Global Needle Free Iv Connectors Market

Market Size in USD Million

USD

995.54 Million

USD

1,857.74 Million

2024

2032

USD

995.54 Million

USD

1,857.74 Million

2024

2032

| 2025 - 2032 | |

| USD 995.54 Million | |

| USD 1,857.74 Million | |

| % | |

|

Needle Free Iv Connectors Market Size

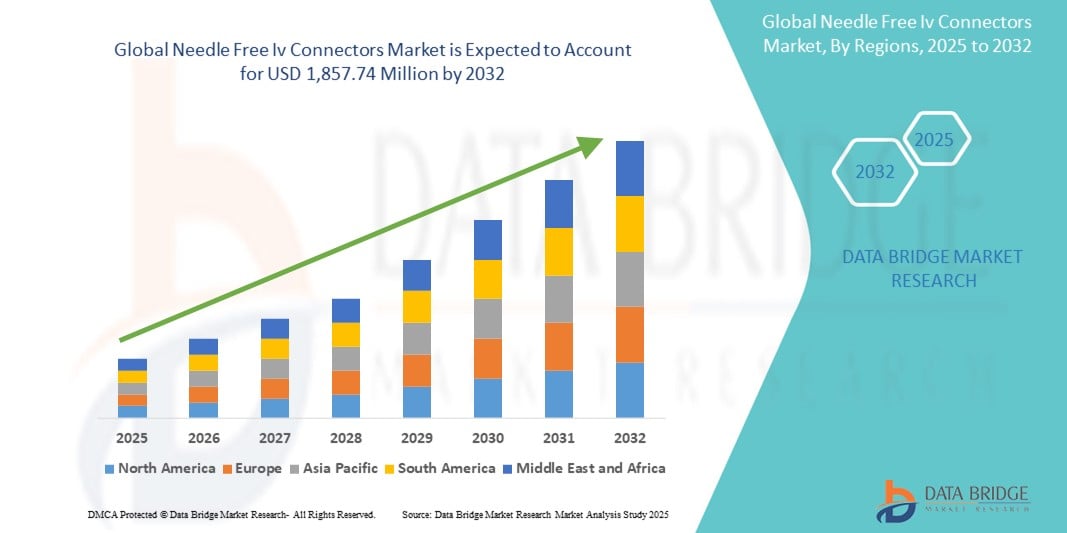

- The global needle free IV connectors market size was valued at USD 995.54 million in 2024 and is expected to reach USD 1,857.74 million by 2032, at a CAGR of 8.11% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within intravenous (IV) therapy equipment and infection prevention technologies, leading to increased digitalization and safety in both hospital and homecare settings

- Furthermore, rising healthcare professional demand for secure, user-friendly, and contamination-free IV access solutions is establishing needle-free IV connectors as the preferred option for reducing bloodstream infection risks. These converging factors are accelerating the uptake of needle-free IV connector solutions, thereby significantly boosting the industry's growth

Needle Free Iv Connectors Market Analysis

- Needle-free IV connectors, designed to reduce the risk of needlestick injuries and prevent catheter-related bloodstream infections, are becoming essential components in modern intravenous therapy practices across hospitals, clinics, and homecare settings due to their safety, ease of use, and infection control benefits

- The escalating demand for needle-free IV connectors is primarily fueled by the increasing prevalence of chronic diseases, rising hospital-acquired infection (HAI) rates, and growing awareness around safe infusion practices among healthcare professionals

- North America dominated the needle-free IV connectors market with the largest revenue share of 42.8% in 2024, driven by advanced healthcare infrastructure, high patient safety standards, and a strong presence of key industry players. The U.S. is witnessing significant adoption of needle-free IV connectors across both inpatient and outpatient care, supported by stringent regulatory policies and continuous product innovation

- Asia-Pacific is expected to be the fastest-growing region in the needle-free IV connectors market during the forecast period, projected to grow at a CAGR of 9.6% from 2025 to 2032, due to increasing healthcare investments, rising incidence of infectious diseases, and rapid expansion of hospital infrastructure in countries such as India, China, and Indonesia

- The straight channel segment dominated the needle-free IV connectors market with the largest market revenue share of 38.6% in 2024, driven by its simplicity, ease of use, and widespread acceptance in hospitals and clinics. Straight connectors are commonly used in intravenous therapy due to their efficient design, which reduces the risk of contamination and provides reliable fluid transfer

Report Scope and Needle Free Iv Connectors Market Segmentation

|

Attributes |

Needle Free IV Connectors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Needle Free Iv Connectors Market Trends

“Increased Emphasis on Infection Control and Patient Safety”

- A significant and accelerating trend in the global needle free IV connectors market is the growing emphasis on infection prevention and patient safety within healthcare settings. The shift from traditional needle-based systems to closed, needle-free alternatives is reshaping clinical practices globally

