Global Myelodysplasia Treatment Market

Market Size in USD Billion

USD

3.60 Billion

USD

5.48 Billion

2025

2033

USD

3.60 Billion

USD

5.48 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.60 Billion | |

| USD 5.48 Billion | |

| % | |

|

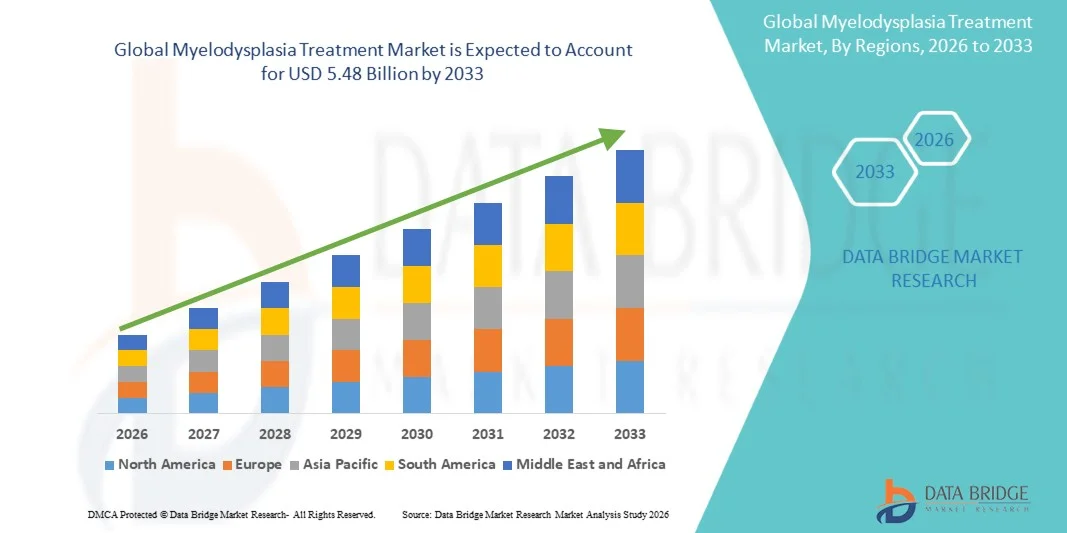

Myelodysplasia Treatment Market Size

- The global myelodysplasia treatment market size was valued at USD 3.60 billion in 2025 and is expected to reach USD 5.48 billion by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by rising prevalence of myelodysplastic syndromes (MDS) worldwide, increasing geriatric population, and continuous advancements in hematology diagnostics and therapeutics, which are enabling earlier detection and more personalized treatment approaches. Improved access to bone marrow biopsies, genetic testing, and advanced prognostic scoring systems is significantly enhancing diagnosis accuracy, thereby accelerating treatment adoption across hospitals and specialty clinics

- Furthermore, growing patient demand for effective, targeted, and less-toxic treatment options is establishing novel therapies—such as hypomethylating agents, immunotherapies, and stem cell transplantation—as the preferred solutions in modern MDS management. These converging factors are driving the uptake of Myelodysplasia Treatment solutions, thereby significantly boosting the industry's growth across both developed and emerging healthcare markets

Myelodysplasia Treatment Market Analysis

- The Myelodysplasia Treatment market is experiencing steady growth driven by increasing global prevalence of myelodysplastic syndromes (MDS), rising adoption of advanced diagnostic technologies, and expanding availability of targeted therapies that improve patient survival and quality of life

- Market expansion is additionally supported by ongoing clinical trials evaluating next-generation hypomethylating agents, combination therapies, and gene-targeted treatments, along with increasing awareness and early detection initiatives across major healthcare markets

- North America dominated the myelodysplasia treatment market with the largest revenue share of approximately 40.60% in 2025, supported by strong healthcare infrastructure, high diagnostic rates, widespread availability of advanced therapeutics, and substantial R&D investment from leading pharmaceutical companies in the U.S.

