Global Mydriasis Market

Market Size in USD Billion

USD

675.50 Billion

USD

1,250.30 Billion

2025

2033

USD

675.50 Billion

USD

1,250.30 Billion

2025

2033

| 2026 - 2033 | |

| USD 675.50 Billion | |

| USD 1,250.30 Billion | |

| % | |

|

Mydriasis Market Size

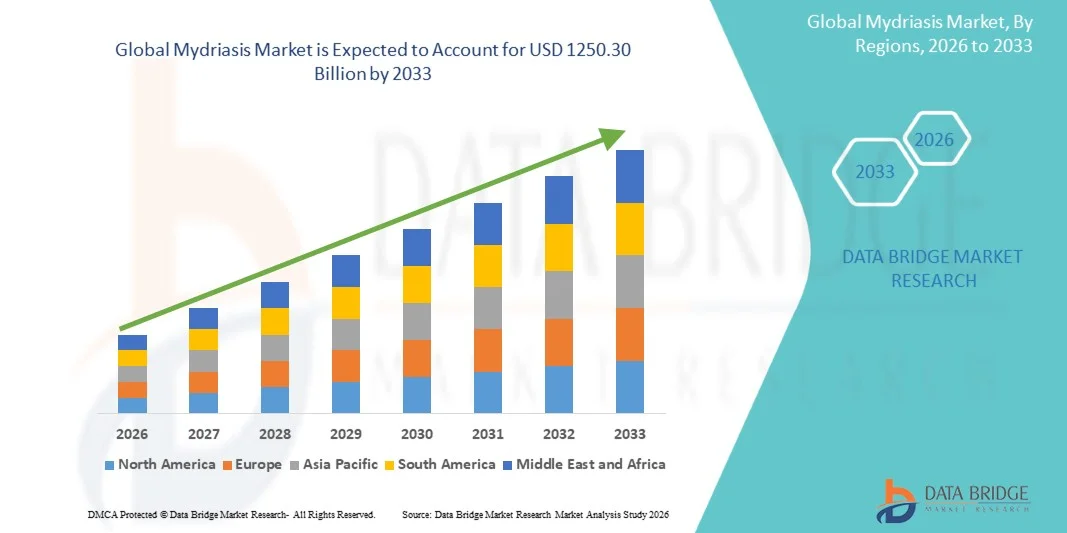

- The global Mydriasis market size was valued at USD 675.50 billion in 2025and is expected to reach USD 1250.30 billion by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of eye disorders requiring diagnostic and surgical procedures, along with the rising demand for ophthalmic examinations that utilize pupil dilation agents for accurate retinal assessment and diagnosis of underlying ocular conditions

- Furthermore, growing awareness regarding early detection of vision-related diseases, expanding access to advanced ophthalmic care, and increasing adoption of routine eye screening practices are establishing mydriasis agents as an essential component in modern ophthalmology. These converging factors are accelerating the uptake of Mydriasis solutions, thereby significantly boosting the industry's growth

Mydriasis Market Analysis

- Mydriasis agents, which are pharmacological eye-dilating solutions used to widen the pupil for diagnostic and surgical ophthalmic examinations, are increasingly vital components of modern eye care and clinical diagnostics due to their essential role in enabling accurate retinal assessment, cataract evaluation, and posterior segment visualization

- The escalating demand for Mydriasis is primarily fueled by the rising prevalence of ophthalmic disorders, increasing number of routine eye examinations, growing geriatric population, and expanding adoption of advanced diagnostic imaging techniques in ophthalmology clinics and hospitals

- North America dominated the Mydriasis market with the largest revenue share of 38.7% in 2025, characterized by advanced ophthalmic healthcare infrastructure, high adoption of routine eye screening practices, and strong presence of key pharmaceutical and ophthalmic solution manufacturers, with the U.S. witnessing substantial growth in diagnostic eye procedures supported by advanced clinical technologies and increasing awareness of preventive eye care

- Asia-Pacific is expected to be the fastest growing region in the Mydriasis market during the forecast period due to rising healthcare expenditure, increasing incidence of vision disorders, improving access to ophthalmic services, and growing awareness regarding early diagnosis of eye diseases across countries such as China and India