- For instance, leading healthcare institutions have reported a measurable reduction in catheter-related bloodstream infections (CRBSIs) following the adoption of needle-free connectors, highlighting their effectiveness in improving patient outcomes

- These connectors reduce the risk of needlestick injuries for healthcare workers and minimize microbial ingress, a key factor in hospital-acquired infections. Advanced connector designs are now incorporating anti-reflux mechanisms, positive displacement, and closed systems to enhance fluid integrity and reduce contamination

- Furthermore, global regulatory guidelines—including those from the CDC, WHO, and FDA—strongly support the adoption of needle-free IV systems, accelerating their use in both inpatient and outpatient care settings

- As healthcare providers increasingly shift towards value-based care and infection prevention becomes a top priority, the demand for safe, user-friendly, and effective IV access devices continue to rise

- This trend toward safer infusion practices is fundamentally transforming the way intravenous therapies are administered across hospitals, ambulatory centers, and homecare environments. Companies such as ICU Medical, Becton Dickinson and Company, and Baxter are actively developing next-generation needle-free connectors to meet evolving clinical needs and regulatory standards

- The growing demand for needle-free IV connectors, supported by strong evidence of their safety benefits and cost-effectiveness, is driving rapid market expansion globally, especially in developed healthcare systems and increasingly in emerging economies.

Needle Free Iv Connectors Market Dynamics

Driver

“Growing Need Due to Rising Hospital-Acquired Infections and Demand for Safe Infusion Systems”

- The increasing prevalence of hospital-acquired infections (HAIs) and the need to reduce catheter-related bloodstream infections (CRBSIs) are significant drivers fueling the demand for needle-free IV connectors. These connectors minimize the risk of contamination, offering a safer alternative to traditional systems

- For instance, the Centers for Disease Control and Prevention (CDC) emphasizes the importance of closed systems such as needle-free connectors in infection control protocols, especially in ICUs and oncology wards

- As hospitals and outpatient facilities increasingly shift towards closed IV systems for safer medication administration, needle-free connectors are becoming a critical part of intravenous therapy

- Furthermore, the rise in chronic disease prevalence, including cancer and diabetes, which require frequent IV access, is propelling the adoption of these connectors across home care and ambulatory surgical centers

- The need for user-friendly, efficient, and compatible infusion solutions—especially in home settings—has driven the development of more ergonomic, secure, and multi-channel designs within needle-free IV connector systems

- The expansion of minimally invasive procedures and value-based healthcare models is also encouraging healthcare providers to adopt cost-effective solutions that improve patient outcomes and reduce hospital stays

- As medical device regulations become stricter in regions such as the U.S. and Europe, manufacturers are compelled to offer high-quality, sterile, and compliant needle-free connectors, thereby enhancing product quality and trust in these devices

Restraint/Challenge

“Complexity in Design and Concerns Regarding Device-Related Infections”

- One of the key restraints limiting the growth of the needle-free IV connectors market is the variation in connector design, which may inadvertently contribute to microbial ingress or backflow—posing infection risks

- Device-related infections can occur if the connectors are not disinfected properly or if incompatible devices are used, leading to complications and increased healthcare costs

- For instance, the FDA has raised concerns about certain designs, especially those with negative pressure mechanisms, which may have a higher association with bloodstream infections when not used with proper flushing techniques

- This challenge has pushed healthcare providers to standardize IV connector use, which can restrict product diversity and limit new entrants in the market

- In addition, the high cost of advanced connectors, particularly those with antimicrobial coatings or multi-channel access points, may deter adoption in resource-limited settings, especially in developing nations

- Training and education gaps regarding the proper usage, cleaning, and maintenance of these devices can also compromise their effectiveness, hindering full market potential

- Overcoming these hurdles will require collaborative efforts between manufacturers, healthcare providers, and regulatory authorities to develop cost-effective, infection-resistant, and user-friendly designs that promote safety and efficacy in intravenous therapy

Needle Free Iv Connectors Market Scope

The market is segmented on the basis of design type, mechanism, dwell time, and end-user.

• By Design Type

On the basis of design type, the needle free IV connectors market is segmented into straight channel, T-channel, Y-channel, and multi-channel. The straight channel segment dominated the largest market revenue share of 38.6% in 2024, driven by its simplicity, ease of use, and widespread acceptance in hospitals and clinics. Straight connectors are commonly used in intravenous therapy due to their efficient design, which reduces the risk of contamination and provides reliable fluid transfer.

The multi-channel segment is anticipated to witness the fastest growth rate of 23.4% from 2025 to 2032, due to its ability to support multiple fluid pathways simultaneously. These connectors offer flexibility in drug administration and are increasingly adopted in complex patient care settings such as ICUs and oncology units.

