Global Microscopic Polyangiitis Market

Market Size in USD Million

USD

750.00 Million

USD

1,195.38 Million

2024

2032

USD

750.00 Million

USD

1,195.38 Million

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 750.00 Million |

Market Size (Forecast Year) |

USD 1,195.38 Million |

CAGR |

% |

Major Markets Players |

|

Microscopic Polyangiitis Market Size

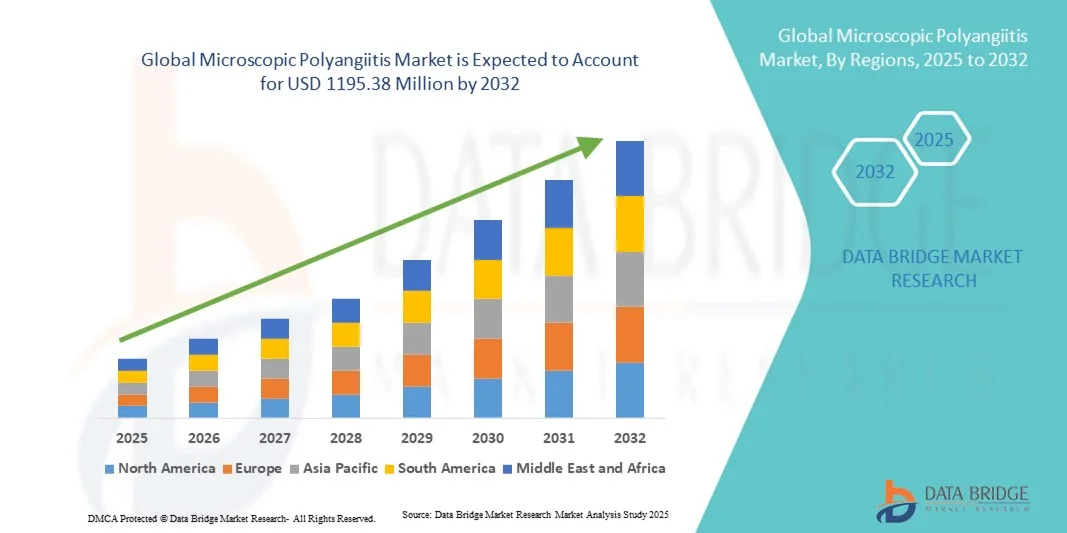

- The global microscopic polyangiitis market size was valued at USD 750.00 Million in 2024 and is expected to reach USD 1195.38 Million by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of autoimmune vasculitis disorders, including Microscopic Polyangiitis (MPA), and growing awareness among healthcare professionals and patients. Advances in diagnostics, such as ANCA testing, imaging techniques, and biopsy procedures, are enabling early detection, which is driving higher adoption of targeted therapies and management solutions

- Furthermore, the market is being propelled by the development of novel therapeutics, including immunosuppressants, biologics, and targeted anti-inflammatory agents. Collaborative initiatives between pharmaceutical companies, research institutions, and healthcare organizations are accelerating the introduction of innovative treatment options, thereby significantly boosting the growth of the Microscopic Polyangiitis market

Microscopic Polyangiitis Market Analysis

- The Microscopic Polyangiitis market is witnessing significant growth due to the rising prevalence of autoimmune vasculitis disorders, increasing awareness among healthcare professionals, and improvements in diagnostic methods such as ANCA testing, imaging, and biopsy. Early detection and timely intervention are driving adoption of immunosuppressants, biologics, and other targeted therapies across global healthcare systems

- North America dominated the microscopic polyangiitis market with the largest revenue share of 43.5% in 2024, driven by advanced healthcare infrastructure, strong presence of key pharmaceutical players, widespread adoption of diagnostic technologies, and supportive reimbursement policies for rare autoimmune disorders. The U.S. leads the region, benefiting from high clinical trial activity and early adoption of biologics

- Asia-Pacific is expected to be the fastest-growing region in the microscopic polyangiitis market during the forecast period (2025–2032), with a CAGR, owing to increasing healthcare expenditure, growing awareness of autoimmune diseases, and expanding patient access to innovative therapeutics in countries like Japan, China, and India

