Global Multimodal Imaging Fusion Systems Market

Market Size in USD Billion

USD

1.94 Billion

USD

6.14 Billion

2025

2033

USD

1.94 Billion

USD

6.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.94 Billion | |

| USD 6.14 Billion | |

| % | |

|

Multimodal Imaging Fusion Systems Market Size

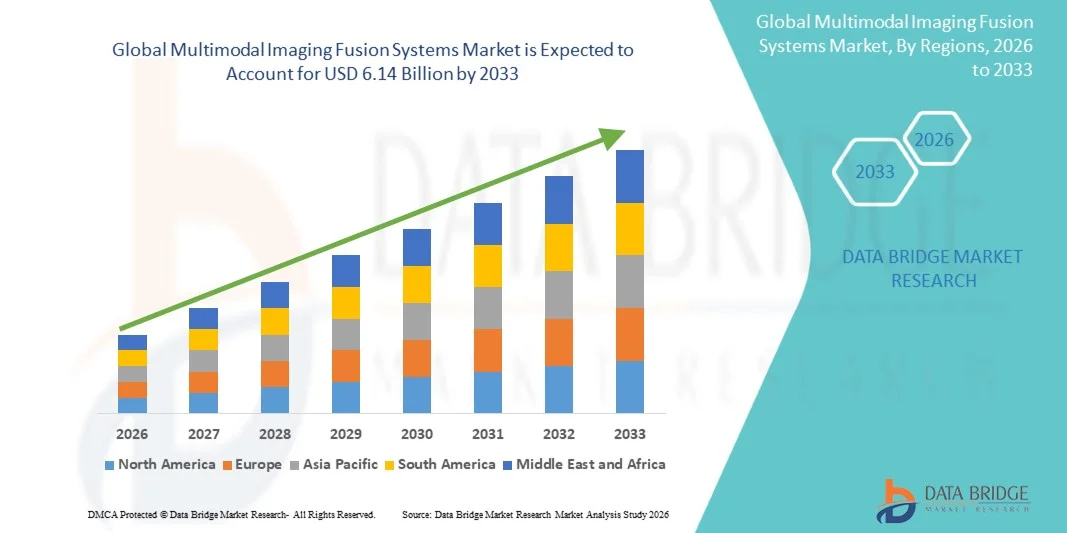

- The global multimodal imaging fusion systems market size was valued at USD 1.94 billion in 2025 and is expected to reach USD 6.14 billion by 2033, at a CAGR of 15.50% during the forecast period

- The market growth is largely fueled by increasing integration of advanced imaging technologies across diagnostic and clinical workflows, expanding adoption in healthcare, research, and industrial sectors, and ongoing improvements in image fusion software and AI‑enabled analytics that enhance diagnostic accuracy and workflow efficiency

- Furthermore, rising prevalence of chronic diseases growing demand for precise, non‑invasive diagnostic methods, and expanding investments in automated and AI‑enhanced imaging solutions are reinforcing multimodal imaging fusion systems as essential tools for modern diagnostics and research. These converging factors are accelerating the uptake of multimodal imaging solutions, thereby significantly boosting the industry’s growth

Multimodal Imaging Fusion Systems Market Analysis

- Multimodal imaging fusion systems, combining two or more imaging modalities such as PET/CT, PET/MRI, or SPECT/CT, are increasingly vital components of modern diagnostic and research workflows in both clinical and industrial settings due to their enhanced imaging accuracy, comprehensive visualization, and seamless integration with AI-driven analytics and workflow automation

- The escalating demand for multimodal imaging fusion systems is primarily fueled by the rising prevalence of chronic diseases such as cancer, cardiovascular, and neurological disorders, growing investments in advanced diagnostic technologies, and an increasing preference for non-invasive, precise imaging solutions that improve clinical decision-making and research outcomes

- North America dominated the multimodal imaging fusion systems market with the largest revenue share of 38.5% in 2025, characterized by early adoption of advanced imaging technologies, strong healthcare infrastructure, and a high presence of key industry players, with the U.S. experiencing substantial growth in installations in hospitals, diagnostic centers, and research institutions, driven by innovations in AI-enhanced image fusion software and hybrid imaging systems

- Asia-Pacific is expected to be the fastest-growing region in the multimodal imaging fusion systems market during the forecast period due to increasing healthcare investments, expanding medical infrastructure, rising awareness of advanced diagnostic imaging, and rapid adoption of hybrid imaging technologies in countries such as China, India, and Japan

