Global Monolayer Cast Films Market

Market Size in USD Billion

USD

3.93 Billion

USD

5.48 Billion

2025

2033

USD

3.93 Billion

USD

5.48 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.93 Billion | |

| USD 5.48 Billion | |

| % | |

|

What is the Global Monolayer Cast Films Market Size and Growth Rate?

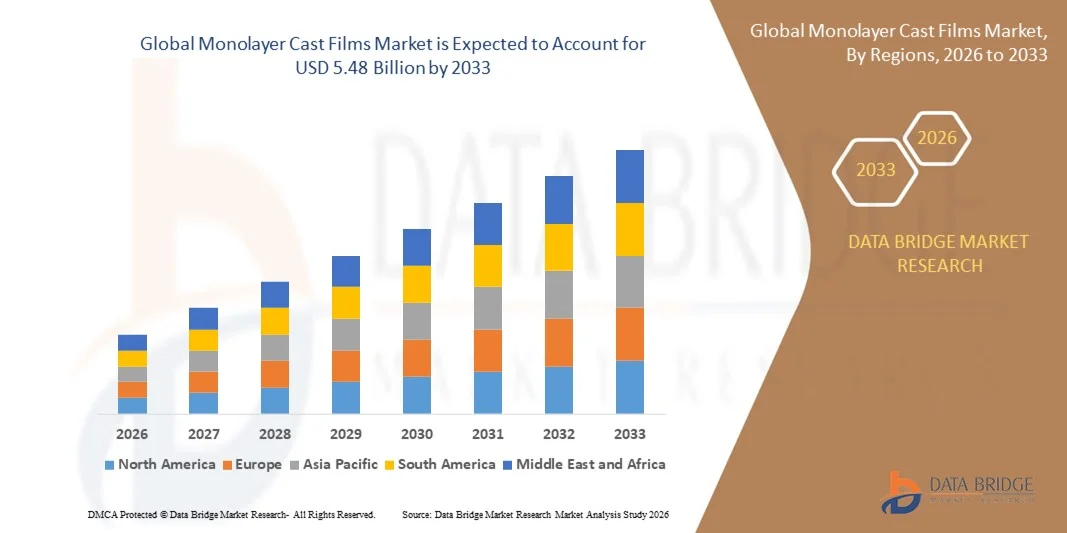

- The global monolayer cast films market size was valued at USD 3.93 billion in 2025 and is expected to reach USD 5.48 billion by 2033, at a CAGR of 4.24% during the forecast period

- Increasing demand for cost-effective and flexible packaging solutions, rising applications in food packaging, consumer goods wrapping, hygiene products, and industrial protection films, growing emphasis on lightweight and recyclable materials, and expansion of retail and e-commerce sectors are some of the major as well as vital factors such asly to augment the growth of the monolayer cast films market

- Rising preference for high-clarity, moisture-resistant, and durable plastic films further support market expansion across both developed and emerging economies

What are the Major Takeaways of Monolayer Cast Films Market?

- Growing demand for packaged food, personal care products, and pharmaceutical packaging across developing economies, along with increasing investments in flexible packaging innovation, is expected to generate significant growth opportunities for the Monolayer Cast Films market

- Fluctuations in raw material prices, particularly polyethylene and polypropylene resins, along with rising environmental concerns regarding plastic waste and regulatory pressure on single-use plastics, are such asly to act as key restraint factors limiting market growth during the forecast period

- Asia-Pacific dominated the monolayer cast films market with a 44.32% revenue share in 2025, driven by strong growth in food processing industries, rapid expansion of flexible packaging manufacturing, and rising demand for cost-efficient packaging solutions across China, India, Japan, South Korea, and Southeast Asia

- North America is projected to register the fastest CAGR of 10.36% from 2026 to 2033, driven by rising demand for sustainable packaging, increasing regulatory pressure on multi-layer plastics, and strong adoption of recyclable mono-material films across the U.S. and Canada

- The Polyethylene segment dominated the market with a 46.9% share in 2025, driven by its superior flexibility, cost-effectiveness, moisture resistance, and excellent sealing performance. LLDPE and LDPE are widely used in food and consumer goods packaging due to their durability and clarity

Report Scope and Monolayer Cast Films Market Segmentation

|

Attributes |

Monolayer Cast Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Monolayer Cast Films Market?