- Asia-Pacific is projected to be the fastest-growing regional market from 2025–2030, driven by increasing healthcare expenditure, rising incidence of hematological disorders, improving access to oncology care, and expanding government efforts to support early cancer diagnosis and treatment

- Bone marrow biopsy dominated with 50.2% share in 2025, remaining the gold standard for MDS diagnosis. It enables accurate disease classification, cytogenetic analysis, and risk stratification, guiding treatment decisions

Report Scope and Myelodysplasia Treatment Market Segmentation

|

Attributes |

Myelodysplasia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Myelodysplasia Treatment Market Trends

“Advancements in Targeted Therapies and Diagnostic Precision”

- A significant and accelerating trend in the global myelodysplasia treatment market is the rapid advancement of targeted therapies and precision-based diagnostic tools that are transforming patient management and clinical outcomes

- For instance, novel agents such as hypomethylating drugs, targeted inhibitors, and next-generation biologics are being increasingly integrated into treatment plans, offering more personalized and effective options for patients across different risk categories. These advancements are enabling clinicians to tailor therapy based on genetic mutations, cytogenetic abnormalities, and disease progression patterns

- Improvements in diagnostic accuracy through advanced molecular testing and cytogenetic profiling are also enhancing early detection and risk stratification. Technologies such as next-generation sequencing (NGS) and high-resolution chromosomal analysis allow clinicians to identify specific mutations that drive disease progression, enabling more refined therapeutic decisions

- The integration of predictive biomarkers further supports individualized treatment strategies, helping physicians anticipate treatment response, therapy-related toxicity, and disease transformation. This shift toward precision medicine is continuously improving patient outcomes by aligning treatment intensity with disease severity

- Pharmaceutical companies and research institutes are accelerating the development of innovative therapeutic approaches, including combination regimens and agents designed to target the underlying molecular mechanisms of Myelodysplasia. These efforts are expanding the therapeutic landscape and offering new opportunities for long-term disease management

- As awareness of precision medicine grows among healthcare providers and patients, the demand for advanced diagnostic testing and targeted therapeutic options is increasing, shaping the broader evolution of the Myelodysplasia Treatment market

Myelodysplasia Treatment Market Dynamics

Driver

“Increasing Prevalence and Rising Adoption of Advanced Therapeutics”

- The growing global burden of myelodysplastic syndromes (MDS), especially in aging populations, is a major driver of the Myelodysplasia Treatment market. The rising number of diagnosed cases has increased the need for timely and effective treatment options, driving demand for advanced therapeutic solutions

- For instance, recent clinical advancements and approvals of novel hypomethylating agents, immunotherapies, and mutation-specific treatments are enabling more effective disease management and improving survival outcomes for many patients. These innovations are expected to significantly boost the Myelodysplasia Treatment industry during the forecast period

- As healthcare providers become more aware of the critical importance of early intervention, the adoption of standardized treatment protocols is rising across hospitals, specialty centers, and clinics. This shift is supported by improvements in diagnostic capabilities and better disease-risk stratification models

- Growing availability of supportive care therapies such as erythropoiesis-stimulating agents, iron chelation therapy, and blood transfusion management further enhances overall patient outcomes and expands treatment opportunities

- Increased research funding, clinical trial activity, and collaborations between pharmaceutical manufacturers and academic institutions are accelerating drug development efforts and improving access to newly approved therapies

- The trend toward personalized medicine, adoption of modern diagnostic tools, and availability of expanded treatment guidelines are key factors driving strong market growth across high-, intermediate-, and lower-risk patient populations

Restraint/Challenge

“High Treatment Costs and Limited Access to Advanced Diagnostic Infrastructure”

- High treatment costs associated with advanced therapeutics, continuous blood transfusions, genetic testing, and long-term disease management present significant barriers to widespread market adoption. Many novel agents and combination regimens come with substantial expense, limiting accessibility for patients in low- and middle-income regions