- PET-CT systems segment dominated the multimodal imaging fusion systems market with a market share of 41.2% in 2025, driven by its established reliability for oncological and cardiovascular diagnostics and ease of integration into existing clinical workflows

Report Scope and Multimodal Imaging Fusion Systems Market Segmentation

|

Attributes |

Multimodal Imaging Fusion Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Multimodal Imaging Fusion Systems Market Trends

“Advancements in AI-Driven Image Fusion and Real-Time Analytics”

- A significant and accelerating trend in the global multimodal imaging fusion systems market is the deepening integration of artificial intelligence (AI) and machine learning algorithms for real-time image fusion, enhancing diagnostic accuracy and workflow efficiency across clinical and research applications

- For instance, the Siemens Biograph Vision PET/CT system incorporates AI-based reconstruction and fusion algorithms that enable clinicians to visualize multimodal images with higher clarity and speed, improving diagnostic confidence

- AI integration enables features such as automated lesion detection, adaptive image processing, and intelligent alerts for abnormal findings, while real-time analytics facilitate immediate clinical decision-making. For instance, GE Healthcare’s Discovery MI PET/CT leverages AI to highlight regions of interest automatically for radiologists

- The seamless integration of multimodal imaging systems with hospital PACS and cloud-based platforms allows centralized management of imaging data, facilitating collaboration among departments and across institutions

- This trend towards smarter, faster, and more intuitive imaging workflows is fundamentally transforming diagnostic imaging expectations, and companies such as Philips Healthcare are developing AI-enabled multimodal systems with automatic fusion, real-time analytics, and workflow optimization

- The demand for multimodal imaging fusion systems with integrated AI and advanced analytics is growing rapidly across both diagnostic and research sectors, as healthcare providers increasingly prioritize accuracy, efficiency, and comprehensive patient insights

- Cloud-based remote imaging and tele-radiology integration is emerging as a key trend, allowing specialists to access fused imaging data across locations for faster and collaborative diagnostics

Multimodal Imaging Fusion Systems Market Dynamics

Driver

“Rising Demand for Accurate Diagnostics and Advanced Clinical Imaging”

- The increasing prevalence of chronic diseases such as cancer, cardiovascular, and neurological disorders, combined with the need for precise, non-invasive imaging, is a significant driver for the heightened demand for multimodal imaging fusion systems

- For instance, in March 2025, Canon Medical launched the Celesteion PET/CT system with enhanced fusion capabilities to improve oncological and cardiac diagnostics, reinforcing advanced imaging adoption in hospitals

- As healthcare providers seek to improve patient outcomes through accurate diagnosis, multimodal imaging systems offer advanced features such as hybrid modality imaging, high-resolution fusion, and real-time analytics, providing a compelling alternative to single-modality systems

- Furthermore, expanding adoption of AI-based image processing and workflow automation in research and clinical trials is making multimodal systems essential for integrated diagnostic workflows, facilitating faster and more accurate results

- The ability to combine anatomical, functional, and molecular imaging in a single system, along with efficient image management and interpretation, is a key factor propelling adoption in hospitals, imaging centers, and research institutions

- Increasing investments in personalized medicine and targeted therapies are driving demand for multimodal imaging fusion, as these systems enable precise monitoring of treatment response

- Strategic collaborations between imaging system manufacturers and healthcare providers to develop customized fusion solutions are further supporting market growth

- Rising awareness of early disease detection and preventive healthcare among patients and clinicians is accelerating adoption of advanced imaging fusion technologies

Restraint/Challenge

“High Costs and Regulatory Compliance Barriers”

- The high cost of advanced multimodal imaging fusion systems, including hybrid PET/MRI and AI-enabled platforms, poses a significant challenge to widespread adoption, particularly in emerging markets or smaller healthcare facilities

- For instance, high acquisition and maintenance costs of systems such as Siemens Biograph Vision PET/CT make budget-constrained hospitals hesitant to invest in cutting-edge fusion imaging technologies

- Addressing regulatory compliance, including FDA, CE, and local approvals, alongside cybersecurity and patient data privacy, is crucial for market acceptance, as strict clinical standards must be met before deployment

- Furthermore, the relatively complex operation and need for trained personnel can limit adoption, especially in regions lacking skilled radiologists or technicians, while lower-cost alternatives may not provide the same imaging precision

- While prices are gradually stabilizing and AI-assisted operation reduces workflow complexity, the perceived premium for advanced fusion technology can still hinder adoption in cost-sensitive markets

- Overcoming these challenges through cost optimization, regulatory guidance support, and enhanced training programs for clinical staff will be vital for sustained market growth

