Global Network Telemetry Market

Market Size in USD Billion

USD

1.01 Billion

USD

14.03 Billion

2025

2033

USD

1.01 Billion

USD

14.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.01 Billion | |

| USD 14.03 Billion | |

| % | |

|

Network Telemetry Market Overview

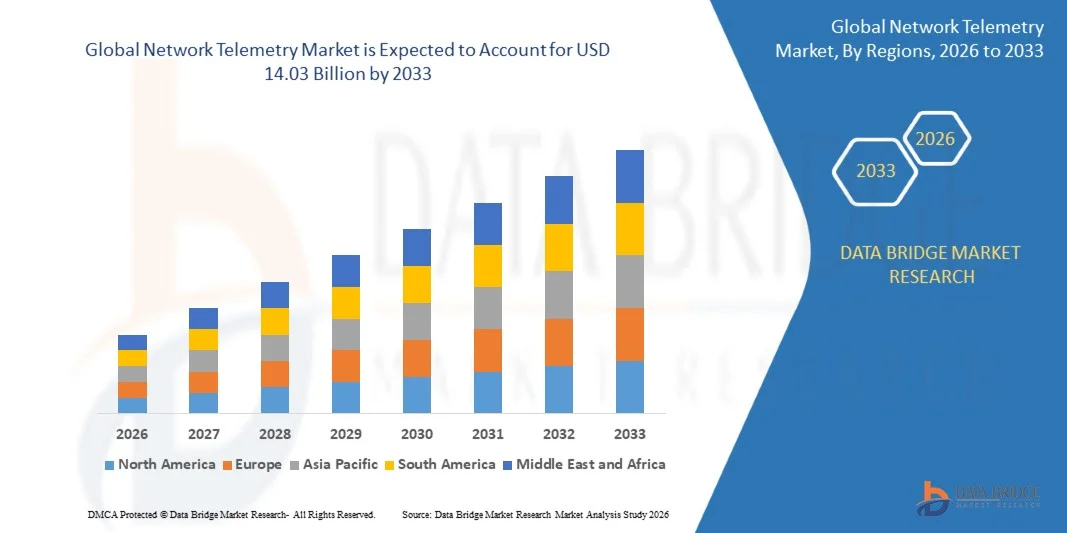

The Network Telemetry Market was valued at USD 1.01 billion in 2025 and is projected to reach USD 14.03 billion by 2033, growing at a CAGR of 39.00% from 2026 to 2033. The market is experiencing rapid growth driven by increasing network complexity, rising adoption of cloud-native architectures, growing deployment of 5G networks, and the need for real-time visibility into network performance, traffic patterns, and security events.

The expansion of hybrid and multi-cloud environments, software-defined networking, and edge computing is increasing the volume and velocity of network data generated across enterprise and service provider infrastructures. Organizations are adopting network telemetry platforms to collect, process, and analyze streaming data from routers, switches, firewalls, and other network devices, enabling proactive fault detection, capacity optimization, and improved service assurance. In addition, rising cybersecurity risks and demand for automated network operations are encouraging enterprises to integrate telemetry solutions with artificial intelligence, machine learning, and network analytics platforms for faster anomaly detection and predictive network management.

Key Market Trends & Insights

- North America dominated the network telemetry market with the largest revenue share of 38.6% in 2025, supported by strong cloud infrastructure, advanced cybersecurity adoption, large-scale data center investments, and growing deployment of network automation platforms across enterprises and telecommunications providers.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 41.8% from 2026 to 2033. Growth is driven by rapid digital transformation, expanding 5G deployment, rising cloud adoption, growing data center capacity, and increasing investment in smart city and industrial IoT infrastructure.

- The Solution segment held the largest market revenue share of approximately 68.4% in 2025 driven by increasing deployment of network monitoring, traffic analytics, performance management, and automated fault detection platforms across enterprise and telecommunications infrastructure. Network telemetry solutions are preferred due to their ability to collect real-time data from routers, switches, firewalls, cloud workloads, and software-defined networks for improved operational visibility and proactive incident management.