Increasing Shift Toward Sustainable, Recyclable, and High-Performance Monolayer Cast Films

- The monolayer cast films market is witnessing strong adoption of recyclable and lightweight film solutions designed to meet growing environmental regulations and sustainability goals across packaging industries

- Manufacturers are introducing high-clarity, improved tensile-strength, and moisture-resistant films that enhance product shelf life while maintaining cost efficiency

- Growing demand for simplified film structures that enable easier recycling compared to multilayer alternatives is driving preference for monolayer solutions in food, hygiene, and consumer goods packaging

- For instance, leading packaging material producers are focusing on polyethylene (PE) and polypropylene (PP)-based monolayer films with improved sealing properties and downgauging capabilities to reduce material consumption

- Increasing emphasis on circular economy initiatives and reduction of plastic waste is accelerating innovation in recyclable cast film technologies

- As flexible packaging demand rises globally, monolayer cast films will remain essential for cost-effective, compliant, and high-volume packaging applications

What are the Key Drivers of Monolayer Cast Films Market?

- Rising demand for packaged food, ready-to-eat meals, frozen products, and personal care goods is significantly boosting the consumption of flexible monolayer packaging films worldwide

- For instance, in 2025, several global packaging converters expanded their cast film production capacities to meet increasing demand from e-commerce and retail supply chains

- Growing urbanization, rising disposable incomes, and expansion of organized retail sectors across Asia-Pacific and Latin America are strengthening market growth

- Advancements in extrusion technology, improved film clarity, enhanced barrier performance, and better heat-sealing efficiency are improving product performance and cost competitiveness

- Increasing adoption of lightweight packaging to reduce transportation costs and carbon footprint further supports market expansion

- Supported by sustained growth in food processing and consumer goods industries, the Monolayer Cast Films market is expected to witness steady long-term growth

Which Factor is Challenging the Growth of the Monolayer Cast Films Market?

- Fluctuations in raw material prices, particularly polyethylene and polypropylene resins, directly impact manufacturing costs and profit margins

- For instance, during 2024–2025, volatility in crude oil prices and supply chain disruptions affected polymer pricing globally

- Rising environmental concerns regarding plastic waste management and stricter government regulations on single-use plastics pose compliance challenges for manufacturers

- Competition from multilayer films and biodegradable packaging alternatives creates market pressure in sustainability-focused regions

- Limited recycling infrastructure in emerging economies restricts large-scale circular adoption of plastic films

- To address these challenges, companies are focusing on recyclable mono-material innovations, downgauging strategies, and partnerships with recycling ecosystems to strengthen global adoption of monolayer cast films

How is the Monolayer Cast Films Market Segmented?

The market is segmented on the basis of material, thickness, and packaging format.

-

By Material

On the basis of material, the monolayer cast films market is segmented into Polyethylene (LLDPE, LDPE, HDPE), Polypropylene (CPP, BOPP), Polyamide, PVC, and Others. The Polyethylene segment dominated the market with a 46.9% share in 2025, driven by its superior flexibility, cost-effectiveness, moisture resistance, and excellent sealing performance. LLDPE and LDPE are widely used in food and consumer goods packaging due to their durability and clarity. Polyethylene films also support recyclability initiatives, making them highly preferred in sustainable packaging solutions.

The Polypropylene segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by rising demand for high-clarity, high-strength films with improved barrier properties. Increasing use of CPP and BOPP films in snacks, confectionery, and label applications is accelerating segment growth globally.

