Global Neurocutaneous Syndromes Market

Market Size in USD Billion

USD

16.20 Billion

USD

27.01 Billion

2024

2032

USD

16.20 Billion

USD

27.01 Billion

2024

2032

| 2025 - 2032 | |

| USD 16.20 Billion | |

| USD 27.01 Billion | |

| % | |

|

Neurocutaneous Syndromes Market Size

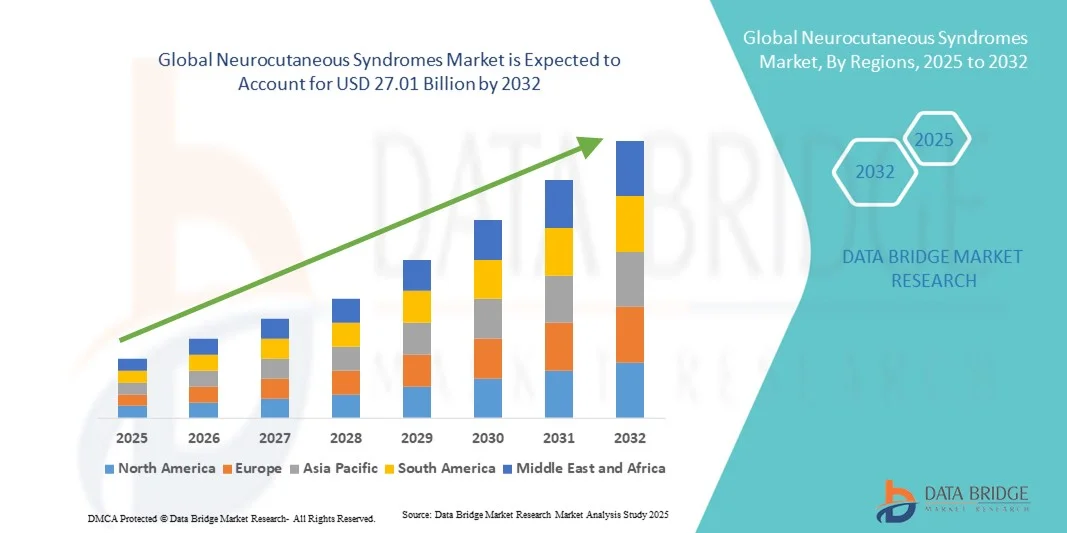

- The global neurocutaneous syndromes market size was valued at USD 16.20 billion in 2024 and is expected to reach USD 27.01billion by 2032, at a CAGR of 6.60% during the forecast period

- The market growth is largely driven by the increasing prevalence of neurocutaneous syndromes such as neurofibromatosis, tuberous sclerosis, and Sturge-Weber syndrome, coupled with rising advancements in genetic testing and neuroimaging technologies that facilitate early diagnosis and treatment

- Furthermore, growing research initiatives focused on understanding the genetic and molecular mechanisms underlying these disorders, along with increasing availability of targeted therapies and multidisciplinary management approaches, are significantly propelling the growth of the neurocutaneous syndromes market

Neurocutaneous Syndromes Market Analysis

- Neurocutaneous syndromes, a group of rare genetic disorders affecting both the nervous system and skin, are becoming an important focus area in neurology and genetic medicine due to their complex manifestations and lifelong management needs

- The growing recognition of these disorders, coupled with advances in molecular diagnostics and neuroimaging, is driving earlier detection and better treatment outcomes for patients across various regions

- North America dominated the neurocutaneous syndromes market with the largest revenue share of 40% in 2024, supported by advanced healthcare infrastructure, a strong presence of research institutions, and significant investments in genetic testing and novel therapeutics. The U.S. continues to lead the region owing to growing awareness programs and improved access to precision medicine

- Asia-Pacific is expected to be the fastest-growing region in the neurocutaneous syndromes market during the forecast period, projected to register a CAGR of 11.5%, fueled by increasing healthcare expenditure, expanding diagnostic access, and government initiatives to address rare genetic disorders

- The Magnetic Resonance Imaging (MRI) segment dominated the largest market revenue share of 45.6% in 2024, attributed to its superior imaging capabilities and critical diagnostic role in neurological manifestations. MRI provides detailed visualization of brain and nerve abnormalities, enabling accurate diagnosis and surgical planning. Its non-invasive and radiation-free nature makes it suitable for repeated assessments, particularly in pediatric cases

