Global Mycetoma Treatment Market

Market Size in USD Million

USD

420.50 Million

USD

616.55 Million

2024

2032

USD

420.50 Million

USD

616.55 Million

2024

2032

| 2025 - 2032 | |

| USD 420.50 Million | |

| USD 616.55 Million | |

| % | |

|

Mycetoma Treatment Market Size

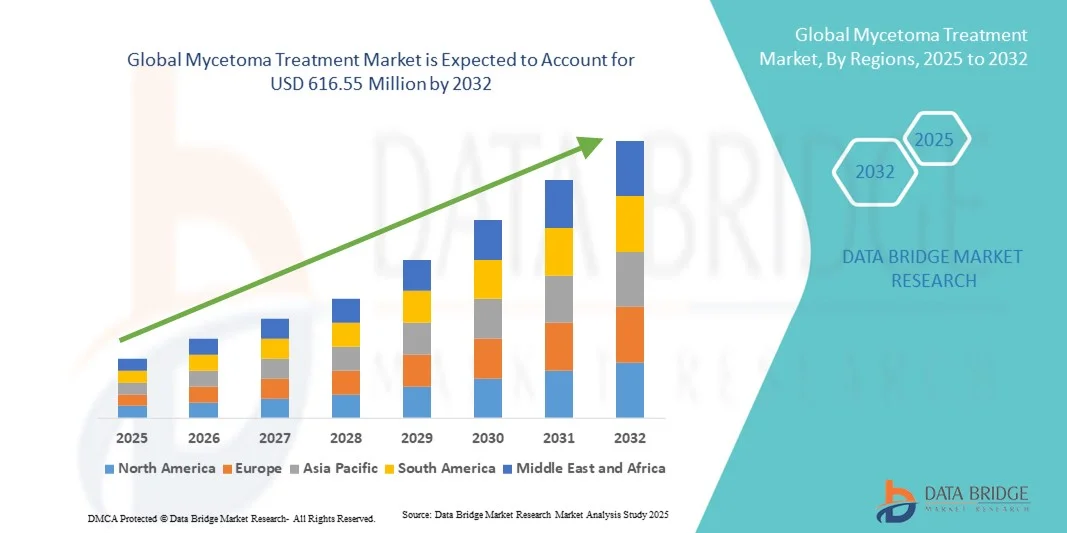

- The global mycetoma treatment market size was valued at USD 420.50 million in 2024 and is expected to reach USD 616.55 million by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely driven by the increasing prevalence of mycetoma cases across endemic regions, coupled with growing awareness and advancements in antifungal and antibacterial therapeutics for effective disease management

- Furthermore, rising investments in rare disease research, improved diagnostic capabilities, and government initiatives supporting neglected tropical disease treatment are fostering market expansion. These combined factors are enhancing access to advanced therapies, thereby significantly accelerating the growth of the mycetoma treatment industry.

Mycetoma Treatment Market Analysis

- Mycetoma treatments, including antifungal and antibacterial therapies, are increasingly vital for managing chronic subcutaneous infections due to their targeted effectiveness and ability to prevent severe tissue damage and disability

- The escalating demand for mycetoma treatment is primarily fueled by rising disease awareness, growing prevalence of actinomycetoma and eumycetoma, and increasing patient preference for accessible, effective, and well-tolerated medication regimens

- North America dominated the mycetoma treatment market with the largest revenue share of 40.7% in 2024, characterized by advanced healthcare infrastructure, strong research and development initiatives, and increasing government support for neglected tropical disease treatment programs, with the U.S. experiencing substantial growth in treatment adoption and clinical trials

- Asia-Pacific is expected to be the fastest-growing region in the mycetoma treatment market during the forecast period due to improving healthcare access, rising awareness campaigns, and increasing availability of antifungal and antibiotic therapies

- Actinomycetoma segment dominated the market with a revenue share of 42.8% in 2024, driven by higher global incidence and well-established antibiotic treatment protocols

Report Scope and Mycetoma Treatment Market Segmentation

|

Attributes |

Mycetoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Mycetoma Treatment Market Trends

Advancements in Oral and Combination Therapies

- A significant and accelerating trend in the global mycetoma treatment market is the development of oral antifungal and combination antibiotic therapies, enhancing treatment efficacy while reducing the need for surgical interventions