- For instance, advanced molecular and cytogenetic tests essential for accurate diagnosis and risk stratification are often unavailable or unaffordable in underserved areas, reducing opportunities for early detection and personalized therapy

- The financial burden of repeated diagnostic evaluations, chronic supportive care, and ongoing therapy cycles can create significant economic strain for patients and healthcare systems, especially when insurance coverage is limited or reimbursement policies are inconsistent

- Concerns about treatment-related toxicities, long-term side effects, and the need for frequent monitoring also contribute to hesitation among certain patient groups and healthcare providers

- Infrastructure limitations, including shortages of trained hematologists, inadequate diagnostic laboratories, and lack of access to advanced therapeutic agents, further restrict market penetration in developing regions

- Overcoming these challenges will require improved reimbursement frameworks, increased government investment in diagnostic and treatment infrastructure, expansion of patient-assistance programs, and broader availability of affordable Myelodysplasia Treatment options to ensure equitable access to high-quality care

Myelodysplasia Treatment Market Scope

The Myelodysplasia Treatment market is segmented on the basis of drug type, treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Drug Type

On the basis of drug type, the market is segmented into Lenalidomide, Azacitidine, Decitabine, Deferasirox, Phase-3 drugs, and others. Lenalidomide dominated the largest market revenue share of 38.7% in 2025, driven by its proven efficacy in low-risk MDS patients, particularly those with deletion 5q. The drug’s favorable safety profile, coupled with strong clinical adoption across hospitals and specialty clinics worldwide, has reinforced its leading position. Oral administration provides convenience for patients, increasing adherence and reducing the need for frequent hospital visits. Physicians favor Lenalidomide for its ability to reduce transfusion dependence and improve quality of life. Inclusion in global treatment guidelines further strengthens its market dominance. It has a predictable side effect profile and consistent outcomes, making it the preferred first-line therapy. The drug is widely accessible due to insurance coverage in developed regions, which supports steady revenue growth. Healthcare providers rely on its efficacy to manage anemia and other MDS symptoms. Pharmaceutical companies continue investing in clinical trials and educational programs to maintain its prominence. The ongoing research on combination therapies and expanded indications reinforces continued market demand.

Azacitidine is anticipated to witness the fastest growth rate of CAGR 9.2% from 2026 to 2033, fueled by rising adoption in higher-risk MDS patients and approval of oral and subcutaneous formulations. Clinical evidence shows improved survival and delayed progression to acute myeloid leukemia, increasing physician preference. Hospitals and clinics in emerging markets are gradually adopting Azacitidine as a standard therapy. Patient awareness campaigns and educational programs further accelerate uptake. The outpatient administration model makes it convenient and cost-effective. Expanding insurance coverage improves access, encouraging wider use. Pharmaceutical companies are actively promoting awareness among hematologists. Combination therapies and supportive care options increase clinical application. The drug’s tolerability profile supports long-term administration. Rising incidence of MDS globally supports market expansion. Physicians increasingly use it for patients unsuitable for transplantation. Overall, Azacitidine is set to capture significant incremental growth.

- By Treatment

On the basis of treatment, the market is segmented into medication, chemotherapy, blood transfusion, supportive therapy, stem cell transplant, and others. Medication dominated the largest market revenue share of 41.5% in 2025, due to widespread use of oral therapies targeting MDS pathways. High patient adherence and convenience contribute to consistent demand. Medications reduce transfusion dependence, improving patient quality of life. Clinical guidelines strongly recommend oral therapies, supporting physician confidence. Hospitals and specialty clinics prioritize these drugs in treatment protocols. Medications offer cost-effective outpatient management compared to intensive procedures. Pharmaceutical companies actively develop new oral formulations to maintain market share. Patient awareness campaigns reinforce usage and acceptance. The strong efficacy and tolerable side effect profile make them the preferred first-line therapy. Inclusion in national treatment programs ensures stable revenue streams. Oral medications reduce hospitalization frequency, increasing healthcare system efficiency. Doctors rely on these drugs to manage both low-risk and intermediate-risk MDS.