-

By Thickness

On the basis of thickness, the market is segmented into Up to 30 Microns, 31–50 Microns, 51–70 Microns, and Above 70 Microns. The 31–50 Microns segment dominated the market with a 38.7% share in 2025, as it offers an optimal balance between durability, flexibility, and cost efficiency. This thickness range is widely used in food pouches, retail packaging, and laminates where moderate strength and clarity are required.

The Up to 30 Microns segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing emphasis on downgauging strategies to reduce material usage and transportation costs. Sustainability initiatives and lightweight packaging trends are further encouraging manufacturers to adopt thinner yet high-performance film structures.

-

By Packaging Format

On the basis of packaging format, the monolayer cast films market is segmented into Pouches, Bags, Laminates, Wraps, and Labels. The Pouches segment dominated the market with a 34.5% share in 2025, owing to rising demand for flexible, lightweight, and resealable packaging solutions across food, personal care, and pharmaceutical sectors. Pouches provide improved shelf appeal, reduced material consumption, and better storage efficiency compared to rigid packaging.

The Laminates segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing demand for improved barrier properties and extended shelf life in premium packaged products. Expansion of organized retail and e-commerce channels is further strengthening growth in this segment.

-

By Application

On the basis of application, the market is segmented into Food & Beverages, Industrial, Personal Care, Pharmaceuticals, Electricals & Electronics, Textile, and Others. The Food & Beverages segment dominated the market with a 49.8% share in 2025, driven by high demand for packaged foods including processed meat, frozen products, dairy, confectionery, fruits, and dry fruits. Rising urbanization, changing consumption patterns, and growth in ready-to-eat products significantly support segment dominance.

The Pharmaceuticals segment is projected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing demand for secure drug and vaccine packaging, regulatory compliance requirements, and rising healthcare expenditure globally. Enhanced barrier protection and hygiene standards are accelerating adoption within the pharmaceutical industry.

Which Region Holds the Largest Share of the Monolayer Cast Films Market?

- Asia-Pacific dominated the monolayer cast films market with a 44.32% revenue share in 2025, driven by strong growth in food processing industries, rapid expansion of flexible packaging manufacturing, and rising demand for cost-efficient packaging solutions across China, India, Japan, South Korea, and Southeast Asia. Increasing urbanization, growing middle-class population, and rising consumption of packaged food, dairy, frozen products, and personal care items significantly fuel regional demand

- Leading manufacturers in Asia-Pacific are expanding polyethylene and polypropylene cast film production capacities, investing in advanced extrusion technologies, and focusing on recyclable mono-material film innovations to meet sustainability regulations

- Strong raw material availability, competitive manufacturing costs, expanding export markets, and rapid retail sector growth further reinforce regional market leadership

China Monolayer Cast Films Market Insight

China is the largest contributor within Asia-Pacific due to its massive packaging manufacturing base, strong domestic consumption, and well-established polymer supply chain. Rapid expansion of food & beverage processing industries and e-commerce packaging demand drives high-volume adoption of polyethylene and polypropylene monolayer films. Government focus on sustainable packaging and recycling initiatives is further accelerating innovation in recyclable mono-material film solutions.

India Monolayer Cast Films Market Insight

India is witnessing strong growth supported by rising demand for packaged foods, dairy products, pharmaceuticals, and personal care items. Expansion of organized retail, increasing disposable income, and growth in local film extrusion capacities are strengthening domestic production. Government-backed manufacturing initiatives and growing investments in flexible packaging infrastructure are accelerating market penetration.

Japan Monolayer Cast Films Market Insight

Japan shows steady growth driven by demand for high-quality, precision packaging solutions in food, healthcare, and consumer goods sectors. Advanced extrusion technologies, strict packaging regulations, and strong focus on sustainability promote adoption of premium-grade monolayer cast films with enhanced clarity and barrier properties.

South Korea Monolayer Cast Films Market Insight

South Korea contributes significantly due to strong demand from processed food exports, cosmetics packaging, and advanced retail packaging formats. Growing focus on lightweight, recyclable films and innovation in downgauging technologies supports long-term market expansion.