- The Injectable segment dominated the largest market revenue share of 54.3% in 2024, primarily due to the widespread use of intravenous Rituximab and Cyclophosphamide for induction therapy in severe or organ-threatening MPA cases

Report Scope and Microscopic Polyangiitis Market Segmentation

|

Attributes |

Microscopic Polyangiitis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Microscopic Polyangiitis Market Trends

Rising Awareness and Focus on Rare Autoimmune Disorders

- A significant and accelerating trend in the global microscopic polyangiitis market is the growing emphasis on early diagnosis and management of rare autoimmune vasculitis conditions. Increasing awareness among healthcare professionals and patients about the disease's clinical manifestations and progression is shaping treatment approaches and patient care

- For instance, specialized centers and academic hospitals are implementing advanced diagnostic protocols, including ANCA testing and imaging modalities, to identify Microscopic Polyangiitis at an earlier stage, enabling timely intervention and improved patient outcomes. Similarly, collaborative research networks are developing guidelines for standardized disease assessment, fostering consistent and evidence-based clinical practices

- Advancements in therapeutic research are also promoting the adoption of targeted treatments such as immunosuppressants, corticosteroids, and biologics, improving efficacy while minimizing adverse effects. Clinical trials are increasingly designed to evaluate patient response, monitor relapse rates, and optimize treatment regimens based on real-world evidence

- Integration of multidisciplinary care models is enabling coordinated management of Microscopic Polyangiitis, combining nephrology, pulmonology, rheumatology, and hematology expertise to address systemic manifestations of the disease. Comprehensive patient monitoring and follow-up programs facilitate early detection of complications and improve long-term prognosis

- This trend towards patient-centric, data-driven, and collaborative healthcare management is fundamentally reshaping expectations for care delivery in rare autoimmune disorders. Consequently, pharmaceutical companies and research organizations are investing in innovative therapies, patient education programs, and advanced monitoring solutions to enhance treatment outcomes

- The demand for effective and accessible microscopic polyangiitis treatment solutions is growing rapidly across both developed and emerging markets, driven by rising disease prevalence, increased awareness campaigns, and expanding healthcare infrastructure

Microscopic Polyangiitis Market Dynamics

Driver

Increasing Incidence and Rising Awareness of Autoimmune Vasculitis

- The increasing prevalence of autoimmune vasculitis, coupled with rising awareness among healthcare providers and patients, is a significant driver for the heightened demand for effective diagnosis and treatment of Microscopic Polyangiitis

- For instance, in March 2024, the Vasculitis Foundation launched a global awareness campaign to educate physicians and patients on early signs and management strategies for Microscopic Polyangiitis. Such initiatives are expected to drive market growth during the forecast period

- Enhanced screening protocols, broader availability of laboratory tests such as ANCA panels, and improved imaging techniques enable more accurate diagnosis, ensuring timely treatment initiation

- Furthermore, the growing focus on personalized medicine and development of targeted therapies, such as biologics and immunomodulatory agents, is improving patient outcomes and reducing disease-related morbidity

- Increasing investments by pharmaceutical companies in research and development, coupled with expanding clinical trial activities, are creating a robust pipeline of novel therapies, further propelling market growth

- Enhanced healthcare infrastructure, growing patient registries, and awareness campaigns are facilitating early diagnosis, improving treatment adherence, and fostering wider access to advanced therapies in both developed and emerging regions

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Emerging Regions

- High treatment costs and limited access to specialized therapies pose significant challenges to market expansion, particularly in low- and middle-income countries. Patients often face financial barriers in accessing costly biologics, immunosuppressants, and comprehensive diagnostic testing

- For instance, reports from healthcare surveys indicate that the out-of-pocket expenditure for rare autoimmune conditions, including Microscopic Polyangiitis, can exceed a household’s annual income in some regions, limiting treatment adherence

- Addressing these challenges through patient assistance programs, insurance coverage expansion, and government subsidies is crucial for improving accessibility and treatment outcomes. Pharmaceutical companies and non-profit organizations are increasingly implementing support programs to provide affordable medications and diagnostics

- In addition, limited awareness among primary care providers in rural or underserved areas can result in delayed diagnosis, suboptimal treatment, and higher risk of complications

- Overcoming these challenges through continued education of healthcare professionals, patient awareness initiatives, and strategic partnerships with governments and NGOs will be vital for sustained growth in the global microscopic polyangiitis market

- Strengthening healthcare infrastructure, reducing the cost of therapy, and expanding availability of diagnostic services are critical measures to ensure equitable access and enhance overall disease management

Microscopic Polyangiitis Market Scope

The market is segmented on the basis of drug, symptoms, diagnosis, route of administration, end-users, and distribution channel.