• By Mechanism

On the basis of mechanism, the needle free IV connectors market is segmented into positive, negative, and neutral. The neutral mechanism segment held the largest market revenue share of 41.2% in 2024, owing to its ability to minimize the risk of catheter-related bloodstream infections (CRBSIs). These connectors are preferred for their balanced flow and safety features, reducing complications associated with reflux.

The positive mechanism segment is expected to witness the fastest CAGR of 22.1% from 2025 to 2032, attributed to its one-way valve system that prevents backflow of blood into the catheter, thereby decreasing infection risk and improving patient outcomes.

• By Dwell Time

On the basis of dwell time, the needle free IV connectors market is segmented into seven-day and other than seven-day. The seven-day segment accounted for the largest market share of 67.5% in 2024, driven by its compatibility with standard infusion protocols and reduced frequency of device changes, which lowers patient discomfort and healthcare costs.

The other than seven-day segment is projected to grow at a fastest CAGR of 20.3% from 2025 to 2032, due to emerging products tailored for short-term procedures or high-risk patients who require frequent line access changes.

• By End-User

On the basis of end-user, the needle free IV connectors market is segmented into hospitals, ambulatory surgical centers, and others. The hospitals segment captured the largest revenue share of 65.9% in 2024, fueled by the high volume of inpatient admissions, growing prevalence of chronic illnesses, and robust demand for infection prevention devices.

The ambulatory surgical centers segment is expected to grow at the fastest CAGR of 21.4% from 2025 to 2032, as outpatient care gains traction and these centers increasingly adopt advanced needle-free technologies to enhance safety, streamline operations, and comply with stringent infection control standards.

Needle Free Iv Connectors Market Regional Analysis

- North America dominated the needle free IV connectors market with the largest revenue share of 42.8% in 2024, driven by advanced healthcare infrastructure, growing prevalence of chronic conditions, and strong emphasis on reducing catheter-related bloodstream infections (CRBSIs) through closed-system IV access technologies

- Hospitals and ambulatory surgical centers across the region increasingly adopt needle-free connectors to improve patient safety and minimize needlestick injuries. The region’s robust regulatory support and healthcare digitization further boost product demand

- The presence of key market players, favorable reimbursement policies, and a shift towards home-based infusion therapies continue to solidify North America’s leadership in this space

U.S. Needle Free IV Connectors Market Insight

The U.S. needle free IV connectors market captured the largest revenue share of 81.05% within North America in 2024, fueled by high infection prevention standards set by the CDC and FDA, rising hospital-acquired infection (HAI) awareness, and adoption of needleless systems across both inpatient and outpatient settings. The market benefits from widespread implementation of home infusion therapies, aging patient demographics, and strong demand for technologically advanced IV connectors.

Europe Needle Free IV Connectors Market Insight

The Europe needle free IV connectors market is projected to expand at a CAGR of 7.2% during 2025–2032, driven by supportive healthcare infrastructure, strict infection prevention regulations, and growing demand for safe IV therapy solutions. Key countries such as Germany, the U.K., and France are increasingly emphasizing closed-system devices in hospitals to mitigate bloodstream infection risks.

U.K. Needle Free IV Connectors Market Insight

The U.K. needle free IV connectors market accounted for 13.5% of the Europe Needle Free IV Connectors market in 2024, and is anticipated to grow at a notable CAGR of 6.8% during the forecast period. This growth is driven by strong NHS-backed initiatives promoting HBV screening, broader infection prevention programs, and increased focus on patient safety in infusion practices.

Germany Needle Free IV Connectors Market Insight

The Germany needle free IV connectors market contributed approximately 18% of Europe’s revenue share in 2024, supported by a technologically advanced medical ecosystem, preference for eco-friendly and disposable medical products, and increased investment in ICU and emergency care infrastructure. The country’s push toward digitized and integrated care systems is further accelerating the demand for needleless IV connectors.

Asia-Pacific Needle Free IV Connectors Market Insight

The Asia-Pacific needle free IV connectors market is poised to grow at the fastest CAGR of 9.6% from 2025 to 2032, led by increasing access to healthcare, rapid hospital infrastructure expansion, and growing awareness of infection control measures. Countries such as China, Japan, and India are investing heavily in safe infusion technologies, making the region a vital hub for market expansion and manufacturing.

Japan Needle Free IV Connectors Market Insight

The Japan needle free IV connectors market accounted for approximately 12% of the Asia-Pacific market revenue in 2024, driven by its aging population, advanced healthcare infrastructure, and proactive infection prevention practices. Hospitals and homecare providers are increasingly adopting needle-free systems due to their safety, ease of use, and compatibility with modern infusion equipment.

China Needle Free IV Connectors Market Insight

The China needle free IV connectors market captured 45% of the Asia-Pacific revenue share in 2024, making it the largest contributor in the region. This dominance stems from its rapidly growing healthcare sector, expansion of tertiary hospitals, favorable government healthcare reforms, and widespread adoption of closed-system IV devices to reduce CRBSIs. In addition, China's position as a manufacturing powerhouse supports affordable and scalable production of these devices.

