Global Motility Systems Market

Market Size in USD Million

USD

742.00 Million

USD

1,958.64 Million

2025

2033

USD

742.00 Million

USD

1,958.64 Million

2025

2033

| 2026 - 2033 | |

| USD 742.00 Million | |

| USD 1,958.64 Million | |

| % | |

|

Motility Systems Market Overview

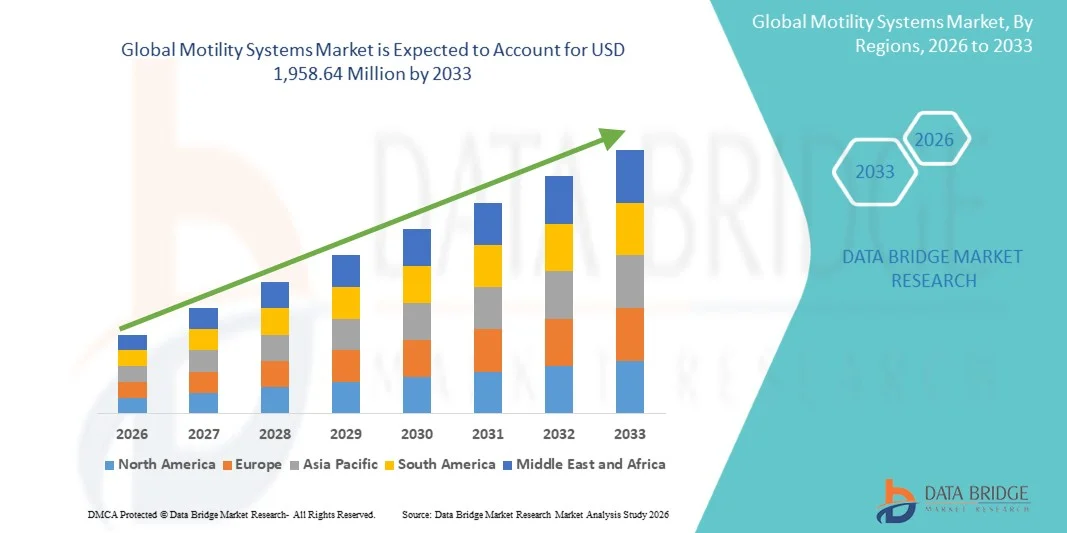

The Motility Systems Market was valued at USD 742.00 million in 2025 and is projected to reach USD 1,958.64 million by 2033, growing at a CAGR of 12.90% from 2026 to 2033. The market is witnessing steady growth driven by increasing prevalence of gastrointestinal motility disorders, rising awareness of early and accurate diagnosis of GI conditions, and continuous advancements in diagnostic technologies such as high-resolution manometry and wireless capsule-based systems.

The growing burden of disorders such as irritable bowel syndrome, gastroesophageal reflux disease, and chronic constipation, along with an aging global population, is significantly boosting demand for advanced motility testing and monitoring solutions. Additionally, increasing adoption of minimally invasive and real-time diagnostic techniques in hospitals and gastroenterology clinics, supported by improvements in healthcare infrastructure and expanding specialty care services, is accelerating market penetration across developed and emerging regions.

Key Market Trends & Insights

- North America dominated the Motility Systems Market with the largest revenue share of 38.6% in 2025, supported by advanced gastroenterology infrastructure, high adoption of diagnostic technologies, and strong presence of specialized GI care centers.

- The Motility Testing Systems segment led the market with a 44.28% share in 2025, driven by critical role in diagnosing gastrointestinal motility disorders such as achalasia, dysphagia, chronic constipation, and irritable bowel syndrome.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by rising gastrointestinal disease prevalence, improving healthcare access, and increasing investments in diagnostic imaging and specialty care services.

- Diagnostic & Monitoring Devices are the fastest-growing product type, projected to register a CAGR of 7.3%, reflecting the surge in demand for minimally invasive and patient-friendly diagnostic solutions.

- The High-Resolution Manometry segment dominated the technology category with a 42.16% revenue share in 2025, led by its superior diagnostic accuracy and widespread acceptance as the gold standard for evaluating esophageal motility disorders.

- Esophageal Motility Disorders accounted for 37.84% of the market, preferred by the high prevalence of conditions such as achalasia, dysphagia, and esophageal spasms.

