Global Mobile Cloud Market

Market Size in USD Billion

USD

72.50 Billion

USD

256.32 Billion

2024

2032

USD

72.50 Billion

USD

256.32 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 72.50 Billion |

Market Size (Forecast Year) |

USD 256.32 Billion |

CAGR |

% |

Major Markets Players |

|

Mobile Cloud Market Size

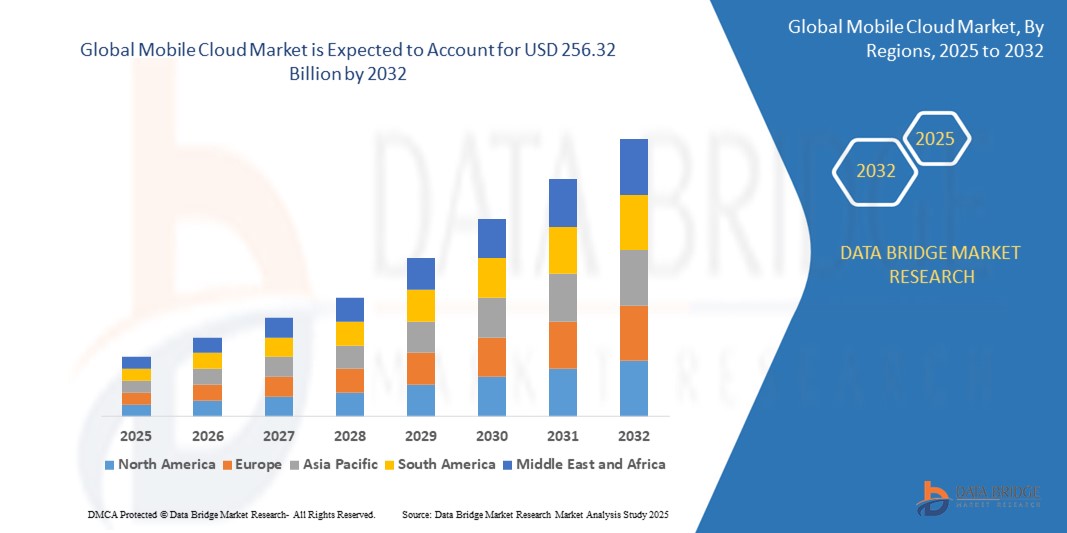

- The global mobile cloud market size was valued at USD 72.5 billion in 2024 and is expected to reach USD 256.32 billion by 2032, at a CAGR of 17.10% during the forecast period

- The market growth is largely fueled by the rapid expansion of mobile device usage and advancements in cloud computing infrastructure, enabling seamless access to applications, data, and services from any location

- Furthermore, the increasing demand for real-time data synchronization, enhanced user experiences, and scalable mobile-first business solutions is driving widespread adoption of mobile cloud platforms across enterprises and consumers, thereby significantly accelerating the industry's growth

Mobile Cloud Market Analysis

- Mobile cloud refers to the integration of cloud computing with mobile devices, allowing users to run applications and store data remotely, reducing the need for powerful on-device hardware and enabling continuous access to services over the internet

- The rising demand for mobile cloud solutions is primarily driven by the surge in remote work, increasing reliance on mobile applications, and the need for flexible, cost-effective computing resources that support productivity, collaboration, and entertainment on the go

- North America dominated the mobile cloud market with a share of 52.57% in 2024, due to the widespread adoption of smartphones, robust cloud infrastructure, and the strong presence of key cloud service providers

- Asia-Pacific is expected to be the fastest growing region in the mobile cloud market during the forecast period due to rapid smartphone proliferation, improving mobile network infrastructure, and aggressive government-led digitalization initiatives

- Public cloud segment dominated the market with a market share of 64.6% in 2024, due to its cost-effectiveness, scalability, and ease of access for mobile users. It enables rapid provisioning of computing resources and supports a wide variety of mobile applications, particularly those that experience fluctuating demand. The strong presence of global cloud service providers and widespread internet accessibility further support the dominance of the public cloud in mobile-centric deployments

Report Scope and Mobile Cloud Market Segmentation

|

Attributes |

Mobile Cloud Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Mobile Cloud Market Trends

“Rising Demand for Seamless and Specialized Mobile Cloud Services”

- The mobile cloud market is experiencing explosive growth driven by the proliferation of mobile devices and the need for on-the-go access to data and applications

- For instance, tech giants such as Amazon (AWS), Microsoft (Azure), Google Cloud, and Salesforce dominate the landscape, using their robust infrastructure to deliver mobile-optimized cloud solutions for streaming, mobile workforce management, gaming, finance, and healthcare