Needle Free Iv Connectors Market Share

The Needle Free Iv Connectors industry is primarily led by well-established companies, including:

- BD (U.S.)

- Ascor SA (Poland)

- Smiths Group plc (U.K.)

- B. Braun SE (Germany)

- AngioDynamics (U.S.)

- Terumo Corporation (Japan)

- RyMed Technologies, LLC (U.S.)

- Baxter (U.S.)

- Nexus Medical (U.S.)

- Vygon (France)

- CU Medical Germany GmbH (South Korea)

Latest Developments in Global Needle Free Iv Connectors Market

- In November 2023, BD introduced the PIVOT Pro Needle-free Blood Collection Device, designed to work seamlessly with both integrated and long peripheral IV catheters. This innovative product aligns with BD's vision of achieving a "One-Stick Hospital Stay," aiming to enhance patient comfort and streamline blood collection procedures. The launch highlights BD's commitment to improving healthcare efficiency through advanced medical technologies

- In September 2023, PharmaJet, known for its precision delivery systems, announced encouraging results from Scancell's Phase 2 clinical trial targeting patients with unresectable advanced melanoma. The trial utilized the PharmaJet Stratis System for needle-free injection, which has emerged as a favored method among patients. This positive data reinforces the effectiveness of needle-free technology in enhancing patient experience and treatment outcomes

- In September 2023, the Indian government launched GEMCOVAC-OM, a COVID-19 booster vaccine specifically designed with mRNA targeting the Omicron variant. Administered intradermally through a needle-free injector, this thermostable vaccine demonstrated enhanced immune responses in study participants. The innovative delivery method contributes to its effectiveness, marking a significant advancement in vaccination strategies

- In August 2023, Pulse Needle Free Systems launched the first-ever line of disposable needle-free vaccination equipment for animals. Priced comparably to traditional syringes and needles, these innovative devices offer significant health and food safety benefits for pig farmers. This development marks a notable advancement in veterinary vaccination methods, enhancing efficiency and reducing the risk of infection

- In June 2023, PharmaJet partnered with Zydus Lifesciences to successfully administer the world’s first plasmid DNA COVID-19 vaccine utilizing its Tropis system. This innovative delivery method has demonstrated enhanced immune responses and improved clinical effectiveness. This collaboration marks a significant milestone in vaccine technology, showcasing the potential of needle-free delivery systems in combating infectious diseases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1. INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL NEEDLE FREE IV CONNECTORS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2. MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL NEEDLE FREE IV CONNECTORS MARKET SIZE

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 TRIPOD DATA VALIDATION MODEL

2.2.4 MARKET GUIDE

2.2.5 MULTIVARIATE MODELLING

2.2.6 TOP TO BOTTOM ANALYSIS

2.2.7 CHALLENGE MATRIX

2.2.8 APPLICATION COVERAGE GRID

2.2.9 STANDARDS OF MEASUREMENT

2.2.10 VENDOR SHARE ANALYSIS

2.2.11 SALES VALUE AND VOLUME

2.2.12 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.13 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL NEEDLE FREE IV CONNECTORS MARKET: RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3. MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4. EXECUTIVE SUMMARY