- By Drug

On the basis of drug, the Microscopic Polyangiitis market is segmented into Rituximab, Azathioprine, Cyclophosphamide, Prednisone, pipeline drugs, and others. The Rituximab segment dominated the largest market revenue share of 45.6% in 2024, driven by its strong clinical efficacy in inducing and maintaining remission in MPA patients. Rituximab’s targeted B-cell depletion therapy offers superior outcomes compared to conventional immunosuppressants, particularly for patients with severe renal involvement. The drug is widely recommended in international treatment guidelines and has high adoption among rheumatologists and nephrologists. Its use reduces relapse rates, minimizes glucocorticoid exposure, and improves long-term patient quality of life. Rituximab also benefits from established reimbursement policies in major markets, ensuring accessibility. Growing awareness of autoimmune vasculitis and early intervention protocols support consistent demand. Integration into hospital formularies and specialized clinics drives sustained utilization. The safety profile and proven long-term efficacy enhance clinician confidence. Combination therapy with corticosteroids further consolidates its market dominance. Clinical trials exploring maintenance dosing and optimized infusion schedules continue to strengthen adoption. Rituximab remains the preferred choice for both induction and maintenance therapy in MPA.

The Pipeline Drugs segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032, driven by innovative therapies under development aimed at targeting novel inflammatory pathways in MPA. These include biologics, small molecules, and targeted immunomodulators. Early-phase clinical trials have shown promising efficacy and safety results, creating strong anticipation among physicians and patients. Regulatory incentives for rare autoimmune disorders and orphan drug designations accelerate development. Advances in drug delivery, including subcutaneous formulations, improve patient convenience and adherence. Partnerships between biotech firms and academic institutions enhance the robustness of the pipeline. The segment benefits from rising awareness of unmet needs in patients intolerant to standard therapy. Positive trial outcomes, along with potential first-in-class approvals, are driving projected growth. Increasing global investment in autoimmune vasculitis research contributes to accelerated commercialization timelines. Pipeline drugs are poised to expand treatment options, improve outcomes, and potentially capture market share from conventional therapies.

- By Symptoms

On the basis of symptoms, the market is segmented into skin rashes, cough, nerve problems, eye irritation, seizures, loss of sensation, muscle pain, and others. The Skin Rashes segment dominated the largest market revenue share of 41.2% in 2024, as dermatological manifestations often serve as early clinical indicators of MPA, prompting physician evaluation and diagnostic testing. Visible symptoms drive rapid clinical consultation, resulting in timely treatment initiation. Skin involvement correlates with systemic disease severity, making it a critical marker for treatment monitoring. Its prevalence across patient populations ensures recurring clinical attention. Symptom visibility aids in early detection and reduces complications from delayed therapy. Dermatological monitoring is frequently incorporated into routine follow-ups, ensuring consistent healthcare engagement. The burden of skin manifestations also motivates patient adherence to immunosuppressive therapy. Recurrent rashes and vasculitic lesions contribute to repeated hospital visits, increasing healthcare utilization. Clinical awareness campaigns for autoimmune vasculitis emphasize dermatological signs, enhancing early diagnosis rates. Skin involvement is also used as a response indicator in clinical trials, reinforcing its significance in the market. Its frequent occurrence in both adults and elderly patients secures continued relevance.