- The Services segment is projected to register the fastest growth at a CAGR of 41.2% from 2026 to 2033, driven by increasing demand for consulting, integration, managed telemetry, and support services. Growing complexity of multi-cloud networks and shortage of skilled network operations professionals are accelerating adoption of specialized service offerings for telemetry deployment, data management, and continuous network optimization.

- The Large Enterprises segment held the largest market revenue share of approximately 71.6% in 2025 driven by extensive network infrastructure, high volumes of application traffic, and increasing adoption of cloud, edge, and hybrid IT environments. Large enterprises are investing in advanced telemetry platforms to monitor distributed operations, reduce service disruptions, strengthen cybersecurity monitoring, and automate network management activities across global locations.

- The Small and Medium-Sized Enterprises segment is projected to register the fastest growth at a CAGR of 42.5% from 2026 to 2033, driven by rising adoption of cloud-based telemetry platforms with lower upfront infrastructure requirements. Increasing digital transformation initiatives, remote workforce expansion, and growing dependence on managed network services are supporting telemetry adoption among smaller organizations seeking cost-effective network visibility and performance optimization capabilities.

- The Cloud-Based segment held the largest market revenue share of approximately 62.9% in 2025 driven by increasing adoption of software-as-a-service platforms, multi-cloud environments, and remotely managed enterprise networks. Cloud-based network telemetry platforms enable organizations to scale data collection and analytics capabilities quickly while reducing the need for extensive on-site infrastructure and internal maintenance resources.

- The On-Premise segment is projected to register the fastest growth at a CAGR of 37.8% from 2026 to 2033, driven by rising data sovereignty requirements, cybersecurity concerns, and the need for direct control over telemetry data within highly regulated industries. Financial institutions, government agencies, defense organizations, and large data center operators are increasingly deploying on-premise solutions to support secure monitoring of critical infrastructure and sensitive network environments.

- The Service Providers segment held the largest market revenue share of approximately 58.7% in 2025 driven by rising demand for real-time monitoring of 5G, broadband, cloud connectivity, and software-defined wide area network infrastructure. Telecommunications operators and managed service providers are using telemetry platforms to monitor network capacity, identify service degradation, optimize traffic routing, and improve customer experience across large-scale distributed networks.

- The Verticals segment is projected to register the fastest growth at a CAGR of 40.6% from 2026 to 2033, driven by increasing deployment of telemetry solutions across banking, healthcare, retail, manufacturing, transportation, and government organizations. Rising reliance on connected applications, industrial automation systems, and cloud-based business operations is encouraging vertical industries to adopt network telemetry for improved network resilience, security monitoring, and automated performance management.

Market Size & Forecast

- Global Market Value (2025): USD 1.01 Billion

- Expected Market Value (2033): USD 14.03 Billion

- Forecast CAGR (2026–2033): 39.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Network Telemetry Market Segmentation

|

Attributes |

Network Telemetry Key Market Insights |

|

Segments Covered |

· By Component: Solution and Services · By Organisation Size: Large Enterprises, Small and Medium-Sized Enterprises · By Deployment Type: Cloud-Based and On-Premise · By End User: Service Providers and Verticals |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Cisco Systems, Inc. (U.S.) |

|

Market Opportunities |

• Expansion Of 5G And Edge Computing Networks • Rising Adoption Of AI-Driven Network Operations |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Network Telemetry Market Trends

Trend: Expansion Of AI-Driven Network Observability And Streaming Telemetry

Increasing adoption of cloud-native applications, hybrid infrastructure, 5G connectivity, and distributed enterprise networks is driving demand for real-time network telemetry solutions. Traditional polling-based monitoring tools often provide delayed and limited visibility into network performance, making it difficult for organizations to identify congestion, packet loss, latency, configuration issues, and security anomalies across highly dynamic environments. As a result, enterprises and service providers are shifting toward streaming telemetry platforms that continuously collect structured operational data from routers, switches, firewalls, cloud workloads, and application environments.

