Global Mobile Handset Protection Market

Market Size in USD Billion

USD

45.06 Billion

USD

118.52 Billion

2025

2033

USD

45.06 Billion

USD

118.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 45.06 Billion | |

| USD 118.52 Billion | |

| % | |

|

Mobile Handset Protection Market Overview

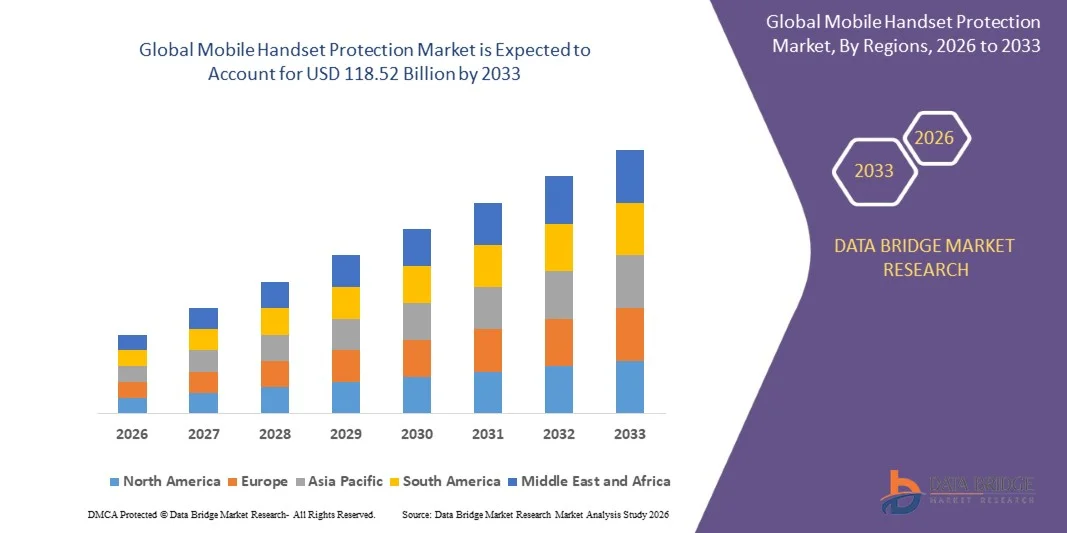

The Mobile Handset Protection Market was valued at USD 45.06 billion in 2025 and is projected to reach USD 118.52 billion by 2033, growing at a CAGR of 12.85% from 2026 to 2033. The market is experiencing strong growth driven by increasing smartphone penetration, rising consumer awareness regarding device protection plans, and the growing cost of premium smartphones and connected mobile devices. The expansion of digital insurance platforms, carrier-based protection programs, and manufacturer-backed extended warranty services is further supporting market development across both developed and emerging economies.

The increasing frequency of accidental damage, screen breakage, liquid damage, theft, and device malfunctions is encouraging consumers and enterprises to invest in comprehensive handset protection solutions. Mobile network operators, device manufacturers, and insurance providers are increasingly offering bundled protection plans that include repair, replacement, technical support, and cybersecurity coverage, enhancing customer value and service adoption. In addition, advancements in digital claims processing, AI-driven fraud detection, and app-based service management are streamlining customer experiences and improving claim settlement efficiency, making handset protection services more accessible and attractive to a broader consumer base.

Key Market Trends & Insights

- North America dominated the mobile handset protection market with the largest revenue share of approximately 39.4% in 2025, supported by high smartphone ownership rates, widespread adoption of premium devices, strong consumer awareness regarding mobile insurance services, and the presence of major telecom operators, insurers, and smartphone manufacturers offering bundled protection programs.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 14.1% from 2026 to 2033. Growth is driven by rapid smartphone adoption, increasing disposable incomes, rising sales of premium mobile devices, expansion of digital insurance platforms, and growing awareness of handset protection services across countries such as China, India, Japan, and South Korea.

- The Carrier Handset Protection segment held the largest market revenue share of approximately 42.6% in 2025 driven by the widespread availability of protection plans bundled with mobile subscriptions and device financing programs. Mobile network operators benefit from strong customer relationships, streamlined billing systems, and extensive distribution networks, making carrier-based protection plans highly accessible to consumers.

- The OEM Protection segment is projected to register the fastest growth at a CAGR of 14.3% from 2026 to 2033, driven by increasing adoption of manufacturer-backed protection programs such as extended warranties, accidental damage coverage, and device replacement services. Growing consumer trust in original equipment manufacturer service quality and repair standards is accelerating segment expansion.

