Global Microsporidiosis Treatment Market

Market Size in USD Billion

USD

285.50 Billion

USD

406.00 Billion

2025

2033

USD

285.50 Billion

USD

406.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 285.50 Billion | |

| USD 406.00 Billion | |

| % | |

|

Microsporidiosis Treatment Market Size

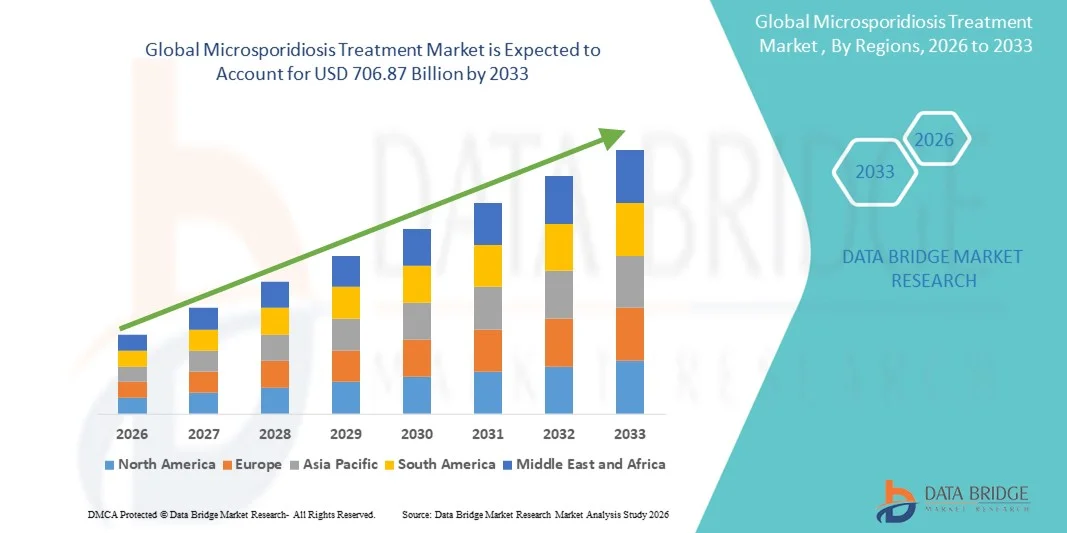

- The global microsporidiosis treatment market size was valued at USD 285.50 billion in 2025 and is expected to reach USD 406.00 billion by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely fueled by increasing prevalence of microsporidiosis infections, rising awareness among healthcare professionals and patients, and advancements in diagnostic and therapeutic technologies

- Furthermore, expanding healthcare infrastructure, early detection initiatives, and the development of targeted treatment options are driving the demand for microsporidiosis Treatment solutions, thereby significantly boosting the industry's growth

Microsporidiosis Treatment Market Analysis

- Microsporidiosis, a rare infectious disease caused by microsporidia, is increasingly gaining attention due to rising prevalence in immunocompromised patients and advancements in diagnosis and treatment options. The market growth is largely driven by improved awareness, early detection initiatives, and expansion of healthcare infrastructure across key regions

- Furthermore, increasing availability of targeted therapeutics, growing investment in infectious disease research, and rising adoption of standardized treatment protocols are accelerating the uptake of Microsporidiosis Treatment solutions, thereby significantly boosting the industry's growth

- North America dominated the microsporidiosis treatment market with the largest revenue share of 40.8% in 2025, supported by well-established healthcare infrastructure, high awareness of rare parasitic infections, and the presence of leading pharmaceutical companies specializing in infectious disease treatments. The U.S. accounted for the majority of this share due to early diagnosis, higher healthcare spending, and rapid adoption of innovative therapie

- Asia-Pacific is expected to be the fastest growing region in the microsporidiosis treatment market during the forecast period, registering a projected CAGR driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about microsporidiosis, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia

- The Oral segment dominated the largest market revenue share of 46.8% in 2025, driven by systemic efficacy and patient preference. Oral administration ensures consistent drug delivery and is applicable for both ART and Fumagillin treatments

