Global Multi Use Bioreactor Market

Market Size in USD Billion

USD

13.11 Billion

USD

46.03 Billion

2025

2033

USD

13.11 Billion

USD

46.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 13.11 Billion | |

| USD 46.03 Billion | |

| % | |

|

Multi Use Bioreactor Market Size

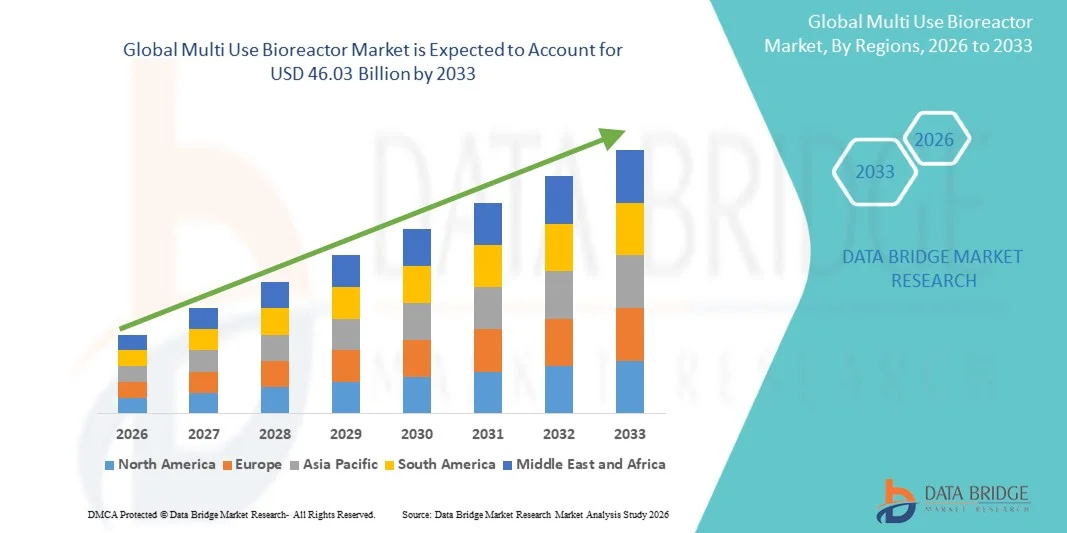

- The global multi use bioreactor market size was valued at USD 13.11 billion in 2025and is expected to reach USD 46.03 billion by 2033, at a CAGR of 17.00% during the forecast period

- The market growth is primarily driven by the increasing demand for large-scale biopharmaceutical manufacturing and the rising adoption of biologics, vaccines, and cell culture-based production processes across the pharmaceutical and biotechnology industries

- Furthermore, continuous advancements in bioprocessing technologies, coupled with the growing focus on production efficiency, process scalability, and contamination control, are positioning multi use bioreactors as essential systems in modern biomanufacturing facilities. These combined factors are significantly accelerating the expansion of the global multi use bioreactor industry

Multi Use Bioreactor Market Analysis

- Multi use bioreactors, designed for repeated and large-scale cultivation of microorganisms and cell cultures, are becoming increasingly essential in modern biopharmaceutical and biotechnology manufacturing processes due to their high production efficiency, scalability, and suitability for commercial biologics production

- The rising demand for multi use bioreactors is primarily driven by the growing production of biologics, vaccines, monoclonal antibodies, and recombinant proteins, along with increasing investments in biopharmaceutical manufacturing infrastructure worldwide

- North America dominated the multi use bioreactor market with the largest revenue share of 41.9% in 2025, supported by the strong presence of leading biopharmaceutical companies, advanced manufacturing capabilities, and increasing adoption of upstream bioprocessing technologies, with the U.S. witnessing significant expansion in biologics and gene therapy production facilities driven by continuous investments in research and development activities

- Asia-Pacific is expected to be the fastest growing region in the multi use bioreactor market during the forecast period due to expanding biopharmaceutical manufacturing capacity, rising healthcare expenditures, and growing government support for biotechnology innovation

- Industrial scale bioreactors (>1000L) segment dominated the multi use bioreactor market with a market share of 46.8% in 2025, driven by their extensive utilization in large-volume commercial biopharmaceutical production and increasing demand for high-capacity manufacturing systems