- Limited standardization across different fusion systems and software platforms may hinder interoperability and workflow integration in multi-vendor healthcare environments

- Maintenance and service requirements for sophisticated hybrid imaging equipment can be a logistical and financial burden for hospitals and diagnostic centers, especially in developing regions

Multimodal Imaging Fusion Systems Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the multimodal imaging fusion systems market is segmented into multimodal imaging equipment, reagents, and software. The multimodal imaging equipment segment dominated the market with the largest market revenue share in 2025, driven by the increasing deployment of hybrid imaging systems such as PET-CT, PET-MRI, and SPECT-CT in hospitals and advanced diagnostic centers. Healthcare providers prefer integrated imaging equipment because it enables simultaneous acquisition of anatomical and functional information, improving diagnostic precision and treatment planning. The growing prevalence of cancer and neurological disorders is encouraging hospitals to invest in sophisticated multimodal imaging infrastructure. In addition, continuous technological advancements such as improved detectors, faster scanning speeds, and AI-assisted image reconstruction are further strengthening equipment adoption. The segment also benefits from strong demand in academic research and pharmaceutical trials, where high-performance imaging systems are required for disease monitoring and therapy evaluation.

The software segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising integration of artificial intelligence and advanced image-processing algorithms into diagnostic workflows. Fusion software enables clinicians to combine data from multiple imaging modalities into a single detailed visualization, improving accuracy and clinical decision-making. Hospitals and diagnostic centers are increasingly adopting advanced software solutions to enhance workflow efficiency and reduce the burden on radiologists. The rapid adoption of cloud-based platforms and remote imaging analysis is further accelerating the demand for imaging fusion software. In addition, software upgrades allow healthcare providers to enhance imaging capabilities without replacing expensive hardware systems. Growing interest in AI-driven diagnostics and automated lesion detection is expected to significantly support the expansion of this segment in the coming years.

- By Technology

On the basis of technology, the multimodal imaging fusion systems market is segmented into PET-CT systems, PET-MRI systems, and SPECT-CT systems. The PET-CT systems segment held the largest market revenue share of 41.2% in 2025 driven by its widespread adoption in oncology diagnostics and disease monitoring. PET-CT combines metabolic imaging from PET with anatomical imaging from CT, allowing clinicians to identify tumors with high precision. Hospitals and cancer centers rely heavily on PET-CT for staging cancers, evaluating treatment response, and detecting metastasis. Technological innovations such as time-of-flight imaging and AI-assisted reconstruction have improved image clarity and reduced scan times. The availability of established radiotracers and trained medical professionals further contributes to the dominance of PET-CT technology. Growing cancer prevalence worldwide continues to strengthen demand for this imaging modality.

The PET-MRI systems segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its superior soft-tissue imaging capabilities and lower radiation exposure compared to PET-CT. PET-MRI is particularly valuable for neurological, pediatric, and cardiovascular imaging applications where radiation reduction is important. Research institutions and advanced hospitals are increasingly investing in PET-MRI systems for precision medicine and clinical research programs. The technology provides enhanced functional and structural imaging, making it useful for complex disease analysis. Integration with AI-based imaging software further improves diagnostic accuracy and workflow efficiency. Increasing investments in advanced healthcare infrastructure and research initiatives are expected to support the rapid growth of this segment.

- By Application

On the basis of application, the multimodal imaging fusion systems market is segmented into oncology, cardiology, neurology, ophthalmology, musculoskeletal disorders, and other clinical uses. The oncology segment dominated the market with the largest revenue share in 2025, reflecting the critical role of multimodal imaging in cancer detection, staging, and treatment monitoring. Hybrid imaging technologies such as PET-CT and PET-MRI provide detailed visualization of tumor metabolism and anatomical structure simultaneously. This capability helps oncologists detect malignancies at early stages and design personalized treatment plans. The increasing global burden of cancer is a major factor driving demand for multimodal imaging in oncology applications. Pharmaceutical companies also use advanced imaging systems in clinical trials to evaluate treatment responses and drug efficacy. Continuous improvements in imaging resolution and AI-assisted diagnostics further strengthen the importance of multimodal imaging in cancer management.

The cardiology segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising incidence of cardiovascular diseases worldwide. Multimodal imaging systems allow clinicians to evaluate cardiac structure, blood flow, and metabolic activity simultaneously. This integrated approach supports accurate diagnosis of conditions such as coronary artery disease and myocardial ischemia. Advanced PET-CT and PET-MRI systems provide detailed cardiac imaging while minimizing invasive procedures. Increasing awareness about early heart disease detection and preventive healthcare is encouraging adoption of advanced cardiac imaging technologies. Growing investments in specialized cardiac centers and diagnostic infrastructure are also expected to accelerate growth in this segment.