North America Monolayer Cast Films Market

North America is projected to register the fastest CAGR of 10.36% from 2026 to 2033, driven by rising demand for sustainable packaging, increasing regulatory pressure on multi-layer plastics, and strong adoption of recyclable mono-material films across the U.S. and Canada. Growth in frozen food, ready-to-eat meals, pharmaceutical packaging, and e-commerce shipping solutions further supports market expansion. Technological advancements in cast film extrusion and increasing investment in circular economy initiatives are accelerating regional growth.

U.S. Monolayer Cast Films Market Insight

The U.S. is the largest contributor in North America, supported by strong demand for flexible packaging in food, healthcare, and industrial applications. Increasing consumer preference for convenient, lightweight, and sustainable packaging formats drives adoption. Expansion of domestic film production facilities and innovation in recyclable polyethylene films further strengthen growth.

Canada Monolayer Cast Films Market Insight

Canada contributes steadily due to rising packaged food demand, growing pharmaceutical packaging needs, and government emphasis on sustainable plastic solutions. Investment in advanced film extrusion technologies and increasing recycling infrastructure development support continued market expansion across the country.

Which are the Top Companies in Monolayer Cast Films Market?

The Monolayer Cast Films industry is primarily led by well-established companies, including:

- Amcor plc (BERRY GLOBAL) (Switzerland)

- UFlex Limited (India)

- Inteplast Group (U.S.)

- Jindal Films Limited (India)

- OBEN GROUP S.A.C. (Ecuador)

- Bischof + Klein SE & CO. KG (Germany)

- MITSUI CHEMICALS AMERICA, INC. (U.S.)

- Polifilm GmbH (Germany)

- PROFOL GmbH (Germany)

- FUTAMURA CHEMICAL CO, LTD. (Japan)

- Polyplex (India)

- Thai Film Industries Public Limited Company (Thailand)

- SCIENTEX BERHAD (Malaysia)

- Polibak Plastik Film Sanayi Ve Ticaret Aş (Turkey)

- Copol International Ltd (India)

- 3B FILMS LIMITED (India)

- Alpha Marathon Film Extrusion Technologies (U.S.)

- Cloudfilm Packaging Materials Co., Ltd. (China)

- IPG (Canada)

- Kingchuan Packaging (CPP Film) (China)

- PANVERTA CAKRAKENCANA (Indonesia)

- Plastchim-T (Russia)

- Pt. Bhineka Tatamulya Industri. (Indonesia)

- TAKIGAWA CORPORATION (Japan)

What are the Recent Developments in Global Monolayer Cast Films Market?

- In July, 2025, Inteplast Group has acquired Perga, a plastics film manufacturer based in Walldürn, south-western Germany. The decision marks Inteplast’s first move into Europe and brings Perga into the company’s engineered films division. This development help the company to ear revenue in the company year

- In June 2025, Amcor has launched a first-of-its-kind, more sustainable Perflex shrink bag with an integrated handle for Butterball’s turkey breast packaging, replacing the traditional net wrap. The new design reduces packaging material and improves production efficiency, eliminating the need for manual netting. Compared with the incumbent packaging, the Perflex bag achieves a 22% reduction in carbon footprint and 22% lower water consumption. This innovation enhances Amcor’s sustainability portfolio by offering a lower-impact packaging solution that meets growing customer and regulatory demand for eco-friendly materials

- In, August, 2024 Jindal Poly Films to add a new BOPP film production line in India. The expansion is intended to increase output capacity and cater to growing demand in flexible packaging. It strengthens the company’s position in the packaging films market.

- In September 2025, UFlex announced a strategic partnership between Morris Packaging LLC and UFlex Packaging Inc. to deliver an innovative and sustainable woven bag series. The collaboration strengthens UFlex’s presence in the North American packaging market and expands its sustainable product offerings. This move underscores the company’s focus on innovation and global expansion in packaging solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Monolayer Cast Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Monolayer Cast Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Monolayer Cast Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.