight

The U.S. Microinsurance market is witnessing strong growth due to rising demand for low-cost, flexible insurance products, increasing adoption of digital insurance platforms, and expanding use of embedded insurance in banking, e-commerce, and gig economy ecosystems. The country’s strong fintech ecosystem, widespread smartphone penetration, and advanced data analytics capabilities are enabling insurers to design personalized micro-level coverage products. In addition, growing awareness of financial risk protection among low-income and gig workers is driving market expansion.

Europe Microinsurance Market Insight

The Europe Microinsurance market remains a major contributor to global revenue, supported by strong regulatory frameworks, rising demand for inclusive insurance solutions, and increasing adoption of digital insurance platforms. Insurance providers across the region are focusing on expanding affordable coverage for health, life, and property risks through mobile and online channels. Growing emphasis on financial inclusion and protection for vulnerable populations is further supporting market growth across Europe.

U.K. Microinsurance Market Insight

The U.K. Microinsurance market is experiencing steady growth, driven by increasing adoption of digital insurance platforms, rising demand for flexible coverage solutions, and strong fintech innovation. Insurers are leveraging AI-based risk assessment and automated underwriting systems to expand low-cost insurance offerings. In addition, growing gig economy participation and rising consumer preference for on-demand insurance products are contributing to market expansion.

Germany Microinsurance Market Insight

The Germany Microinsurance market is expanding steadily due to increasing digital transformation in the insurance sector, strong regulatory support for financial protection products, and growing adoption of embedded insurance solutions. Insurance providers are focusing on improving accessibility through mobile platforms and simplifying policy issuance and claims processes. Rising awareness of risk protection among low-income groups is further driving market growth.

Asia-Pacific Microinsurance Market Insight

The Asia-Pacific Microinsurance market is expected to witness rapid growth, driven by rapid financial inclusion initiatives, large underinsured populations, increasing penetration of mobile-based insurance platforms, expanding fintech ecosystems, and strong government-backed social protection programs. Rising adoption of affordable microinsurance products across India, China, Indonesia, Vietnam, and other Southeast Asian countries is further accelerating regional market growth. Expanding digital payment infrastructure and mobile-first insurance distribution are significantly improving access to insurance in rural and semi-urban areas.

Japan Microinsurance Market Insight

The Japan Microinsurance market is witnessing steady growth due to increasing adoption of digital insurance platforms, rising demand for flexible coverage solutions, and growing focus on financial protection among aging populations. Insurance providers are integrating advanced analytics and digital onboarding systems to improve accessibility and efficiency in policy distribution.

China Microinsurance Market Insight

The China Microinsurance market is growing rapidly, driven by expanding digital insurance ecosystems, rising adoption of mobile financial services, and strong government support for inclusive financial protection programs. Increasing use of AI-driven underwriting, embedded insurance in e-commerce platforms, and rapid fintech expansion are significantly boosting market penetration. Growing awareness of risk protection among rural and urban populations is further supporting market expansion.

Microinsurance Market Share

The Microinsurance industry is primarily led by well-established companies, including:

- Allianz SE (Germany)

- AXA S.A. (France)

- Zurich Insurance Group (Switzerland)

- MetLife Inc. (U.S.)

- Prudential Financial Inc. (U.S.)

- AIG (American International Group Inc.) (U.S.)

- Munich Re Group (Germany)

- Swiss Re Ltd. (Switzerland)

- MAPFRE S.A. (Spain)

- Generali Group (Italy)

- Aviva plc (United Kingdom)

- Old Mutual Limited (South Africa)

- Prudential plc (United Kingdom)

- Ping An Insurance (China)

- China Life Insurance Company Limited (China)

- ICICI Prudential Life Insurance (India)

- HDFC Life Insurance Company Limited (India)

- LIC (Life Insurance Corporation of India) (India)

- MicroEnsure (United Kingdom)

- BIMA (Milvik) (Sweden)

- APA Insurance (Kenya)

- Jubilee Insurance (Kenya)

- Allianz Microinsurance (Germany)

- Pula Advisors (Kenya)

- AXA Climate (France)

Latest Developments in Microinsurance Market

- In April 2021, BIMA (Milvik), a digital microinsurance provider, expanded its mobile insurance distribution partnership with telecom operators in Bangladesh to strengthen low-cost life and health insurance penetration. The initiative leveraged mobile payments and USSD-based onboarding to increase access among low-income populations, significantly boosting microinsurance adoption in South Asia

- In August 2021, MicroEnsure (now Micro Insurance Company) strengthened its partnership network in East Africa by expanding collaboration with mobile network operators to scale embedded insurance distribution. The expansion focused on integrating insurance products into mobile airtime and financial services ecosystems, improving access for rural and underserved customers across Kenya and neighboring markets

- In November 2021, AXA Group enhanced its “AXA Emerging Customers” division by expanding microinsurance and inclusive insurance offerings across Africa and Asia. The initiative focused on low-income households by bundling life, health, and property microinsurance products with digital financial services and mobile distribution channels, reinforcing AXA’s position in inclusive insurance markets

- In March 2022, Allianz Partners expanded its microinsurance and embedded insurance solutions across Asia-Pacific through partnerships with digital platforms and fintech companies. The expansion included mobile-first insurance products covering health and travel protection, targeting underserved populations through low-cost digital distribution ecosystems

- In July 2023, Prudential plc expanded its inclusive insurance strategy in Asia through its “PRUHealth” and microinsurance initiatives across Indonesia and Vietnam. The company focused on affordable health protection products distributed via bancassurance and digital channels to improve insurance penetration among low- and middle-income groups

- In September 2023, Turaco, a tech-enabled microinsurance provider in Africa, completed the acquisition and integration of MicroEnsure Ghana operations. The transition strengthened digital insurance distribution in West Africa, enabling scalable, mobile-first insurance products for informal workers and low-income populations

- In May 2024, India’s Ayushman Bharat Digital Mission (ABDM) advanced its National Health Claim Exchange (NHCX) rollout to digitize insurance claims processing across insurers and hospitals. The initiative improved interoperability, reduced claim settlement time, and strengthened infrastructure for micro-level health insurance distribution across India’s public and private healthcare systems

- In October 2024, BIMA (Milvik) expanded its embedded microinsurance offerings in partnership with telecom operators in Africa, enhancing mobile-based health and life insurance access. The expansion leveraged AI-driven underwriting and mobile-first distribution to improve affordability and penetration in underinsured markets

- In February 2025, LeapFrog Investments increased its funding focus on microinsurance and financial inclusion platforms across Asia and Africa. The investment strategy targeted scalable digital insurance startups, supporting innovations in mobile microinsurance, AI underwriting, and embedded financial protection products for underserved populations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.