- The Monthly Fee segment held the largest market revenue share of approximately 51.8% in 2025 driven by growing consumer preference for subscription-based protection services that offer affordable recurring payments and continuous coverage throughout the device lifecycle. Monthly plans are particularly popular among premium smartphone users seeking comprehensive protection and flexible service options.

- The Billed by Carrier/OEM segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033, driven by increasing integration of handset protection services into carrier contracts and manufacturer financing programs. The convenience of automatic billing and bundled service offerings is supporting rapid adoption across both developed and emerging markets.

- The Retail Chains segment held the largest market revenue share of approximately 39.7% in 2025 driven by strong in-store device sales, direct customer interaction, and the ability to promote handset protection plans at the point of purchase. Retailers continue to play a significant role in educating consumers about device protection benefits and coverage options.

- The E-commerce/Online segment is projected to register the fastest growth at a CAGR of 15.6% from 2026 to 2033, driven by rising online smartphone purchases, digital insurance platforms, and increasing consumer preference for app-based policy enrollment and claims management. Growing digitalization and the expansion of direct-to-consumer protection services are accelerating segment growth globally.

Market Size & Forecast

- Global Market Value (2025): USD 45.06 Billion

- Expected Market Value (2033): USD 118.52 Billion

- Forecast CAGR (2026–2033): 12.85%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Mobile Handset Protection Market Segmentation

|

Attributes |

Mobile Handset Protection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• AT&T Intellectual Property (U.S.) |

|

Market Opportunities |

• Expansion Of Embedded Protection Plans Through Mobile Network Operators And Smartphone Manufacturers • Growing Adoption Of AI Powered Claims Management And Digital Device Protection Services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Mobile Handset Protection Market Trends

Trend: Growth In Embedded Device Protection Ecosystems And AI-Driven Claims Management

Increasing demand for comprehensive smartphone protection solutions is transforming the mobile handset protection market across consumer and enterprise segments. The rising cost of premium smartphones, foldable devices, and connected mobile technologies is encouraging consumers to invest in protection plans that cover accidental damage, theft, loss, mechanical failures, and cybersecurity risks. Traditional warranty offerings are increasingly being replaced by subscription-based protection ecosystems that provide continuous coverage and value-added services.

Mobile device manufacturers and telecom operators are increasingly integrating embedded protection plans, For instance at the point of sale, to improve customer retention and enhance device ownership experiences. Companies such as Apple, Samsung, and major telecom carriers offer bundled protection programs that include screen repair, device replacement, technical support, and theft coverage. In addition, digital claims platforms are utilizing artificial intelligence to automate claim verification and fraud detection, reducing processing times and improving customer satisfaction.

The rapid expansion of premium smartphone adoption and device financing programs is further increasing demand for handset protection services. In addition, insurers and service providers are leveraging mobile applications for policy management, real-time claim tracking, and instant customer support. Industry data from 2025 indicates that smartphone repair costs for flagship devices frequently exceed USD 250–400 per incident, significantly increasing consumer willingness to purchase device protection plans and subscription-based coverage services.

Mobile Handset Protection Market Dynamics

Key Market Driver: Rising Smartphone Replacement Costs And Increasing Device Damage Incidents

Consumers worldwide are increasingly purchasing high-value smartphones featuring advanced displays, premium materials, and sophisticated hardware components. As device prices continue to rise, accidental damage, theft, liquid exposure, and mechanical failures create substantial financial risks for consumers, generating strong demand for handset protection solutions.

Mobile network operators, insurers, and device manufacturers are expanding protection offerings to cover a broader range of risks while improving customer convenience. For instance, premium smartphone models launched by leading manufacturers often exceed USD 1,000 in retail value, making repair and replacement expenses significant for consumers. As a result, many customers are opting for monthly subscription-based protection plans that provide affordable access to repair and replacement services.

Similarly, increasing smartphone usage for digital banking, e-commerce, remote work, and entertainment is making uninterrupted device functionality more important than ever. Industry estimates indicate that screen damage alone accounts for more than 50% of smartphone repair claims globally, supporting continued demand for handset protection programs across major markets.