Stem cell transplant is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by advancements in transplantation techniques, improved donor matching, and better post-transplant survival rates. Curative potential attracts adoption, especially among younger high-risk patients. Awareness campaigns and clinical education increase acceptance. Hospitals in developed countries are expanding transplant programs. Reduced mortality and morbidity rates encourage physician confidence. Growing patient willingness to pursue curative options supports growth. Investment in supportive care improves outcomes. Advances in immunosuppressive therapy reduce complications. Transplantation remains a standard recommendation for eligible patients. Insurance coverage expansion facilitates affordability. Research on risk-adapted protocols increases adoption. Overall, stem cell transplant is the fastest-growing therapeutic segment.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, bone marrow biopsy, and others Bone marrow biopsy dominated with 50.2% share in 2025, remaining the gold standard for MDS diagnosis. It enables accurate disease classification, cytogenetic analysis, and risk stratification, guiding treatment decisions. Hospitals and specialty clinics rely heavily on biopsy results to determine appropriate therapy. The procedure’s ability to provide detailed marrow morphology makes it indispensable. Physicians prioritize biopsies for their diagnostic precision. Bone marrow biopsy also helps monitor disease progression and treatment response. Its adoption is supported by established protocols in developed and emerging markets. Accurate results influence medication choice and transplantation planning. Patient management plans heavily depend on biopsy outcomes. Technological improvements in biopsy tools enhance accuracy. Clinics invest in training for proper biopsy technique. The test is critical for clinical trials and research studies.

Blood tests are expected to witness the fastest CAGR of 7.5% from 2026 to 2033, due to their non-invasive nature and routine use in initial screening and ongoing monitoring. Automated hematology analyzers improve detection accuracy. Blood tests allow for early identification of cytopenias and disease progression. Outpatient clinics increasingly adopt tests for convenience. They are cost-effective compared to invasive procedures. Patient compliance is higher due to simplicity and reduced discomfort. Blood tests support telemedicine and remote monitoring programs. Adoption is rising in emerging markets with limited hospital access. Blood count trends guide therapy adjustments and transfusion needs. They complement biopsy results for comprehensive disease management. Continuous innovations improve sensitivity and specificity. Overall, blood tests are the fastest-growing diagnostic tool in MDS care.

- By Symptoms

On the basis of symptoms, the market is segmented into fatigue, frequent infection, shortness of breath, bleeding, unusual paleness, and others. Fatigue dominated the largest market revenue share of 42.8% in 2025, as it is the most commonly reported symptom among MDS patients. Its high prevalence drives demand for supportive care therapies and monitoring. Physicians prioritize fatigue management to improve patient quality of life. Hospitals integrate fatigue assessment into standard clinical protocols. Pharmaceutical interventions and supportive therapies, such as erythropoiesis-stimulating agents, are widely prescribed. Fatigue influences medication dosage and transfusion schedules. Awareness programs emphasize the need for symptom tracking. Patient-reported outcomes guide therapy adjustments. The high impact on daily activities reinforces the focus on this symptom. Clinics use fatigue scoring to monitor treatment response. Fatigue management protocols are supported by global guidelines. Long-term monitoring helps reduce hospitalization due to complications.

Frequent infection is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by rising neutropenia cases in MDS patients and the increasing use of prophylactic antibiotics and immunomodulatory therapies. Hospitals monitor infection rates closely to reduce morbidity. Frequent infection influences treatment choice, especially in high-risk patients. Outpatient management programs aim to prevent hospitalization. Awareness campaigns emphasize early detection and intervention. Pharmaceutical companies develop supportive care solutions targeting infection control. Clinical guidelines recommend routine monitoring of neutrophil counts. Emerging markets are increasing adoption of preventive measures. Infection management improves survival rates and patient outcomes. Growing awareness among physicians accelerates adoption of prophylactic strategies. Advanced diagnostics allow early detection of infection trends. Frequent infection remains a key driver for supportive therapy growth.