Report Scope and Multi Use Bioreactor Market Segmentation

|

Attributes |

Multi Use Bioreactor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· The growing commercialization of gene therapies and personalized biologics · Increasing investments in emerging biopharmaceutical manufacturing hubs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Multi Use Bioreactor Market Trends

“Rising Adoption of Automated and Digitalized Bioprocessing Systems”

- A significant and accelerating trend in the global multi use bioreactor market is the increasing integration of automation, digital monitoring platforms, and advanced process analytics within biopharmaceutical manufacturing facilities. This convergence of technologies is significantly improving production efficiency, process consistency, and operational scalability across biologics manufacturing operations

- For instance, Sartorius AG offers advanced multi use bioreactor systems integrated with automated control software and real-time monitoring technologies that enable manufacturers to optimize cell culture conditions and streamline production workflows. Similarly, Thermo Fisher Scientific provides industrial-scale bioreactor platforms equipped with digital process control systems for enhanced manufacturing precision

- Automation integration in multi use bioreactors enables features such as predictive process optimization, real-time parameter adjustments, and continuous monitoring of cell growth conditions to improve production outcomes. For instance, some Cytiva bioreactor platforms utilize intelligent automation technologies to enhance batch consistency and minimize operational downtime during biologics production. Furthermore, advanced monitoring capabilities allow manufacturers to remotely supervise production processes and improve process reliability across multiple manufacturing sites

- The seamless integration of multi use bioreactors with upstream and downstream bioprocessing technologies facilitates centralized control over various stages of biologics manufacturing. Through unified digital platforms, manufacturers can manage fermentation, purification, and quality monitoring processes simultaneously, creating a more efficient and interconnected biomanufacturing environment

- This trend toward more automated, scalable, and digitally connected bioprocessing systems is fundamentally reshaping operational standards within the biopharmaceutical industry. Consequently, companies such as Eppendorf SE are developing advanced multi use bioreactor solutions with intelligent automation features, integrated monitoring systems, and scalable production capabilities for commercial biologics manufacturing

- The demand for multi use bioreactors with advanced automation and digital integration capabilities is growing rapidly across biopharmaceutical and biotechnology sectors, as manufacturers increasingly prioritize production efficiency, process reproducibility, and large-scale biologics manufacturing flexibility

Multi Use Bioreactor Market Dynamics

Driver

“Growing Demand Due to Expanding Biologics and Vaccine Manufacturing Activities”

- The increasing global demand for biologics, vaccines, monoclonal antibodies, and cell-based therapies, coupled with the rapid expansion of biopharmaceutical manufacturing infrastructure, is a significant driver for the heightened demand for multi use bioreactors

- For instance, in March 2025, Thermo Fisher Scientific announced the expansion of its biologics manufacturing capabilities through investments in large-scale bioprocessing technologies and advanced bioreactor production systems. Such strategies by key companies are expected to drive the multi use bioreactor industry growth in the forecast period

- As pharmaceutical and biotechnology companies continue increasing production capacities for biologics and advanced therapies, multi use bioreactors offer enhanced scalability, operational reliability, and high-volume manufacturing efficiency, making them essential for commercial bioprocessing applications

- Furthermore, the rising adoption of continuous bioprocessing technologies and the growing need for efficient upstream manufacturing systems are making multi use bioreactors an integral component of modern biologics production facilities, offering seamless integration with advanced monitoring and process automation technologies

- The capability to support large-scale cell culture operations, maintain consistent production quality, and optimize manufacturing throughput through automated control systems are key factors propelling the adoption of multi use bioreactors across pharmaceutical and biotechnology sectors. The growing establishment of biologics manufacturing plants and increasing investments in biopharmaceutical research further contribute to market growth

Restraint/Challenge

“High Operational Costs and Complex Validation Requirements”

- Concerns surrounding the high installation, maintenance, and operational costs associated with large-scale bioprocessing equipment, including multi use bioreactors, pose a significant challenge to broader market expansion. As multi use bioreactors require extensive cleaning, sterilization, and validation procedures, manufacturers often face increased operational complexity and production downtime concerns

- For instance, stringent regulatory requirements related to biopharmaceutical manufacturing validation and contamination control procedures have made some smaller biotechnology companies hesitant to invest in large-scale multi use bioreactor systems

- Addressing these operational and regulatory challenges through advanced automation, improved cleaning technologies, and efficient validation systems is crucial for enhancing manufacturing productivity and reducing process complexity. Companies such as Merck KGaA and Danaher Corporation emphasize integrated monitoring technologies and automated process controls within their bioprocessing platforms to improve operational efficiency

