Global Military Cloud Computing Market

Market Size in USD Billion

USD

12.83 Billion

USD

40.92 Billion

2025

2033

USD

12.83 Billion

USD

40.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 12.83 Billion | |

| USD 40.92 Billion | |

| % | |

|

Military Cloud Computing Market Overview

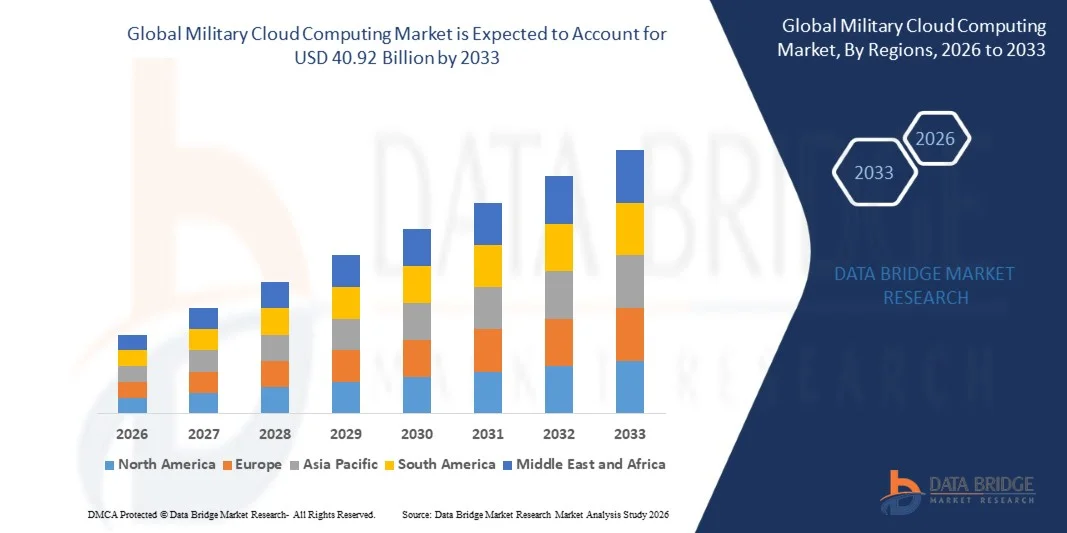

As per Data Bridge Market Research Analysis the Military Cloud Computing Market was valued at USD 12.83 billion in 2025 and is projected to reach USD 40.92 billion by 2033, growing at a CAGR of 15.60% from 2026 to 2033. market is experiencing robust growth, driven by the fundamental need for secure, scalable, and agile IT infrastructure to support modern data-centric warfare. The market is being reshaped by the transition from legacy on-premises data centers to advanced cloud environments—including public, private, hybrid, and tactical edge clouds—to host mission-critical systems for intelligence, surveillance, reconnaissance (ISR), command and control, logistics, and training .

This growth is propelled by the exponential surge in battlefield data, the increasing complexity of multi-domain operations, and the urgent requirement for real-time data sharing and AI-driven decision-making across allied forces .

Market Size & Forecast

- Global Market Value (2025): USD 12.83 Billion

- Expected Market Value (2033): USD 40.92 Billion

- Forecast CAGR (2026–2033): 15.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Military Cloud Computing Market in 2025, holding the largest revenue share of approximately 35.39% . This leadership is attributed to substantial U.S. defense cloud spending, major programs like the Joint Warfighting Cloud Capability (JWCC), and extensive use of secure cloud services for mission and ISR workloads .

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, fueled by rising defense budgets, military modernization, and increasing adoption of digital systems for command, ISR, and joint operations in countries like China, India, and Japan .

- The Cloud Service Models segment (IaaS, PaaS, SaaS) is expected to register the highest CAGR, as defense users seek scalable infrastructure and software capabilities without building every cloud layer themselves .

- The Hybrid Cloud deployment model is projected to lead, combining the security of private clouds with the scalability of public clouds to support sensitive workloads and large-scale data processing .

- Command, Control, and Mission Applications represent the largest application segment, as defense forces rely on cloud systems for operational data sharing and faster decision-making across domains .

- ISR Data Processing & Analytics is the fastest-growing application, driven by the need to manage and analyze vast data from sensors, satellites, and drones for intelligence and mission planning .

- Public Cloud is the dominant deployment model, favored for its scalability and ability to support secure collaboration and enterprise workloads .