- The arrival of 5G technology is accelerating demand for real-time, high-speed cloud services with minimal latency, empowering more sophisticated mobile apps, remote collaboration, and immersive experiences

- Enterprises are rapidly adopting cloud-based mobile platforms for workforce management, centralized data storage, and productivity, while SMBs are projected to allocate more than half of their tech budgets to cloud services in 2025

- The surge in generative AI and embedded machine learning within cloud platforms is optimizing resource management, automating processes, enhancing mobile user experiences, and creating new mobile app capabilities

- Smaller and niche players are emerging with industry-specific solutions for sectors such as gaming, healthcare, and education, capitalizing on the trend toward verticalized cloud services

Mobile Cloud Market Dynamics

Driver

“Rising Cloud Adoption and Mobile Device Proliferation”

- The widespread adoption of cloud-based services, coupled with the skyrocketing use of smartphones, tablets, and other connected devices, remains the primary catalyst behind market expansion.

- For instance, organizations across North America, Asia Pacific, and Europe are transitioning critical applications to the mobile cloud for greater scalability, better data synchronization, and remote access, with public cloud spending expected to top USD723 billion globally in 2025

- Businesses—from startups to large enterprises—are leveraging mobile cloud platforms for application deployment, data storage, real-time communication, and efficient collaboration among distributed teams

- Mobile cloud services are seeing increased uptake in high-demand verticals such as entertainment (streaming, gaming), finance (mobile payments, banking), healthcare (mHealth apps), and travel, reflecting evolving consumer and enterprise needs

- Enhancements in wireless technology and the adoption of hybrid and multi-cloud strategies are further boosting mobile cloud’s performance, flexibility, and resilience

Restraint/Challenge

“Concerns Over Data Security, Privacy, and Regulatory Compliance”

- As mobile cloud adoption intensifies, concerns about data security, privacy, and regulatory compliance are prominent challenges for service providers and end-users

- For instance, reliance on cloud-based storage and real-time processing of sensitive mobile data heightens the risks of data breaches, unauthorized access, and compliance lapses—especially in regulated industries such as healthcare and finance

- Regulatory hurdles and the evolving patchwork of data sovereignty laws require significant investments in robust cybersecurity and localized data hosting, potentially slowing adoption for some organizations

- The complexity of managing secure access across diverse mobile endpoints and multiple cloud environments (public, private, hybrid) increases the security burden for IT departments and cloud vendors

- Smaller organizations may lack the expertise and resources to implement comprehensive security measures, leading to increased vulnerability and hesitance to migrate sensitive workloads to the cloud

Mobile Cloud Market Scope

The market is segmented on the basis of service model, deployment model, application, and end use.

- By Service Model

On the basis of service model, the mobile cloud market is segmented into Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). The Software as a Service segment dominated the largest market revenue share in 2024, driven by the growing adoption of cloud-based mobile applications across both consumer and enterprise environments. SaaS solutions offer seamless access, reduced device storage dependency, and real-time synchronization, making them especially popular among mobile-first users. Enterprises increasingly prefer SaaS for its scalability, subscription-based pricing, and minimal infrastructure maintenance, further fueling its widespread integration in mobile workflows.

The Platform as a Service segment is anticipated to witness the fastest growth rate from 2025 to 2032, propelled by the rising demand for flexible, scalable environments for mobile application development and testing. PaaS supports developers with pre-built backend services, streamlining the app lifecycle from creation to deployment, and enabling faster time-to-market. The increasing focus on DevOps, microservices, and containerization is further accelerating PaaS adoption among mobile-focused startups and enterprises.

- By Deployment Model

On the basis of deployment model, the mobile cloud market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud. The Public Cloud segment held the largest market revenue share of 64.6% in 2024, attributed to its cost-effectiveness, scalability, and ease of access for mobile users. It enables rapid provisioning of computing resources and supports a wide variety of mobile applications, particularly those that experience fluctuating demand. The strong presence of global cloud service providers and widespread internet accessibility further support the dominance of the public cloud in mobile-centric deployments.

The Hybrid Cloud segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing need to balance control and flexibility across mobile enterprise environments. Hybrid cloud allows organizations to run sensitive workloads on private infrastructure while leveraging public cloud scalability for mobile applications and content delivery. This deployment model is particularly appealing for businesses that require data sovereignty, compliance, and disaster recovery capabilities while maintaining mobile performance and scalability.