The Seizures segment is expected to witness the fastest CAGR of 18.7% from 2025 to 2032, driven by recognition of neurological involvement in systemic vasculitis and the need for specialized management. Seizures indicate CNS complications and require multidisciplinary care, including neurologists, nephrologists, and rheumatologists. Advanced imaging and EEG diagnostics support rapid detection and intervention. Rising awareness of neurological manifestations increases demand for adjunctive therapies and monitoring tools. Integration with hospital-based autoimmune clinics facilitates early diagnosis and management. The growing prevalence of severe MPA cases in aging populations contributes to increasing clinical focus. Neurological complications significantly impact quality of life, further encouraging intervention. Research into neuroprotective agents and targeted biologics supports pipeline growth. Improved management protocols are enhancing patient outcomes and driving adoption of novel therapies. Specialized patient monitoring and telemedicine applications are increasing accessibility and treatment adherence.

- By Diagnosis

On the basis of diagnosis, the market is segmented into physical examination, blood test, urinalysis, tissue biopsy, and imaging testing. The Blood Test segment dominated the largest market revenue share of 48.5% in 2024, owing to its role in detecting ANCA (anti-neutrophil cytoplasmic antibodies), which are critical biomarkers for MPA diagnosis and disease monitoring. Blood tests are cost-effective, widely accessible, and frequently repeated for therapy assessment and relapse detection. Standardization of ANCA testing and incorporation in clinical guidelines support widespread adoption. Laboratories and hospital diagnostic units routinely conduct blood testing for autoimmune vasculitis. Integration with patient management protocols facilitates timely therapeutic interventions. Recurrent testing is needed during immunosuppressive therapy, sustaining long-term market demand. Blood testing allows early differentiation from other vasculitides and informs treatment selection. Clinical familiarity and established diagnostic pathways reinforce dominance. Patient compliance is higher due to minimally invasive procedures and rapid result availability. Blood tests also contribute to epidemiological studies and clinical research.

The Tissue Biopsy segment is expected to witness the fastest CAGR of 20.5% from 2025 to 2032, driven by its role in definitive diagnosis and organ-specific evaluation of vasculitis. Biopsies of renal, skin, or lung tissue provide histopathological confirmation and assess disease severity. Emerging minimally invasive biopsy techniques improve safety and patient acceptance. Biopsy results guide treatment selection, monitoring, and prognosis. Growing awareness among clinicians of the importance of early, accurate diagnosis accelerates adoption. Integration with hospital centers of excellence ensures access to specialized testing. Clinical trials increasingly require histological confirmation, supporting biopsy utilization. Technological improvements in imaging-guided biopsy enhance precision. Expansion of tertiary care facilities and diagnostic centers contributes to growth. Rising prevalence of severe or atypical MPA cases ensures sustained biopsy demand.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and injectable. The Injectable segment dominated the largest market revenue share of 54.3% in 2024, primarily due to the widespread use of intravenous Rituximab and Cyclophosphamide for induction therapy in severe or organ-threatening MPA cases. Hospital-based administration ensures safety and monitoring for adverse events. Injectable therapies demonstrate rapid efficacy in controlling systemic inflammation. Adoption is supported by clinical guidelines and insurance reimbursement policies. Hospitals and infusion centers maintain routine administration schedules, sustaining demand. Injectable biologics provide prolonged remission and reduce the need for long-term corticosteroid use. Patient adherence is higher under supervised administration. Injectable therapies also serve as standard-of-care comparators in clinical trials, reinforcing market share. Long-term efficacy and safety data support continued reliance on injectable formulations.

The Oral segment is expected to witness the fastest CAGR of 17.9% from 2025 to 2032, driven by convenience, patient preference, and the development of oral immunomodulators and corticosteroids for maintenance therapy. Oral drugs enable outpatient management, improve compliance, and reduce hospital visits. Advances in sustained-release formulations enhance pharmacokinetics and therapeutic effect. Increased adoption of oral therapy in mild-to-moderate cases supports growth. Telemedicine and e-prescription integration facilitate distribution. Patient-centric care models prioritize oral therapy convenience. Expanding pipeline for oral small molecules targeting vasculitis inflammation contributes to projected CAGR. Reduced administration costs encourage adoption in emerging markets.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, diagnostic centers, and others. The Hospitals segment dominated the largest market revenue share of 49.7% in 2024, owing to their role as primary care centers for diagnosis, induction therapy, and complex disease management. Hospitals provide integrated services including intravenous therapy, monitoring, biopsy procedures, and multidisciplinary care. Tertiary hospitals and centers of excellence attract severe MPA cases and clinical trial participation. Concentration of high-value services ensures continued revenue dominance. Established referral networks and specialist access reinforce adoption. Hospitals manage long-term follow-up and maintenance therapy, contributing to sustained demand. Hospital-based pharmacies facilitate drug procurement and controlled administration. Patient trust and institutional credibility support hospital preference. Insurance and reimbursement systems favor hospital-based therapy. Complex interventions and specialized care maintain high hospital utilization.