- By Dosage

On the basis of dosage, the market is segmented into tablet, capsule, injection, and others. Tablet dominated the largest market revenue share of 46.3% in 2025, primarily due to its convenience, patient adherence, and widespread use of oral medications such as Lenalidomide and Azacitidine. Tablets allow home-based therapy, reducing hospital visits. Physicians favor tablets for low-risk patients and maintenance therapy. Hospitals and clinics stock tablets widely due to high demand. Tablets support precise dosage titration based on patient response. Pharmaceutical companies develop extended-release formulations to enhance adherence. Patients prefer tablets over injections due to comfort and ease of administration. Global distribution networks ensure widespread availability. Tablets reduce the burden on healthcare facilities. Clinical guidelines recommend tablets for long-term management. Patient education emphasizes adherence to maximize therapeutic outcomes. Tablet therapy dominates both developed and emerging markets.

Injection is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by the increased use of injectable Azacitidine and supportive therapies. Injectable dosage ensures precise delivery and rapid onset, especially for high-risk patients. Hospitals and clinics increasingly adopt injection protocols for intensive therapy. Injectable formulations improve treatment outcomes in combination therapies. Pharmaceutical advancements reduce side effects and improve tolerability. Emerging markets see growing adoption due to expanding hospital infrastructure. Physicians prefer injection for patients with poor oral absorption or compliance issues. Training programs enhance safe administration. Injection therapy supports chemotherapy and stem cell transplantation protocols. Insurance coverage expansion facilitates adoption. Frequent injections support close monitoring of patient response. Injectable therapies are projected to capture high incremental growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, injectable, and others. Oral dominated the largest market revenue share of 44.7% in 2025, driven by the widespread use of orally administered drugs like Lenalidomide and Deferasirox. Oral administration improves patient compliance and reduces hospital dependency. Physicians prefer oral routes for long-term management of low-risk MDS. Outpatient clinics favor oral therapy due to ease of monitoring. Pharmaceutical companies invest in oral formulation innovations to extend patent life. Oral administration supports combination therapy and maintenance protocols. Patients benefit from home-based therapy reducing travel and costs. Oral drugs align with global treatment guidelines for standard care. Hospitals prioritize oral therapies for stable patients. Patient education ensures proper adherence. Oral therapy dominates both developed and emerging markets. Accessibility through retail and hospital pharmacies supports adoption.

Injectable is expected to witness the fastest CAGR of 8.2% from 2026 to 2033, fueled by increasing use of Azacitidine, supportive care injections, and chemotherapy protocols. Injectable routes provide precise dosing and rapid effect in high-risk patients. Hospitals expand outpatient infusion programs to meet growing demand. Physicians rely on injectables for intensive therapy and disease control. Clinical guidelines support injectable therapy for higher-risk MDS patients. Advanced formulations improve safety and tolerability. Adoption rises in emerging markets with improved healthcare infrastructure. Injectable therapies support combination protocols for better outcomes. Regular injections allow close monitoring of patient response. Patient awareness of efficacy boosts adoption. Hospital training programs ensure safe administration. Overall, injectables show robust market growth.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. Hospitals dominated the largest market revenue share of 51.6% in 2025, serving as the primary centers for diagnosis, treatment, and management of MDS patients. Hospitals provide comprehensive care including chemotherapy, blood transfusions, and stem cell transplantation. Physicians rely on hospitals for access to advanced diagnostics and therapies. Hospitals have trained staff and infrastructure for complex treatment protocols. Adoption is supported by clinical guidelines and national healthcare programs. Hospitals ensure proper monitoring and follow-up, improving patient outcomes. Availability of multiple therapies under one roof supports patient convenience. Hospitals are key for participation in clinical trials and research studies. Advanced hospitals invest in modern equipment to enhance diagnostic accuracy. They serve as centers for physician education and training. Hospitals dominate the market due to high patient volumes and treatment capabilities.