- For instance, fosravuconazole is being explored as an oral therapy for eumycetoma, offering patients improved compliance and minimizing hospital visits

- These advanced treatment options enable longer-term therapy with fewer side effects, providing better patient adherence and outcomes in endemic regions

- The integration of combination therapies targeting both actinomycetoma and eumycetoma is facilitating personalized treatment protocols and optimized clinical results

- This trend towards more accessible, effective, and patient-friendly treatment regimens is fundamentally reshaping clinical expectations and care strategies for mycetoma management

- The demand for innovative oral and combination therapies is growing rapidly, as patients and healthcare providers increasingly prioritize treatment accessibility and improved clinical outcomes

Mycetoma Treatment Market Dynamics

Driver

Rising Disease Awareness and Healthcare Initiatives

- The increasing prevalence of mycetoma and rising awareness among healthcare providers and communities are key drivers for heightened treatment demand

- For instance, the Drugs for Neglected Diseases initiative (DNDi) has launched programs to promote accessible treatment and research in endemic regions, boosting market adoption

- As patients become more aware of disease symptoms and available therapies, timely diagnosis and early treatment help reduce complications and disability

- Furthermore, government and NGO initiatives improving healthcare access are making treatments more widely available, particularly in Africa, Asia, and Latin America

- Collaboration between pharmaceutical companies and public health organizations is strengthening drug accessibility and affordability in endemic regions

- The integration of awareness campaigns, improved healthcare infrastructure, and research initiatives collectively drives the growth of the mycetoma treatment market

- The development of outreach programs, community health campaigns, and local distribution channels are key factors propelling the adoption of mycetoma treatments in underserved areas

Restraint/Challenge

Limited Drug Availability and Treatment Costs

- Limited availability of essential antifungal and antibiotic drugs in endemic regions poses a significant challenge to broader market penetration

- For instance, logistical hurdles in distributing medications in remote areas make consistent treatment difficult, delaying therapy and reducing efficacy

- Addressing these challenges through improved supply chains, local manufacturing, and subsidy programs is crucial for increasing treatment coverage. Additionally, the relatively high cost of newer oral antifungal therapies compared to traditional regimens can be a barrier for low-income patients

- While generic drugs are available, limited production and regulatory hurdles can hinder access, especially in rural and underserved regions

- Lack of trained healthcare professionals in endemic areas can delay diagnosis and proper treatment, affecting patient outcomes

- Cultural stigma and low disease awareness in certain regions may lead to late-stage treatment seeking, limiting therapy effectiveness

- Overcoming these challenges through improved affordability, wider drug availability, healthcare training, and awareness campaigns will be vital for sustained market growth

Mycetoma Treatment Market Scope

The market is segmented on the basis of type, antibiotic type, treatment type, route of administration, mode of purchase, and distribution channel.

- By Type

On the basis of type, the mycetoma treatment market is segmented into Actinomycetoma and Eumycetoma. The Actinomycetoma segment dominated the market with the largest revenue share of 42.8% in 2024, driven by its higher global prevalence, particularly in Africa and Asia. Actinomycetoma is more responsive to standard antibiotic therapies, making it easier for healthcare providers to establish consistent treatment protocols. Governments and NGOs focus on providing accessible antibiotics in endemic regions, further strengthening the market share of this segment. Patients benefit from well-established regimens, increasing adherence and reducing complications. The availability of treatment guidelines and training programs for actinomycetoma also reinforces its dominance. Overall, the combination of higher incidence, effective therapies, and structured healthcare support sustains its market leadership.

The Eumycetoma segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising research in oral antifungal therapies such as fosravuconazole. Eumycetoma often requires prolonged treatment or combination therapy, creating demand for newer, patient-friendly solutions. Increasing clinical trials and governmental programs to improve access in remote regions are boosting market uptake. Patient awareness campaigns and digital health solutions supporting adherence are also contributing to growth. Additionally, improved diagnostic tools are facilitating early detection, enhancing treatment outcomes. The segment’s rapid growth reflects both unmet medical needs and emerging treatment innovations.