Report Scope and Neurocutaneous Syndromes Market Segmentation

|

Attributes |

Neurocutaneous Syndromes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Neurocutaneous Syndromes Market Trends

Rising Integration of Artificial Intelligence and Precision Diagnostics

- A significant and accelerating trend in the global neurocutaneous syndromes market is the deepening integration with artificial intelligence (AI) and data-driven clinical technologies. This integration enhances diagnostic accuracy, treatment monitoring, and patient-specific therapy planning for conditions such as Tuberous Sclerosis Complex (TSC), Neurofibromatosis (NF), and Sturge-Weber syndrome

- For instance, in June 2023, Arbor Pharmaceuticals announced the expansion of its AI-supported diagnostic algorithm for Tuberous Sclerosis Complex in partnership with rare disease research centers to enable early identification of neurocutaneous manifestations using imaging data

- AI-driven solutions are improving real-time interpretation of MRI and CT scans, allowing for faster detection of neurological lesions and vascular abnormalities. Moreover, machine learning platforms are supporting clinicians in mapping gene–phenotype relationships that inform treatment plans

- These advancements are particularly crucial in rare disorders where symptom variability is high and early detection greatly affects prognosis. Integrating AI tools in diagnosis and monitoring also allows healthcare providers to make more accurate treatment adjustments and track patient progress

- In addition, AI-supported telehealth platforms are enhancing patient management by enabling continuous remote assessment and timely intervention, particularly for those in regions with limited access to neurogenetic specialists

- This convergence of AI technology with precision diagnostics is reshaping the landscape of neurocutaneous disorder management and is expected to drive innovation and investment in the coming years

Neurocutaneous Syndromes Market Dynamics

Driver

Growing Need Due to Rising Disease Awareness and Advancements in Genetic Diagnostics

- The increasing global awareness of rare neurocutaneous conditions and the growing adoption of advanced genetic and molecular testing methods are driving the market. These technologies enable earlier and more accurate diagnosis, resulting in improved patient outcomes

- For instance, in April 2024, Ultragenyx Pharmaceutical Inc. partnered with GeneDx to expand access to whole-exome sequencing programs aimed at early detection of rare neurocutaneous disorders such as Neurofibromatosis Type 1 and Tuberous Sclerosis

- The rising emphasis on patient registries and international data-sharing collaborations further strengthens understanding of disease prevalence and response to therapies. Governments and non-profit organizations are investing in rare disease awareness programs to promote early intervention

- Moreover, biopharmaceutical firms are focusing on targeted therapies addressing underlying molecular mechanisms rather than symptomatic treatment, a shift that significantly enhances therapeutic precision

- These efforts are supported by increasing clinical research funding and improved infrastructure for genetic counseling and testing, particularly in North America and Europe

- As diagnostic technologies become more cost-effective and widely available, early identification and treatment are expected to improve substantially, further boosting the market growth trajectory

Restraint/Challenge

High Cost of Therapies and Limited Accessibility in Emerging Markets

- Despite scientific advances, high treatment costs and limited availability of specialized care centers remain significant barriers to adoption in developing regions. Complex treatment protocols involving biologics, surgical interventions, or long-term pharmacotherapy pose affordability challenges

- For instance, in March 2022, Novartis AG announced pricing challenges associated with its everolimus-based therapy for Tuberous Sclerosis Complex in lower-income countries, highlighting global disparities in access to neurocutaneous disorder treatments

- These affordability constraints often lead to delayed or suboptimal care, especially where healthcare insurance coverage for rare diseases is limited

- In addition, the lack of skilled specialists, neuroimaging facilities, and genomic diagnostic labs in low-resource settings exacerbates delayed diagnosis and management

- Efforts to reduce therapy costs through tiered pricing, patient access programs, and local manufacturing partnerships are being explored but remain insufficient in many regions

- Addressing these financial and infrastructural limitations is essential for achieving equitable global access to treatment and ensuring sustainable growth of the neurocutaneous syndromes market

Neurocutaneous Syndromes Market Scope

The market is segmented on the basis of type, diagnosis, treatment, and end user.