Report Scope and Microsporidiosis Treatment Market Segmentation

|

Attributes |

Microsporidiosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Microsporidiosis Treatment Market Trends

Adoption of Advanced Diagnostic and Targeted Therapy Approaches

- Increasing use of molecular diagnostics, such as PCR-based testing, is enhancing early detection and precision treatment of microsporidiosis

- For instance, in March 2024, a hospital in Japan implemented routine PCR screening for immunocompromised patients, enabling targeted therapy and reducing morbidity

- Research on newer antiparasitic compounds is ongoing to improve efficacy and reduce side effects

- Combination therapies tailored to patient immune status are gaining traction in clinical practice

- Integration of rapid diagnostics with hospital electronic health records allows more timely prescription and treatment monitoring

- Telemedicine programs are also supporting adherence by enabling remote consultation and follow-up for patients on long-term therapy

- Evidence-based guidelines for managing chronic and disseminated infections are being widely adopted

- Overall, advancements in diagnostics and therapy optimization are shaping market trends toward more efficient and personalized microsporidiosis treatment

Microsporidiosis Treatment Market Dynamics

Driver

Rising Incidence and Increasing Awareness Among Healthcare Providers

- The growing prevalence of microsporidiosis, particularly among immunocompromised populations such as HIV/AIDS patients and transplant recipients, is driving the global market. Increased clinical awareness has led to earlier diagnosis and more widespread treatment

- For instance, in June 2022, a study in the Journal of Clinical Microbiology highlighted the rising number of diagnosed cases in immunocompromised patients in Southeast Asia, encouraging proactive screening and treatment protocols

- Healthcare providers are increasingly adopting standard treatment regimens such as Albendazole and Fumagillin for both intestinal and disseminated microsporidiosis. The rise in opportunistic infections due to organ transplants and chemotherapy has further pushed the need for effective treatment solutions

- Expanded clinical guidelines and physician education programs are contributing to faster adoption of recommended treatment protocols. Hospitals and clinics are now better equipped to identify microsporidial infections through molecular and serological diagnostic methods, enabling timely therapy initiation

- Awareness campaigns by healthcare organizations in endemic regions have increased patient visits and treatment adherence. Improved patient outcomes with early and appropriate therapy reinforce physician confidence in treatment efficacy

- Pharmaceutical companies are increasing distribution of antiparasitic drugs in regions with high microsporidiosis prevalence. The convenience of oral and injectable formulations encourages broader use in both outpatient and hospital settings

- The trend of combination therapies for immunocompromised patients has strengthened market demand for tailored treatment plans. Overall, the rising incidence of microsporidiosis and growing awareness among healthcare professionals are expected to drive market growth during the forecast period

Restraint/Challenge

Limited Drug Availability and Cost Constraints

- Restricted availability of specific antiparasitic medications, such as Fumagillin, in many regions poses a challenge for market expansion

- For instance, in September 2023, the World Health Organization highlighted limited access to critical anti-microsporidial drugs in low-income countries, impacting treatment coverage

- High treatment costs, particularly for hospital-administered intravenous formulations, may deter some patients from completing full courses. Lack of generic alternatives for certain medications increases financial burden on healthcare systems and patients

- Diagnostic challenges and delayed identification of microsporidiosis can lead to advanced disease requiring more intensive and costly interventions. In rural or resource-limited areas, limited laboratory infrastructure further restricts timely treatment initiation

- Treatment adherence is sometimes low due to the prolonged therapy duration for chronic or disseminated infections. Insurance coverage for antiparasitic drugs is limited in some regions, adding to out-of-pocket expenses for patients

- Supply chain interruptions for critical drugs have been reported in certain endemic countries, affecting continuity of care

- Efforts to improve drug accessibility through donation programs and government initiatives are ongoing but not yet sufficient

- Overall, limited drug availability, high costs, and infrastructure challenges remain key restraints affecting widespread market penetration

