Global Military Radar Market

Market Size in USD Billion

USD

13.42 Billion

USD

24.71 Billion

2024

2032

USD

13.42 Billion

USD

24.71 Billion

2024

2032

| 2025 - 2032 | |

| USD 13.42 Billion | |

| USD 24.71 Billion | |

| % | |

|

Military Radar Market Size

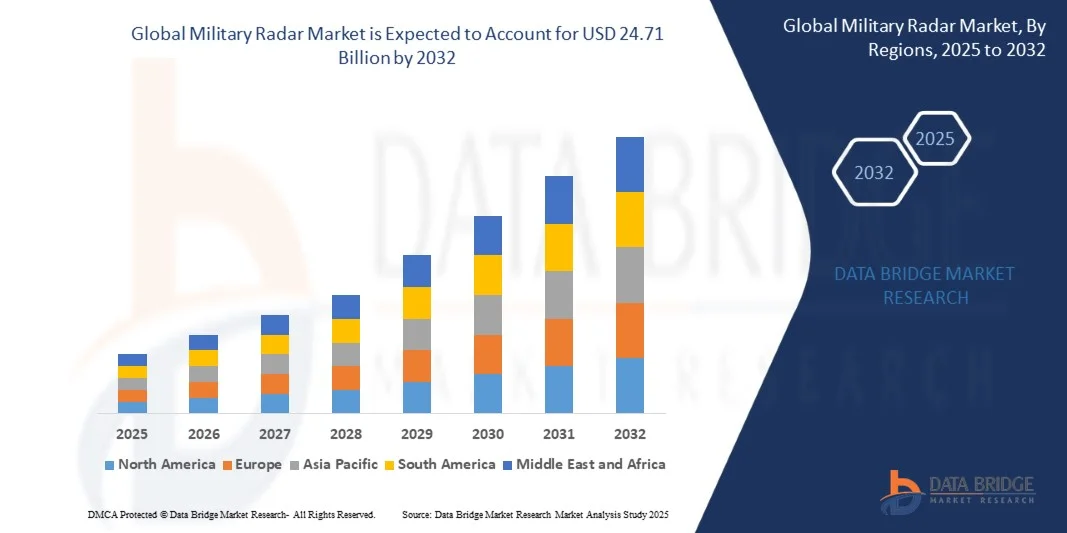

- The global military radar market size was valued at USD 13.42 billion in 2024 and is expected to reach USD 24.71 billion by 2032, at a CAGR of 7.93% during the forecast period

- The market growth is largely fuelled by the rising defense expenditure globally, increasing modernization of armed forces, and growing demand for advanced surveillance and threat detection systems

- Increasing investments in naval, air, and ground defense systems, along with technological advancements in radar systems such as AESA (Active Electronically Scanned Array) and multi-function radars, are supporting market expansion

Military Radar Market Analysis

- The market is witnessing rapid technological evolution with integration of AI, machine learning, and network-centric operations to improve target detection, tracking accuracy, and threat response time

- Expansion in unmanned aerial vehicles (UAVs), missile defense systems, and battlefield management solutions is contributing to increased demand for advanced radar systems

- North America dominated the military radar market with the largest revenue share of 39.5% in 2024, driven by increasing defense budgets, modernization of military infrastructure, and growing investments in advanced surveillance and threat detection systems. The presence of major defense contractors and technologically advanced military programs further strengthens regional dominance

- Asia-Pacific region is expected to witness the highest growth rate in the global military radar market, driven by rapid military modernization, increasing geopolitical tensions, and rising demand for advanced radar solutions in countries such as China, Japan, and South Korea

- Ground-based radars held the largest market revenue share in 2024, driven by their extensive deployment in border security, coastal surveillance, and terrestrial defense networks. These systems offer reliable detection of aircraft, missiles, and ground threats over wide areas, making them a preferred choice for national defense authorities

Report Scope and Military Radar Market Segmentation

|

Attributes |

Military Radar Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Military Radar Market Trends

“Increasing Adoption of Advanced Radar Systems in Defense Applications”