Report Scope and Military Cloud Computing Market Segmentation

|

Attributes |

Military Cloud Computing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· General Dynamics Corporation (U.S.) · Microsoft (U.S.) · Amazon.com, Inc (AWS) (U.S.) · Leidos (U.S.) · Accenture (Ireland) · Oracle (U.S.) · Google LLC (U.S.) · IBM (U.S.) · SAIC (U.S.) · Atos SE (France) · Thales (France) · Capgemini (France) · BAE Systems (U.K.) · Cisco Systems, Inc. (U.S.) · Dell Inc (U.S.) · RTX (U.S.) · Lockheed Martin Corporation (U.S.) |

|

Market Opportunities |

· Integration of AI and Generative AI for advanced analytics and decision-support . · Growth of Tactical Edge Cloud for deployed and contested operations . · Expansion of sovereign and nationally controlled cloud environments . |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Military Cloud Computing Market Trends

Trend: Growth in Sovereign and Nationally Controlled Clouds

A significant trend is the rising preference for sovereign cloud environments to ensure full national ownership and control over sensitive defense data . Heightened national security concerns and evolving legal frameworks are driving defense organizations to invest in domestically hosted or nationally governed cloud platforms. This ensures data residency, compliance, and operational assurance while still providing the scalability and flexibility of cloud systems, reducing dependence on foreign-owned infrastructure, especially during geopolitical tensions .

Military Cloud Computing Market Dynamics

Key Market Driver: Increasing Complexity of Multi-Domain and Joint Operations

Contemporary military operations span land, sea, air, cyber, and space, requiring seamless data sharing across services and allied nations. Traditional siloed IT systems are insufficient to support the scale, speed, and integration required for modern warfare . Military cloud computing provides a unified digital backbone enabling data fusion, real-time information sharing, and coordinated decision-making across multiple domains. This operational necessity is a primary driver for the adoption of secure, scalable, and interoperable cloud-based architectures . For instance, in July 2025, Systematic launched SitaWare BattleCloud, a cloud-based command-and-control system designed for flexibility and real-time data access, drawing lessons from modern conflicts .

Key Restraint/Challenge: High Cybersecurity Threats and Integration Complexity

Security remains a primary challenge due to the high stakes of protecting sensitive military data from sophisticated cyberattacks. Moving classified data to cloud platforms, even secure ones, can create vulnerabilities . A notable example is the March 2023 accidental exposure of U.S. military emails via a misconfigured cloud server . Furthermore, the complexity of integrating modern cloud solutions with legacy defense IT systems poses a significant hurdle, requiring careful migration strategies and workforce training to ensure seamless interoperability and data integrity .

Key Market Opportunity: Shift Toward Digital Battlefield Operations and AI Integration

The modern digital battlefield, integrating unmanned systems, networked sensors, and autonomous platforms, generates vast data volumes that require real-time analysis . Military cloud computing is essential to manage and exploit this data, enabling faster, more informed decisions. The market opportunity lies in delivering secure, low-latency cloud platforms that integrate AI for advanced analytics and operate across centralized and edge environments, becoming core enablers of situational awareness and mission effectiveness .

Military Cloud Computing Market Scope

The military cloud computing market is segmented on the basis of offering, deployment, end user and application.

- By Offering

On the basis of offering, the military cloud computing market is segmented into cloud service models, cloud migration & modernization services, cloud integration & engineering services, managed cloud operations, cloud security, compliance & authorization services, and cloud cost management & governance (FinOps) . The cloud service models segment is projected to register the highest CAGR of 21.1% from 2026 to 2031, driven by defense users' need for scalable IaaS, PaaS, and SaaS to run mission applications and ISR data workloads without building infrastructure from scratch . The Cloud Security, Compliance & Authorization Services segment is also critical, as defense cloud adoption depends heavily on accreditation, data protection, and zero-trust architecture .

- By Deployment

On the basis of deployment, the military cloud computing market is segmented into public cloud, private cloud, hybrid cloud, community cloud, and tactical edge cloud . The hybrid cloud segment is anticipated to dominate with a 46.0% share in 2025, as it combines the security and control of private clouds with the scalability of public clouds for sensitive workloads and mission simulations . The Tactical Edge Cloud segment is one of the fastest-scaling growth areas, enabling compute and analytics closer to deployed forces in disconnected or low-bandwidth environments . Community Cloud is expected to witness the highest CAGR of 18.6% .

- By End User

On the basis of end user, the military cloud computing market is segmented into is classified into land forces, naval forces, air forces, space forces, and other defense agencies . The other defense agencies segment (including joint commands and intelligence agencies) is estimated to account for a 35.8% market share in 2026 due to managing large, data-heavy cloud workloads for cross-service operations and intelligence sharing . The Army segment held the majority share in 2025, driven by the need to manage data from large troop deployments, armored vehicles, and extensive sensor networks . The Air Force segment is expected to witness the highest CAGR of 13.4% .

- By Application

On the basis of application, the market is segmented into command, control & mission applications; ISR data processing & analytics; logistics & supply chain management; readiness & personnel management; training & simulation; and others . The command, control, and mission applications segment is expected to dominate the market, as defense forces rely on cloud systems for operational data sharing and faster multi-domain decision-making .

