Global Neurosurgical Devices Market

Market Size in USD Billion

USD

15.25 Billion

USD

33.29 Billion

2025

2033

USD

15.25 Billion

USD

33.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 15.25 Billion | |

| USD 33.29 Billion | |

| % | |

|

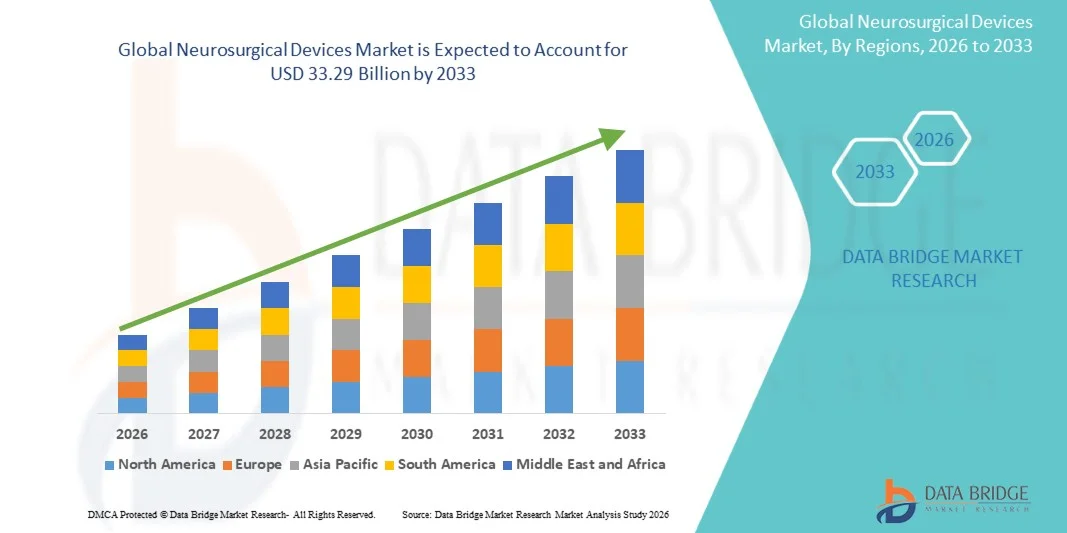

Neurosurgical Devices Market Size

- The global Neurosurgical Devices market size was valued at USD 15.25 billion in 2025 and is expected to reach USD 33.29 billion by 2033, at a CAGR of 10.25% during the forecast period.

- Market growth is primarily driven by the escalating global prevalence of neurological disorders — including Parkinson's disease, Alzheimer's disease, epilepsy, brain tumors, and cerebrovascular conditions — coupled with the rapid adoption of robotic-assisted neurosurgery, AI-powered intraoperative navigation, and expanding demand for minimally invasive cranial and spinal interventions.

- Additionally, favorable government healthcare spending initiatives, growing investments in neurology center infrastructure across emerging economies, rising geriatric population susceptibility to neurodegenerative conditions, and continuous innovation in device miniaturization, biocompatible implants, and real-time neuro-monitoring technologies are collectively supporting robust global market expansion.

Neurosurgical Devices Market Analysis

- Neurosurgical devices encompass a broad range of high-precision medical instruments, implants, and technology systems — including neurostimulation devices, neurointerventional devices, navigation systems, CSF management tools, power tools, and endoscopes — designed to diagnose, treat, and surgically manage disorders of the brain, spinal cord, and peripheral nervous system.

- The growing demand for neurosurgical devices is driven by rising neurological disease burden globally, the increasing shift toward minimally invasive and endoscopic neurosurgical approaches, growing deep brain stimulation (DBS) adoption for Parkinson's disease and treatment-resistant epilepsy, expanding cerebrovascular intervention volumes, and the integration of AI and robotics into neurosurgical workflows.

- North America dominated the Neurosurgical Devices market with a share of 40.67% in 2025, supported by a well-established neurology care ecosystem, advanced hospital infrastructure, strong reimbursement frameworks for complex neurosurgical procedures, high adoption of next-generation navigation and robotic systems, and a significant concentration of leading device manufacturers in the United States.

- Asia-Pacific is expected to be the fastest-growing region with a cagr of 12.30%, driven by rapidly rising neurological disorder prevalence across China, India, Japan, and South Korea, increasing government investments in neuroscience centers, growing medical tourism for complex brain and spine surgeries, and improving healthcare infrastructure capable of accommodating advanced neurosurgical technologies.

- The Neurostimulation Devices segment dominated the market with a share of 34.20% due to widespread clinical adoption of deep brain stimulators, spinal cord stimulators, and vagal nerve stimulators as effective, long-term management solutions for Parkinson's disease, chronic pain, epilepsy, and other neurological conditions.