In modern enterprise networks, organizations are integrating telemetry data with artificial intelligence and machine learning platforms to automate anomaly detection, root-cause analysis, and incident prioritization. For instance, Cisco reported in 2025 that its internal IT organization unified telemetry data across a network containing hundreds of thousands of assets, enabling automation to handle 99.998% of alerts and supporting zero major incidents. Streaming telemetry architectures also enable network teams to analyze CPU utilization, memory usage, interface statistics, and traffic behavior continuously rather than relying on periodic manual checks.

The rapid growth of containerized applications and AI workloads is further increasing telemetry volumes and the need for standardized observability frameworks. OpenTelemetry became a graduated Cloud Native Computing Foundation project in 2026 and had more than 28,000 contributors, reflecting strong industry momentum toward interoperable telemetry collection across logs, metrics, and traces. In addition, 82% of container users reported running Kubernetes in production in 2025, increasing the need for continuous monitoring of distributed application and network environments.

Network Telemetry Market Dynamics

Key Market Driver: Rising Need For Real-Time Network Visibility And Automated Operations

Organizations worldwide are facing growing operational pressure to maintain high network availability, reduce downtime, improve user experience, and secure increasingly complex digital infrastructure. The expansion of multi-cloud deployments, remote work environments, software-defined wide area networks, and connected devices is generating large volumes of network data that cannot be efficiently managed through conventional manual monitoring processes. This is creating strong demand for telemetry solutions capable of delivering continuous and granular visibility into network behavior.

Enterprises and telecommunications providers are increasingly deploying model-driven streaming telemetry to collect operational data directly from network devices and transmit it to centralized analytics platforms. For instance, Cisco’s telemetry framework enables organizations to subscribe to specific sensor paths and stream structured operational data to remote management systems for proactive monitoring, predictive troubleshooting, and network automation. This supports faster identification of utilization bottlenecks, abnormal traffic patterns, and infrastructure failures before they affect business operations.

Similarly, the adoption of artificial intelligence for IT operations is accelerating demand for high-quality telemetry data that can train anomaly detection and predictive analytics models. A 2026 observability survey covering 1,363 respondents across 76 countries found that 92% of organizations see value in using AI to surface anomalies before they result in downtime, while 77% reported time or cost savings through centralized observability. These trends are encouraging enterprises to consolidate network, application, and infrastructure telemetry into unified operational platforms.

Key Restraint/Challenge: Data Volume Complexity And Integration Challenges

Network telemetry platforms generate substantial volumes of high-frequency data, particularly in large-scale cloud, telecom, and data center environments. Collecting, storing, processing, and analyzing telemetry from thousands of network devices, applications, and endpoints can increase infrastructure costs and create data management challenges. Organizations must also ensure that telemetry pipelines maintain low latency and high reliability while preventing excessive data duplication and storage consumption.

In addition, integration complexity remains a major challenge because many enterprises operate multi-vendor network environments that combine legacy equipment with modern cloud-native infrastructure. Differences in telemetry protocols, data models, interfaces, and device capabilities can make it difficult to establish a consistent and unified monitoring architecture. Organizations may need to continue using traditional SNMP monitoring, APIs, and proprietary tools alongside streaming telemetry, increasing operational complexity.

A February 2026 survey of 407 cloud-native practitioners found that 46.7% of organizations operated two to three observability tools in parallel, while only 7.4% had achieved a unified observability environment. The same survey identified dashboard and alert configuration as the leading setup challenge for 54% of respondents, followed by integration complexity for 46.4%. These findings indicate that organizations continue to face implementation and operational barriers despite growing availability of open telemetry standards.