- In addition, the substantial capital investment required for industrial-scale multi use bioreactor installations compared to alternative production technologies can limit adoption among cost-sensitive manufacturers, particularly emerging biotechnology firms or regional production facilities. While modular bioprocessing solutions are becoming more accessible, advanced automation and large-capacity production systems often involve significantly higher infrastructure expenditures

- While operational efficiencies are gradually improving, the high cost associated with large-scale biomanufacturing infrastructure and stringent compliance requirements can still hinder widespread adoption, especially for companies with limited production budgets or early-stage biologics pipelines

- Overcoming these challenges through enhanced process automation, cost-efficient manufacturing strategies, and the development of scalable multi use bioreactor platforms will be vital for sustained market growth

Multi Use Bioreactor Market Scope

The market is segmented on the basis of product type, cell, molecule, modality, and technology.

- By Product Type

On the basis of product type, the multi use bioreactor market is segmented into benchtop bioreactors (up to 15L), pilot scale bioreactors (15-1000L), and industrial scale bioreactors (>1000L). The industrial scale bioreactors (>1000L) segment dominated the market with the largest market revenue share of 46.8% in 2025, driven by the rising demand for high-volume biologics and vaccine manufacturing across commercial biopharmaceutical facilities. These bioreactors are extensively utilized in large-scale production processes due to their ability to support high-capacity operations, process consistency, and long-term manufacturing efficiency. Pharmaceutical companies increasingly prefer industrial-scale systems for monoclonal antibody and recombinant protein production because of their scalability and integration with advanced automation technologies. In addition, the growing expansion of commercial biologics manufacturing plants worldwide is further supporting segment growth. The capability of these systems to manage complex upstream processing applications while maintaining contamination control also contributes significantly to their widespread adoption.

The pilot scale bioreactors (15-1000L) segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing research activities and the growing transition of biologic products from laboratory to commercial-scale production. These bioreactors provide flexibility for process optimization, clinical-scale manufacturing, and technology validation before full-scale commercialization. Biotechnology companies and contract manufacturing organizations are increasingly utilizing pilot-scale systems to accelerate product development timelines and reduce operational risks. Furthermore, rising investments in biosimilar and gene therapy research are driving the need for scalable and adaptable pilot-scale bioprocessing solutions. Their lower operational complexity and ability to support multiple applications across research and development environments are also contributing to segment expansion. Increasing focus on process intensification and rapid product development further enhances market demand for pilot scale bioreactors.

- By Cell

On the basis of cell, the multi use bioreactor market is segmented into mammalian cells, bacterial cells, and yeast cells. The mammalian cells segment dominated the market with the largest market revenue share in 2025, driven by the increasing production of monoclonal antibodies, vaccines, recombinant proteins, and advanced biologics requiring complex cell culture systems. Mammalian cells are widely preferred in biopharmaceutical manufacturing due to their ability to produce proteins with human-compatible structures and post-translational modifications. The growing commercialization of cell-based therapies and biologics is further accelerating the adoption of mammalian cell culture technologies across pharmaceutical manufacturing facilities. In addition, advancements in cell line engineering and upstream bioprocessing technologies are improving production efficiency and product quality. Biopharmaceutical companies continue investing heavily in mammalian cell-based production systems to support expanding biologics pipelines and large-scale commercial manufacturing operations. The increasing prevalence of chronic diseases and rising demand for targeted therapies also contribute significantly to segment dominance.

The yeast cells segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for cost-effective and rapid biologics production systems across biotechnology and vaccine manufacturing applications. Yeast-based expression systems offer advantages such as faster growth rates, simplified cultivation processes, and lower production costs compared to mammalian cell cultures. The increasing utilization of yeast cells in recombinant protein production and vaccine development is supporting segment expansion across emerging biopharmaceutical markets. Furthermore, growing research activities related to synthetic biology and industrial biotechnology are increasing the adoption of yeast-based bioprocessing platforms. Their ability to support scalable fermentation processes and improve manufacturing productivity also contributes to rising market demand. Increasing investments in microbial-based therapeutics and alternative protein production are expected to further accelerate segment growth during the forecast period.