Key Restraint/Challenge: Rising Fraudulent Claims And Complex Claims Processing Requirements

Despite strong market growth, handset protection providers face increasing challenges associated with fraudulent claims, identity verification issues, and operational complexities in claims management. Fraudulent damage reports, false theft claims, and device misuse can significantly increase costs for insurers and protection service providers.

In addition, managing device diagnostics, repair logistics, replacement inventories, and customer verification processes requires substantial operational resources. Variations in coverage policies, deductibles, and claim eligibility requirements can also create customer dissatisfaction and limit adoption among price-sensitive consumers. These challenges are particularly significant in emerging markets where insurance awareness and digital verification systems remain less developed.

Industry assessments indicate that fraudulent and disputed claims can account for approximately 8–12% of total handset protection claim volumes in certain markets, increasing operational expenses and placing pressure on provider profitability and service efficiency.

Key Market Opportunity: Expansion Of Subscription-Based Protection Services And Digital Insurance Platforms

The growing popularity of device-as-a-service models, smartphone financing programs, and digital insurance ecosystems is creating significant opportunities for handset protection providers. Consumers increasingly prefer flexible subscription services that combine device protection, technical support, cloud security, and replacement benefits under a single monthly payment structure.

Mobile operators and smartphone manufacturers are increasingly launching integrated protection programs, For instance covering accidental damage, theft, cyber threats, and extended warranty services, to improve customer loyalty and generate recurring revenue streams. In enterprise environments, businesses are adopting protection plans for employee-owned and company-issued mobile devices to minimize downtime and reduce IT support costs.

In addition, advancements in artificial intelligence, predictive analytics, and automated claims processing are improving operational efficiency and customer experience, creating opportunities across North America, Europe, and Asia-Pacific. Industry pilot programs conducted during 2025 utilizing AI-powered claims automation reported reductions of approximately 30–40% in claim processing times while improving fraud detection accuracy and customer satisfaction levels.

Mobile Handset Protection Market Scope

The market is segmented on the basis of protection provider, pricing model, and sales channel.

• By Protection Provider

On the basis of protection provider, the mobile handset protection market is segmented into Carrier Handset Protection, OEM Protection, Direct to Consumer Services, and Others. The Carrier Handset Protection segment held the largest market revenue share of approximately 42.6% in 2025 driven by the widespread availability of protection plans bundled with mobile subscriptions and device financing programs. Mobile network operators benefit from strong customer relationships, streamlined billing systems, and extensive distribution networks, making carrier-based protection plans highly accessible to consumers.

The OEM Protection segment is projected to register the fastest growth at a CAGR of 14.3% from 2026 to 2033, driven by increasing adoption of manufacturer-backed protection programs such as extended warranties, accidental damage coverage, and device replacement services. Growing consumer trust in original equipment manufacturer service quality and repair standards is accelerating segment expansion.

• By Pricing Model

On the basis of pricing model, the market is segmented into One-time Fee, Monthly Fee, and Billed by Carrier/OEM. The Monthly Fee segment held the largest market revenue share of approximately 51.8% in 2025 driven by growing consumer preference for subscription-based protection services that offer affordable recurring payments and continuous coverage throughout the device lifecycle. Monthly plans are particularly popular among premium smartphone users seeking comprehensive protection and flexible service options.

The Billed by Carrier/OEM segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033, driven by increasing integration of handset protection services into carrier contracts and manufacturer financing programs. The convenience of automatic billing and bundled service offerings is supporting rapid adoption across both developed and emerging markets.

• By Sales Channel

On the basis of sales channel, the market is segmented into Retail Chains, Brand Stores, and E-commerce/Online. The Retail Chains segment held the largest market revenue share of approximately 39.7% in 2025 driven by strong in-store device sales, direct customer interaction, and the ability to promote handset protection plans at the point of purchase. Retailers continue to play a significant role in educating consumers about device protection benefits and coverage options.

The E-commerce/Online segment is projected to register the fastest growth at a CAGR of 15.6% from 2026 to 2033, driven by rising online smartphone purchases, digital insurance platforms, and increasing consumer preference for app-based policy enrollment and claims management. Growing digitalization and the expansion of direct-to-consumer protection services are accelerating segment growth globally.

Mobile Handset Protection Market Regional Analysis

North America Mobile Handset Protection Market Insight

North America dominated the mobile handset protection market with the largest revenue share of 39.4% in 2025, supported by high smartphone penetration, widespread adoption of premium mobile devices, and strong consumer awareness regarding device protection services. Consumers in the region increasingly purchase handset protection plans to safeguard against accidental damage, theft, loss, and mechanical failures. The presence of major telecom operators, device manufacturers, and insurance providers offering bundled protection plans further supports market growth, making handset protection a standard component of smartphone ownership across both consumer and enterprise segments.