5. PREMIUM INSIGHTS

5.1 PESTEL ANALYSIS

5.2 PORTER’S FIVE FORCES MODEL

6. INDUSTRY INSIGHTS

6.1 MICRO AND MACRO ECONOMIC FACTORS

6.2 PENETRATION AND GROWTH PROSPECT MAPPING

6.3 KEY PRICING STRATEGIES

6.4 INTERVIEWS WITH SPECIALIST

6.5 ANALYIS AND RECOMMENDATION

7. INTELLECTUAL PROPERTY (IP) PORTFOLIO

7.1 PATENT QUALITY AND STRENGTH

7.2 PATENT FAMILIES

7.3 LICENSING AND COLLABORATIONS

7.4 COMPETITIVE LANDSCAPE

7.5 IP STRATEGY AND MANAGEMENT

7.6 OTHER

8. COST ANALYSIS BREAKDOWN

9. TECHNONLOGY ROADMAP

10. INNOVATION TRACKER AND STRATEGIC ANALYSIS

10.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

10.1.1 JOINT VENTURES

10.1.2 MERGERS AND ACQUISITIONS

10.1.3 LICENSING AND PARTNERSHIP

10.1.4 TECHNOLOGY COLLABORATIONS

10.1.5 STRATEGIC DIVESTMENTS

10.2 NUMBER OF PRODUCTS IN DEVELOPMENT

10.3 STAGE OF DEVELOPMENT

10.4 TIMELINES AND MILESTONES

10.5 INNOVATION STRATEGIES AND METHODOLOGIES

10.6 RISK ASSESSMENT AND MITIGATION

10.7 FUTURE OUTLOOK

11. REGULATORY COMPLIANCE

11.1 REGULATORY AUTHORITIES

11.2 REGULATORY CLASSIFICATIONS

11.2.1 CLASS I

11.2.2 CLASS II

11.2.3 CLASS III

11.3 REGULATORY SUBMISSIONS

11.4 INTERNATIONAL HARMONIZATION

11.5 COMPLIANCE AND QUALITY MANAGEMENT SYSTEMS

11.6 REGULATORY CHALLENGES AND STRATEGIES

12. REIMBURSEMENT FRAMEWORK

13. OPPUTUNITY MAP ANALYSIS

14. VALUE CHAIN ANALYSIS

15. HEALTHCARE ECONOMY

15.1 HEALTHCARE EXPENDITURE

15.2 CAPITAL EXPENDITURE

15.3 CAPEX TRENDS

15.4 CAPEX ALLOCATION

15.5 FUNDING SOURCES

15.6 INDUSTRY BENCHMARKS

15.7 GDP RATION IN OVERALL GDP

15.8 HEALTHCARE SYSTEM STRUCTURE

15.9 GOVERNMENT POLICIES

15.10 ECONOMIC DEVELOPMENT

16. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY PRODUCT

16.1 OVERVIEW

16.2 STRAIGHT CHANNEL

16.2.1 BY TUBE LUMEN

16.2.1.1. SINGLE

16.2.1.2. DOUBLE

16.2.1.3. TRIPLE

16.2.2 BY TUBE LENGTH

16.2.2.1. 10 CM

16.2.2.2. 15 CM

16.2.2.3. 30 CM

16.2.2.4. OTHERS

16.2.3 BY BORE SIZE

16.2.3.1. SMALL BORE

16.2.3.2. LARGE BORE

16.2.4 BY MATERIAL

16.2.4.1. SILICONE

16.2.4.2. PLASTIC

16.2.4.3. POLYVINYL CHLORIDE (PVC)

16.2.4.4. POLYCARBONATE OR COPOLYESTER

16.2.4.5. OTHERS

16.2.5 BY HYGEINE

16.2.5.1. STERILE

16.2.5.2. NON-STERILE

16.2.6 BY COLOUR

16.2.6.1. YELLOW

16.2.6.2. GREEN

16.2.6.3. RED

16.2.6.4. OTHERS

16.2.7 OTHERS

16.3 Y CHANNEL

16.3.1 BY TUBE LUMEN

16.3.1.1. SINGLE

16.3.1.2. DOUBLE

16.3.1.3. TRIPLE

16.3.2 BY TUBE LENGTH

16.3.2.1. 10 CM

16.3.2.2. 15 CM

16.3.2.3. 30 CM

16.3.2.4. OTHERS

16.3.3 BY BORE SIZE

16.3.3.1. SMALL BORE

16.3.3.2. LARGE BORE

16.3.4 BY MATERIAL

16.3.4.1. SILICONE

16.3.4.2. PLASTIC

16.3.4.3. POLYVINYL CHLORIDE (PVC)

16.3.4.4. POLYCARBONATE OR COPOLYESTER

16.3.4.5. OTHERS

16.3.5 BY HYGEINE

16.3.5.1. STERILE

16.3.5.2. NON-STERILE

16.3.6 BY COLOUR

16.3.6.1. YELLOW

16.3.6.2. GREEN