- The Functional Gastrointestinal Disorders segment is the fastest-growing application category, with a CAGR of 7.5%, driven by increasing global burden of irritable bowel syndrome and related functional GI conditions.

Market Size & Forecast

- Global Market Value (2025): USD 742.00 Million

- Expected Market Value (2033): USD 1,958.64 Million

- Forecast CAGR (2026–2033): 12.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Motility Systems Market Segmentation

|

Attributes |

Motility Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Medtronic (Ireland) · Laborie Medical Technologies Corp. (Canada) · Diversatek Healthcare (U.S.) · MMS Medical Measurement Systems (Netherlands) · ALACER Biomedica (Turkey) · Synectics Medical AB (Sweden) · Standard Instruments GmbH (Germany) · Cook (U.S.) · Sierra Scientific Instruments, Inc. (U.S.) · CapsoVision, Inc. (U.S.) · Royal Philips (Netherlands) · FUJIFILM Holdings Corporation (Japan) · Olympus Corporation (Japan) · PENTAX Medical (Japan) · Medspira, LLC (U.S.) · Medica S.p.A. (Italy) · EB Neuro S.p.A. (Italy) · Gaeltec Devices Ltd (U.K.) · Medi-Globe GmbH (Germany) · CONMED Corporation (U.S.) |

|

Market Opportunities |

· Expansion of wireless capsule motility testing · Growing adoption of AI-powered motility data analysis platforms · Increasing penetration of motility diagnostic systems in emerging healthcare markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Motility Systems Market Trends

Trend: Rising Adoption of Minimally Invasive Gastrointestinal Motility Diagnostics

Healthcare providers are increasingly adopting minimally invasive motility diagnostic technologies to improve patient comfort, reduce procedure-related complications, and enhance clinical workflow efficiency. Innovations such as wireless motility capsules, high-resolution manometry systems, and ambulatory monitoring devices enable comprehensive assessment of gastrointestinal function without extensive hospital stays. Gastroenterology centers are similarly utilizing advanced diagnostic platforms to support early disease detection through standardized, data-driven evaluation protocols, while digital analytics tools provide deeper insights that closely reflect real-world gastrointestinal physiological conditions. For instance, in May 2024, Medtronic expanded clinical support and adoption initiatives for its gastrointestinal diagnostic technologies, including motility assessment solutions used in advanced gastroenterology practices.

Motility Systems Market Dynamics

Key Market Driver: Growing Prevalence of Gastrointestinal Motility Disorders Worldwide

The increasing prevalence of gastrointestinal motility disorders and functional digestive diseases has created substantial demand for advanced motility systems that can accurately diagnose complex abnormalities across the gastrointestinal tract. Hospitals, specialty clinics, and diagnostic centers are deploying these technologies as a core component of gastroenterology services, improving diagnostic accuracy, accelerating treatment decisions, and enhancing patient outcomes. Rising awareness among physicians and patients regarding early diagnosis is further supporting adoption across both developed and emerging healthcare markets globally. For instance, in January 2024, Laborie Medical Technologies continued expanding its gastroenterology diagnostics portfolio, supporting healthcare providers with advanced motility testing solutions for esophageal and anorectal disorders.

Key Restraint/Challenge: High Cost of Advanced Motility Diagnostic Systems

A significant restraint in the Motility Systems Market is the high acquisition and implementation cost associated with advanced diagnostic platforms. Modern systems integrate sophisticated sensors, high-resolution pressure measurement technologies, specialized software platforms, and comprehensive data analysis capabilities, requiring substantial investment in equipment procurement, installation, and personnel training. The total cost of ownership also includes maintenance contracts, software updates, and calibration requirements, making adoption challenging for smaller healthcare facilities, independent clinics, and resource-constrained institutions.

For instance, the continued adoption of high-resolution manometry platforms across tertiary care hospitals highlights the substantial capital investment and operational expertise required for advanced gastrointestinal motility testing infrastructure.

Key Market Opportunity: Integration of Artificial Intelligence in Motility Data Analysis

The integration of artificial intelligence into motility diagnostics presents a significant market opportunity. AI-enabled platforms can automate interpretation of complex gastrointestinal motility patterns, provide real-time clinical decision support, and improve diagnostic consistency across healthcare settings. The development of cloud-connected analytics solutions and interoperable healthcare platforms is further expanding access to advanced diagnostic capabilities, creating growth opportunities across emerging healthcare markets in Asia-Pacific, Latin America, and the Middle East. For instance, in 2024, leading gastroenterology technology providers increased investments in AI-assisted diagnostic software designed to enhance interpretation of high-resolution manometry and gastrointestinal motility datasets.