- The topical segment dominated the largest market revenue share of 60.7% in 2025, driven by the widespread use of eye drops and topical ophthalmic agents for pupil dilation management

Report Scope and Mydriasis Market Segmentation

|

Attributes |

Mydriasis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Bausch + Lomb (U.S.) |

|

Market Opportunities |

· Integration with IoT and Smart Home Ecosystems · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Mydriasis Market Trends

“Advancement in Ophthalmic Drug Delivery Systems and Precision Eye Care”

- A significant and accelerating trend in the global Mydriasis market is the increasing adoption of advanced ophthalmic drug delivery systems and precision-based eye care approaches aimed at improving diagnostic accuracy and patient outcomes in eye examinations and surgical procedures

- For instance, mydriatic agents such as tropicamide, phenylephrine, and cyclopentolate are increasingly being optimized in formulation to achieve faster onset, controlled pupil dilation, and reduced side effects, thereby improving efficiency in ophthalmic diagnostics and retinal examinations

- The growing demand for early detection of eye disorders such as diabetic retinopathy, glaucoma, and age-related macular degeneration is driving the routine use of mydriasis-inducing agents in diagnostic ophthalmology practices

- Furthermore, advancements in digital ophthalmic imaging technologies, including retinal scanning and fundus photography, are increasing the need for consistent and predictable pupil dilation to ensure high-quality imaging results

- The expansion of outpatient eye care services and increasing number of ophthalmic diagnostic centers are further supporting the widespread adoption of mydriatic agents across healthcare facilities globally

- This trend toward improved diagnostic precision, enhanced drug formulations, and expanding ophthalmic infrastructure is reshaping clinical eye care practices. Consequently, companies such as Alcon and Bausch + Lomb are focusing on expanding ophthalmic drug portfolios and improving formulations for diagnostic eye care applications

- The demand for mydriatic agents is increasing steadily due to the rising prevalence of ocular disorders and the growing importance of early and accurate eye disease diagnosis

Mydriasis Market Dynamics

Driver

“Rising Prevalence of Eye Disorders and Increasing Demand for Diagnostic Ophthalmology”

- The increasing prevalence of ocular diseases such as diabetic retinopathy, cataracts, glaucoma, and macular degeneration is a major driver for the growth of the global Mydriasis market

- For instance, the rising global diabetic population is significantly increasing the need for regular retinal screening, which relies heavily on effective pupil dilation using mydriatic agents

- The growing awareness regarding preventive eye care and early diagnosis of vision-related disorders is encouraging patients to undergo routine ophthalmic examinations, thereby increasing the demand for mydriasis-inducing medications

- Furthermore, expanding healthcare infrastructure, improved access to ophthalmology services, and rising investments in eye care programs are supporting higher adoption rates of diagnostic eye procedures globally

- The increasing number of ophthalmic surgeries, including cataract and retinal procedures, also requires consistent pupil dilation for better surgical visibility, further driving market growth. In addition, continuous advancements in ophthalmic pharmaceuticals are enhancing drug safety, efficacy, and duration of action

Restraint/Challenge

“Side Effects of Mydriatic Agents and Limited Patient Tolerance”

- The potential side effects associated with mydriatic drugs remain a significant challenge for the global Mydriasis market

- For instance, commonly used mydriatic agents may cause temporary blurred vision, light sensitivity (photophobia), eye irritation, and difficulty in near vision focusing, which can lead to patient discomfort following eye examinations

- In some cases, systemic absorption of certain mydriatic drugs may also result in adverse effects such as increased heart rate or dry mouth, particularly in sensitive patient populations such as children and the elderly

- In addition, patient reluctance toward temporary vision impairment following dilation procedures can affect compliance with routine ophthalmic check-ups and screenings

- The availability of alternative non-dilating imaging technologies in ophthalmology may also reduce reliance on traditional mydriatic agents in certain diagnostic settings

- Overcoming these challenges through the development of safer formulations, improved drug delivery mechanisms, patient education, and enhanced ophthalmic screening technologies will be essential for sustained growth in the global Mydriasis market