Report Scope and Neurosurgical Devices Market Segmentation

|

Attributes |

Neurosurgical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America:

Europe:

Asia-Pacific:

Middle East and Africa:

South America:

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Neurosurgical Devices Market Trends

"Rapid Adoption of Robotic-Assisted Neurosurgery and AI-Powered Intraoperative Navigation is Redefining Surgical Precision and Outcomes"

- The integration of robotic-assisted systems and AI-driven intraoperative navigation into neurosurgical workflows is rapidly transforming the global neurosurgical devices market, enabling surgeons to achieve unprecedented levels of precision, reproducibility, and patient safety in complex cranial and spinal procedures.

- AI-powered real-time tracking of neural pathways, automated image segmentation, and predictive surgical planning tools are significantly reducing the risk of post-operative neurological deficits and improving patient recovery trajectories.

- The growing deployment of closed-loop neurostimulation systems — particularly next-generation deep brain stimulators that sense and automatically adjust electrical stimulation based on neural biomarkers — represents a paradigm shift toward responsive, patient-adaptive therapy for Parkinson's disease, epilepsy, and chronic pain.

- Increasing clinical adoption of minimally invasive neuroendoscopy and fluorescence-guided surgery platforms is driving demand for advanced visualization and access devices, improving tumor resection completeness and reducing complications.

- Expansion of tele-neurosurgery and remote surgical guidance platforms is gradually reducing geographical barriers to specialized neurosurgical expertise, particularly in underserved emerging markets.

- Rising investments in personalized neurosurgery — including patient-specific cranial implants manufactured via 3D printing and AI-optimized surgical plans — are creating premium technology segments within the broader neurosurgical devices market.

- Overall, convergence of robotics, AI, advanced imaging, and biocompatible implant innovation is positioning neurosurgical devices as one of the most technologically advanced and highest-growth segments within the global medical device industry.

Neurosurgical Devices Market Dynamics

Driver

"Rising Global Prevalence of Neurological Disorders and Expanding Geriatric Population Are Driving Neurosurgical Device Demand"

- The escalating global burden of neurological disorders — including Parkinson's disease, Alzheimer's disease, epilepsy, brain tumors, stroke, and traumatic brain and spinal cord injuries — is a primary driver of demand for advanced neurosurgical devices across all major markets.

- According to the World Health Organization (WHO), neurological disorders affect over 3 billion people worldwide, making them the leading contributor to global disability burden and generating sustained demand for diagnostic and interventional neurosurgical solutions.

- The rapidly aging global population is amplifying neurological disease incidence, as conditions such as Parkinson's, Alzheimer's, and cerebrovascular disease disproportionately affect individuals over 65, creating a growing and enduring patient base requiring neurosurgical interventions.

- Increasing adoption of deep brain stimulation (DBS) for Parkinson's disease and treatment-resistant depression, spinal cord stimulation for chronic pain management, and vagal nerve stimulation for epilepsy are substantially expanding neurostimulation device utilization globally.

- Growing investments in neurology infrastructure — including dedicated neuroscience centers, advanced imaging suites, and surgical robotics installations — across both developed and emerging markets are supporting higher procedural volumes and expanded device adoption.

- Rising awareness among patients and caregivers regarding neurosurgical treatment options, supported by healthcare professional education programs and clinical outcome publications, is reducing treatment delays and increasing the number of patients receiving surgical interventions.

Restraint / Challenge

"High Device Costs, Stringent Regulatory Requirements, and Shortage of Specialized Neurosurgeons Are Constraining Market Growth"

- The significant capital costs associated with advanced neurosurgical device systems — including robotic surgery platforms, high-resolution intraoperative imaging, and complex neurostimulation implants — create substantial financial barriers for hospitals and clinics in cost-sensitive healthcare environments.

- Stringent regulatory approval processes, particularly for Class III implantable neurostimulation and neurointerventional devices, involve lengthy clinical trial requirements and high compliance costs that slow the commercial market entry of innovative technologies.

- A global shortage of trained and experienced neurosurgeons — particularly acute in low- and middle-income countries across sub-Saharan Africa, South Asia, and Latin America — significantly limits neurosurgical device adoption in regions with growing neurological disease burdens.

- Complex post-operative care requirements, risk of device-related complications (such as infection, lead migration, or hardware failure), and the technical complexity of neurosurgical procedures contribute to cautious adoption, particularly in lower-resource settings.

- Trade tensions and tariff uncertainties affecting medical equipment supply chains, including imported surgical-grade steel, electronic components, and imaging device parts, are creating procurement cost pressures that may constrain device upgrade and replacement cycles in certain markets.

Neurosurgical Devices Market Scope

The market is segmented on the basis of product type, application, procedure, and end user.