16.3.6.3. RED

16.3.6.4. OTHERS

16.3.7 OTHERS

16.4 T CHANNEL

16.4.1 BY TUBE LUMEN

16.4.1.1. SINGLE

16.4.1.2. DOUBLE

16.4.1.3. TRIPLE

16.4.2 BY TUBE LENGTH

16.4.2.1. 10 CM

16.4.2.2. 15 CM

16.4.2.3. 30 CM

16.4.2.4. OTHERS

16.4.3 BY BORE SIZE

16.4.3.1. SMALL BORE

16.4.3.2. LARGE BORE

16.4.4 BY MATERIAL

16.4.4.1. SILICONE

16.4.4.2. PLASTIC

16.4.4.3. POLYVINYL CHLORIDE (PVC)

16.4.4.4. POLYCARBONATE OR COPOLYESTER

16.4.4.5. OTHERS

16.4.5 BY HYGEINE

16.4.5.1. STERILE

16.4.5.2. NON-STERILE

16.4.6 BY COLOUR

16.4.6.1. YELLOW

16.4.6.2. GREEN

16.4.6.3. RED

16.4.6.4. OTHERS

16.4.7 OTHERS

16.5 MULTI CHANNEL

16.5.1 BY TUBE LUMEN

16.5.1.1. SINGLE

16.5.1.2. DOUBLE

16.5.1.3. TRIPLE

16.5.2 BY TUBE LENGTH

16.5.2.1. 10 CM

16.5.2.2. 15 CM

16.5.2.3. 30 CM

16.5.2.4. OTHERS

16.5.3 BY BORE SIZE

16.5.3.1. SMALL BORE

16.5.3.2. LARGE BORE

16.5.4 BY MATERIAL

16.5.4.1. SILICONE

16.5.4.2. PLASTIC

16.5.4.3. POLYVINYL CHLORIDE (PVC)

16.5.4.4. POLYCARBONATE OR COPOLYESTER

16.5.4.5. OTHERS

16.5.5 BY HYGEINE

16.5.5.1. STERILE

16.5.5.2. NON-STERILE

16.5.6 BY COLOUR

16.5.6.1. YELLOW

16.5.6.2. GREEN

16.5.6.3. RED

16.5.6.4. OTHERS

16.5.7 OTHERS

17. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY TYPE

17.1 OVERVIEW

17.2 POSITIVE FLUID DISPLACEMENT

17.3 NEGATIVE FLUID DISPLACEMENT

17.4 NEUTRAL FLUID DISPLACEMENT

18. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY MATERIAL

18.1 OVERVIEW

18.2 SILICONE

18.3 PLASTIC

18.4 POLYVINYL CHLORIDE (PVC)

18.5 POLYCARBONATE OR COPOLYESTER

18.6 OTHERS

19. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY HYGEINE

19.1 OVERVIEW

19.2 STERILE

19.3 NON-STERILE

20. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY PACKAGING

20.1 OVERVIEW

20.2 50/BOX

20.3 100/BOX

20.4 OTHERS

21. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY APPLICATION

21.1 OVERVIEW

21.2 UROLOGY

21.3 CARDIOLOGY

21.4 BLOOD PROCESSING

21.5 OTHERS

22. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY END USER

22.1 OVERVIEW

22.2 HOSPITALS

22.2.1 BY TYPE

22.2.1.1. PUBLIC

22.2.1.2. PRIVATE

22.2.2 BY LEVEL

22.2.2.1. TIER 1

22.2.2.2. TIER 2

22.2.2.3. TIER 3

22.3 SPECIALTY CLINICS

22.3.1 PUBLIC

22.3.2 PRIVATE

22.4 HOME CARE SETTINGS

22.5 AMBULATORY SURGICAL CENTRE

22.6 ACADEMIC AND RESEARCH INSTITUTES

22.7 OTHERS

23. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY DISTRIBUTION CHANNEL

23.1 OVERVIEW

23.2 DIRECT TENDER

23.3 RETAIL SALES

23.3.1 OFFLINE

23.3.1.1. HOSPITAL PAHRMACY

23.3.1.2. DRUGS STORES

23.3.1.3. OTHERS

23.3.2 ONLINE

23.3.2.1. E-STORES

23.3.2.2. COMPANY WEBSITE

23.3.2.3. OTHERS

23.4 OTHERS

24. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, BY GEOGRAPHY

GLOBAL NEEDLE FREE IV CONNECTORS MARKET (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