- The growing deployment of advanced radar systems is transforming the military surveillance and defense landscape by enabling real-time threat detection and situational awareness. High-resolution tracking and early warning capabilities allow for immediate response decisions, especially in combat zones where rapid detection of aerial, naval, and ground threats is critical. This results in enhanced operational efficiency, reduced security risks, and improved strategic decision-making. In addition, integration with mobile command centers ensures continuous monitoring in dynamic environments, supporting joint force operations across multiple domains

- The rising demand for radar solutions in remote and challenging terrains is accelerating the adoption of mobile, portable, and networked radar platforms. These systems are particularly effective in border security, maritime surveillance, and battlefield monitoring, helping reduce detection delays and ensuring timely military interventions. Governments are increasingly investing in ruggedized and all-weather radar units capable of functioning in extreme conditions, which boosts deployment reliability. The trend is further supported by defense modernization programs and multinational exercises that highlight the importance of versatile radar systems

- The integration of radar with artificial intelligence, electronic warfare systems, and command-and-control platforms is making these systems highly attractive for comprehensive defense operations. Military forces benefit from more accurate targeting, enhanced threat prioritization, and reduced operational risk, which ultimately improves overall mission effectiveness. Predictive analytics and automated threat recognition are enabling faster response times, while interoperability with UAVs and satellite networks provides multi-layered situational awareness. This integration strengthens defense readiness and tactical superiority

- For instance, in 2023, several defense agencies in Europe and North America reported enhanced situational awareness and faster threat neutralization after deploying next-generation multifunctional radar systems. These platforms improved target tracking accuracy and operational readiness, strengthening national security. The adoption also led to better coordination between air defense, naval units, and ground forces, showcasing the strategic advantages of modern radar deployment. Furthermore, successful field trials highlighted improved system reliability and lower false alarm rates

- While advanced radar adoption is accelerating strategic defense capabilities, its impact depends on continued innovation, system integration, and affordability. Manufacturers must focus on localized solutions, training programs, and high-performance designs to fully capitalize on growing demand. Continuous upgrades and modular designs ensure scalability for evolving mission requirements, while cost optimization and standardization across systems help expand adoption across mid-tier and smaller defense forces

Military Radar Market Dynamics

Driver

“Rising Defense Expenditure and Modernization of Military Infrastructure”

- Increasing defense budgets worldwide are driving investments in modern radar technologies. Governments are prioritizing the acquisition of multifunctional and network-centric radar systems to improve national security and combat readiness. Enhanced funding allows for research in high-frequency, long-range, and stealth radar capabilities, boosting innovation. Defense alliances and procurement programs are also accelerating global adoption of interoperable radar systems

- The growing emphasis on air, sea, and land defense surveillance is supporting market expansion, particularly in regions facing geopolitical tensions. Advanced radar ensures timely detection of hostile threats, enhancing military strategic capabilities. Countries are investing in multi-domain radar networks capable of detecting low-observable aircraft, drones, and ballistic missiles. This comprehensive coverage strengthens national security and operational confidence across multiple theaters of operation

- Adoption of radars in missile defense, early warning, and electronic warfare applications is increasing across military forces, reinforcing overall market growth. Radar systems integrated with missile defense networks improve interception accuracy and reduce response time, while electronic warfare compatibility enables threat jamming and spoofing detection. These enhancements contribute to the modernization of armed forces and elevate combat effectiveness across all branches

- For instance, in 2022, several NATO countries expanded their radar modernization programs, significantly increasing adoption of high-frequency and multifunctional radar systems for comprehensive battlefield awareness. This resulted in improved real-time threat tracking, enhanced communication across military units, and higher readiness levels. The investment also facilitated joint exercises and interoperability testing among allied nations, demonstrating operational cohesion

- While rising defense budgets and modernization efforts are fueling growth, sustained technological innovation and reliable production remain essential to maintain a competitive edge. Continuous R&D in radar miniaturization, energy efficiency, and automated target recognition is critical to meet evolving defense needs. Strategic partnerships between defense contractors and government agencies further drive adoption and market expansion

Restraint/Challenge

“High System Costs and Technological Complexity”