Microsporidiosis Treatment Market Scope

The Global Microsporidiosis Treatment market is segmented on the basis of treatment, diagnosis, dosage, route of administration, transmission, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Microsporidiosis Treatment market is segmented into Antiretroviral Therapy (ART), Albendazole, Fumagillin, and Others. The Antiretroviral Therapy (ART) segment dominated the largest market revenue share of 41.5% in 2025, driven by its critical role in managing Microsporidiosis in immunocompromised patients, especially those with HIV/AIDS. ART provides effective viral suppression, improving immune response and reducing susceptibility to opportunistic infections. Hospitals and specialty clinics prefer ART for its proven efficacy and standardized treatment protocols. Its established availability in hospital pharmacies ensures accessibility for patients. Integration with combination therapies enhances overall treatment outcomes. ART has consistently demonstrated reduced mortality and morbidity rates among high-risk populations. Patient adherence programs and government-supported ART initiatives further drive adoption. Continuous medical education encourages physicians to prescribe ART as first-line therapy. The segment benefits from extensive clinical trials and long-term safety data. ART’s dominance is reinforced by increasing prevalence of immunodeficiency disorders worldwide. Additionally, global funding programs and NGO initiatives ensure ART reaches underserved regions, maintaining its leadership in the treatment segment.

The Fumagillin segment is expected to witness the fastest CAGR of 11.8% from 2026 to 2033, owing to its efficacy against intestinal microsporidia infections and rising clinical awareness. Fumagillin is increasingly used in patients resistant to conventional therapy, and its adoption is supported by specialized infectious disease units. The drug is favored for targeted treatment, with fewer systemic side effects. Hospitals and research institutions are integrating Fumagillin protocols for complicated cases. Its usage is expanding due to increasing cases of zoonotic microsporidiosis from animal exposure. Clinical guidelines now recommend Fumagillin in combination with supportive care for severe infections. The drug is being manufactured in higher quantities, improving availability. Pharmaceutical companies are investing in R&D for new formulations and dosing schedules. Enhanced patient outcomes, shorter treatment durations, and better tolerability drive its adoption. Awareness campaigns among clinicians increase prescriptions in both urban and semi-urban hospitals. As incidence rates rise in both developing and developed countries, Fumagillin adoption is projected to accelerate steadily.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Blood Tests, Electron Microscopy, Polymerase Chain Reaction (PCR), Immunofluorescence Assays, and Others. The PCR segment dominated the largest market revenue share of 38.6% in 2025, due to its high sensitivity, specificity, and rapid detection of Microsporidia in clinical samples. PCR allows early and accurate identification, essential for immunocompromised patients. Hospitals and diagnostic labs widely use PCR for both routine testing and research purposes. Its non-invasive sampling and compatibility with multiple specimen types enhance its clinical appeal. PCR testing supports timely intervention, improving patient outcomes. Integration with automated lab platforms improves throughput and efficiency. Growing awareness of opportunistic infections in immunosuppressed populations drives demand. Clinical guidelines recommend PCR as a preferred diagnostic method in tertiary care centers. PCR’s reliability and reproducibility make it the standard for both epidemiological studies and routine screening. Adoption is reinforced by government and NGO programs targeting HIV/AIDS and transplant patients. Research institutions rely on PCR for pathogen monitoring. PCR kits are increasingly available in retail and online channels, expanding reach.

The Immunofluorescence Assay (IFA) segment is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, due to its ability to provide rapid, visual confirmation of Microsporidia in clinical samples. IFA is preferred in settings requiring immediate diagnosis. Increasing adoption in hospital laboratories and specialty clinics is driving growth. The method is particularly useful in detecting mixed infections and monitoring treatment efficacy. Rising investments in laboratory infrastructure, especially in emerging countries, support its market expansion. IFA kits are becoming easier to use, reducing reliance on highly skilled personnel. The segment benefits from integration with automated imaging systems for faster results. Continuous innovation in fluorescent dyes improves sensitivity and specificity. Training programs for laboratory technicians accelerate adoption. IFA is increasingly applied in research studies to track emerging Microsporidia strains. Hospitals and clinics favor IFA for its cost-effectiveness and reliability in early-stage detection.