Clinics are expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing outpatient management, home-based care programs, and the rise of specialized hematology clinics. Clinics offer convenience for routine monitoring and oral therapy administration. Patient preference for shorter waiting times and proximity supports clinic adoption. Telemedicine integration in clinics enhances follow-up care. Clinics reduce hospital burden while maintaining quality treatment. Adoption is rising in urban and semi-urban areas. Physicians use clinics for low-risk patient management and supportive care. Clinics provide cost-effective solutions for long-term monitoring. Expansion of hematology networks drives growth. Patient awareness programs increase acceptance. Clinics increasingly collaborate with hospitals for comprehensive care. Overall, clinics show strong growth potential.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. Hospital pharmacy dominated the largest market revenue share of 48.9% in 2025, due to direct access to patients receiving therapy within hospitals. Hospital pharmacies ensure correct dispensing of oral and injectable drugs under medical supervision. Physicians prescribe medications administered or picked up from hospital pharmacies. Integrated inventory management supports consistent drug availability. Hospital pharmacies facilitate treatment adherence and monitoring. Specialty drugs like Lenalidomide and Azacitidine are primarily accessed here. Hospitals coordinate with insurance providers for cost coverage. Clinical trials and research studies use hospital pharmacies for controlled distribution. Access to supportive care drugs is streamlined through hospital pharmacies. Patient counseling is offered at the point of dispensing. Hospital pharmacy remains the most trusted channel for advanced therapies. Hospitals invest in pharmacy infrastructure to meet increasing demand.

Online pharmacy is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by the convenience of home delivery, rising e-commerce penetration, and patient preference for remote access. Online pharmacies offer subscription-based services for chronic therapy. Patients benefit from doorstep delivery and timely refills. Online channels reduce hospital visits for stable patients. Teleconsultation integration promotes remote prescription verification. Online pharmacy adoption is increasing in urban and semi-urban regions. Regulatory improvements ensure safety and authenticity of drugs. Cost-effectiveness attracts patients seeking affordable options. Patient adherence improves through reminders and digital tracking. Awareness campaigns and partnerships with hospitals increase trust. Overall, online pharmacies are set to grow rapidly.

Myelodysplasia Treatment Market Regional Analysis

- North America dominated the myelodysplasia treatment market with the largest revenue share of approximately 40.60% in 2025, supported by strong healthcare infrastructure, high diagnostic rates, widespread availability of advanced therapeutics, and substantial R&D investment from leading pharmaceutical companies in the U.S.

- The region’s growth is further driven by the increasing adoption of novel therapies, growing awareness of hematological malignancies, and rapid expansion of genomic testing, which supports early detection and personalized treatment approaches

- In addition, favorable reimbursement frameworks, high treatment affordability, and strong clinical trial activity have positioned North America as a leading market for MDS treatment advancements

U.S. Myelodysplasia Treatment Market Insight

The U.S. myelodysplasia treatment market accounted for the North American market share in 2025, driven by high prevalence of myelodysplastic syndromes, early adoption of innovative drugs such as hypomethylating agents and immunomodulators, and strong availability of specialized cancer centers. Increasing demand for genomic profiling, next-generation sequencing (NGS), and personalized treatment regimens is further accelerating market growth. Substantial investments by U.S.-based biotech companies and expanding clinical trials for new MDS therapies also significantly contribute to the country’s dominance.

Europe Myelodysplasia Treatment Market Insight

The Europe myelodysplasia treatment market is projected to grow at a strong CAGR during the forecast period, supported by well-established healthcare systems, increasing diagnosis of hematologic disorders, and rising use of advanced therapies. The region benefits from stringent clinical guidelines, early cancer screening programs, and government-funded research initiatives. Growth is evident across major countries, with increasing adoption of outpatient chemotherapy, targeted therapies, and supportive care treatments.