- By Antibiotic Type

On the basis of antibiotic type, the market is segmented into Netilmicin-TS and Sulfonamides DDS (4,4 diaminodiphenyl-sulfone). The Sulfonamides DDS segment dominated the market in 2024 due to its long-standing use in actinomycetoma treatment and proven efficacy in endemic regions. Sulfonamides are widely available through hospital and retail pharmacies, making them accessible even in low-resource areas. Physicians favor this antibiotic for its predictable outcomes and manageable side-effect profile. Awareness programs by NGOs and health ministries often highlight Sulfonamides as the primary therapy for actinomycetoma, reinforcing adoption. Bulk production and affordability also help maintain its dominance. Furthermore, training healthcare workers on dosage protocols strengthens compliance and treatment success rates.

The Netilmicin-TS segment is expected to witness the fastest growth from 2025 to 2032, driven by its effectiveness in combination therapies and rising inclusion in clinical guidelines for mycetoma management. The injectable form allows targeted treatment in severe cases, improving patient outcomes. Increased research and advocacy for more accessible antibiotic formulations are boosting market expansion. Hospitals and specialty clinics in emerging markets are adopting Netilmicin-TS for resistant cases. Patient adherence is enhanced through supervised therapy programs. Its growth is supported by ongoing investment in antibiotic innovation and distribution.

- By Treatment Type

On the basis of treatment type, the market is segmented into medication and supportive care. The Medication segment dominated the market in 2024, driven by the necessity of antifungal and antibacterial therapies as primary treatment modalities. Medication offers the most direct path to infection control and is supported by well-established clinical protocols. Public health initiatives prioritize medication distribution in endemic regions, ensuring consistent market demand. Accessibility through hospital and retail pharmacies strengthens patient adherence. Clinical evidence demonstrating improved recovery rates reinforces the reliance on medication. Healthcare professionals continue to recommend drug therapy as the first line of treatment, maintaining its dominant position.

The Supportive Care segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing awareness of holistic patient management, including wound care, physiotherapy, and nutritional support. Integration of supportive care with medication improves overall treatment outcomes. Community health programs emphasizing patient education and follow-up care are expanding adoption. Telemedicine platforms and mobile health apps enable remote monitoring, enhancing compliance. The focus on quality of life during treatment drives demand. Growth is further strengthened by NGO initiatives promoting comprehensive patient management strategies.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The Oral segment dominated the market in 2024 due to its convenience, better patient compliance, and suitability for long-term therapy in outpatient settings. Oral medications allow patients to continue treatment at home, reducing hospitalization costs. Public health campaigns and awareness programs often emphasize oral regimens for their ease of use. Widespread availability in pharmacies ensures reliable access. Oral therapy’s safety profile and minimal supervision requirements further drive adoption. Combined with combination therapy protocols, oral medications remain the preferred choice in endemic regions.

The Parenteral segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing use of injectable antibiotics such as Netilmicin-TS in severe or resistant cases. Parenteral administration ensures precise dosing and rapid therapeutic effect. Hospitals and specialty clinics are adopting injectable treatments for critical patients. Research into outpatient injectable therapies is improving accessibility. Training programs for healthcare providers are enhancing proper administration. Rising clinical adoption in emerging markets supports the segment’s growth trajectory.

- By Mode of Purchase

On the basis of mode of purchase, the market is segmented into prescription and over the counter (OTC). The Prescription segment dominated the market in 2024 due to the requirement of professional supervision for accurate diagnosis and treatment, especially for actinomycetoma and eumycetoma. Prescription ensures correct dosage, reduces side effects, and supports adherence to long-term therapy. Hospitals and clinics act as primary distribution points for prescription medications. Public health regulations in most regions mandate prescription-only access for antibiotics and antifungals. Awareness campaigns emphasize supervised treatment to prevent resistance. Prescription-driven access continues to strengthen this segment’s dominance.