The Diagnostic Centres segment is expected to witness the fastest CAGR of 20.8% from 2025 to 2032, driven by the increasing role of laboratories in ANCA testing, urinalysis, and imaging for early detection and monitoring. Standalone diagnostic centers expand accessibility, especially in outpatient settings. Advanced testing platforms and automation improve efficiency and reliability. Collaborations with hospitals and clinics enhance service reach. Demand for regular monitoring, especially in maintenance therapy, fuels growth. Genetic and biomarker testing integration supports early diagnosis. Tele-diagnostics and home sample collection services accelerate adoption. The expansion of diagnostic capabilities in emerging markets contributes to sustained growth. Cost-effectiveness and patient convenience make diagnostic centers a rapidly growing segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 51.6% in 2024, primarily because most specialized MPA drugs, including biologics and immunosuppressants, are administered under clinical supervision. Hospital pharmacies ensure safe handling, dosing, and monitoring of high-cost therapies. They benefit from bulk procurement and integration into treatment protocols. Ongoing patient monitoring and follow-up care reinforce demand concentration. Hospitals provide the infrastructure for infusion, storage, and patient counseling. Insurance and reimbursement policies support hospital pharmacy distribution. Long-term therapy adherence programs rely on hospital pharmacy coordination. Standardization of care and centralized distribution ensure consistent supply.

The Online Pharmacy segment is expected to witness the fastest CAGR of 22.3% from 2025 to 2032, fueled by growing e-pharmacy adoption, patient preference for home delivery, and telemedicine integration. Patients increasingly access oral maintenance therapies and supportive medications online. Online channels enhance convenience, especially in regions with limited hospital access. Regulatory reforms supporting e-pharmacy growth facilitate expansion. Partnerships between pharmaceutical companies and digital platforms accelerate adoption. Wider geographical reach and cost-effectiveness further drive growth. Home delivery models improve adherence and patient satisfaction. Increasing awareness of rare autoimmune disorders encourages online ordering. Technological integration with mobile apps and e-prescriptions supports rapid adoption and growth.

Microscopic Polyangiitis Market Regional Analysis

- North America dominated the microscopic polyangiitis market with the largest revenue share of 43.5% in 2024, driven by advanced healthcare infrastructure, strong presence of key pharmaceutical players, widespread adoption of diagnostic technologies, and supportive reimbursement policies for rare autoimmune disorders. The U.S. leads the region, benefiting from high clinical trial activity and early adoption of biologics

- Consumers in the region increasingly benefit from the availability of specialized treatment centers, access to innovative therapies, and well-established healthcare networks, which enhance early diagnosis and effective management of microscopic polyangiitis

- This widespread adoption is further supported by high awareness of rare autoimmune disorders, advanced research infrastructure, and the growing preference for personalized treatment plans, establishing North America as a dominant region for microscopic polyangiitis care

U.S. Microscopic Polyangiitis Market Insight

The U.S. microscopic polyangiitis market captured the largest revenue share in 2024 within North America, fueled by a well-developed healthcare ecosystem and robust presence of specialized autoimmune disorder centers. Patients benefit from early adoption of biologics and immunosuppressive therapies, alongside high clinical trial activity focused on rare autoimmune vasculitis. Additionally, supportive reimbursement policies and increasing investments in rare disease research further contribute to market growth.

Europe Microscopic Polyangiitis Market Insight

The Europe microscopic polyangiitis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of autoimmune disorders and the need for early diagnosis and treatment. Increasing healthcare expenditure, coupled with the availability of advanced diagnostic facilities, is facilitating better disease management. European countries are also focusing on patient education, clinical research, and adoption of guideline-based therapies, fueling growth across both residential and institutional healthcare settings.