- By Type

On the basis of type, the Neurocutaneous Syndromes market is segmented into Tuberous Sclerosis (TS), Neurofibromatosis (NF), Sturge-Weber Syndrome, Ataxia-Telangiectasia (A-T), Von Hippel-Lindau Disease (VHL), and Others. The Neurofibromatosis (NF) segment dominated the largest market revenue share of 38.5% in 2024, supported by its higher prevalence, established clinical guidelines, and robust diagnostic infrastructure. NF’s management requires multidisciplinary follow-up, genetic testing, and imaging, driving significant healthcare spending. Pharmaceutical research targeting NF1-related tumors and pain management contributes further to demand. Enhanced patient registries and growing specialist centers worldwide sustain consistent diagnostic and therapeutic uptake. Reimbursement support for NF-targeted interventions in developed regions further boosts revenue share. Public awareness programs and early screening initiatives increase patient identification and healthcare engagement. Integration of telemedicine and clinical decision platforms enhances care continuity. Collaboration between academic institutions and advocacy groups improves access to clinical trials and innovative therapies. The large patient base and established treatment pathways reinforce NF’s market dominance.

The Tuberous Sclerosis (TS) segment is expected to witness the fastest CAGR of 18.2% from 2025 to 2032, driven by advances in genetic testing and targeted therapies such as mTOR inhibitors. Rising pediatric screening and awareness initiatives lead to early diagnosis and long-term monitoring. Expanding clinical use of precision medicine tools and newborn screening programs is fueling adoption of TS-related diagnostics. Continuous clinical research in epilepsy management and tumor control contributes to growing treatment uptake. Increasing government funding for rare neurological disorders promotes accessibility to specialized centers. Integration of multidisciplinary care models combining neurology, nephrology, and genetics enhances patient outcomes. Broader regional availability of TS-specific genetic panels accelerates diagnosis rates. Growing collaboration among biotech firms and hospitals fosters innovation in targeted therapeutics. Rising prevalence awareness through patient advocacy drives faster adoption across developed and emerging regions. Combined, these drivers are projected to deliver strong and sustained market expansion for TS.

- By Diagnosis

On the basis of diagnosis, the Neurocutaneous Syndromes market is segmented into Skull Radiography, Magnetic Resonance Imaging (MRI), Computed Tomography (CT) Scan, Electroencephalogram (EEG), Genetic Tests (Blood Testing), Biopsy, and Others. The Magnetic Resonance Imaging (MRI) segment dominated the largest market revenue share of 45.6% in 2024, attributed to its superior imaging capabilities and critical diagnostic role in neurological manifestations. MRI provides detailed visualization of brain and nerve abnormalities, enabling accurate diagnosis and surgical planning. Its non-invasive and radiation-free nature makes it suitable for repeated assessments, particularly in pediatric cases. The proliferation of high-resolution and functional MRI technologies enhances clinical decision-making. Increasing investments in hospital imaging infrastructure and radiology capacity expansion support strong adoption. Integration with artificial intelligence (AI) for image analysis is improving diagnostic precision. MRI’s vital role in monitoring disease progression and post-treatment outcomes further reinforces its market leadership. Hospitals and diagnostic centers increasingly rely on MRI as the first-line modality in syndromic evaluation. The broad clinical applications and diagnostic reliability continue to sustain its revenue share.

The Genetic Tests (Blood Testing) segment is expected to witness the fastest CAGR of 15.4% from 2025 to 2032, fueled by technological advancement and declining sequencing costs. Expanded understanding of the genetic origins of neurocutaneous disorders drives clinicians toward early genetic confirmation. Adoption of next-generation sequencing (NGS) panels enables precise identification of pathogenic variants. Broader insurance coverage and favorable reimbursement policies increase patient access to testing. Integration of genetic counseling services with testing centers enhances care personalization. Growing patient and physician awareness of gene-based therapies encourages earlier testing. Partnerships between biotech firms and laboratories strengthen innovation pipelines. The increasing use of liquid biopsy and home-based testing kits supports accessibility in remote regions. Public health programs focusing on rare-disease genomics further accelerate adoption. Overall, the clinical importance and affordability of genetic testing make it the fastest-growing diagnostic category in this market.

- By Treatment

On the basis of treatment, the Neurocutaneous Syndromes market is segmented into Medication, Laser Therapy, Surgical Procedures, and Others. The Medication segment held the largest market revenue share of 40.1% in 2024, driven by long-term pharmacologic management of seizures, tumors, and dermatologic manifestations. The widespread use of mTOR inhibitors, anti-seizure drugs, and supportive medications underpins consistent demand. Pharmaceutical companies continue to expand label indications for NF and TS-related conditions. Reimbursement frameworks supporting chronic medication therapies bolster accessibility. Continuous R&D investment in rare neurological disease drugs sustains innovation momentum. Medication-based treatment remains the first-line approach for many neurocutaneous manifestations. Patient adherence programs and telehealth-based prescription monitoring enhance continuity of care. Combination regimens integrating medication with surgical or laser interventions also add to therapy uptake. Availability of generics for certain agents increases affordability, expanding patient reach. Thus, medication remains the foundation of therapeutic management and revenue generation.