The OTC segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing patient awareness and accessibility of supportive care medications and basic antifungals in retail and online pharmacies. Convenience and reduced need for hospital visits are boosting adoption. Rising e-pharmacy platforms improve reach in remote areas. Education on self-monitoring and adherence supports safe OTC usage. OTC availability also facilitates early treatment initiation, improving outcomes. The combination of convenience, awareness, and digital distribution drives growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The Hospital Pharmacies segment dominated the market in 2024 due to direct access to healthcare providers and structured prescription-based treatment programs. Hospital pharmacies provide medications under professional supervision, ensuring compliance with treatment protocols. Endemic regions rely on hospitals for distributing essential antifungal and antibacterial drugs. Clinical follow-up and monitoring are integrated with hospital-based medication distribution. Public health initiatives often leverage hospitals for targeted drug delivery. The segment benefits from established infrastructure and trusted healthcare networks, maintaining its dominant position.

The Online Pharmacies segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing penetration of digital health platforms and rising e-commerce adoption in emerging markets. Online pharmacies improve accessibility for patients in remote areas. Mobile apps and telemedicine services facilitate safe ordering and adherence monitoring. Convenience, privacy, and doorstep delivery are key adoption factors. Awareness campaigns and improved payment systems are boosting confidence in online purchases. The segment’s rapid growth reflects the digitalization of healthcare delivery and patient demand for convenience.

Mycetoma Treatment Market Regional Analysis

- North America dominated the mycetoma treatment market with the largest revenue share of 40.7% in 2024, characterized by advanced healthcare infrastructure, strong research and development initiatives, and increasing government support for neglected tropical disease treatment programs, with the U.S. experiencing substantial growth in treatment adoption and clinical trials

- Patients and healthcare providers in the region highly value timely diagnosis, effective antibiotic and antifungal therapies, and comprehensive care programs that improve treatment outcomes and reduce complications

- This widespread adoption is further supported by high healthcare spending, well-established clinical guidelines, ongoing research and clinical trials, and strong public health campaigns, establishing mycetoma treatments as a key solution for managing chronic subcutaneous infections

U.S. Mycetoma Treatment Market Insight

The U.S. mycetoma treatment market captured the largest revenue share of 81% in 2024 within North America, fueled by advanced healthcare infrastructure and rising awareness of neglected tropical diseases. Patients and healthcare providers increasingly prioritize timely diagnosis and effective treatment with antibiotics and antifungal therapies. The growing adoption of telemedicine and digital health solutions, alongside patient adherence programs, further propels market growth. Moreover, the presence of strong R&D initiatives and clinical trials for novel treatments significantly contributes to the market's expansion. Early intervention programs and public health campaigns also support widespread uptake of mycetoma therapies.

Europe Mycetoma Treatment Market Insight

The Europe mycetoma treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing disease awareness, structured healthcare systems, and access to advanced therapies. Rising urbanization and well-established medical facilities are fostering the adoption of mycetoma treatments. European healthcare providers emphasize comprehensive patient care, integrating medication with supportive care and monitoring. Government health programs and NGO initiatives promoting tropical disease management further stimulate market growth. The region is witnessing increased clinical research and pharmaceutical investments, enhancing treatment availability. Patients in both residential and commercial healthcare settings benefit from structured, guideline-based interventions.

U.K. Mycetoma Treatment Market Insight

The U.K. mycetoma treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the focus on early diagnosis and effective treatment to prevent long-term disability. Increasing awareness campaigns, along with robust healthcare infrastructure, are encouraging patients to seek timely therapy. The country’s adoption of telemedicine platforms and e-health initiatives supports monitoring and adherence. Public and private healthcare programs are improving access to both antibiotics and antifungal therapies. Rising interest in global tropical disease research is also contributing to market growth. Structured community health programs further enhance treatment reach in high-risk populations.

Germany Mycetoma Treatment Market Insight

The Germany mycetoma treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of rare and neglected tropical diseases. The country’s advanced healthcare infrastructure, emphasis on innovation, and strong clinical research environment promote adoption of effective mycetoma therapies. Integration of digital health tools, telemedicine, and patient monitoring systems is becoming increasingly prevalent. German patients show a strong preference for standardized, evidence-based treatment protocols. Government initiatives to support infectious disease management further strengthen the market. Hospitals and specialty clinics play a key role in delivering therapy and follow-up care.