Mydriasis Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Mydriasis market is segmented into emerging drugs, surgery, and others. The surgery segment dominated the largest market revenue share of 56.8% in 2025, driven by the increasing prevalence of severe ocular conditions requiring surgical intervention and advanced ophthalmic procedures. Surgical approaches are widely used in cases where pharmacological management is insufficient, particularly in trauma-induced or disease-associated pupil dilation complications. The segment benefits from advancements in ophthalmic surgical technologies and improved precision-based eye care procedures. Rising investments in ophthalmology infrastructure and growing availability of skilled eye surgeons further support market expansion. Healthcare providers increasingly prefer surgical intervention in complex cases to ensure long-term visual stability and prevent complications. The growing geriatric population and increasing incidence of eye disorders are significantly contributing to segment growth. In addition, favorable reimbursement policies for ophthalmic surgeries are improving patient access to treatment. Hospitals and specialty eye care centers are expanding their surgical capabilities, further strengthening segment dominance. Increasing awareness regarding advanced eye care procedures is also encouraging early diagnosis and treatment adoption. Furthermore, continuous innovation in minimally invasive ophthalmic surgery is expected to sustain segment leadership during the forecast period.

The emerging drugs segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by increasing research and development in ophthalmic pharmacology and demand for non-invasive treatment options. Pharmaceutical companies are actively developing novel drug formulations aimed at controlling abnormal pupil dilation and improving ocular response regulation. Rising prevalence of eye-related disorders and increasing focus on early-stage pharmacological intervention are supporting segment growth. The segment also benefits from advancements in targeted drug delivery systems and sustained-release ophthalmic formulations. Growing investments in clinical trials and biotechnology research are accelerating innovation in ocular therapeutics. Healthcare providers are increasingly adopting drug-based therapies to reduce dependency on surgical procedures. Expanding access to ophthalmic medications in emerging markets is further driving adoption. In addition, increasing awareness regarding vision health and preventive eye care is contributing to market expansion. Favorable regulatory approvals for new ophthalmic drugs are also supporting commercialization. Furthermore, rising demand for personalized eye treatment solutions is expected to accelerate segment growth throughout the forecast period.

- By Diagnosis

On the basis of diagnosis, the Mydriasis market is segmented into blood tests, visual acuity test, ocular motility test, and others. The visual acuity test segment accounted for the largest market revenue share of 41.5% in 2025, driven by its widespread use as a primary diagnostic tool for assessing eye function and detecting abnormal pupil dilation conditions. Visual acuity testing is a fundamental and cost-effective method widely used in hospitals, clinics, and ophthalmology centers. The segment benefits from increasing prevalence of ocular disorders and rising awareness regarding early eye examinations. Healthcare professionals rely heavily on visual acuity tests to evaluate patient vision quality and detect underlying causes of mydriasis. Growing adoption of routine eye screening programs is further supporting segment growth globally. The test is non-invasive, simple to perform, and widely accessible, making it highly preferred in both developed and emerging healthcare systems. Increasing investments in ophthalmic diagnostic infrastructure are improving test availability and accuracy. Rising geriatric population and higher incidence of vision impairment are also contributing to segment expansion. In addition, integration of digital eye testing technologies is enhancing diagnostic precision. Furthermore, increasing public awareness regarding preventive eye health is expected to sustain segment dominance during the forecast period.

The ocular motility test segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by increasing demand for advanced diagnostic techniques for comprehensive eye movement and neurological assessment. This test is increasingly used to identify abnormalities associated with pupil function and related ocular disorders. Healthcare providers are adopting ocular motility testing for early detection of complex neurological and ophthalmic conditions. Rising cases of trauma-related eye disorders and neurological complications are significantly supporting segment growth. The segment also benefits from technological advancements in ophthalmic diagnostic devices and imaging systems. Increasing investments in specialized eye care centers are improving accessibility to advanced testing procedures. Growing awareness regarding early diagnosis and preventive ophthalmic care is further accelerating adoption. In addition, integration of AI-based diagnostic tools is improving accuracy and efficiency of ocular assessments. Expanding healthcare infrastructure in emerging economies is also contributing to market growth. Furthermore, rising demand for comprehensive eye examination procedures is expected to drive strong segment expansion throughout the forecast period.