- The high acquisition and maintenance costs of advanced military radar systems restrict adoption among smaller or budget-constrained defense forces. Premium pricing can limit widespread deployment and accessibility. Lifecycle costs, including calibration, software upgrades, and personnel training, add additional financial burdens. Cost-effective alternatives are challenging to develop without compromising performance

- In many regions, there is a shortage of trained personnel capable of operating, maintaining, and integrating complex radar platforms. The absence of technical expertise and infrastructure reduces operational efficiency and slows deployment. Specialized training programs and simulation-based education are required to ensure effective system utilization. Workforce limitations may hinder timely deployment, particularly in developing countries

- Supply chain challenges, including component scarcity and logistics hurdles, may affect consistent radar production and system availability, impacting defense readiness. Delays in semiconductor chips, RF components, and high-precision sensors can slow program delivery and limit operational deployment. Geographic and political factors also affect the supply of critical materials, adding further risk to project timelines

- For instance, in 2023, several defense programs in Asia-Pacific experienced project delays due to limited availability of high-frequency radar components, affecting operational timelines and strategic deployment. These delays impacted training schedules, equipment commissioning, and interoperability testing. Manufacturers and defense agencies had to adjust procurement and operational plans to mitigate risks associated with component shortages

- While radar technologies continue to evolve, addressing cost, technical complexity, and supply chain constraints remains critical. Manufacturers and defense agencies must focus on modular designs, scalable production, and comprehensive training to unlock long-term market potential. Adoption of flexible procurement strategies, local sourcing, and advanced manufacturing techniques can further reduce operational risks and improve system accessibility globally

Military Radar Market Scope

The market is segmented on the basis of radar type, component, and application.

• By Radar

On the basis of radar type, the military radar market is segmented into Ground-based, Naval, Airborne, and Space-based systems. Ground-based radars held the largest market revenue share in 2024, driven by their extensive deployment in border security, coastal surveillance, and terrestrial defense networks. These systems offer reliable detection of aircraft, missiles, and ground threats over wide areas, making them a preferred choice for national defense authorities.

The Airborne segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing adoption of airborne early warning and control (AEW&C) systems for tactical surveillance, rapid threat detection, and enhanced operational flexibility. Airborne radars provide mobility, elevated vantage points, and integration with command-and-control systems, making them ideal for real-time mission-critical applications.

• By Component

On the basis of component, the military radar market is segmented into Antenna, Transmitter, Duplexer, Receiver, and Others. Antennas held the largest market revenue share in 2024, owing to their essential role in signal transmission, target acquisition, and accuracy in threat detection across diverse radar platforms.

The Transmitter segment is expected to witness the fastest growth rate from 2025 to 2032, driven by technological advancements in high-power, compact radar transmitters. These components enhance signal strength, range, and detection precision, supporting critical military operations and intelligence missions.

• By Application

On the basis of application, the military radar market is segmented into Air and Missile Defense, Intelligence, Surveillance and Reconnaissance (ISR), Navigation and Weapon Guidance, Space Situation Awareness, and Others. Air and Missile Defense systems held the largest market revenue share in 2024, driven by increasing investments in layered defense strategies and protection against aerial threats.

The ISR segment is expected to witness the fastest growth rate from 2025 to 2032, owing to rising demand for real-time battlefield intelligence, automated target recognition, and networked surveillance systems. These applications enhance situational awareness and support timely decision-making in defense operations.

Military Radar Market Regional Analysis

- North America dominated the military radar market with the largest revenue share of 39.5% in 2024, driven by increasing defense budgets, modernization of military infrastructure, and growing investments in advanced surveillance and threat detection systems. The presence of major defense contractors and technologically advanced military programs further strengthens regional dominance

- Defense forces in the region highly value real-time threat detection, multifunctional radar capabilities, and seamless integration with command-and-control systems. This enables rapid situational awareness and enhances operational readiness

- Widespread adoption is supported by strong government initiatives, strategic alliances, and extensive R&D in radar technologies, establishing North America as a critical hub for both domestic deployment and exports of military radar systems

U.S. Military Radar Market Insight

The U.S. military radar market captured the largest revenue share in 2024 within North America, fueled by the modernization of airborne, naval, and ground-based radar systems. The growing focus on missile defense, early warning, and intelligence, surveillance, and reconnaissance (ISR) applications is driving demand. Increasing integration with AI-based threat detection and network-centric warfare platforms is enhancing operational efficiency and reducing response times. Furthermore, partnerships between government defense agencies and private radar manufacturers are accelerating adoption of next-generation radar technologies.

