Global Natural Oil Polyols Market

Market Size in USD Billion

USD

7.48 Billion

USD

12.19 Billion

2025

2033

USD

7.48 Billion

USD

12.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.48 Billion | |

| USD 12.19 Billion | |

| % | |

|

Natural Oil Polyols Market Overview

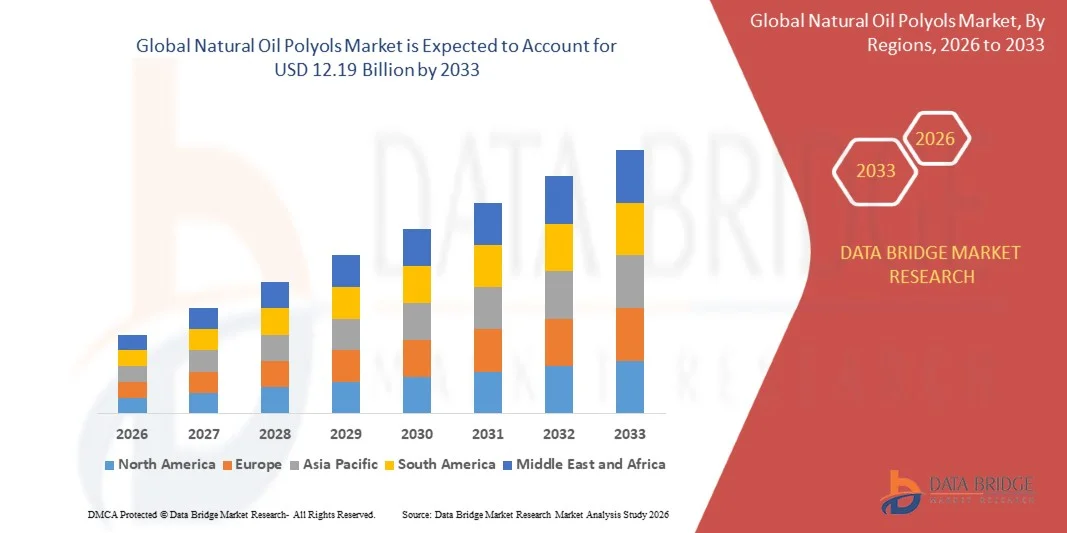

The global natural oil polyols market was valued at USD 7.48 billion in 2025 and is projected to reach USD 12.19 billion by 2033, growing at a CAGR of 6.30% from 2026 to 2033. The market is experiencing steady growth driven by rising demand for bio-based and sustainable polyurethane raw materials, increasing regulatory pressure to reduce petrochemical dependency, and expanding applications across foams, coatings, adhesives, and elastomers.

The growing shift toward green chemistry and circular economy practices is accelerating the adoption of natural oil-based polyols derived from sources such as soybean, palm, and castor oil, offering lower carbon footprint alternatives to conventional petroleum-based polyols. Industries such as automotive, construction, and furniture manufacturing are increasingly integrating these materials to enhance sustainability credentials and meet evolving environmental standards.

Key Market Trends & Insights

- North America dominated the natural oil polyols market with the largest revenue share of 38.9% in 2025, supported by strong demand for bio-based polyurethane materials across automotive, construction, and furniture industries.

- Asia-Pacific natural oil polyols market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding construction activities, and growing awareness of sustainable chemical alternatives in countries such as China, Japan, and India.

- The Polyether Oil segment held the largest market revenue share of approximately 58.6% in 2025 driven by its extensive use in flexible polyurethane foams, adhesives, and cushioning applications across automotive and furniture industries. Polyether oil polyols are preferred due to their superior elasticity, hydrolysis resistance, and compatibility with a wide range of bio-based feedstocks used in large-scale polyurethane production.

- The Polyester Oil segment is projected to register the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing demand in rigid foams, coatings, and high-performance insulation materials. Rising adoption in construction-grade thermal insulation panels and industrial coatings is accelerating segment expansion, particularly in Europe and North America where green building regulations are strengthening bio-based material usage.

- The Soy Oil Polyols segment held the largest market revenue share of approximately 34.2% in 2025 driven by high availability, cost efficiency, and strong integration across polyurethane foam manufacturing for furniture and automotive seating applications.