The Laser Therapy segment is projected to witness the fastest CAGR of 14.8% from 2025 to 2032, driven by its rising role in treating visible skin lesions and vascular abnormalities. Advancements in pulsed dye and fractional laser technologies are improving clinical outcomes and patient satisfaction. Increasing dermatologic adoption for cosmetic and functional improvement boosts utilization. The shift toward outpatient and aesthetic settings enhances procedure accessibility. Growing insurance coverage for medically indicated laser therapy supports patient affordability. Laser therapy’s minimally invasive nature and quick recovery profile attract patient preference. Expansion of dermatology centers equipped with advanced laser systems drives procedural volumes. Integration of image-guided systems and portable devices supports personalized treatment. Combination use with pharmacologic agents enhances overall therapeutic efficacy. Continuous device innovation by manufacturers further contributes to adoption growth across global markets.

- By End User

On the basis of end user, the Neurocutaneous Syndromes market is segmented into Hospitals and Clinics, Diagnostic Centres, and Others. The Hospitals and Clinics segment dominated the largest market revenue share of 62.3% in 2024, attributed to their multidisciplinary infrastructure and capacity to manage complex cases. Hospitals serve as the primary centers for diagnosis, imaging, genetic testing, and long-term treatment. Presence of specialized departments such as neurology, dermatology, and genetics strengthens integrated care. Large patient footfall and referral systems support steady revenue flow. Institutional partnerships with pharmaceutical and diagnostic firms enhance service offerings. Hospitals also act as research hubs for rare disease trials and new therapy evaluations. The availability of advanced imaging systems, surgical capabilities, and in-house laboratories supports comprehensive care delivery. Government and private funding in rare disease centers further strengthen hospital dominance. The concentration of skilled specialists and advanced equipment ensures hospitals remain key end users in this market.

The Diagnostic Centres segment is expected to witness the fastest CAGR of 13.9% from 2025 to 2032, driven by the expansion of specialized outpatient diagnostic services. Standalone diagnostic centers are increasingly offering MRI, CT, EEG, and genetic testing with reduced turnaround time. Their accessibility, affordability, and faster scheduling attract both patients and referring physicians. Rising investments in digital platforms, AI-driven diagnostics, and tele-reporting solutions enhance efficiency. Growth in rare-disease screening programs and clinical collaborations expands service demand. Integration of counseling and follow-up services fosters patient retention. These centers are also entering public-private partnerships to improve regional diagnostic outreach. The trend toward decentralizing diagnostic services from hospitals to outpatient facilities further accelerates growth. As awareness increases and technology costs decline, diagnostic centers will play a key role in supporting rapid, accurate, and cost-effective testing services across the Neurocutaneous Syndromes landscape.

Neurocutaneous Syndromes Market Regional Analysis

- North America dominated the neurocutaneous syndromes market with the largest revenue share of 40% in 2024, supported by advanced healthcare infrastructure, a strong presence of research institutions, and significant investments in genetic testing and novel therapeutics

- The growing emphasis on early diagnosis of rare genetic disorders and an increasing number of awareness programs are further strengthening regional growth

- Moreover, collaboration between academic research centers and pharmaceutical companies is accelerating innovation and clinical trial activity in this space

U.S. Neurocutaneous Syndromes Market Insight

The U.S. neurocutaneous syndromes market accounted for the largest revenue share in 2024 within North America, driven by improved access to precision medicine and the growing availability of advanced genetic testing technologies. Substantial investments in rare disease research, along with supportive policies from organizations such as the NIH and FDA for orphan drug development, are fostering market growth. The presence of leading biotech companies and research initiatives focused on Tuberous Sclerosis and Neurofibromatosis are also fueling therapeutic advancements in the country.

Europe Neurocutaneous Syndromes Market Insight

The Europe neurocutaneous syndromes market is projected to register steady growth throughout the forecast period, driven by the region’s strong emphasis on clinical research, patient registries, and early diagnostic programs for rare genetic conditions. The increasing prevalence of neurocutaneous disorders and rising adoption of molecular diagnostics in hospitals and research labs are propelling market expansion. European healthcare systems are also witnessing increased collaboration between patient advocacy groups and pharmaceutical firms to enhance awareness and treatment access.