Key Market Opportunity: Integration With 5G Edge Computing And Cloud-Native Networks

The expansion of 5G networks, edge computing infrastructure, and cloud-native applications is creating significant opportunities for network telemetry providers. These environments require real-time monitoring because service quality depends on low latency, dynamic traffic routing, and reliable connectivity across distributed locations. Traditional monitoring systems are often unable to provide the speed and granularity needed to manage network slices, edge nodes, virtualized network functions, and rapidly changing application workloads.

Telecommunications operators are increasingly using telemetry platforms to monitor network performance indicators, such as bandwidth utilization, packet delay, jitter, and service availability, across 5G and edge infrastructure. For instance, streaming telemetry can support proactive capacity planning and automated traffic optimization by continuously identifying congestion patterns across core, transport, and access networks. This enables operators to improve service assurance for enterprise connectivity, connected vehicles, industrial automation, and smart city applications.

In addition, the growing use of Kubernetes and microservices is increasing demand for telemetry solutions that correlate network data with application traces and infrastructure metrics. The Cloud Native Computing Foundation reported that 82% of container users were running Kubernetes in production during 2025, while OpenTelemetry emerged as the second-highest-velocity Cloud Native Computing Foundation project with more than 24,000 contributors. These developments are creating opportunities for telemetry vendors to provide integrated platforms that support automated network operations, AI-assisted troubleshooting, and end-to-end observability across cloud and edge environments.

Network Telemetry Market Scope

The market is segmented on the basis of component, organisation size, deployment type, and end user.

- By Component

On the basis of component, the network telemetry market is segmented into Solution and Services. The Solution segment held the largest market revenue share of approximately 68.4% in 2025 driven by increasing deployment of network monitoring, traffic analytics, performance management, and automated fault detection platforms across enterprise and telecommunications infrastructure. Network telemetry solutions are preferred due to their ability to collect real-time data from routers, switches, firewalls, cloud workloads, and software-defined networks for improved operational visibility and proactive incident management.

The Services segment is projected to register the fastest growth at a CAGR of 41.2% from 2026 to 2033, driven by increasing demand for consulting, integration, managed telemetry, and support services. Growing complexity of multi-cloud networks and shortage of skilled network operations professionals are accelerating adoption of specialized service offerings for telemetry deployment, data management, and continuous network optimization.

- By Organisation Size

On the basis of organisation size, the network telemetry market is segmented into Large Enterprises and Small and Medium-Sized Enterprises. The Large Enterprises segment held the largest market revenue share of approximately 71.6% in 2025 driven by extensive network infrastructure, high volumes of application traffic, and increasing adoption of cloud, edge, and hybrid IT environments. Large enterprises are investing in advanced telemetry platforms to monitor distributed operations, reduce service disruptions, strengthen cybersecurity monitoring, and automate network management activities across global locations.

The Small and Medium-Sized Enterprises segment is projected to register the fastest growth at a CAGR of 42.5% from 2026 to 2033, driven by rising adoption of cloud-based telemetry platforms with lower upfront infrastructure requirements. Increasing digital transformation initiatives, remote workforce expansion, and growing dependence on managed network services are supporting telemetry adoption among smaller organizations seeking cost-effective network visibility and performance optimization capabilities.

- By Deployment Type

On the basis of deployment type, the network telemetry market is segmented into Cloud-Based and On-Premise. The Cloud-Based segment held the largest market revenue share of approximately 62.9% in 2025 driven by increasing adoption of software-as-a-service platforms, multi-cloud environments, and remotely managed enterprise networks. Cloud-based network telemetry platforms enable organizations to scale data collection and analytics capabilities quickly while reducing the need for extensive on-site infrastructure and internal maintenance resources.

The On-Premise segment is projected to register the fastest growth at a CAGR of 37.8% from 2026 to 2033, driven by rising data sovereignty requirements, cybersecurity concerns, and the need for direct control over telemetry data within highly regulated industries. Financial institutions, government agencies, defense organizations, and large data center operators are increasingly deploying on-premise solutions to support secure monitoring of critical infrastructure and sensitive network environments.