- By Molecule

On the basis of molecule, the multi use bioreactor market is segmented into monoclonal antibodies, vaccines, recombinant proteins, stem cells, and gene therapy. The monoclonal antibodies segment dominated the market with the largest market revenue share in 2025, driven by the expanding global demand for targeted biologic therapies across oncology, autoimmune disorders, and chronic disease treatment applications. Monoclonal antibodies require advanced large-scale bioprocessing systems to maintain high production quality, consistency, and manufacturing efficiency. The increasing number of regulatory approvals for antibody-based therapeutics and the growing pipeline of biologic drugs are significantly supporting segment growth. In addition, pharmaceutical companies are investing heavily in high-capacity manufacturing infrastructure to address rising global demand for antibody therapies. Continuous advancements in upstream processing technologies and cell culture optimization are further improving monoclonal antibody production efficiency. The increasing adoption of biosimilars and personalized medicine solutions also contributes substantially to the dominance of this segment.

The gene therapy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising investments in advanced therapeutics, increasing clinical trial activities, and expanding regulatory approvals for gene-based treatments. Gene therapy manufacturing requires specialized bioprocessing systems capable of supporting viral vector production and complex cell culture operations. Biotechnology companies are increasingly adopting flexible multi use bioreactor platforms to accelerate the development and commercialization of gene therapies targeting rare and genetic disorders. Furthermore, growing collaborations between pharmaceutical companies and contract manufacturing organizations are supporting the expansion of gene therapy production capabilities worldwide. The increasing focus on personalized medicine and regenerative therapies is also driving demand for advanced bioreactor technologies. Rising government funding and technological advancements in vector manufacturing processes are expected to further strengthen segment growth during the forecast period.

- By Modality

On the basis of modality, the multi use bioreactor market is segmented into manual, automatic, and semi-automatic. The automatic segment dominated the market with the largest market revenue share in 2025, driven by the increasing need for process automation, operational efficiency, and real-time monitoring across large-scale biopharmaceutical manufacturing facilities. Automatic bioreactor systems enable manufacturers to optimize production parameters, reduce human intervention, and improve process reproducibility during biologics manufacturing operations. The growing adoption of digitalized bioprocessing technologies and integrated monitoring systems is significantly supporting the expansion of automatic bioreactor installations worldwide. In addition, pharmaceutical companies increasingly prefer automated systems to minimize contamination risks and improve manufacturing consistency across commercial production environments. Advanced automation features such as predictive analytics, remote monitoring, and automated nutrient control are further contributing to segment growth. The increasing focus on continuous bioprocessing and smart manufacturing practices also reinforces the dominance of automatic bioreactor systems.

The semi-automatic segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the growing demand for cost-effective and flexible bioprocessing solutions among small and mid-sized biotechnology companies. Semi-automatic systems provide a balance between operational control and automation, making them suitable for research laboratories, pilot-scale manufacturing, and emerging biopharmaceutical facilities. Biotechnology firms increasingly utilize semi-automatic bioreactors to reduce capital investment costs while maintaining efficient process management capabilities. Furthermore, the rising number of clinical-stage biologics and biosimilar development projects is supporting demand for adaptable and scalable bioprocessing systems. Their relatively lower operational complexity and ease of implementation are also driving adoption across developing markets. Increasing focus on improving research productivity and accelerating product development timelines is expected to further support segment expansion.

- By Technology

On the basis of technology, the multi use bioreactor market is segmented into downstream and upstream. The upstream segment dominated the market with the largest market revenue share in 2025, driven by the increasing utilization of cell culture and fermentation technologies during biologics, vaccine, and recombinant protein manufacturing processes. Upstream bioprocessing plays a critical role in cell cultivation, nutrient optimization, and large-scale production efficiency within biopharmaceutical manufacturing operations. The growing demand for monoclonal antibodies, biosimilars, and advanced therapeutics is significantly increasing the adoption of advanced upstream bioreactor technologies worldwide. In addition, continuous advancements in cell line development and process automation are improving production yields and operational scalability across commercial manufacturing facilities. Pharmaceutical companies are investing heavily in upstream process optimization to enhance manufacturing productivity and reduce production costs. The increasing expansion of biologics manufacturing infrastructure globally also contributes substantially to segment dominance.