- The Castor Oil Polyols segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by superior chemical functionality, high hydroxyl value, and increasing adoption in specialty coatings and flexible foam applications. Rising industrial preference for non-edible oil-based feedstocks is further supporting castor oil polyol expansion across emerging economies.

- The Polyurethane Foams segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong demand from furniture, automotive interiors, insulation panels, and packaging applications. Bio-based foams are increasingly preferred due to their lightweight properties, durability, and reduced environmental impact.

- The Metallic Coatings segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by rising demand for corrosion-resistant and sustainable coating systems in automotive and industrial equipment applications. Increasing replacement of petroleum-based polyols in high-performance coating formulations is supporting segment growth.

- The Construction segment held the largest market revenue share of approximately 38.7% in 2025 driven by increasing adoption of green building materials, energy-efficient insulation systems, and rising infrastructure development activities across emerging economies.

- The Automobile segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing integration of bio-based polyurethane materials in vehicle seating, interiors, and lightweight components. Automotive OEMs are increasingly adopting natural oil polyols to reduce vehicle weight and meet stringent emission reduction targets.

Market Size & Forecast

- Global Market Value (2025): USD 7.48 Billion

- Expected Market Value (2033): USD 12.19 Billion

- Forecast CAGR (2026–2033): 6.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Natural Oil Polyols Market Segmentation

|

Attributes |

Natural Oil Polyols Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Dow (U.S.) |

|

Market Opportunities |

• Expansion In Bio-Based Polyurethane Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Natural Oil Polyols Market Trends

Trend: Growth In Bio-Based Feedstock Integration And Low-Carbon Polyurethane Production

Increasing demand for sustainable and renewable chemical intermediates is accelerating the adoption of natural oil polyols across polyurethane manufacturing. Conventional petrochemical-based polyols are being increasingly replaced due to regulatory pressure on carbon emissions, volatile crude oil pricing, and rising corporate sustainability commitments. Natural oil polyols derived from soybean, castor, and palm kernel oils are gaining traction as they offer reduced carbon footprint and improved lifecycle performance in foam, coatings, and elastomers applications.

In automotive manufacturing, producers are integrating bio-based polyols into seat cushioning and interior foams to meet EU end-of-life vehicle directives and U.S. EPA sustainability guidelines. For instance, several global automotive OEMs have reported up to 20–25% reduction in product carbon intensity by shifting toward bio-polyurethane seating systems in 2024–2025 model lines. In construction, green building certifications such as LEED and BREEAM are encouraging the use of renewable insulation materials, driving adoption of natural oil polyols in rigid foam insulation panels for energy-efficient buildings.

The rapid expansion of electric mobility, cold-chain logistics, and energy-efficient construction materials is further increasing demand for lightweight and durable polyurethane components. In addition, advancements in epoxidized vegetable oil processing and catalytic conversion technologies are improving polyol yield efficiency and performance consistency. Pilot-scale industrial deployments in Europe during 2025 have demonstrated improved thermal insulation performance of nearly 10–15% in bio-based rigid foams compared to conventional petrochemical variants under standardized testing conditions.

Global Natural Oil Polyols Market Dynamics

Key Market Driver: Rising Demand For Sustainable Polyurethane Materials

Industries globally are shifting toward renewable chemical inputs due to tightening environmental regulations and rising pressure to reduce dependence on fossil-based raw materials. Natural oil polyols are gaining traction as a sustainable alternative in flexible foams, rigid foams, adhesives, and coatings due to their lower carbon footprint and improved biodegradability.

Manufacturers in automotive and construction sectors are increasingly adopting bio-based polyurethane systems to comply with emission reduction targets and green building standards. For instance, EU REACH regulations and U.S. EPA sustainability initiatives are encouraging substitution of petroleum-derived polyols with renewable alternatives. Industrial trials in 2024–2025 have shown that bio-based polyurethane foams can reduce carbon emissions by approximately 15–30% compared to conventional systems while maintaining comparable mechanical performance.

Key Restraint/Challenge: Feedstock Price Volatility And Processing Limitations

The natural oil polyols market faces challenges due to fluctuations in agricultural raw material supply such as soybean and palm oil, which are affected by climate variability and global commodity price changes. These fluctuations directly impact production stability and cost predictability for manufacturers.