Asia-Pacific Mycetoma Treatment Market Insight

The Asia-Pacific mycetoma treatment market is poised to grow at the fastest CAGR during the forecast period, driven by rising disease prevalence, expanding healthcare infrastructure, and increasing awareness programs in countries such as India, China, and Thailand. Government-led health initiatives and NGO campaigns are facilitating early diagnosis and treatment adherence. Telemedicine and mobile health solutions are improving access in remote areas. Rising disposable incomes and urbanization are enhancing patients’ ability to seek timely care. Public-private partnerships are increasing the availability of antifungal and antibiotic therapies. The region’s growing investment in healthcare technology and training supports the rapid adoption of mycetoma treatments.

Japan Mycetoma Treatment Market Insight

The Japan mycetoma treatment market is gaining momentum due to the country’s advanced healthcare systems, high awareness of rare diseases, and emphasis on patient-centered care. Early diagnosis programs and telemedicine platforms are improving treatment adherence. Integration of digital tools enables better monitoring of long-term therapy outcomes. The aging population drives demand for easier-to-administer treatments and supportive care. Clinical research on novel antifungal therapies is expanding the available treatment options. Patients benefit from structured follow-up care and advanced hospital infrastructure, fueling market growth in both residential and clinical settings.

India Mycetoma Treatment Market Insight

The India mycetoma treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to high disease prevalence, growing healthcare awareness, and expanding access to medications. The country’s increasing urbanization, improving medical infrastructure, and government initiatives for tropical disease management are key drivers. Affordable antibiotic and antifungal therapies, along with NGO-led outreach programs, are increasing treatment accessibility. Telemedicine and mobile health solutions are enhancing patient monitoring in remote areas. Rising patient awareness and education campaigns are encouraging timely treatment. Strong domestic pharmaceutical manufacturers and government support further propel market growth.

Mycetoma Treatment Market Share

The Mycetoma Treatment industry is primarily led by well-established companies, including:

- Biochem Pharma (India)

- Zydus Group (India)

- GSK plc (U.K.)

- Vernalis Limited (U.K.)

- Irisfarma (Italy)

- Sun Pharmaceutical Industries Ltd (India)

- Sanofi (France)

- Pfizer Inc (U.S.)

- GALDERMA (U.S.)

- Mayne Pharma Group Limited (Australia)

- Akorn (U.S.)

- Johnson & Johnson Services, Inc (U.S.)

- Medimetriks Pharmaceuticals, Inc (U.S.)

- F-Hoffmann-La Roche (Switzerland)

- Eisai Co., Ltd. (Japan)

- Panacea Biotec (India)

- ViiV Healthcare (U.K.)

- Xellia Pharmaceuticals (Denmark)

What are the Recent Developments in Global Mycetoma Treatment Market?

- In July 2025, the LEO Foundation partnered with the Drugs for Neglected Diseases initiative (DNDi) to develop a new treatment method for mycetoma. This partnership focuses on advancing the clinical development of oxfendazole as an anti-parasitic macrofilaricidal treatment and supporting epidemiological studies to understand the burden and distribution of mycetoma in endemic areas

- In June 2025, researchers developed a clinical scoring system to assess the activity and severity of mycetoma. This tool aids clinicians in evaluating the progression of the disease, tailoring treatment plans, and monitoring patient outcomes more effectively. The scoring system enhances the standardization of care and supports clinical decision-making in managing mycetoma cases

- In October 2024, a comprehensive database of mycetoma tissue microscopic images was introduced to facilitate automated detection and classification of mycetoma. The database includes images from 142 patients, providing a valuable resource for histopathological analysis and aiding in the accurate diagnosis of mycetoma, especially in regions with limited access to specialized pathology services

- In July 2024, Eisai Co., Ltd. entered into a license agreement with the Drugs for Neglected Diseases initiative (DNDi) to jointly develop fosravuconazole as a novel treatment for mycetoma, a neglected tropical disease. This collaboration aims to advance the clinical development of fosravuconazole and support epidemiological studies to understand the burden and distribution of mycetoma in endemic areas

- In November 2023, the Drugs for Neglected Diseases initiative (DNDi) and Eisai Co., Ltd. announced the completion of a Phase II clinical trial for fosravuconazole, an oral antifungal agent, for the treatment of eumycetoma. The trial demonstrated that fosravuconazole is safe, well-tolerated, and effective, offering a more affordable alternative to the standard treatment, itraconazole, which is often inaccessible in endemic regions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.