- By Symptoms

On the basis of symptoms, the Mydriasis market is segmented into blurred vision, red eye, pain around the eye, photophobia, diplopia, headache, transient visual obscurations, and others. The blurred vision segment dominated the largest market revenue share of 38.6% in 2025, driven by its high prevalence among patients experiencing abnormal pupil dilation and underlying ocular disorders. Blurred vision is one of the most commonly reported symptoms, prompting early medical consultation and diagnosis. The segment benefits from increasing awareness regarding eye health and rising incidence of vision-related disorders globally. Healthcare professionals frequently use blurred vision as a key indicator for diagnosing mydriasis and related conditions. The growing aging population is significantly contributing to higher cases of vision impairment. Increasing exposure to digital screens and lifestyle-related eye strain is also accelerating symptom occurrence. Ophthalmology clinics and hospitals are witnessing higher patient inflow due to blurred vision complaints. Rising investments in eye care infrastructure are improving diagnostic capabilities. In addition, growing adoption of preventive eye check-ups is supporting early detection. Furthermore, increasing public health awareness campaigns are expected to sustain segment dominance during the forecast period.

The photophobia segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing sensitivity to light-related eye disorders and rising prevalence of neurological and ophthalmic conditions. Photophobia is commonly associated with abnormal pupil dilation and other underlying ocular diseases. Healthcare providers are increasingly focusing on early detection and management of light sensitivity symptoms. Rising cases of migraines, eye infections, and corneal disorders are significantly contributing to segment growth. The segment also benefits from increasing awareness regarding eye protection and preventive healthcare. Advancements in diagnostic technologies are improving detection accuracy of light sensitivity-related conditions. Growing adoption of digital health monitoring tools is further supporting symptom tracking and diagnosis. Increasing environmental factors such as prolonged screen exposure are also contributing to rising photophobia cases. Expanding ophthalmic healthcare infrastructure is improving patient access to treatment. Furthermore, rising research activities in ocular neuroscience are expected to drive strong segment growth during the forecast period.

- By Dosage

On the basis of dosage, the Mydriasis market is segmented into solutions, tablet, injection, and others. The solutions segment accounted for the largest market revenue share of 52.3% in 2025, driven by the widespread use of ophthalmic solutions for pupil dilation management and diagnostic procedures. Solutions are highly preferred due to their fast action, ease of application, and direct delivery to ocular tissues. Healthcare providers commonly use ophthalmic solutions in clinical settings for routine eye examinations and diagnostic tests. The segment benefits from increasing demand for non-invasive treatment options in ophthalmology. Rising prevalence of eye disorders and growing adoption of preventive eye care practices are significantly contributing to market growth. Pharmaceutical companies continue to develop advanced ophthalmic formulations with improved efficacy and patient comfort. Increasing availability of over-the-counter eye solutions is also supporting segment expansion. Hospitals and clinics are witnessing higher usage of solution-based therapies for diagnostic and therapeutic purposes. In addition, growing awareness regarding eye hygiene and care is further driving demand. Furthermore, expanding ophthalmic drug distribution networks are expected to sustain segment dominance during the forecast period.

The injection segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing use of advanced ophthalmic therapies and emergency treatment requirements. Injectable treatments are being explored for severe ocular conditions requiring rapid pharmacological intervention. The segment benefits from advancements in drug delivery technologies and development of targeted ophthalmic injections. Rising cases of eye trauma and neurological complications are significantly supporting segment growth. Healthcare providers are increasingly adopting injectable therapies for controlled and effective treatment outcomes. Growing investments in ophthalmic research and clinical trials are further accelerating innovation. The segment also benefits from improved hospital infrastructure and availability of specialized eye care services. Increasing adoption of biologic therapies in ophthalmology is contributing to market expansion. In addition, rising demand for precision-based treatment approaches is supporting segment growth. Furthermore, continuous advancements in injectable drug formulations are expected to drive strong segment expansion throughout the forecast period.