- By End User

On the basis of end user, the network telemetry market is segmented into Service Providers and Verticals. The Service Providers segment held the largest market revenue share of approximately 58.7% in 2025 driven by rising demand for real-time monitoring of 5G, broadband, cloud connectivity, and software-defined wide area network infrastructure. Telecommunications operators and managed service providers are using telemetry platforms to monitor network capacity, identify service degradation, optimize traffic routing, and improve customer experience across large-scale distributed networks.

The Verticals segment is projected to register the fastest growth at a CAGR of 40.6% from 2026 to 2033, driven by increasing deployment of telemetry solutions across banking, healthcare, retail, manufacturing, transportation, and government organizations. Rising reliance on connected applications, industrial automation systems, and cloud-based business operations is encouraging vertical industries to adopt network telemetry for improved network resilience, security monitoring, and automated performance management.

Network Telemetry Market Regional Analysis

North America Network Telemetry Market Insight

North America dominated the network telemetry market with the largest revenue share of 38.6% in 2025, supported by high adoption of cloud computing, software-defined networking, artificial intelligence, and advanced cybersecurity platforms across enterprises and telecommunications providers. Organizations in the region are increasingly investing in real-time network monitoring and analytics solutions to improve infrastructure visibility, reduce downtime, and manage growing volumes of network traffic. The presence of major cloud service providers, network equipment manufacturers, and technology companies is further supporting deployment of streaming telemetry platforms across enterprise, data center, and service provider environments.

U.S. Network Telemetry Market Insight

The U.S. network telemetry market captured the largest revenue share in 2025 within North America, fueled by rapid expansion of hybrid cloud infrastructure, large-scale data centers, and AI-driven enterprise applications. Organizations are increasingly prioritizing continuous monitoring of network performance, security events, and application traffic to maintain service availability and improve customer experience. The growing adoption of network automation, zero-trust security frameworks, and observability platforms is further propelling the market. Moreover, increasing investment in 5G infrastructure and edge computing is significantly contributing to demand for advanced network telemetry solutions.

Europe Network Telemetry Market Insight

The Europe network telemetry market is expected to witness significant growth from 2026 to 2033, primarily driven by rising adoption of cloud-based business operations, increasing cybersecurity concerns, and strict data protection requirements. Enterprises across the region are deploying network telemetry platforms to strengthen operational resilience, monitor distributed infrastructure, and improve compliance with data governance standards. The expansion of digital services, industrial automation, and connected enterprise networks is fostering demand for real-time traffic analytics and automated network performance management across financial services, manufacturing, healthcare, and government sectors.

U.K. Network Telemetry Market Insight

The U.K. network telemetry market is expected to witness strong growth from 2026 to 2033, driven by rising adoption of multi-cloud environments, remote work infrastructure, and advanced cybersecurity technologies. Organizations are increasingly deploying telemetry solutions to monitor application performance, identify abnormal network behavior, and reduce the impact of service disruptions. The U.K.’s expanding financial technology, telecommunications, and digital services sectors are supporting demand for automated network observability platforms. In addition, increasing investment in 5G connectivity and cloud data centers is expected to continue stimulating market growth.

Germany Network Telemetry Market Insight

The Germany network telemetry market is expected to witness strong growth from 2026 to 2033, fueled by increasing digitalization across industrial manufacturing, automotive, logistics, and enterprise sectors. Germany’s advanced industrial infrastructure and growing adoption of Industry 4.0 technologies are encouraging organizations to deploy network telemetry solutions for monitoring connected production systems, industrial IoT devices, and cloud-integrated operations. The increasing focus on data security, operational reliability, and compliance with European data protection regulations is also supporting demand for secure and privacy-focused network monitoring platforms.

Asia-Pacific Network Telemetry Market Insight

The Asia-Pacific network telemetry market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid digital transformation, expanding 5G deployment, rising cloud adoption, and increasing investment in smart city infrastructure. Countries such as China, Japan, India, South Korea, and Singapore are experiencing significant growth in data center capacity, connected device deployment, and enterprise digitization, creating demand for real-time network visibility and performance management solutions. The region’s growing telecommunications industry and expanding cloud service ecosystem are further improving the accessibility and adoption of network telemetry platforms across large enterprises and small and medium-sized organizations.