U.K. Microscopic Polyangiitis Market Insight

The U.K. microscopic polyangiitis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increased awareness of rare autoimmune diseases and a strong focus on specialized treatment options. Growing patient access to advanced therapies, coupled with government initiatives promoting early diagnosis and disease monitoring, is expected to stimulate market expansion. The country’s strong healthcare infrastructure and established pharmaceutical ecosystem further support growth.

Germany Microscopic Polyangiitis Market Insight

The Germany microscopic polyangiitis market is expected to expand at a considerable CAGR during the forecast period, fueled by a well-established healthcare system and increasing investment in autoimmune disorder research. Germany’s emphasis on personalized medicine, advanced diagnostic capabilities, and accessibility to innovative treatments is promoting better disease management. Collaboration between research institutions and pharmaceutical companies is further accelerating market development.

Asia-Pacific Microscopic Polyangiitis Market Insight

The Asia-Pacific microscopic polyangiitis market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare expenditure, rising awareness of autoimmune diseases, and expanding access to advanced therapeutics in countries such as Japan, China, and India. Government initiatives to improve rare disease diagnosis, growing number of specialty treatment centers, and investments in healthcare infrastructure are key factors driving regional growth.

Japan Microscopic Polyangiitis Market Insight

The Japan microscopic polyangiitis market is gaining momentum due to the country’s robust healthcare system, high awareness of autoimmune disorders, and increasing patient access to innovative therapies. Growing adoption of advanced diagnostic technologies and rising research activities are facilitating early diagnosis and effective disease management. Japan’s aging population is also likely to increase demand for specialized autoimmune treatments in both hospital and clinic settings.

China Microscopic Polyangiitis Market Insight

The China microscopic polyangiitis market accounted for the largest revenue share within Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, rapid urbanization, and increasing patient access to innovative therapeutics. Government initiatives to improve rare disease diagnosis, growing clinical research activity, and strong presence of domestic pharmaceutical companies are key factors propelling market growth. China is expected to play a pivotal role in the regional expansion of Microscopic Polyangiitis treatments.

Microscopic Polyangiitis Market Share

The Microscopic Polyangiitis industry is primarily led by well-established companies, including:

- Roche (Switzerland)

- Genentech (U.S.)

- Amgen (U.S.)

- Celltrion (South Korea)

- Teva Pharmaceutical Industries (Israel)

- InflaRx N.V. (Germany)

- Bristol‑Myers Squibb (U.S.)

- Novartis (Switzerland)

- Amerigen Pharmaceuticals Limited (China)

- Pfizer Inc. (U.S.)

- Sanofi S.A. (France)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company (Japan)

- Regeneron Pharmaceuticals (U.S.)

Latest Developments in Global Microscopic Polyangiitis Market

- In October 2024, Australia’s Pharmaceutical Benefits Scheme (PBS) listed the oral complement‑C5a receptor inhibitor Avacopan (TAVNEOS) for patients with severe MPA, following a recommendation by the Pharmaceutical Benefits Advisory Committee earlier in 2024. This marked a significant step in making a targeted therapy accessible for patients with serious disease manifestations

- In September 2024, a Phase 1 study was announced to evaluate the combination of Rituximab plus AB‑101 in patients with MPA and Granulomatosis with Polyangiitis (GPA). This trial represented a move toward innovative B-cell targeted therapies for autoimmune vasculitis, aiming to improve efficacy while reducing corticosteroid use

- In December 2024, a systematic review reported that rituximab achieved remission rates comparable to cyclophosphamide in childhood-onset AAV, including MPA. This evidence supported the expanding use of rituximab in pediatric populations and highlighted its favorable safety profile

- In January 2024, the KDIGO 2024 guideline update for ANCA-associated vasculitis formally incorporated Avacopan as an alternative to glucocorticoids for remission induction in GPA and MPA. This guideline change underscored the clinical recognition of Avacopan’s effectiveness and its role in reducing steroid-related adverse effects

- In March 2025, the British Society for Rheumatology (BSR) published updated management recommendations for AAV, including MPA. The guidance advised induction therapy with either cyclophosphamide or rituximab combined with glucocorticoids or Avacopan, reflecting the evolving standard of care and incorporation of newer targeted therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.