In addition, processing complexity in converting vegetable oils into high-performance polyols increases production costs compared to conventional petrochemical routes. Performance limitations in extreme temperature and high-load industrial applications also restrict broader substitution in some polyurethane segments. Industry studies indicate that bio-based polyols may exhibit up to 10–20% variation in performance consistency depending on feedstock purity and processing conditions, limiting their use in high-precision applications.

Key Market Opportunity: Expansion In Green Construction And Electric Mobility Applications

The rapid expansion of sustainable construction and electric mobility industries is creating strong opportunities for natural oil polyols. Green building certifications and energy efficiency mandates are driving demand for bio-based insulation materials, while EV manufacturers are increasingly focusing on lightweight and low-emission interior components.

For instance, insulation foam manufacturers in North America and Europe are integrating bio-polyols into rigid foam panels to improve thermal efficiency and meet net-zero building targets. In the EV sector, natural oil polyols are being used in lightweight seating systems and interior components, contributing to improved vehicle efficiency and reduced cabin weight. In addition, advancements in catalytic bio-refining technologies are improving polyol performance consistency, enabling broader adoption across industrial polyurethane applications. Pilot projects in 2025 have demonstrated up to 12–18% improvement in insulation efficiency in hybrid bio-based foam systems compared to conventional formulations.

Global Natural Oil Polyols Market Scope

The market is segmented on the basis of model, type, functionality, offering, and end-use application.

• By Type

On the basis of type, the natural oil polyols market is segmented into Polyester Oil and Polyether Oil. The Polyether Oil segment held the largest market revenue share of approximately 58.6% in 2025 driven by its extensive use in flexible polyurethane foams, adhesives, and cushioning applications across automotive and furniture industries. Polyether oil polyols are preferred due to their superior elasticity, hydrolysis resistance, and compatibility with a wide range of bio-based feedstocks used in large-scale polyurethane production.

The Polyester Oil segment is projected to register the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing demand in rigid foams, coatings, and high-performance insulation materials. Rising adoption in construction-grade thermal insulation panels and industrial coatings is accelerating segment expansion, particularly in Europe and North America where green building regulations are strengthening bio-based material usage.

• By Product

On the basis of product, the natural oil polyols market is segmented into Soy Oil Polyols, Palm Oil Polyols, Castor Oil Polyols, Sunflower Oil Polyols, Canola Oil Polyols, and Others. The Soy Oil Polyols segment held the largest market revenue share of approximately 34.2% in 2025 driven by high availability, cost efficiency, and strong integration across polyurethane foam manufacturing for furniture and automotive seating applications.

The Castor Oil Polyols segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by superior chemical functionality, high hydroxyl value, and increasing adoption in specialty coatings and flexible foam applications. Rising industrial preference for non-edible oil-based feedstocks is further supporting castor oil polyol expansion across emerging economies.

• By Application

On the basis of application, the market is segmented into Polyurethane Foams, Metallic Coatings, Cushioning, Feed Stocks, Bakery Products, and Others. The Polyurethane Foams segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong demand from furniture, automotive interiors, insulation panels, and packaging applications. Bio-based foams are increasingly preferred due to their lightweight properties, durability, and reduced environmental impact.

The Metallic Coatings segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by rising demand for corrosion-resistant and sustainable coating systems in automotive and industrial equipment applications. Increasing replacement of petroleum-based polyols in high-performance coating formulations is supporting segment growth.

• By End User

On the basis of end user, the market is segmented into Construction, Transportation, Automobile, Food, and Others. The Construction segment held the largest market revenue share of approximately 38.7% in 2025 driven by increasing adoption of green building materials, energy-efficient insulation systems, and rising infrastructure development activities across emerging economies.

The Automobile segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing integration of bio-based polyurethane materials in vehicle seating, interiors, and lightweight components. Automotive OEMs are increasingly adopting natural oil polyols to reduce vehicle weight and meet stringent emission reduction targets.

Global Natural Oil Polyols Market Regional Analysis

North America Natural Oil Polyols Market Insight

North America dominated the natural oil polyols market with the largest revenue share of 38.9% in 2025, supported by strong demand for bio-based polyurethane materials across automotive, construction, and furniture industries. The region benefits from strict environmental regulations, high adoption of sustainable manufacturing practices, and growing preference for low-carbon and renewable chemical intermediates. Consumers and manufacturers in the region increasingly prioritize green materials that reduce lifecycle emissions while maintaining high performance in foam and coating applications.