- By Application

On the basis of application, the mobile cloud market is segmented into Content Delivery, Data Storage, Mobile Application Development, and Cloud Gaming. The Content Delivery segment captured the largest market revenue share in 2024, supported by the surge in video streaming, social media usage, and mobile-first digital consumption. Mobile cloud content delivery networks (CDNs) enhance user experiences by reducing latency and buffering times, making them vital for media-rich applications. The proliferation of 5G and edge computing also contributes to the expansion of this segment.

Cloud Gaming is projected to register the fastest growth rate from 2025 to 2032, fueled by advancements in mobile GPUs, low-latency cloud infrastructure, and consumer demand for high-performance gaming on smartphones and tablets. Cloud gaming eliminates the need for high-end mobile hardware by offloading game processing to the cloud, making premium gaming experiences more accessible to a broader audience. The entry of major tech firms into this space and the development of cross-platform streaming services are rapidly advancing this segment.

- By End Use

On the basis of end use, the mobile cloud market is segmented into Individual Users, Small and Medium Enterprises (SMEs), and Large Enterprises. The Individual Users segment held the largest revenue share in 2024, driven by the widespread use of cloud-based apps for storage, communication, media, and productivity on mobile devices. Increasing smartphone penetration, improved mobile broadband, and the reliance on cloud for personal data access and backup contribute significantly to segment dominance.

The Small and Medium Enterprises segment is expected to witness the fastest CAGR from 2025 to 2032, as mobile cloud services offer SMEs a cost-effective alternative to traditional IT infrastructure. With limited in-house resources, SMEs are leveraging mobile cloud platforms to drive agility, enable remote work, and scale operations efficiently. The growing availability of industry-specific mobile cloud tools tailored for SMEs is also accelerating adoption across diverse sectors including retail, education, and logistics.

Mobile Cloud Market Regional Analysis

- North America dominated the mobile cloud market with the largest revenue share of 52.57% in 2024, driven by the widespread adoption of smartphones, robust cloud infrastructure, and the strong presence of key cloud service providers

- The region's mature mobile ecosystem and high-speed connectivity support seamless access to mobile cloud applications across sectors such as BFSI, healthcare, and media

- The demand for scalable and flexible solutions, coupled with the growing trend of remote work and mobile workforce, further accelerates mobile cloud adoption across both enterprises and individual users

U.S. Mobile Cloud Market Insight

The U.S. mobile cloud market captured the largest revenue share within North America in 2024, fueled by rapid digital transformation, high mobile device penetration, and strong enterprise demand for scalable, cloud-based mobility solutions. Businesses across finance, healthcare, media, and retail are embracing mobile cloud services to streamline operations, enhance mobile app performance, and deliver seamless user experiences. The increasing reliance on mobile apps for remote collaboration, video streaming, mobile banking, and e-commerce continues to push demand. Moreover, the U.S. benefits from early adoption of cloud-native technologies, wide-scale deployment of edge computing, and strong integration with AI and analytics, which collectively strengthen its mobile cloud market outlook.

Europe Mobile Cloud Market Insight

Europe is projected to experience robust growth in the mobile cloud market during the forecast period, supported by digitalization efforts, strict data protection regulations, and an increasing shift toward mobile-first business models. The region benefits from well-developed digital infrastructure and high mobile internet penetration, enabling widespread adoption of mobile cloud applications across both public and private sectors. As businesses focus on improving agility, efficiency, and user engagement, mobile cloud platforms are being increasingly deployed in industries such as education, healthcare, retail, and media. The rising demand for secure, GDPR-compliant mobile cloud solutions further drives the market in this region, along with innovation in mobile app development and mobile workforce enablement.

U.K. Mobile Cloud Market Insight

The U.K. mobile cloud market is anticipated to grow at a strong CAGR, driven by high demand for enterprise mobility, digital banking, and online services. The country’s mature ICT infrastructure, high smartphone usage, and progressive approach to digital transformation have created a conducive environment for mobile cloud adoption. Sectors such as fintech, healthcare, and e-commerce are actively investing in mobile cloud solutions to enhance service delivery and operational agility. The government’s focus on smart public services and secure cloud environments, combined with the increasing popularity of mobile learning and mobile healthcare, continues to strengthen demand across both consumer and enterprise markets.

Germany Mobile Cloud Market Insight

Germany’s mobile cloud market is expected to register steady growth during the forecast period, backed by its strong industrial base and growing emphasis on secure cloud computing. The manufacturing and automotive sectors are key adopters of mobile cloud platforms to enable real-time data access and streamline mobile workflows. German enterprises value privacy, control, and data sovereignty, leading to growing demand for hybrid mobile cloud models. With ongoing investments in Industry 4.0, smart factories, and workforce mobility, Germany is expanding mobile cloud usage in industrial applications and also in healthcare, education, and public administration.