- By Route of Administration

On the basis of route of administration, the Mydriasis market is segmented into oral, intravenous, topical, and others. The topical segment dominated the largest market revenue share of 60.7% in 2025, driven by the widespread use of eye drops and topical ophthalmic agents for pupil dilation management. Topical administration is highly preferred due to its direct action, ease of use, and minimal systemic side effects. Healthcare providers frequently use topical formulations for diagnostic and therapeutic ophthalmic procedures. The segment benefits from increasing prevalence of eye disorders and rising demand for non-invasive treatments. Growing awareness regarding eye health and preventive care is significantly supporting market growth. Pharmaceutical companies are continuously developing improved topical formulations with enhanced absorption and effectiveness. Increasing availability of ophthalmic eye drops in retail and hospital pharmacies is further driving segment expansion. The segment also benefits from rising adoption of routine eye examinations globally. In addition, growing geriatric population and increasing vision-related disorders are contributing to demand. Furthermore, advancements in ophthalmic drug delivery technologies are expected to sustain segment dominance during the forecast period.

The intravenous segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing use in emergency ophthalmic care and complex medical conditions requiring rapid drug delivery. Intravenous administration is gaining importance in hospital settings for severe ocular and neurological complications associated with mydriasis. The segment benefits from advancements in critical care ophthalmology and improved hospital infrastructure. Rising cases of trauma-related eye conditions are significantly contributing to segment growth. Healthcare providers are increasingly adopting intravenous therapies for faster and more controlled treatment outcomes. Growing investments in emergency care units and specialized ophthalmic departments are supporting market expansion. In addition, increasing clinical research on intravenous ophthalmic drug applications is driving innovation. Expanding access to advanced healthcare facilities in emerging markets is further contributing to growth. Furthermore, rising demand for precision-based emergency treatments is expected to accelerate segment development throughout the forecast period.

- By End-Users

On the basis of end-users, the Mydriasis market is segmented into clinic, hospital, and others. The hospital segment dominated the largest market revenue share of 55.2% in 2025, driven by the high volume of diagnostic and therapeutic ophthalmic procedures performed in hospital settings. Hospitals serve as primary care centers for complex eye conditions requiring specialized diagnosis and treatment. The segment benefits from the availability of advanced ophthalmic equipment and skilled healthcare professionals. Increasing hospital admissions for eye disorders and trauma-related cases are significantly supporting market growth. Hospitals also provide integrated care services, including diagnosis, treatment, and post-operative management. Rising investments in ophthalmology departments and infrastructure are strengthening hospital-based care delivery. The segment is further supported by favorable reimbursement policies and insurance coverage for eye treatments. Growing awareness regarding early diagnosis and vision care is driving higher hospital visits. Pharmaceutical and medical device companies frequently collaborate with hospitals for clinical research and product development. Furthermore, increasing prevalence of eye diseases and aging population are expected to sustain hospital segment dominance during the forecast period.

The clinic segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by increasing preference for outpatient eye care services and growing accessibility to ophthalmology clinics. Clinics provide cost-effective and convenient diagnostic and treatment options for patients with mild to moderate eye conditions. The segment benefits from rising awareness regarding preventive eye care and regular vision screening. Increasing number of private eye care clinics and specialty ophthalmology centers is supporting market growth. Clinics are increasingly adopting advanced diagnostic technologies for early disease detection. Growing demand for personalized and accessible eye care services is also contributing to segment expansion. In addition, expanding tele-ophthalmology services are improving patient reach in remote areas. Rising healthcare expenditure and increasing ophthalmologist availability are further supporting growth. Furthermore, government initiatives promoting eye health awareness are expected to drive strong clinic segment expansion during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Mydriasis market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment accounted for the largest market revenue share of 49.8% in 2025, driven by the high volume of prescription dispensing within hospital-based ophthalmic care settings. Hospital pharmacies play a crucial role in providing specialized eye medications for diagnostic and therapeutic procedures. The segment benefits from strong integration with hospital ophthalmology departments and surgical units. Increasing hospital admissions for eye disorders are significantly contributing to market growth. Hospital pharmacies ensure accurate dispensing and monitoring of ophthalmic drugs, improving treatment safety. Rising investments in healthcare infrastructure and ophthalmology services are supporting segment expansion. The segment is also driven by favorable reimbursement systems and centralized procurement processes. Pharmaceutical companies collaborate closely with hospital pharmacies for drug supply and clinical research activities. Growing prevalence of eye diseases and increasing surgical procedures further support demand. Furthermore, expanding hospital networks and rising healthcare expenditure are expected to sustain segment dominance during the forecast period.