Motility Systems Market Scope

The motility systems market is segmented on the basis of product type, technology, application, and end user.

- By Product Type

On the basis of product type, the Motility Systems Market is segmented into motility testing systems, motility therapy systems, and diagnostic & monitoring devices. The Motility Testing Systems segment dominated the market with a 44.28% share in 2025, owing to its critical role in diagnosing gastrointestinal motility disorders such as achalasia, dysphagia, chronic constipation, and irritable bowel syndrome. These systems are extensively used in hospitals and gastroenterology clinics for accurate assessment of esophageal, anorectal, and intestinal functions. Growing awareness regarding early diagnosis of GI disorders is driving demand for advanced testing platforms. High-resolution manometry and transit testing technologies have significantly improved diagnostic precision. Increasing patient volumes and expanding gastroenterology services are further supporting adoption. Their indispensable role in clinical decision-making continues to strengthen the segment’s market leadership.

The Diagnostic & Monitoring Devices segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing demand for minimally invasive and patient-friendly diagnostic solutions. Wireless motility capsules and ambulatory monitoring systems are gaining popularity due to their ability to provide real-time physiological data. Continuous technological advancements are improving patient comfort and diagnostic efficiency. The shift toward outpatient care and remote monitoring is further accelerating adoption. Healthcare providers are increasingly utilizing these devices to reduce procedure times and enhance patient outcomes. Rising investments in digital healthcare technologies are also supporting market expansion. The growing preference for non-invasive diagnostics is expected to fuel long-term growth.

- By Technology

On the basis of technology, the Motility Systems Market is segmented into high-resolution manometry, impedance monitoring systems, wireless capsule-based systems, electrogastrography, and imaging & sensor-based systems. The High-Resolution Manometry (HRM) segment led the market with a 42.16% share in 2025, driven by its superior diagnostic accuracy and widespread acceptance as the gold standard for evaluating esophageal motility disorders. HRM provides detailed pressure mapping of the gastrointestinal tract, enabling clinicians to identify complex abnormalities with greater precision. The technology is widely adopted in tertiary care hospitals and specialty GI centers. Growing prevalence of GERD and swallowing disorders is increasing demand for HRM procedures. Continuous improvements in catheter design and software analytics are enhancing diagnostic capabilities. Strong clinical validation and guideline recommendations continue to support segment dominance.

The Wireless Capsule-Based Systems segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising demand for non-invasive gastrointestinal diagnostic solutions. These systems allow comprehensive evaluation of GI transit and motility without the discomfort associated with conventional catheter-based procedures. Patients increasingly prefer capsule-based technologies due to convenience and reduced procedural burden. Technological advancements have improved data transmission, battery life, and diagnostic accuracy. Expanding applications in gastric emptying and intestinal transit studies are further accelerating adoption. Healthcare providers are increasingly incorporating these systems into routine clinical practice. The growing focus on patient-centered care is expected to sustain rapid growth.

- By Application

On the basis of application, the Motility Systems Market is segmented into esophageal motility disorders, gastroesophageal reflux disease, intestinal motility disorders, colonic transit disorders, functional gastrointestinal disorders, and post-surgical GI dysfunction. The Esophageal Motility Disorders segment dominated the market with a 37.84% share in 2025, owing to the high prevalence of conditions such as achalasia, dysphagia, and esophageal spasms. Accurate diagnosis of these disorders requires advanced motility testing systems, particularly high-resolution manometry platforms. Increasing awareness among healthcare professionals regarding early detection is supporting segment growth. Rising incidence of chronic digestive diseases and aging populations are contributing to higher testing volumes. Improvements in diagnostic protocols have enhanced clinical outcomes for affected patients. The segment continues to benefit from strong adoption across specialized gastroenterology centers worldwide.