U.S. Mobile Handset Protection Market Insight

The U.S. mobile handset protection market captured the largest revenue share in 2025 within North America, fueled by increasing ownership of high-value smartphones and strong adoption of subscription-based protection plans. Consumers are increasingly seeking coverage for screen damage, device replacement, theft protection, and technical support services. The growing popularity of smartphone financing programs, carrier-bundled insurance offerings, and manufacturer-backed protection services such as AppleCare and Samsung Care+ continues to drive market expansion. In addition, advancements in digital claims processing and AI-powered customer support are enhancing the overall customer experience.

Europe Mobile Handset Protection Market Insight

The Europe mobile handset protection market is expected to witness significant growth from 2026 to 2033, primarily driven by rising smartphone replacement costs, increasing adoption of premium devices, and growing consumer awareness regarding mobile insurance services. Strong regulatory frameworks supporting consumer protection and increasing digitalization are encouraging adoption of comprehensive handset protection plans. The region is witnessing growing demand across both individual consumers and enterprise mobility programs, with protection services increasingly bundled into smartphone purchases and service contracts.

U.K. Mobile Handset Protection Market Insight

The U.K. mobile handset protection market is expected to witness strong growth from 2026 to 2033, driven by increasing dependence on smartphones for banking, shopping, communication, and entertainment activities. Consumers are increasingly investing in protection plans to mitigate repair and replacement expenses associated with premium devices. Furthermore, the country's mature telecommunications sector, widespread device financing programs, and expanding digital insurance ecosystem continue to stimulate demand for handset protection services.

Germany Mobile Handset Protection Market Insight

The Germany mobile handset protection market is expected to witness strong growth from 2026 to 2033, fueled by increasing smartphone ownership, rising adoption of premium mobile devices, and strong consumer focus on financial protection against device-related risks. Germany’s well-developed insurance sector and high levels of digital adoption support market expansion. Consumers are increasingly opting for comprehensive protection plans that include accidental damage coverage, theft protection, and extended warranty benefits, particularly for high-end smartphones and connected devices.

Asia-Pacific Mobile Handset Protection Market Insight

The Asia-Pacific mobile handset protection market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid smartphone adoption, increasing disposable incomes, and growing awareness of device protection services. Countries such as China, India, Japan, and South Korea are witnessing substantial growth in premium smartphone sales, creating strong demand for handset insurance and protection plans. The expansion of e-commerce platforms, digital payment systems, and mobile financing programs is further accelerating market growth across the region.

Japan Mobile Handset Protection Market Insight

The Japan mobile handset protection market is expected to witness strong growth from 2026 to 2033 due to high smartphone penetration, strong consumer preference for premium devices, and increasing reliance on mobile technology in everyday life. Japanese consumers place significant emphasis on device reliability and service quality, driving demand for comprehensive handset protection solutions. The integration of digital claims management platforms and advanced customer support services is further contributing to market growth across both consumer and business segments.

China Mobile Handset Protection Market Insight

The China mobile handset protection market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's massive smartphone user base, growing middle-class population, and increasing adoption of premium mobile devices. China represents one of the world's largest smartphone markets, creating substantial demand for device protection plans covering accidental damage, theft, and repair services. The rapid expansion of digital insurance platforms, strong participation from telecom operators, and growing smartphone financing programs are key factors driving market growth across the country.

Mobile Handset Protection Market Share

The Mobile Handset Protection industry is primarily led by well-established companies, including:

• AT&T Intellectual Property (U.S.)

• SquareTrade, Inc. (U.S.)

• Asurion (U.S.)

• Liberty Mutual Insurance (U.S.)

• American International Group, Inc. (U.S.)

• Verizon (U.S.)

• Sprint.com (U.S.)

• T-Mobile USA, Inc. (U.S.)

• Pier Insurance Managed Services Ltd (U.K.)

• Brightstar Corp. (U.S.)

• Safeware (U.S.)

• XCellIns Technologies Pvt. Ltd. (India)

• Deutsche Telekom AG (Germany)

• Xiaomi (China)

• T-Mobile (Germany)

• Samsung (South Korea)

• Sprint Corporation (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.