24.1 NORTH AMERICA

24.1.1 U.S.

24.1.2 CANADA

24.1.3 MEXICO

24.2 EUROPE

24.2.1 GERMANY

24.2.2 FRANCE

24.2.3 U.K.

24.2.4 ITALY

24.2.5 SPAIN

24.2.6 RUSSIA

24.2.7 TURKEY

24.2.8 BELGIUM

24.2.9 DENMARK

24.2.10 NETHERLANDS

24.2.11 SWITZERLAND

24.2.12 SWEDEN

24.2.13 POLAND

24.2.14 NORWAY

24.2.15 FINLAND

24.2.16 REST OF EUROPE

24.3 ASIA-PACIFIC

24.3.1 JAPAN

24.3.2 CHINA

24.3.3 SOUTH KOREA

24.3.4 INDIA

24.3.5 AUSTRALIA

24.3.6 NEW ZEALAND

24.3.7 SINGAPORE

24.3.8 THAILAND

24.3.9 MALAYSIA

24.3.10 VIETNAM

24.3.11 TAIWAN

24.3.12 INDONESIA

24.3.13 PHILIPPINES

24.3.14 REST OF ASIA-PACIFIC

24.4 SOUTH AMERICA

24.4.1 BRAZIL

24.4.2 ARGENTINA

24.4.3 REST OF SOUTH AMERICA

24.5 MIDDLE EAST AND AFRICA

24.5.1 SOUTH AFRICA

24.5.2 SAUDI ARABIA

24.5.3 BAHRAIN

24.5.4 UAE

24.5.5 KUWAIT

24.5.6 OMAN

24.5.7 QATAR

24.5.8 EGYPT

24.5.9 ISRAEL

24.5.10 REST OF MIDDLE EAST AND AFRICA

24.6 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

25. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, SWOT AND DBMR ANALYSIS

26. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, COMPANY LANDSCAPE

26.1 COMPANY SHARE ANALYSIS: GLOBAL

26.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

26.3 COMPANY SHARE ANALYSIS: EUROPE

26.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

26.5 COMPANY SHARE ANALYSIS: MIDDLE EAST AND AFRICA

26.6 MERGERS & ACQUISITIONS

26.7 NEW PRODUCT DEVELOPMENT & APPROVALS

26.8 EXPANSIONS

26.9 REGULATORY CHANGES

26.10 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

27. GLOBAL NEEDLE FREE IV CONNECTORS MARKET, COMPANY PROFILE

27.1 BD

27.1.1 COMPANY OVERVIEW

27.1.2 REVENUE ANALYSIS

27.1.3 GEOGRAPHIC PRESENCE

27.1.4 PRODUCT PORTFOLIO

27.1.5 RECENT DEVELOPMENTS

27.2 ROMSONS

27.2.1 COMPANY OVERVIEW

27.2.2 REVENUE ANALYSIS

27.2.3 GEOGRAPHIC PRESENCE

27.2.4 PRODUCT PORTFOLIO

27.2.5 RECENT DEVELOPMENTS

27.3 NP MEDICAL

27.3.1 COMPANY OVERVIEW

27.3.2 REVENUE ANALYSIS

27.3.3 GEOGRAPHIC PRESENCE

27.3.4 PRODUCT PORTFOLIO

27.3.5 RECENT DEVELOPMENTS

27.4 NORDSON CORPORATION

27.4.1 COMPANY OVERVIEW

27.4.2 REVENUE ANALYSIS

27.4.3 GEOGRAPHIC PRESENCE

27.4.4 PRODUCT PORTFOLIO

27.4.5 RECENT DEVELOPMENTS

27.5 VYGON GROUP

27.5.1 COMPANY OVERVIEW

27.5.2 REVENUE ANALYSIS

27.5.3 GEOGRAPHIC PRESENCE

27.5.4 PRODUCT PORTFOLIO

27.5.5 RECENT DEVELOPMENTS

27.6 BAIHE MEDICAL EUROPE

27.6.1 COMPANY OVERVIEW

27.6.2 REVENUE ANALYSIS

27.6.3 GEOGRAPHIC PRESENCE

27.6.4 PRODUCT PORTFOLIO

27.6.5 RECENT DEVELOPMENTS

27.7 ADVACARE PHARMA

27.7.1 COMPANY OVERVIEW

27.7.2 REVENUE ANALYSIS

27.7.3 GEOGRAPHIC PRESENCE

27.7.4 PRODUCT PORTFOLIO

27.7.5 RECENT DEVELOPMENTS

27.8 LEPU MEDICAL TECHNOLOGY(BEIJING)CO.,LTD.

27.8.1 COMPANY OVERVIEW

27.8.2 REVENUE ANALYSIS

27.8.3 GEOGRAPHIC PRESENCE

27.8.4 PRODUCT PORTFOLIO

27.8.5 RECENT DEVELOPMENTS

27.9 ICU MEDICAL , INC.

27.9.1 COMPANY OVERVIEW

27.9.2 REVENUE ANALYSIS

27.9.3 GEOGRAPHIC PRESENCE

27.9.4 PRODUCT PORTFOLIO

27.9.5 RECENT DEVELOPMENTS

27.10 POLYMEDICURE

27.10.1 COMPANY OVERVIEW

27.10.2 REVENUE ANALYSIS

27.10.3 GEOGRAPHIC PRESENCE

27.10.4 PRODUCT PORTFOLIO

27.10.5 RECENT DEVELOPMENTS