Japan Network Telemetry Market Insight

The Japan network telemetry market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced technology infrastructure, high adoption of connected devices, and increasing investment in cloud and edge computing. Japanese organizations are focusing on improving network reliability and security across manufacturing facilities, financial institutions, telecommunications networks, and smart building environments. The growing deployment of industrial IoT systems and automation technologies is increasing demand for telemetry platforms capable of monitoring network traffic, device performance, and operational anomalies in real time. Moreover, Japan’s aging workforce is encouraging enterprises to adopt network automation tools that reduce manual monitoring requirements.

China Network Telemetry Market Insight

The China network telemetry market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid expansion of cloud infrastructure, large-scale 5G network deployment, and growing investment in digital transformation initiatives. China is one of the largest markets for telecommunications equipment, data centers, and connected enterprise technologies, increasing the need for advanced network monitoring and analytics platforms. The expansion of smart cities, industrial internet applications, and cloud-based business operations is encouraging organizations to deploy telemetry solutions for traffic optimization, security monitoring, and automated network management. Strong domestic technology providers and increasing adoption of AI-enabled network operations are key factors propelling market growth in China.

Network Telemetry Market Share

The Network Telemetry industry is primarily led by well-established companies, including:

• Cisco Systems, Inc. (U.S.)

• Juniper Networks, Inc. (U.S.)

• Arista Networks, Inc. (U.S.)

• Palo Alto Networks, Inc. (U.S.)

• Hewlett Packard Enterprise Development LP (U.S.)

• IBM Corporation (U.S.)

• Accenture plc (Ireland)

• Capgemini SE (France)

• Infosys Limited (India)

• Wipro Limited (India)

• HCL Technologies Limited (India)

• Tata Consultancy Services Limited (India)

• Genpact Limited (U.S.)

• VOLANSYS Technologies (U.S.)

• Pluribus Networks, Inc. (U.S.)

Latest Developments in Network Telemetry Market

- In January 2025, Corelight expanded its network detection and response capabilities by integrating Microsoft Defender for Endpoint and Microsoft Defender Vulnerability Management insights with its sensor platform. The development is expected to provide risk-prioritized telemetry alerts, enabling security teams to identify critical vulnerabilities and threats more efficiently while supporting wider adoption of integrated network telemetry platforms

- In 2025, Hewlett Packard Enterprise developed scalable network telemetry platforms integrated with artificial intelligence and intent-based networking capabilities. The platform is designed to support autonomous network management, predictive maintenance, and faster fault resolution, strengthening demand for AI-enabled telemetry solutions across enterprise and service provider networks

- In October 2024, Lekha Wireless and NewSpace collaborated to launch 4G and 5G-enabled uncrewed aerial systems. The development enables high-speed transmission of video streams, telemetry data, and control commands, expanding network telemetry applications across defense, surveillance, industrial inspection, and autonomous aerial operations

- In August 2024, Netscout introduced Omnis AI Insights to provide enterprises with AI-ready network telemetry data without requiring extensive data transformation. The solution is expected to improve AIOps implementation, support faster operational decision-making, and increase demand for high-quality network data analytics platforms

- In April 2024, Wyebot integrated its Wireless Intelligence Platform with Cisco Catalyst Center using Cisco telemetry data and application programming interfaces. The integration enhances Wi-Fi network automation, improves visibility into wireless performance issues, and supports growing adoption of telemetry-driven network management across enterprise environments

- In 2023, Nokia expanded its network telemetry portfolio with 5G-specific monitoring tools offering high-frequency data collection, real-time traffic analysis, and advanced fault detection. The development is expected to strengthen service assurance capabilities for telecommunications operators and accelerate deployment of telemetry solutions across 5G infrastructure

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.