The online pharmacy segment is expected to witness the fastest CAGR of 11.1% from 2026 to 2033, driven by rapid digitalization of healthcare services and increasing demand for convenient medication access. Online pharmacies offer easy access to ophthalmic medications, diagnostic eye drops, and prescription therapies through home delivery services. The segment benefits from increasing internet penetration and smartphone adoption globally. Patients prefer online platforms due to convenience, affordability, and discreet purchasing options. The COVID-19 pandemic significantly accelerated adoption of e-pharmacy services, creating long-term growth opportunities. Pharmaceutical companies are expanding partnerships with online platforms to improve distribution networks. Regulatory support for e-prescriptions is further enhancing market expansion. Online pharmacies also provide medication reminders and digital healthcare support services. Rising demand for contactless healthcare solutions is driving segment growth. Furthermore, increasing investments in digital health infrastructure are expected to accelerate strong expansion during the forecast period.

Mydriasis Market Regional Analysis

- North America dominated the Mydriasis market with the largest revenue share of 36.9% in 2025, supported by strong ophthalmic infrastructure, high screening rates, and early adoption of advanced diagnostic eye care technologies. The region benefits from well-established eye care systems, increasing prevalence of vision disorders, and widespread availability of routine ophthalmic examinations across hospitals and specialty clinics

- The rising demand for diagnostic eye care procedures, growing geriatric population, and increasing incidence of conditions requiring pupil dilation for accurate retinal and ocular assessments are key factors driving the use of mydriatic agents in the region. In addition, strong clinical adoption and integration of advanced ophthalmic imaging technologies continue to support market growth

- Furthermore, favorable reimbursement systems, high awareness regarding preventive eye care, and continuous advancements in ophthalmology diagnostics are reinforcing North America’s leadership in the global Mydriasis market

U.S. Mydriasis Market Insight

The U.S. Mydriasis market captured the largest revenue share of 81% within North America in 2025, driven by high procedural volumes in ophthalmology clinics and hospitals, along with increasing demand for routine eye examinations and retinal screening procedures. The growing prevalence of diabetic retinopathy, glaucoma, and age-related macular degeneration is significantly contributing to increased use of mydriatic agents. In addition, the presence of advanced healthcare infrastructure, strong adoption of ophthalmic diagnostic technologies, and rising awareness regarding early detection of eye diseases continue to propel the Mydriasis market in the U.S.

Europe Mydriasis Market Insight

The Europe Mydriasis market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing healthcare expenditure, rising prevalence of vision-related disorders, and strong focus on preventive ophthalmic care. The region’s well-developed healthcare systems and government-supported eye screening programs are encouraging wider adoption of diagnostic eye examinations requiring mydriasis. Moreover, increasing elderly population and rising demand for early detection of ocular diseases are contributing significantly to market growth across Europe.

U.K. Mydriasis Market Insight

The U.K. Mydriasis market is anticipated to grow at a noteworthy CAGR during the forecast period due to increasing awareness regarding eye health and rising demand for routine ophthalmic screenings. Expanding access to NHS-funded eye care services and growing focus on early diagnosis of retinal diseases are supporting market growth. In addition, increasing prevalence of diabetes-related eye complications and aging population are further driving demand for mydriatic agents in clinical ophthalmology settings.

Germany Mydriasis Market Insight

The Germany Mydriasis market is expected to expand at a considerable CAGR during the forecast period, fueled by strong ophthalmic healthcare infrastructure, high adoption of advanced diagnostic technologies, and increasing prevalence of chronic eye diseases. Germany’s emphasis on precision diagnostics and preventive healthcare is supporting the routine use of mydriatic agents in eye examinations. In addition, rising investments in ophthalmology research and increasing patient awareness regarding vision health are contributing to market growth.