- By Dosage

On the basis of dosage, the market is segmented into Tablet, Solution, Cream, Ointment, and Others. The Tablet segment dominated the largest market revenue share of 44.2% in 2025, driven by convenience, precise dosing, and high patient adherence. Tablets are preferred for both hospital-administered and outpatient treatments. Standardized tablet formulations allow integration into ART or Fumagillin regimens. The segment benefits from widespread availability in hospital and retail pharmacies. Tablets facilitate long-term therapy with consistent bioavailability. Hospitals often stock tablets due to stability and shelf life. Global supply chains ensure accessibility in developing regions. Patient compliance is easier compared to liquid or topical forms. Tablets can be combined with other medications to manage co-infections. The manufacturing process ensures cost-effectiveness, further boosting adoption. Educational initiatives encourage adherence to prescribed tablet regimens. Tablet use is standard across clinics, hospitals, and home-care settings, consolidating its market dominance.

The Solution segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by ease of administration in pediatric, elderly, and critically ill patients. Solutions are particularly useful in hospital settings requiring precise weight-based dosing. The segment benefits from improved formulation stability and palatability. Solutions are preferred in patients with swallowing difficulties. Hospitals and clinics increasingly adopt oral solutions for controlled drug delivery. Solution formulations enable rapid absorption and faster onset of action. Pharmaceutical companies are investing in flavored and ready-to-use solutions for better patient compliance. Solutions allow flexibility in treatment adjustments based on clinical response. The segment supports combination therapy protocols. Expansion of hospital pharmacies and online availability drives adoption. Solutions are also used in clinical trials and research studies for evaluating efficacy.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Topical, and Others. The Oral segment dominated the largest market revenue share of 46.8% in 2025, driven by systemic efficacy and patient preference. Oral administration ensures consistent drug delivery and is applicable for both ART and Fumagillin treatments. Hospitals and clinics rely on oral therapy for outpatient management and long-term prophylaxis. Ease of administration improves patient adherence, especially in home-care settings. Oral drugs are integral to standardized treatment protocols. Tablets and solutions form the majority of oral therapies. Oral administration supports combination regimens with antibiotics and antivirals. The segment benefits from extensive clinical trial validation and regulatory approvals. Pharmaceutical supply chains ensure wide availability. Oral therapy minimizes the need for hospital visits, enhancing convenience. Global disease prevalence drives adoption in both developed and developing nations.

The Topical segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, due to localized treatment needs in skin and ocular microsporidiosis. Topical formulations are preferred for direct action with minimal systemic exposure. Hospitals and specialty clinics adopt topical therapy in combination with systemic treatment. Increased awareness of ocular infections drives demand. Topical formulations are being optimized for better penetration and efficacy. Growth is supported by rising availability of creams and ointments in retail pharmacies. Topical therapy is cost-effective for mild infections. Adoption is further fueled by educational initiatives for healthcare providers. Patient-friendly applicators improve compliance. Research on novel topical agents accelerates market expansion.

- By Transmission

On the basis of transmission, the market is segmented into Animal Contact, Inhalation, Person-to-Person Transmission, Ingestion, and Direct Contact with the Conjunctiva. The Ingestion segment dominated the largest market revenue share of 40.7% in 2025, driven by its prevalence in contaminated food and water sources. Ingestion-based infections are common in immunocompromised patients, making preventive measures and timely treatment critical. Hospitals and clinics prioritize ingestion-related diagnosis for early intervention. Awareness campaigns regarding hygiene and sanitation contribute to recognition of this transmission route. The segment benefits from established clinical protocols for oral and systemic therapies. Laboratory testing for ingested pathogens is standardized and widely accessible. Dietary monitoring and patient counseling help reduce risk and improve treatment outcomes. Government programs in endemic regions emphasize controlling ingestion-based microsporidiosis. Research studies highlight ingestion as a major pathway for sporadic outbreaks. Hospitals stock relevant drugs such as Fumagillin and Albendazole to address ingestion-related infections. Rapid detection and management protocols strengthen the segment’s dominance. The high prevalence of ingestion-transmitted cases continues to drive consistent treatment demand.