- By End User

On the basis of end user, the multimodal imaging fusion systems market is segmented into hospitals, diagnostic imaging centers, academic & research institutions, and other end-users. The hospitals segment held the largest market revenue share in 2025 driven by the high demand for advanced diagnostic capabilities and integrated healthcare services. Hospitals perform a large volume of diagnostic procedures and require comprehensive imaging systems to support various medical specialties such as oncology, cardiology, and neurology. Multimodal imaging fusion systems help hospitals improve diagnostic accuracy and optimize treatment planning. The presence of trained radiologists and specialized departments further supports the adoption of advanced imaging equipment in hospital settings. In addition, hospitals often serve as major centers for clinical trials and research collaborations. Rising investments in hospital infrastructure and modernization of healthcare facilities are strengthening the dominance of this segment.

The diagnostic imaging centers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for specialized and cost-efficient diagnostic services. Imaging centers are rapidly adopting multimodal imaging technologies to provide advanced diagnostic capabilities without the high overhead costs associated with large hospitals. These centers focus on high patient throughput and efficient imaging workflows, making fusion imaging software and hybrid systems highly valuable. The expansion of private healthcare networks and outpatient diagnostic services is further fueling the growth of this segment. Many imaging centers are forming partnerships with hospitals and healthcare providers to offer specialized imaging services. Growing awareness among patients regarding early disease detection and advanced diagnostic techniques is expected to accelerate the expansion of this segment.

Multimodal Imaging Fusion Systems Market Regional Analysis

- North America dominated the multimodal imaging fusion systems market with the largest revenue share of 38.5% in 2025, characterized by early adoption of advanced imaging technologies, strong healthcare infrastructure, and a high presence of key industry players

- Healthcare providers in the region highly value the improved diagnostic accuracy, integrated imaging capabilities, and advanced analytics offered by multimodal imaging systems, particularly in critical applications such as oncology, cardiology, and neurology

- This widespread adoption is further supported by significant healthcare expenditure, strong research and development activities, and the presence of leading medical imaging companies, establishing multimodal imaging fusion systems as essential tools for advanced diagnostics and clinical research across hospitals and specialized imaging centers

U.S. Multimodal Imaging Fusion Systems Market Insight

The U.S. multimodal imaging fusion systems market captured the largest revenue share of 79% in 2025 within North America, fueled by strong adoption of advanced diagnostic imaging technologies and the presence of leading medical imaging companies. Healthcare providers are increasingly prioritizing accurate disease detection through hybrid imaging solutions such as PET-CT and PET-MRI systems. The growing demand for early diagnosis of cancer, neurological, and cardiovascular diseases further propels the imaging technology industry. Moreover, the increasing integration of artificial intelligence, cloud-based imaging platforms, and advanced analytics into diagnostic workflows is significantly contributing to the market's expansion.

Europe Multimodal Imaging Fusion Systems Market Insight

The Europe multimodal imaging fusion systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong healthcare infrastructure and increasing investments in advanced medical imaging technologies. The rise in chronic diseases and demand for precise diagnostic solutions is fostering the adoption of hybrid imaging systems. European healthcare providers are also attracted to the accuracy and clinical efficiency these systems offer. The region is experiencing notable growth across hospitals, diagnostic imaging centers, and research institutions, with multimodal imaging systems being incorporated into both new healthcare facilities and modernization projects.

U.K. Multimodal Imaging Fusion Systems Market Insight

The U.K. multimodal imaging fusion systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing demand for advanced diagnostic technologies and improved patient outcomes. In addition, rising cases of cancer and neurological disorders are encouraging healthcare providers to adopt hybrid imaging solutions. The U.K.’s emphasis on medical research, alongside its well-established healthcare infrastructure and clinical research ecosystem, is expected to continue to stimulate market growth.

Germany Multimodal Imaging Fusion Systems Market Insight

The Germany multimodal imaging fusion systems market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing adoption of technologically advanced diagnostic equipment and strong investment in healthcare innovation. Germany’s well-developed healthcare infrastructure, combined with its focus on research and medical technology development, promotes the adoption of multimodal imaging systems, particularly in hospitals and academic institutions. The integration of advanced imaging systems with AI-enabled diagnostic platforms is also becoming increasingly prevalent, with a strong preference for precision and high-quality clinical diagnostics aligning with local healthcare standards.