Asia-Pacific Mydriasis Market Insight

The Asia-Pacific Mydriasis market is expected to witness the fastest CAGR during the forecast period due to rising healthcare expenditure, increasing incidence of vision disorders, improving access to ophthalmic services, and growing awareness regarding early diagnosis of eye diseases across countries such as China and India. Rapid improvements in healthcare infrastructure, expanding ophthalmology clinics, and increasing government initiatives for blindness prevention are driving market growth in the region. Furthermore, growing adoption of affordable eye care diagnostics and rising patient volumes are significantly accelerating demand across Asia-Pacific.

Japan Mydriasis Market Insight

The Japan Mydriasis market is gaining momentum due to the country’s aging population, high prevalence of age-related eye disorders, and advanced ophthalmic healthcare system. Increasing demand for routine eye screening and early diagnosis of retinal conditions is driving the use of mydriatic agents in clinical practice. In addition, Japan’s strong focus on preventive healthcare, advanced diagnostic technologies, and well-established ophthalmology services are contributing to steady market growth.

China Mydriasis Market Insight

The China Mydriasis market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid healthcare infrastructure development, increasing prevalence of vision disorders, and growing awareness regarding early eye disease diagnosis. Expanding access to ophthalmic care services, rising patient volumes in hospitals and eye clinics, and government initiatives for vision health screening are key factors driving market growth. In addition, increasing investments in healthcare modernization and expanding ophthalmology service networks are significantly contributing to the growth of the Mydriasis market in China.

Mydriasis Market Share

The Mydriasis industry is primarily led by well-established companies, including:

• Bausch + Lomb (U.S.)

• Alcon Inc. (Switzerland)

• Johnson & Johnson Vision (U.S.)

• Novartis AG (Switzerland)

• Santen Pharmaceutical Co., Ltd. (Japan)

• AbbVie Inc. (U.S.)

• Allergan (an AbbVie company) (U.S.)

• Sun Pharmaceutical Industries Ltd. (India)

• Cipla Limited (India)

• Dr. Reddy’s Laboratories Ltd. (India)

• Alcon Laboratories (division of Alcon Inc.) (Switzerland)

• Bayer AG (Germany)

• Pfizer Inc. (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Hikma Pharmaceuticals PLC (U.K.)

• Apotex Inc. (Canada)

• Aurobindo Pharma Limited (India)

• Zydus Lifesciences Limited (India)

• Bharat Serums and Vaccines Ltd. (India)

• Akorn Operating Company LLC (U.S.)

Latest Developments in Global Mydriasis Market

- In March 2021, Ocuphire Pharma announced positive Phase 3 MIRA-2 trial results for Nyxol (phentolamine ophthalmic solution), designed to reverse pharmacologically induced mydriasis caused by routine eye-dilation drugs like tropicamide and phenylephrine. This marked a major step toward the first dedicated reversal therapy for mydriasis, improving patient recovery time after eye exams

- In November 2021, Ocuphire Pharma completed enrollment for the Phase 3 MIRA-3 clinical trial evaluating Nyxol for reversal of pharmacologic mydriasis, strengthening the late-stage pipeline for post-dilation recovery treatments used in ophthalmology clinics worldwide

- In May 2023, the U.S. FDA approved Mydcombi (tropicamide 1% + phenylephrine 2.5% ophthalmic spray) developed by Eyenovia for inducing mydriasis for diagnostic eye examinations. This was the first fixed-dose combination spray for pupil dilation, improving dosing accuracy and reducing variability compared to conventional eye drops

- In May 2023, the FDA approval of Mydcombi also marked the introduction of the Optejet microdose delivery system, a novel drug-device platform designed to improve safety, reduce ocular surface exposure, and enhance efficiency in routine ophthalmic dilation procedures

- In January 2025, clinical research published in ophthalmology journals highlighted ongoing evaluation of tropicamide-based cycloplegic agents in pediatric and diagnostic applications, showing measurable effects on ocular biometrics such as choroidal thickness and axial length, reinforcing the role of mydriatic drugs in advanced diagnostic imaging workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.