The ISR Data Processing & Analytics segment is projected to register the highest CAGR, driven by the need to manage exponential data from sensors, drones, and satellites for intelligence and mission planning .

Military Cloud Computing Market Analysis

North America dominated the market and accounted for the largest revenue share of approximately 35.39% in 2025 . Supported by high defense cloud spending, large-scale modernization programs like JWCC and CJADC2, and a strong ecosystem of cloud providers such as AWS, Microsoft, and Google, the region leads in adopting secure cloud environments for mission, ISR, and command systems .

U.S. Military Cloud Computing Market Insight

The U.S. market is the most significant globally, driven by the Department of Defense's strategic shift towards cloud computing via major contracts like JWCC (awarded to AWS, Google, Microsoft, and Oracle) and the Dell-Microsoft CETA worth USD 9.69 billion . The focus on modernizing command, logistics, and weapons systems, alongside investments in AI, zero-trust security, and tactical edge computing, positions the U.S. as the core innovation hub in the industry . The U.S. market was estimated at around USD 1.71 billion in 2025 .

Europe Military Cloud Computing Market Insight

The European market is projected to grow steadily, driven by defense modernization programs, increased focus on multi-domain interoperability, and rising investment in AI and autonomous systems across NATO and EU member states . Adherence to strict data sovereignty and security regulations drives demand for secure, sovereign cloud solutions. The Europe market reached a valuation of USD 1.49 billion in 2025 .

Asia-Pacific Military Cloud Computing Market Insight

The Asia-Pacific region is expected to witness the fastest growth, driven by increasing defense budgets, rapid military digitalization, and regional security concerns . Nations such as China, India, Japan, and Australia are investing heavily in military cloud infrastructure to enhance operational capabilities, improve data management, and support rapid decision-making . The region is leapfrogging legacy IT systems by adopting cloud-native architectures for real-time intelligence sharing and coalition coordination, making it a key growth engine for the market .

Japan Military Cloud Computing Market Insight

The Japan market is experiencing growth due to rising investments in advanced digital defense capabilities, automotive innovation, and road safety initiatives. The Japanese market in 2025 stood at around USD 0.13 billion . Integration of cloud technologies for defense and intelligence, alongside the country's focus on efficient and safe mobility solutions, is contributing to market growth.

China Military Cloud Computing Market Insight

China is projected to be one of the largest markets in the region, with 2025 revenues estimated at around USD 0.45 billion . The market is growing rapidly due to increasing urbanization, expanding transportation infrastructure, and a rising government focus on digitalization for defense. Growing adoption of AI-enabled and cloud platforms across commercial, automotive, and defense sectors is significantly boosting market demand .

Military Cloud Computing Market Share

The military cloud computing industry is primarily led by well-established companies, including:

- General Dynamics Corporation (U.S.)

- Microsoft (U.S.)

- Amazon.com, Inc (AWS) (U.S.)

- Leidos (U.S.)

- Accenture (Ireland)

- Oracle (U.S.)

- Google LLC (U.S.)

- IBM (U.S.)

- SAIC (U.S.)

- Atos SE (France)

- Thales (France)

- Capgemini (France)

- BAE Systems (U.K.)

- Cisco Systems, Inc. (U.S.)

- Dell Inc (U.S.)

- RTX (U.S.)

- Lockheed Martin Corporation (U.S.)

Latest Developments in Military Cloud Computing Market

- In January 2026, the U.S. Air Force awarded Amazon Web Services a USD 581.3 million contract to continue operating Cloud One, its enterprise military cloud platform, through 2028, highlighting the Pentagon's continued shift toward secure, scalable cloud computing .

- In January 2026, Microsoft won a USD 170.4 million contract from the U.S. Air Force to provide cloud computing services for the Cloud One program, reinforcing Microsoft Azure's role in supporting secure military cloud infrastructure .

- In December 2025, the U.S. Department of Defense awarded Hewlett Packard Enterprise a 10-year, USD 931 million contract to modernize DISA's most sensitive data centers with a hybrid on-premises cloud platform using HPE GreenLake, aiming to deliver public cloud-style capabilities with zero-trust security .

- In November 2025, Google Cloud won a new NATO contract, described as a multimillion-pound deal, to provide secure, isolated cloud services for military use, supporting classified data, AI, and analytics as part of NATO's move toward secure, sovereign military cloud infrastructure .

- In April 2025, Oracle received a task order under the U.S. Department of Defense's JWCC contract to provide the U.S. Army's Enterprise Cloud Management Agency with secure multicloud compute and storage services using Oracle Defense Cloud .

- In March 2025, Oracle announced it would provide air-gapped, isolated cloud and AI services to Singapore's military and defense ministry, marking its first defense cloud deal in Southeast Asia to enable secure AI-driven analysis for classified military networks .

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.