The Functional Gastrointestinal Disorders segment is projected to be the fastest-growing application segment at a CAGR of 7.5% from 2026 to 2033, driven by the increasing global burden of irritable bowel syndrome and related functional GI conditions. Growing recognition of the impact of these disorders on quality of life is encouraging greater diagnostic evaluation. Advanced motility technologies help clinicians better understand underlying physiological abnormalities. Increasing healthcare expenditure and access to specialist care are supporting market growth. Research efforts focused on functional GI diseases are expanding diagnostic applications. Improved reimbursement coverage in several regions is also facilitating adoption. Rising patient awareness is expected to further accelerate demand.

- By End User

On the basis of end user, the Motility Systems Market is segmented into hospitals, gastroenterology clinics, diagnostic laboratories, academic & research institutes, and ambulatory surgical centers. The Hospitals segment accounted for the largest market share of 51.32% in 2025, driven by the availability of advanced diagnostic infrastructure and multidisciplinary gastroenterology services. Hospitals perform a high volume of motility procedures due to their ability to manage complex gastrointestinal disorders. Access to specialized healthcare professionals and advanced technologies supports widespread adoption. Increasing patient admissions related to digestive diseases are contributing to segment growth. Many hospitals are investing in state-of-the-art diagnostic systems to improve clinical outcomes. Strong reimbursement support in developed markets further strengthens their market position. Hospitals remain the primary centers for comprehensive motility assessment and treatment.

The Gastroenterology Clinics segment is anticipated to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by the increasing shift toward specialized outpatient digestive healthcare services. These clinics offer focused expertise in gastrointestinal diagnosis and treatment, improving patient convenience and access to care. Rising demand for early disease detection is supporting the adoption of advanced motility testing technologies. Clinics are increasingly investing in modern diagnostic equipment to expand service capabilities. Shorter waiting times and cost-effective care models are attracting more patients. Growing prevalence of chronic digestive disorders is also increasing patient visits to specialty centers. Expansion of private healthcare networks is expected to further drive segment growth.

Motility Systems Market Regional Analysis

North America dominated the Motility Systems Market with the largest revenue share of 38.6% in 2025, supported by advanced gastroenterology infrastructure, high adoption of diagnostic technologies, and strong presence of specialized GI care centers. The region also benefits from strong awareness of gastrointestinal motility disorders, favorable reimbursement frameworks, and growing utilization of high-resolution manometry and wireless capsule-based diagnostic systems across hospitals and specialty clinics. Increasing investments in digestive disease research, expanding access to specialized gastrointestinal care, and rising demand for minimally invasive diagnostic procedures continue to strengthen North America’s leadership position in the global market.

U.S. Motility Systems Market Insight

The U.S. motility systems market is witnessing strong growth due to rising prevalence of gastrointestinal disorders, increasing investments in advanced diagnostic technologies, and expanding awareness regarding early disease detection. The country’s well-established healthcare infrastructure, along with growing adoption of high-resolution manometry, impedance monitoring, and wireless capsule-based systems, is driving demand across hospitals, specialty clinics, and diagnostic centers. In addition, increasing emphasis on minimally invasive diagnostics and improved patient outcomes is accelerating the adoption of motility systems throughout the healthcare sector.

Europe Motility Systems Market Insight

The Europe motility systems market remains a major contributor to global revenue, driven by advanced healthcare systems, growing prevalence of digestive disorders, and strong adoption of innovative diagnostic technologies. The widespread use of motility testing systems in hospitals and gastroenterology centers is supporting market expansion across the region. Increasing investments in gastrointestinal research, coupled with favorable healthcare policies and rising awareness of functional GI disorders, continue to enhance the adoption of motility systems throughout Europe.

U.K. Motility Systems Market Insight

The U.K. motility systems market is experiencing steady growth, supported by increasing demand for advanced gastrointestinal diagnostics and rising awareness regarding digestive health conditions. Growing investments in modern healthcare infrastructure and the expansion of specialist gastroenterology services are contributing to market growth. Furthermore, integration of digital diagnostic platforms, improved patient management solutions, and increased utilization of minimally invasive motility testing technologies are strengthening the U.K.'s position as a key market for gastrointestinal diagnostics.

Germany Motility Systems Market Insight

The Germany motility systems market is expanding steadily due to the country’s advanced healthcare infrastructure, strong medical technology sector, and increasing focus on digestive disease management. Hospitals, academic institutions, and specialty gastroenterology clinics are increasingly utilizing motility systems for accurate diagnosis and treatment planning. Continuous advancements in manometry technologies, digital diagnostics, and patient monitoring systems, along with growing healthcare investments and research activities, are further driving market growth in Germany.