Asia-Pacific Multimodal Imaging Fusion Systems Market Insight

The Asia-Pacific multimodal imaging fusion systems market is poised to grow at the fastest CAGR of 13% during the forecast period of 2026 to 2033, driven by expanding healthcare infrastructure, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region's increasing focus on early disease diagnosis and advanced imaging solutions is driving the adoption of multimodal imaging systems. Furthermore, as APAC emerges as a significant hub for medical technology manufacturing and healthcare innovation, the accessibility and deployment of advanced imaging systems are expanding across hospitals and diagnostic centers.

Japan Multimodal Imaging Fusion Systems Market Insight

The Japan multimodal imaging fusion systems market is gaining momentum due to the country’s advanced healthcare technology landscape, rapid adoption of precision diagnostics, and growing demand for early disease detection. The Japanese healthcare sector places strong emphasis on accurate medical imaging, and the adoption of multimodal systems is driven by the increasing number of specialized hospitals and research facilities. The integration of hybrid imaging systems with AI-based diagnostic platforms is fueling growth. Moreover, Japan's aging population is expected to spur demand for advanced diagnostic technologies for the effective management of chronic diseases.

India Multimodal Imaging Fusion Systems Market Insight

The India multimodal imaging fusion systems market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's rapidly expanding healthcare infrastructure, rising investments in medical technology, and increasing demand for advanced diagnostic imaging. India stands as one of the fastest-growing markets for healthcare technology adoption, and multimodal imaging systems are becoming increasingly important in hospitals, diagnostic centers, and research institutions. The push toward digital healthcare initiatives and modernization of healthcare facilities, alongside growing domestic and international investments in medical imaging technology, are key factors propelling the market in India.

Multimodal Imaging Fusion Systems Market Share

The Multimodal Imaging Fusion Systems industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Shimadzu Corporation (Japan)

- Bruker Corporation (U.S.)

- PerkinElmer Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Carl Zeiss AG (Germany)

- Miltenyi Biotec B.V. & Co. KG (Germany)

- Aspect Imaging Ltd. (Israel)

- Cubresa Inc. (Canada)

- MR Solutions Ltd (U.K.)

- MILabs B.V. (Netherlands)

- TriFoil Imaging (U.S.)

- Mediso Ltd. (Hungary)

- Carestream Health, Inc. (U.S.)

- United Imaging Healthcare Co., Ltd. (China)

- Positron Corporation (U.S.)

What are the Recent Developments in Global Multimodal Imaging Fusion Systems Market?

- In November 2025, GE HealthCare announced that its Omni 128 cm Total-Body PET/CT system received CE Mark approval, enabling commercialization in European markets. The advanced hybrid imaging system is designed to deliver high-sensitivity total-body scanning and faster image acquisition for oncology, cardiology, and neurology applications. The system also integrates AI-based image processing and advanced detector technology to enhance diagnostic accuracy and workflow efficiency

- In June 2025, United Imaging Healthcare showcased several next-generation PET/CT imaging technologies and its uExcel technology platform at the SNMMI 2025 conference. The platform enables scalable hybrid imaging solutions that share key components across systems, improving efficiency and reducing engineering complexity. These technologies support higher resolution imaging, advanced data processing, and improved accessibility for hospitals and research institutions

- In October 2024, GE HealthCare expanded production of its Omni Legend PET/CT scanner by establishing manufacturing operations in the United States at its facility in Waukesha, Wisconsin. The hybrid imaging system integrates PET and CT technologies to provide detailed anatomical and functional imaging for disease detection and treatment monitoring. The move aims to strengthen supply chain capabilities and increase availability of advanced multimodal imaging systems for healthcare providers

- In June 2024, GE HealthCare introduced AI-powered reconstruction and imaging technologies for PET/CT and SPECT systems during the Society of Nuclear Medicine and Molecular Imaging (SNMMI) meeting. The innovations include deep-learning reconstruction tools designed to reduce image noise while maintaining high diagnostic accuracy. These technologies aim to enhance image clarity, reduce scanning time, and improve clinical workflow efficiency

- In June 2023, GE HealthCare launched the SIGNA PET/MR AIR system, an advanced hybrid imaging platform combining positron emission tomography (PET) and magnetic resonance imaging (MRI) technologies. The system integrates deep-learning-based MR image reconstruction and lightweight AIR coil technology to improve image quality and patient comfort while reducing scan times. It is designed to support precise diagnosis and treatment planning for diseases such as cancer and neurological disorders

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.