The Animal Contact segment is expected to witness the fastest CAGR of 12.1% from 2026 to 2033, due to increasing human-animal interactions and zoonotic transmission awareness. Pet owners, veterinarians, and farm workers are key populations at risk. Hospitals and specialized clinics are actively monitoring patients exposed to livestock or exotic pets. Clinical guidelines now recommend screening for microsporidia in patients with animal exposure. Growth is fueled by rising cases in both developed and developing nations. Pharmaceutical companies are producing targeted therapies for zoonotic infections. Animal contact awareness campaigns and preventive strategies accelerate detection. The segment benefits from research on emerging Microsporidia strains in wildlife and domesticated animals. Outbreaks in rural and urban areas drive demand for prophylactic and therapeutic drugs. Hospitals stock specialized formulations for high-risk patients. Public health initiatives highlight the importance of monitoring animal contact exposure.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated the largest market revenue share of 47.5% in 2025, driven by the need for specialized care for immunocompromised patients, such as those with HIV/AIDS, cancer, or transplant recipients. Hospitals offer access to advanced diagnostic tools including PCR and immunofluorescence assays, which are critical for early detection. Multidisciplinary teams provide combination therapies, including ART, Fumagillin, and Albendazole. Hospital pharmacies ensure consistent drug availability. Hospitals also handle severe or systemic microsporidiosis cases requiring inpatient care. Government and NGO-supported treatment programs further increase hospital utilization. Clinical trials for new therapies are often hospital-based, boosting patient inflow. Hospitals provide monitoring and follow-up care for high-risk populations. Patient education programs improve adherence to long-term therapies. The presence of trained infectious disease specialists enhances hospital preference. Advanced infrastructure and access to latest formulations reinforce hospital dominance.

The Clinic segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, due to the rapid growth of specialized infectious disease and dermatology clinics. Clinics provide quicker consultations, flexible treatment schedules, and follow-up care, particularly for mild to moderate cases. Expansion of private healthcare networks and urbanization contribute to clinic adoption. Clinics offer targeted therapy regimens and personalized patient management. Increased awareness among physicians encourages early referral to clinics. Clinics stock ART, Fumagillin, and Albendazole for immediate treatment initiation. Telemedicine integration allows remote monitoring and guidance for patients. Clinics are expanding in semi-urban and rural areas, improving treatment accessibility. Educational initiatives enhance patient compliance in outpatient settings. Clinics often serve as the first point of contact for ingestion or animal contact transmission cases. Growing preference for outpatient management drives faster adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 43.8% in 2025, owing to direct access to critical medications for inpatient and outpatient treatment. Hospitals manage severe and systemic cases, ensuring timely availability of ART, Fumagillin, and Albendazole. Controlled access and physician-recommended dispensing enhance treatment adherence. Hospital pharmacies support combination therapy protocols. Bulk procurement and stable supply chains reinforce the segment’s market leadership. Specialized storage facilities maintain drug efficacy. Integration with hospital management systems ensures seamless patient care. Emergency treatments and outbreak management rely on hospital pharmacy stocks. Hospital pharmacies also facilitate clinical trial participation. Collaborative programs with NGOs and government initiatives boost reach. Hospitals provide comprehensive counseling and patient education at the pharmacy point.

The Online Pharmacy segment is expected to witness the fastest CAGR of 13.6% from 2026 to 2033, driven by convenience, expanding e-commerce platforms, and growing smartphone penetration. Patients prefer online ordering for long-term therapies and home delivery, especially in remote areas. Online pharmacies offer competitive pricing and subscription-based models for chronic treatments. Expansion of telemedicine services complements online drug delivery. Increased trust in certified online platforms accelerates adoption. Online channels facilitate access to both branded and generic formulations. Patient reviews and easy reordering improve adherence. Growth is fueled by rising awareness of Microsporidiosis and need for continuous therapy. Online pharmacies provide doorstep delivery for immunocompromised patients. Digital payment options and insurance integration enhance convenience. Educational content and dosage instructions are often provided online. Global expansion of e-pharmacy networks contributes to high CAGR growth.