27.11 LARS MEDICARE PVT. LTD

27.11.1 COMPANY OVERVIEW

27.11.2 REVENUE ANALYSIS

27.11.3 GEOGRAPHIC PRESENCE

27.11.4 PRODUCT PORTFOLIO

27.11.5 RECENT DEVELOPMENTS

27.12 HANGZHOU FUSHAN MEDICAL APPLIANCES CO., LTD.

27.12.1 COMPANY OVERVIEW

27.12.2 REVENUE ANALYSIS

27.12.3 GEOGRAPHIC PRESENCE

27.12.4 PRODUCT PORTFOLIO

27.12.5 RECENT DEVELOPMENTS

27.13 BAXTER

27.13.1 COMPANY OVERVIEW

27.13.2 REVENUE ANALYSIS

27.13.3 GEOGRAPHIC PRESENCE

27.13.4 PRODUCT PORTFOLIO

27.13.5 RECENT DEVELOPMENTS

27.14 NEXUS MEDICAL

27.14.1 COMPANY OVERVIEW

27.14.2 REVENUE ANALYSIS

27.14.3 GEOGRAPHIC PRESENCE

27.14.4 PRODUCT PORTFOLIO

27.14.5 RECENT DEVELOPMENTS

27.15 MAIS INDIA

27.15.1 COMPANY OVERVIEW

27.15.2 REVENUE ANALYSIS

27.15.3 GEOGRAPHIC PRESENCE

27.15.4 PRODUCT PORTFOLIO

27.15.5 RECENT DEVELOPMENTS

27.16 SPARK LIFESCIENCES

27.16.1 COMPANY OVERVIEW

27.16.2 REVENUE ANALYSIS

27.16.3 GEOGRAPHIC PRESENCE

27.16.4 PRODUCT PORTFOLIO

27.16.5 RECENT DEVELOPMENTS

27.17 ASSET MEDICAL

27.17.1 COMPANY OVERVIEW

27.17.2 REVENUE ANALYSIS

27.17.3 GEOGRAPHIC PRESENCE

27.17.4 PRODUCT PORTFOLIO

27.17.5 RECENT DEVELOPMENTS

27.18 TERUMO CORPORATION

27.18.1 COMPANY OVERVIEW

27.18.2 REVENUE ANALYSIS

27.18.3 GEOGRAPHIC PRESENCE

27.18.4 PRODUCT PORTFOLIO

27.18.5 RECENT DEVELOPMENTS

27.19 RYMED TECHNOLOGIES, LLC

27.19.1 COMPANY OVERVIEW

27.19.2 REVENUE ANALYSIS

27.19.3 GEOGRAPHIC PRESENCE

27.19.4 PRODUCT PORTFOLIO

27.19.5 RECENT DEVELOPMENTS

27.20 INDOSURGICALS PRIVATE LIMITED

27.20.1 COMPANY OVERVIEW

27.20.2 REVENUE ANALYSIS

27.20.3 GEOGRAPHIC PRESENCE

27.20.4 PRODUCT PORTFOLIO

27.20.5 RECENT DEVELOPMENTS

27.21 WEIGAO MEIDCAL INTERNATIONAL CO., LTD

27.21.1 COMPANY OVERVIEW

27.21.2 REVENUE ANALYSIS

27.21.3 GEOGRAPHIC PRESENCE

27.21.4 PRODUCT PORTFOLIO

27.21.5 RECENT DEVELOPMENTS

27.22 HUBIOMED INC.

27.22.1 COMPANY OVERVIEW

27.22.2 REVENUE ANALYSIS

27.22.3 GEOGRAPHIC PRESENCE

27.22.4 PRODUCT PORTFOLIO

27.22.5 RECENT DEVELOPMENTS

27.23 KINDLY(KDL) MEDITECH

27.23.1 COMPANY OVERVIEW

27.23.2 REVENUE ANALYSIS

27.23.3 GEOGRAPHIC PRESENCE

27.23.4 PRODUCT PORTFOLIO

27.23.5 RECENT DEVELOPMENTS

27.24 SHANGHAI INT MEDICAL INSTRUMENTS CO., LTD.

27.24.1 COMPANY OVERVIEW

27.24.2 REVENUE ANALYSIS

27.24.3 GEOGRAPHIC PRESENCE

27.24.4 PRODUCT PORTFOLIO

27.24.5 RECENT DEVELOPMENTS

27.25 KAPSAM HEALTH PRODUCTS

27.25.1 COMPANY OVERVIEW

27.25.2 REVENUE ANALYSIS

27.25.3 GEOGRAPHIC PRESENCE

27.25.4 PRODUCT PORTFOLIO

27.25.5 RECENT DEVELOPMENTS

27.26 HALKEY-ROBERTS CORPORATION

27.26.1 COMPANY OVERVIEW

27.26.2 REVENUE ANALYSIS

27.26.3 GEOGRAPHIC PRESENCE

27.26.4 PRODUCT PORTFOLIO

27.26.5 RECENT DEVELOPMENTS

27.27 EIB CO., LTD

27.27.1 COMPANY OVERVIEW

27.27.2 REVENUE ANALYSIS

27.27.3 GEOGRAPHIC PRESENCE

27.27.4 PRODUCT PORTFOLIO

27.27.5 RECENT DEVELOPMENTS

27.28 MEDIPLUS LTD.

27.28.1 COMPANY OVERVIEW

27.28.2 REVENUE ANALYSIS

27.28.3 GEOGRAPHIC PRESENCE

27.28.4 PRODUCT PORTFOLIO

27.28.5 RECENT DEVELOPMENTS

28. RELATED REPORT

29. CONCLUSION

30. QUESTIONNAIRE

31. ABOUT DATA BRIDGE MARKET RESEARCH

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.