Asia-Pacific Mobile Cloud Market Insight

Asia-Pacific is poised to grow at the fastest CAGR from 2025 to 2032, driven by rapid smartphone proliferation, improving mobile network infrastructure, and aggressive government-led digitalization initiatives. The region’s dynamic economies—particularly China, India, and Japan—are embracing mobile cloud technologies to support innovation in education, commerce, finance, and entertainment. The affordability of mobile devices and cloud services, coupled with a growing tech-savvy population, is significantly expanding mobile cloud adoption. Startups and enterprises alike are turning to mobile cloud platforms to scale their services, improve mobile app performance, and reach wider audiences. The region's rising demand for on-demand video, mobile payments, and cloud gaming further fuels market momentum.

Japan Mobile Cloud Market Insight

The Japan mobile cloud market is gaining traction due to its highly advanced telecommunications infrastructure and increasing reliance on cloud-enabled mobile services. Japanese consumers and businesses are progressively integrating mobile cloud platforms for productivity, collaboration, and security across personal and enterprise environments. The rise of smart homes, connected vehicles, and AI-powered mobile applications is fueling demand for responsive and reliable mobile cloud solutions. In addition, Japan’s aging population is driving the development of mobile cloud-based healthcare tools that offer accessibility, remote monitoring, and ease of use, further expanding the country’s application scope.

China Mobile Cloud Market Insight

China accounted for the largest revenue share in the Asia-Pacific mobile cloud market in 2024, supported by a booming digital ecosystem, fast-growing smartphone penetration, and government support for smart infrastructure and digital services. Cloud-powered mobile applications are widely used across sectors such as education, healthcare, e-commerce, and online gaming. Major domestic tech firms are leading innovation in mobile cloud platforms, offering cost-effective and scalable solutions tailored to local user needs. With strong policy backing, rapid urbanization, and increasing investment in smart city projects, China continues to lead the regional market, making mobile cloud solutions more accessible to enterprises and consumers alike.

Mobile Cloud Market Share

The mobile cloud industry is primarily led by well-established companies, including:

- Google LLC (U.S.)

- T-Mobile (U.S.)

- AT&T (U.S.)

- SAP (Germany)

- IBM (U.S.)

- Oracle (U.S.)

- Salesforce (U.S.)

- Intel (U.S.)

- Red Hat (U.S.)

- Cisco (U.S.)

- Microsoft Corporation (U.S.)

- VMware (U.S.)

- Huawei (China)

- Amazon (U.S.)

- Alibaba (China)

Latest Developments in Global Mobile Cloud Market

- In November 2024, ZTE Corporation, in collaboration with China Mobile, launched an AI-Driven Green Telco Cloud solution featuring diverse hardware architectures. By integrating artificial intelligence to enhance energy efficiency in telco cloud environments, the solution underscores growing momentum toward sustainable, intelligent infrastructure. This initiative strengthens China's position in energy-optimized mobile cloud innovation and sets a benchmark for AI integration in telco-grade cloud solutions

- In October 2024, Zoom Video Communications launched its Zoom Phone cloud solution in India, beginning with the Maharashtra Telecom Circle (Pune). As India’s first licensed cloud PBX service approved by the DoT, this move marks a significant expansion of enterprise-grade mobile cloud communication in one of the fastest-growing telecom markets, reinforcing India’s transition toward cloud-based voice and collaboration platforms

- In February 2024, a joint innovation by China Mobile and Huawei was recognized with the “Compute-enabled Innovative Application” award by China's MIIT-backed publication. The acknowledgment of their Mobile Cloud Phone initiative highlights the strategic role of cloud-powered mobile experiences in advancing 5G services, enhancing user accessibility, and driving adoption of compute-rich mobile cloud applications across China

- In October 2023, Bharti Airtel launched Airtel CCaaS (Contact Center as a Service)—India’s first omni-channel enterprise cloud contact center platform. This offering expands the scope of enterprise cloud communication by providing a unified experience across channels, accelerating mobile cloud adoption in India’s enterprise landscape and reinforcing Airtel’s leadership in business cloud services

- In March 2022, Nokia introduced its Adaptive Cloud Networking solution at MWC 2022 to enable agile, automated, and consumable service provider cloud networks. This development supports telcos in modernizing their infrastructure, reinforcing the shift toward programmable, scalable cloud environments critical for advancing mobile cloud services globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.