Asia-Pacific Motility Systems Market Insight

The Asia-Pacific motility systems market is expected to witness rapid growth, driven by increasing incidence of gastrointestinal disorders, expanding healthcare access, and rising investments in diagnostic infrastructure across countries such as China, India, and Japan. Growing awareness regarding digestive health, rising adoption of advanced motility testing technologies, and increasing demand for accurate and patient-friendly diagnostic solutions are supporting regional market expansion. Additionally, the expansion of specialty healthcare facilities and improving healthcare expenditure are accelerating adoption across the region.

Japan Motility Systems Market Insight

The Japan motility systems market is witnessing consistent growth due to rising investments in advanced gastrointestinal diagnostics, increasing prevalence of age-related digestive disorders, and growing emphasis on early disease detection. Healthcare providers, research institutions, and specialty clinics are increasingly adopting advanced motility testing systems for clinical assessment and treatment planning. Moreover, ongoing technological advancements and the country’s focus on high-quality healthcare services are further contributing to market growth.

China Motility Systems Market Insight

The China motility systems market is growing rapidly, driven by increasing healthcare expenditure, expanding hospital infrastructure, and rising awareness regarding gastrointestinal disorders. Growing adoption of advanced diagnostic technologies, including high-resolution manometry and wireless capsule-based systems, is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing focus on early diagnosis, and continuous technological advancements are positioning China as one of the fastest-growing markets for motility systems globally.

Motility Systems Market Share

The motility systems industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Laborie Medical Technologies Corp. (Canada)

- Diversatek Healthcare (U.S.)

- MMS Medical Measurement Systems (Netherlands)

- ALACER Biomedica (Turkey)

- Synectics Medical AB (Sweden)

- Standard Instruments GmbH (Germany)

- Cook (U.S.)

- Sierra Scientific Instruments, Inc. (U.S.)

- CapsoVision, Inc. (U.S.)

- Royal Philips (Netherlands)

- FUJIFILM Holdings Corporation (Japan)

- Olympus Corporation (Japan)

- PENTAX Medical (Japan)

- Medspira, LLC (U.S.)

- Medica S.p.A. (Italy)

- EB Neuro S.p.A. (Italy)

- Gaeltec Devices Ltd (U.K.)

- Medi-Globe GmbH (Germany)

- CONMED Corporation (U.S.)

Latest Developments in Motility Systems Market

- In June 2025, Diversatek Healthcare, a leading provider of gastrointestinal diagnostic solutions, announced the launch of Zvu® 3.4.0 software with full compatibility with Chicago Classification 4.0 and Lyon Consensus 2.0 standards. The update enhances high-resolution manometry and reflux monitoring analysis through automated measurements, guided workflows, and improved diagnostic accuracy, supporting more efficient evaluation of gastrointestinal motility disorders

- In May 2024, researchers reported successful validation of a deep-learning-based long-term high-resolution manometry (LTHRM) analysis platform capable of detecting and clustering swallowing events with over 94% accuracy. The development represents a significant advancement in automated motility diagnostics, helping clinicians analyze large volumes of gastrointestinal motility data more efficiently and accurately

- In October 2023, Laborie Medical Technologies, a global developer of diagnostic and therapeutic medical technologies, completed the acquisition of Urotronic. While primarily focused on urology, the acquisition strengthened Laborie’s overall medical technology portfolio and reinforced its strategic investments in diagnostic platforms, supporting continued innovation across its gastrointestinal motility and gastroenterology business segments

- In April 2022, Laborie Medical Technologies completed the acquisition of GI Supply, a leader in specialty gastroenterology products. The transaction expanded Laborie’s gastroenterology portfolio and strengthened its position in gastrointestinal diagnostics and therapeutic solutions, enhancing its ability to serve clinicians involved in the diagnosis and management of motility-related disorders

- In February 2022, researchers published a multi-stage artificial intelligence model for automated diagnosis of esophageal motility disorders using high-resolution manometry data. The system demonstrated strong predictive performance and highlighted the growing integration of AI into motility diagnostics, with the potential to improve diagnostic consistency and reduce interpretation variability among clinicians

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.