U.K. Myelodysplasia Treatment Market Insight

The U.K. myelodysplasia treatment market is expected to grow at a notable CAGR, driven by rising cancer awareness, increasing preference for early hematological testing, and the expansion of specialized oncology centers. Government initiatives aimed at improving rare disease diagnosis and broadening access to innovative treatments are also playing a vital role. The growing aging population—more susceptible to MDS—is further supporting market expansion.

Germany Myelodysplasia Treatment Market Insight

Germany myelodysplasia treatment market is expected to record significant growth due to its strong oncology research ecosystem, high rate of hospital-based treatment, and substantial use of advanced diagnostic tools. The country’s emphasis on developing and adopting innovative, efficient, and cost-effective cancer treatments continues to support MDS market growth. Availability of reimbursement for most hematologic cancer treatments also enhances access to therapy.

Asia-Pacific Myelodysplasia Treatment Market Insight

The Asia-Pacific myelodysplasia treatment market region is expected to grow at the fastest from 2026 to 2033, fueled by rising healthcare expenditure, increasing patient population, growing awareness of hematological disorders, and improving access to oncology services. Government-led digital health initiatives and expanding diagnostic capabilities are enhancing early detection. Countries like China, India, and Japan are rapidly advancing in cancer treatment infrastructure, contributing substantially to regional market growth.

Japan Myelodysplasia Treatment Market Insight

Japan myelodysplasia treatment market is witnessing steady growth due to its aging population—one of the world’s highest—which significantly increases the incidence of MDS. The country’s strong focus on precision medicine, widespread adoption of advanced diagnostics, and high investment in oncology R&D are major contributors. Increasing integration of molecular testing and availability of cutting-edge therapies continue to boost market expansion.

China Myelodysplasia Treatment Market Insight

China myelodysplasia treatment market captured the largest share of the Asia-Pacific market in 2025, driven by a large patient population, rapid urbanization, and strong government support for cancer diagnosis and treatment improvement. Expansion of cancer hospitals, greater access to innovative drugs, and rising adoption of genetic testing are contributing to fast market growth. Partnerships between global pharmaceutical companies and domestic firms are further accelerating therapy availability and affordability.

Myelodysplasia Treatment Market Share

The Myelodysplasia Treatment industry is primarily led by well-established companies, including:

- Bristol Myers Squibb (U.S.)

- Novartis AG (Switzerland)

- Takeda Pharmaceutical Company (Japan)

- Amgen Inc. (U.S.)

- Otsuka Holdings Co., Ltd. (Japan)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Jazz Pharmaceuticals (Ireland)

- Astellas Pharma (Japan)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories (India)

- Cipla Ltd. (India)

- Sanofi S.A. (France)

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Eli Lilly and Company (U.S.)

- GlaxoSmithKline (U.K.)

Latest Developments in Global Myelodysplasia Treatment Market

- In August 2023, Reblozyl (luspatercept‑aamt) was approved by the U.S. Food and Drug Administration (FDA) as first‑line treatment for anemia in adult patients with lower‑risk MDS who may require red blood cell transfusions — including those who had never received an erythropoiesis‑stimulating agent (ESA). This expanded indication means more MDS patients can receive a therapy that nearly doubled rates of transfusion independence and hemoglobin increase versus prior standard (epoetin alfa)

- In October 2023, the FDA approved Tibsovo (ivosidenib) for adult patients with relapsed or refractory MDS having an IDH1 mutation, marking the first targeted therapy approved specifically for that genetic subtype of MDS. A companion diagnostic assay (RealTime IDH1 Assay) was also approved to identify eligible patients

- In January 2024, it was reported that the first patient was dosed in a Phase II trial of Bexmarilimab (BEXMAB), in combination with standard-of-care, for hypomethylating‑agent–refractory or relapsed MDS. This represents ongoing clinical development aiming to address unmet needs in patients not responding to existing therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.