U.K. Neurocutaneous Syndromes Market Insight

The U.K. neurocutaneous syndromes market is expected to grow at a noteworthy CAGR during the forecast period, supported by the National Health Service’s (NHS) focus on genomic medicine and rare disease research. The expansion of nationwide genetic testing programs and partnerships with biopharmaceutical innovators are contributing to market advancement. Rising awareness about neurocutaneous conditions and improved patient support frameworks are also fostering diagnosis and treatment uptake.

Germany Neurocutaneous Syndromes Market Insight

The Germany neurocutaneous syndromes market is poised to grow at a significant CAGR, driven by advancements in molecular diagnostics, expanding healthcare R&D investment, and a robust biotechnology sector. Germany’s strong focus on personalized medicine and clinical innovation supports early detection and targeted therapy development for conditions like Tuberous Sclerosis and Von Hippel-Lindau Disease. Additionally, government-backed funding initiatives for rare diseases are creating favorable conditions for long-term market growth.

Asia-Pacific Neurocutaneous Syndromes Market Insight

The Asia-Pacific neurocutaneous syndromes market is anticipated to grow at the fastest CAGR of 11.5% during the forecast period (2025–2032), fueled by increasing healthcare expenditure, expanding diagnostic access, and government initiatives addressing rare genetic disorders. Rapid advancements in genomic sequencing technologies and improved healthcare infrastructure in countries such as China, Japan, and India are enhancing early diagnosis rates. Moreover, the growing involvement of regional biotech companies in research collaborations is expected to boost therapeutic innovation.

Japan Neurocutaneous Syndromes Market Insight

The Japan neurocutaneous syndromes market is expanding steadily due to the country’s strong adoption of advanced diagnostic technologies and its commitment to precision healthcare. Government-backed rare disease initiatives, combined with a high level of clinical research activity, are driving the detection and management of neurocutaneous conditions. Japan’s rapidly aging population and technological leadership in medical imaging and genetics are expected to further stimulate market growth.

China Neurocutaneous Syndromes Market Insight

The China neurocutaneous syndromes market accounted for the largest revenue share in Asia-Pacific in 2024, driven by rapid healthcare modernization, increasing awareness of genetic disorders, and expanding access to advanced diagnostics. The country’s strong biotechnology ecosystem, supported by public and private sector investment, is promoting the development of innovative therapies. Additionally, the establishment of national rare disease registries and screening programs is improving patient identification and treatment outcomes.

Neurocutaneous Syndromes Market Share

The Neurocutaneous Syndromes industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- GSK plc (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Biogen Inc. (U.S.)

Latest Developments in Global Neurocutaneous Syndromes Market

- In April 2022, the U.S. Food & Drug Administration (FDA) approved HYFTOR (sirolimus topical gel) 0.2% for the treatment of facial angiofibromas in adult and pediatric patients (6 years and older) with Tuberous Sclerosis Complex (TSC). This approval marked the first topical therapy specifically indicated for TSC-related skin lesions, enhancing treatment options for patients

- In May 2024, Marinus Pharmaceuticals, Inc. announced completion of enrolment in its pivotal Phase 3 TRUST-TSC trial evaluating ganaxolone oral suspension CV for the treatment of seizures associated with TSC in children and adults. This development represents an important milestone toward addressing unmet neurological needs within the TSC population

- In September 2024, Marinus Pharmaceuticals announced that it was preparing commercial launch readiness for ganaxolone (ZTALMY) in TSC and CDKL5 deficiency disorder indications, including expanded manufacturing capacity to support expected demand following regulatory submission

- In January 2025, the FDA granted final approval to generic everolimus tablets for oral suspension for use in patients aged 1 year and older with TSC-associated subependymal giant cell astrocytoma (SEGA) that cannot be curatively resected. This approval broadens access to an essential targeted therapy for managing tumor-related complications in TSC

- In February 2025, the National Institute for Health and Care Excellence (NICE) in England agreed to fund Fintepla (fenfluramine) for treatment of seizures in patients with TSC. This reimbursement decision expands access to an important anti-seizure medication for eligible patients in the UK, reinforcing global therapeutic adoption

- In February 2025, major advocacy and research groups highlighted new progress in Neurofibromatosis Type 1 (NF1) research, including initiation of an AI-driven NF drug discovery trial and expanded patient enrolment across international clinical centers. This marked a key milestone in leveraging technology for rare disease innovation and accelerating potential treatment pipelines

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.