Europe Military Radar Market Insight

The Europe military radar market is expected to witness the fastest growth rate from 2025 to 2032, driven by defense modernization programs and growing investments in maritime and aerial surveillance systems. Rising geopolitical tensions, combined with stringent defense regulations, are encouraging the deployment of advanced multifunctional radar platforms. European militaries are increasingly adopting radar solutions for ISR, missile defense, and navigation applications across land, air, and naval forces.

U.K. Military Radar Market Insight

The U.K. military radar market is expected to witness the fastest growth rate from 2025 to 2032, driven by government initiatives to upgrade existing radar infrastructure and deploy next-generation surveillance systems. The demand for integrated air defense, early warning, and coastal monitoring solutions is supporting growth. In addition, the U.K.’s emphasis on advanced defense technologies, combined with strong collaboration with domestic and international radar manufacturers, is boosting market expansion.

Germany Military Radar Market Insight

The Germany military radar market is expected to witness the fastest growth rate from 2025 to 2032, fueled by the adoption of high-performance radar systems for ISR, air and missile defense, and naval applications. Germany’s strong defense R&D ecosystem and focus on technological innovation promote adoption of multifunctional and networked radar systems. Integration with advanced command-and-control platforms ensures enhanced situational awareness and operational efficiency.

Asia-Pacific Military Radar Market Insight

The Asia-Pacific military radar market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing defense expenditure, regional security concerns, and modernization of military forces in countries such as China, India, Japan, and South Korea. The deployment of airborne, naval, and ground-based radar systems, along with AI-enabled threat detection and mobile radar platforms, is accelerating market growth. Government initiatives promoting domestic defense manufacturing and procurement further support adoption across the region.

Japan Military Radar Market Insight

The Japan military radar market is expected to witness the fastest growth rate from 2025 to 2032 due to rising defense spending, the need for advanced air and missile defense systems, and strategic focus on ISR capabilities. Japan’s adoption of networked radar solutions for early warning, maritime surveillance, and airspace monitoring is driving growth. Integration with allied defense systems and advanced command-and-control infrastructure further enhances operational effectiveness.

China Military Radar Market Insight

The China military radar market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding defense budget, rapid modernization of military forces, and development of domestic radar technologies. China is heavily investing in airborne, naval, and space-based radar systems, as well as advanced multifunctional radars for ISR and missile defense. The push towards smart and network-centric military capabilities, coupled with government-supported defense manufacturing, is significantly propelling the market.

Military Radar Market Share

The Military Radar industry is primarily led by well-established companies, including:

- L3Harris Technologies, Inc. (U.S.)

- BAE Systems (U.K.)

- Leonardo S.p.A. (Italy)

- General Dynamics Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- RTX (U.S.)

- Airbus (Netherlands/France)

- Thales (France)

- Saab (Sweden)

Latest Developments in Military Radar Market

- In December 2024, the Defence Acquisition Program Administration (DAPA) of South Korea approved an upgrade plan for the Boeing F-15K Slam Eagle combat aircraft. The enhancements focus on critical components, including advanced radar systems, to improve the operational capabilities, survivability, and mission efficiency of the F-15K jets currently deployed by the Republic of Korea Air Force (RoKAF). This upgrade is expected to strengthen the air force’s defense readiness and bolster market demand for radar and avionics modernization programs

- In July 2024, Raytheon, a business unit of RTX, secured a USD 1.2 billion contract to supply Germany with additional missile defense and Patriot air systems. The contract includes delivery of Patriot Configuration 3+ radars, launchers, command and control stations, spare parts, and support services. This development enhances Germany’s air defense infrastructure, improves threat detection and response capabilities, and positively impacts the global market for advanced military radar and missile defense systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.