Microsporidiosis Treatment Market Regional Analysis

- North America dominated the microsporidiosis treatment market with the largest revenue share of 40.8% in 2025

- Supported by well-established healthcare infrastructure, high awareness of rare parasitic infections, and the presence of leading pharmaceutical companies specializing in infectious disease treatments

- The market accounted for the majority of this share due to early diagnosis, higher healthcare spending, and rapid adoption of innovative therapies

U.S. Microsporidiosis Treatment Market Insight

The U.S. microsporidiosis treatment market captured a significant revenue share within North America in 2025, driven by advanced healthcare facilities, widespread availability of diagnostic tools, and increasing adoption of specialized anti-parasitic therapies. Growing awareness among clinicians and patients, coupled with rising government and private funding for infectious disease research, is further propelling the market’s expansion.

Europe Microsporidiosis Treatment Market Insight

The Europe microsporidiosis treatment market is expected to witness steady growth during the forecast period, driven by improving infectious disease management protocols, increasing access to healthcare facilities, and rising awareness of rare parasitic infections. Countries like Germany and the U.K. are leading in adoption due to their well-established healthcare systems and government-supported disease awareness programs.

U.K. Microsporidiosis Treatment Market Insight

The U.K. microsporidiosis treatment market is projected to expand at a noteworthy CAGR, supported by growing healthcare expenditure, enhanced diagnostic services, and increasing awareness about parasitic infections among both clinicians and patients. The country’s robust healthcare infrastructure and accessibility to treatment options are major growth drivers.

Germany Microsporidiosis Treatment Market Insight

The Germany microsporidiosis treatment market is anticipated to grow steadily, fueled by rising research initiatives, increasing availability of treatment options, and strong focus on infectious disease prevention and management. Germany’s advanced healthcare infrastructure and government-led health programs facilitate early diagnosis and effective treatment adoption.

Asia-Pacific Microsporidiosis Treatment Market Insight

The Asia-Pacific microsporidiosis treatment market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about microsporidiosis, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia. Rapid urbanization and expanding healthcare infrastructure further contribute to market growth.

Japan Microsporidiosis Treatment Market Insight

The Japan microsporidiosis treatment market is gaining traction due to increasing awareness about rare parasitic infections, growing healthcare expenditure, and advanced diagnostic capabilities. Rising demand for patient-friendly treatment options and specialized therapies is fueling market adoption.

China Microsporidiosis Treatment Market Insight

The China microsporidiosis treatment market accounted for the largest revenue share in the Asia-Pacific region in 2025, driven by the country’s expanding middle class, growing healthcare spending, rapid urbanization, and increasing awareness of microsporidiosis. Government initiatives to improve healthcare access and the availability of affordable treatment options further support market growth.

Microsporidiosis Treatment Market Share

The Microsporidiosis Treatment industry is primarily led by well-established companies, including:

• Gilead Sciences (U.S.)

• GlaxoSmithKline (U.K.)

• Janssen Pharmaceuticals (Belgium)

• Sigma-Tau Pharmaceuticals (Italy)

• Merck & Co. (U.S.)

• Bayer AG (Germany)

• Roche (Switzerland)

• Pfizer (U.S.)

• Takeda Pharmaceutical Company (Japan)

• Cipla (India)

• Sun Pharmaceutical Industries (India)

• Novartis (Switzerland)

• AbbVie (U.S.)

• Astellas Pharma (Japan)

• Sanofi (France)

Latest Developments in Global Microsporidiosis Treatment Market

- In January 2025, a pilot study published in Ocular Immunology & Inflammation reported that 0.007% topical Fumagillin — used alone or in combination with other agents — successfully resolved cases of mild-to-moderate microsporidial stromal keratitis without the need for surgery. This suggests a promising non‑surgical treatment route for what was previously often a surgically treated eye disease

- In August 2025, a multi‑year outbreak (2022–2024) of microsporidial keratoconjunctivitis caused by Vittaforma corneae was reported from the Sea of Galilee in Israel. Patients treated with 0.02% topical Chlorhexidine achieved full recovery without scarring, demonstrating that simple, cost‑effective topical therapy can be effective in outbreak settings — a development that could shape public‑health response and drive demand for accessible treatments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.