The downstream segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising need for efficient purification, separation, and product recovery technologies within biologics manufacturing workflows. Downstream processing is becoming increasingly important for maintaining product quality, regulatory compliance, and manufacturing efficiency across commercial biopharmaceutical production operations. Biotechnology companies are adopting advanced downstream technologies to improve purification accuracy and streamline product recovery processes for complex biologic therapies. Furthermore, the growing commercialization of cell and gene therapies is creating strong demand for specialized downstream processing systems capable of handling high-value biologic products. Their ability to support process intensification and reduce manufacturing turnaround times is also driving market growth. Increasing investments in integrated bioprocessing platforms and continuous manufacturing technologies are expected to further accelerate segment expansion during the forecast period

Multi Use Bioreactor Market Regional Analysis

- North America dominated the multi use bioreactor market with the largest revenue share of 41.9% in 2025, supported by the strong presence of leading biopharmaceutical companies, advanced manufacturing capabilities, and increasing adoption of upstream bioprocessing technologies

- Biopharmaceutical companies in the region highly prioritize large-scale production efficiency, process automation, and integrated manufacturing systems offered by multi use bioreactors for biologics, vaccines, and recombinant protein production

- This widespread adoption is further supported by the strong presence of leading biotechnology companies, advanced healthcare research capabilities, and increasing demand for high-capacity commercial biomanufacturing facilities, establishing multi use bioreactors as essential systems across pharmaceutical and biotechnology production environments

U.S. Multi Use Bioreactor Market Insight

The U.S. multi use bioreactor market captured the largest revenue share in 2025 within North America, fueled by the rapid expansion of biologics manufacturing and increasing investments in advanced biopharmaceutical production facilities. Pharmaceutical and biotechnology companies are increasingly prioritizing large-scale manufacturing efficiency through automated and high-capacity bioprocessing systems. The growing demand for monoclonal antibodies, vaccines, and cell-based therapies, combined with strong adoption of upstream processing technologies and digitalized manufacturing platforms, further propels the multi use bioreactor industry. Moreover, the increasing presence of contract development and manufacturing organizations (CDMOs), along with continuous advancements in process automation and biologics production infrastructure, is significantly contributing to the market's expansion.

Europe Multi Use Bioreactor Market Insight

The Europe multi use bioreactor market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing investments in biotechnology research and the escalating demand for biologics and biosimilar production. The expansion of pharmaceutical manufacturing capabilities, coupled with rising adoption of advanced bioprocessing technologies, is fostering the utilization of multi use bioreactors. European manufacturers are also focusing on operational efficiency, regulatory compliance, and sustainable biomanufacturing processes. The region is experiencing significant growth across pharmaceutical, biotechnology, and research applications, with multi use bioreactors being increasingly incorporated into both commercial-scale manufacturing facilities and clinical production environments.

U.K. Multi Use Bioreactor Market Insight

The U.K. multi use bioreactor market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investments in biologics development and a growing focus on advanced pharmaceutical manufacturing capabilities. In addition, rising demand for cell and gene therapies is encouraging pharmaceutical companies and research organizations to adopt scalable bioprocessing systems. The U.K.’s expanding biotechnology sector, alongside its strong clinical research infrastructure and government support for life sciences innovation, is expected to continue to stimulate market growth.

Germany Multi Use Bioreactor Market Insight

The Germany multi use bioreactor market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing demand for technologically advanced biomanufacturing systems and the country’s strong pharmaceutical production capabilities. Germany’s well-established biotechnology infrastructure, combined with its emphasis on industrial innovation and process automation, promotes the adoption of multi use bioreactors, particularly across biologics and vaccine manufacturing facilities. The integration of automated monitoring systems and advanced upstream bioprocessing technologies is also becoming increasingly prevalent, with manufacturers prioritizing production efficiency, quality control, and regulatory compliance in commercial biopharmaceutical operations.

Asia-Pacific Multi Use Bioreactor Market Insight

The Asia-Pacific multi use bioreactor market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by expanding biopharmaceutical manufacturing capacity, increasing healthcare investments, and technological advancements in countries such as China, Japan, and India. The region's growing focus on biologics production, supported by government initiatives promoting biotechnology innovation and pharmaceutical self-sufficiency, is driving the adoption of multi use bioreactors. Furthermore, as APAC emerges as a major hub for biopharmaceutical manufacturing and contract production services, the accessibility and deployment of advanced bioprocessing systems are expanding across both established and emerging biotechnology companies.