U.S. Natural Oil Polyols Market Insight

The U.S. natural oil polyols market captured the largest revenue share in 2025 within North America, driven by rapid expansion of bio-based chemical production and strong demand from automotive seating, insulation foams, and packaging industries. Manufacturers are increasingly shifting toward soybean and castor oil-based polyols to comply with sustainability mandates and corporate ESG goals. In addition, rising investment in green building materials and energy-efficient infrastructure is accelerating adoption of natural oil polyols in rigid insulation panels and construction-grade polyurethane systems.

Europe Natural Oil Polyols Market Insight

The Europe natural oil polyols market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent carbon reduction regulations, circular economy policies, and strong demand for renewable raw materials in polyurethane production. The region is witnessing increased adoption of bio-based polyols in automotive interiors, insulation foams, and coatings, supported by EU Green Deal initiatives and sustainability certification standards.

U.K. Natural Oil Polyols Market Insight

The U.K. natural oil polyols market is expected to witness strong growth from 2026 to 2033, driven by rising demand for sustainable construction materials and increasing focus on low-emission manufacturing practices. The expansion of green building projects and retrofit insulation upgrades is supporting higher consumption of bio-based polyurethane foams in residential and commercial applications.

Germany Natural Oil Polyols Market Insight

The Germany natural oil polyols market is expected to witness rapid growth from 2026 to 2033, fueled by strong industrial focus on sustainability, advanced chemical manufacturing infrastructure, and increasing demand for eco-friendly insulation materials. Germany’s automotive and construction sectors are increasingly integrating bio-based polyols to reduce carbon intensity and comply with strict environmental standards.

Asia-Pacific Natural Oil Polyols Market Insight

The Asia-Pacific natural oil polyols market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding construction activities, and growing awareness of sustainable chemical alternatives in countries such as China, Japan, and India. The region is also emerging as a key production hub for natural oil-based feedstocks, improving cost competitiveness and supply chain accessibility for bio-based polyurethane manufacturing.

Japan Natural Oil Polyols Market Insight

The Japan natural oil polyols market is expected to witness steady growth from 2026 to 2033 due to increasing demand for lightweight, high-performance, and environmentally friendly materials in automotive and electronics applications. Japanese manufacturers are gradually shifting toward bio-based polyurethane systems to enhance sustainability and improve energy efficiency in industrial applications.

China Natural Oil Polyols Market Insight

The China natural oil polyols market accounted for the largest market revenue share in Asia Pacific in 2025, driven by rapid urbanization, strong manufacturing capabilities, and expanding demand for polyurethane foams in construction, automotive, and packaging industries. China’s push toward low-carbon industrial development and green materials adoption is significantly accelerating the use of natural oil polyols across large-scale industrial applications.

Global Natural Oil Polyols Market Share

The Natural Oil Polyols industry is primarily led by well-established companies, including:

• Dow (U.S.)

• Cargill, Incorporated (U.S.)

• BASF SE (Germany)

• Huntsman International LLC (U.S.)

• Emery Oleochemicals (U.S.)

• Elevance Renewable Sciences, Inc. (U.S.)

• IFS Group (U.K.)

• Stepan Company (U.S.)

• Jayant Agro-Organics Limited (India)

• Mitsui Chemicals, Inc. (Japan)

• The Lubrizol Corporation (U.S.)

• Vertellus Holdings LLC (U.S.)

Latest Developments in Global Natural Oil Polyols Market

- In March 2023, Perstorp Holding AB, product launch, introduced Evyron T100 (trimethylolpropane) and Neeture N100 (neopentyl glycol), both derived from 100% renewable sources, aiming to reduce carbon footprint across the value chain and strengthen its position in low-emission chemical solutions, positively impacting demand for sustainable polyols in the market.

- In November 2022, C16 Biosciences, Inc., strategic development, announced plans to launch a fermentation-based palm oil alternative for personal care and food applications by 2024 and prepare FDA submission, which is expected to support sustainable ingredient substitution and accelerate bio-based oil adoption in global end-use industries.

- In September 2022, Ingevity, capacity expansion, expanded its DeRidder, Louisiana manufacturing facility, increasing polyol production capacity by 40% and reducing lead times, thereby improving supply efficiency and helping the company meet rising demand for its Capa range in industrial applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Natural Oil Polyols Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Natural Oil Polyols Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Natural Oil Polyols Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.