Japan Multi Use Bioreactor Market Insight

The Japan multi use bioreactor market is gaining momentum due to the country’s advanced biotechnology sector, growing investments in regenerative medicine, and increasing demand for high-quality biologics production systems. The Japanese market places a significant emphasis on precision manufacturing and process efficiency, and the adoption of multi use bioreactors is driven by the expansion of biologics and cell therapy development activities. The integration of advanced automation technologies and digital monitoring systems within bioprocessing facilities is fueling growth. Moreover, Japan's strong focus on pharmaceutical innovation and next-generation therapeutics is likely to spur demand for scalable and high-performance bioreactor solutions across research and commercial manufacturing sectors.

India Multi Use Bioreactor Market Insight

The India multi use bioreactor market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s rapidly expanding biopharmaceutical sector, increasing vaccine production capabilities, and rising investments in biotechnology infrastructure. India stands as one of the leading global hubs for generic biologics and vaccine manufacturing, and multi use bioreactors are becoming increasingly important across pharmaceutical, biotechnology, and contract manufacturing facilities. The growing focus on biosimilars, expanding government support for domestic biomanufacturing, and increasing availability of cost-efficient production technologies, alongside strong local pharmaceutical manufacturers, are key factors propelling the market in India

Multi Use Bioreactor Market Share

The Multi Use Bioreactor industry is primarily led by well-established companies, including:

- Sartorius AG (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher (U.S.)

- Merck KGaA (Germany)

- Eppendorf SE (Germany)

- Getinge AB (Sweden)

- ABEC, Inc. (U.S.)

- PBS Biotech, Inc. (U.S.)

- Meissner Filtration Products, Inc. (U.S.)

- Repligen Corporation (U.S.)

- Avantor, Inc. (U.S.)

- Entegris, Inc. (U.S.)

- Saint-Gobain Life Sciences (France)

- Parker Hannifin Corporation (U.S.)

- Alfa Laval AB (Sweden)

- Corning Incorporated (U.S.)

- Hamilton Company (U.S.)

- Lonza Group AG (Switzerland)

- GEA Group Aktiengesellschaft (Germany)

- Bioengineering AG (Switzerland)

What are the Recent Developments in Global Multi Use Bioreactor Market?

- In August 2025, Cytiva expanded its collaboration with Culture Biosciences to commercialize cloud-connected Stratyx 250 bioreactor systems and jointly develop additional scalable bioreactor formats. Under the agreement, Cytiva became the exclusive global distributor of the platform while both companies committed to advancing connected and automated bioprocessing technologies. This partnership reflects the industry’s increasing emphasis on smart manufacturing, scalable production systems, and digitally integrated biologics manufacturing infrastructure

- In April 2025, Culture Biosciences launched the Stratyx 250, a cloud-integrated mobile bioreactor platform designed to enable remote monitoring, automation, and AI-driven bioprocess optimization. The platform combines cloud-based software with flexible bioreactor hardware to support real-time process control and scalable biologics development workflows. This launch underscores the increasing adoption of digitalized and connected bioprocessing systems within the global bioreactor industry

- In April 2025, Thermo Fisher Scientific announced the launch of its 5L DynaDrive Single-Use Bioreactor, designed to accelerate bench-scale process development and simplify the transition from laboratory-scale production to commercial biologics manufacturing. The new system offers scalability from 1 to 5,000 liters and incorporates advanced automation and sustainable bioprocessing technologies to improve manufacturing efficiency. The launch reflects the company’s focus on supporting faster biologics commercialization and enhancing operational flexibility across biopharmaceutical production environments

- In April 2025, ABEC unveiled its Advanced Therapy Bioreactor (ATB™), a next-generation single-use bioreactor platform developed for cell therapy and advanced therapy medicinal product manufacturing. The system utilizes hollow fiber membrane technology and vibration-based mixing to enhance cell growth conditions while supporting closed, fully automated operations. This innovation demonstrates the growing industry focus on scalable and contamination-controlled bioprocessing solutions for sensitive cell therapy applications

- In March 2025, Cytiva announced the expansion of its Xcellerex X-platform portfolio with the introduction of new 500-L and 2000-L bioreactors aimed at supporting large-scale advanced therapeutics manufacturing. The expanded platform enables improved scalability from clinical development through commercial production while enhancing operational efficiency and reducing manufacturing risks. This development highlights Cytiva’s commitment to meeting the increasing global demand for biologics and next-generation therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.