By Product Type

On the basis of Product Type, the global Neurosurgical Devices market is segmented into Neurostimulation Devices, Neurointerventional Devices, Neurosurgical Navigation Systems, Neurosurgical Power Tools, CSF Management Devices, Neuroendoscopes, and Others. The Neurostimulation Devices segment dominated the market with the largest revenue share with a share of 34.20% in 2025, driven by widespread adoption of deep brain stimulators (DBS), spinal cord stimulators, vagal nerve stimulators, and transcranial magnetic stimulation (TMS) systems for the management of Parkinson's disease, epilepsy, chronic pain, treatment-resistant depression, and other neurological conditions. The reusable, long-term clinical utility of neurostimulation devices across multiple high-prevalence indications, combined with expanding reimbursement coverage and strong clinical evidence bases, underpins segment leadership.

The Neurosurgical Navigation Systems segment is expected to witness the fastest growth with a cagr of 13.80% during the forecast period, fueled by the accelerating integration of AI-powered real-time imaging, electromagnetic and optical tracking, augmented reality visualization, and robotic surgical guidance into neurosurgical workflows. Rising demand for precision in complex cranial and spinal tumor resections, minimally invasive approaches, and deep structure targeting is significantly driving adoption of advanced navigation platforms across both established and emerging neurosurgical centers.

By Application

On the basis of Application, the global Neurosurgical Devices market is segmented into Brain Tumors, Parkinson's Disease, Epilepsy, Hydrocephalus, Cerebral Aneurysm, Spinal Disorders, and Others. The Brain Tumors segment dominated the market with the largest revenue share of 28.50% in 2025, driven by the high global incidence of both primary and metastatic brain tumors, which necessitate complex surgical interventions using a broad range of neurosurgical devices including navigation systems, power tools, neuroendoscopes, and intraoperative monitoring equipment. The critical need for precision in tumor resection to maximize extent of removal while preserving neurological function sustains high device utilization per procedure.

The Parkinson's Disease segment is expected to witness the fastest growth with a cagr of 3.20% during the forecast period, propelled by rising global Parkinson's prevalence driven by an aging population, increasing adoption of deep brain stimulation as a gold-standard treatment option for advanced Parkinson's, and the development of next-generation adaptive DBS systems with sensing capabilities that allow real-time, personalized therapy adjustments. Expanding DBS indications into earlier disease stages and new neurological conditions are further supporting segment growth.

By Procedure

On the basis of Procedure, the global Neurosurgical Devices market is segmented into Open Neurosurgery, Minimally Invasive Neurosurgery, Stereotactic Neurosurgery, and Endoscopic Neurosurgery. The Open Neurosurgery segment dominated the market with a share of 47.60% in 2025, driven by its continued necessity for complex intracranial tumor resections, vascular malformation repairs, traumatic brain injury evacuations, and extensive spinal reconstructive procedures where full surgical access remains clinically essential. The broad spectrum of high-acuity cases requiring open approaches sustains device utilization across surgical instruments, cranial fixation, power tools, and haemostatic products.

The Minimally Invasive Neurosurgery segment is expected to witness the fastest growth with a cagr of 14.10%, propelled by the growing clinical and patient preference for approaches that offer reduced blood loss, shorter hospital stays, faster recovery, lower infection risk, and equivalent or superior clinical outcomes for eligible cases. Technological advances in tubular retractor systems, robotic-assisted MIS platforms, and fluorescence-guided visualization are continuously broadening the range of conditions treatable via minimally invasive neurosurgical approaches.

By End User

On the basis of End User, the global Neurosurgical Devices market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Neurology Clinics, and Others. The Hospitals segment dominated the market with the largest revenue share in 2025, accounting for over 61.29% of the market share, driven by their comprehensive neurosurgical capabilities, multidisciplinary neuro-critical care teams, advanced imaging and intraoperative monitoring infrastructure, and capacity to manage the full spectrum of neurosurgical cases from emergency trauma to elective complex brain and spine procedures. Hospitals serve as primary referral centers and primary adopters of capital-intensive neurosurgical technologies.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest growth of 12.85% during the forecast period, fueled by increasing procedural migration of select minimally invasive and less-complex neurosurgical cases to outpatient settings, cost-efficiency pressures driving health system restructuring, and the growing availability of compact, ASC-compatible neurosurgical navigation and endoscopy systems that do not require the infrastructure of a full operating theater.

Neurosurgical Devices Market Regional Analysis

- North America dominated the Neurosurgical Devices market with the largest revenue share in 2025, supported by the highest per capita healthcare expenditure globally, an advanced neuroscience hospital ecosystem, broad reimbursement coverage for complex neurosurgical interventions including DBS, spinal cord stimulation, and neurointerventional procedures, and the concentrated presence of world-leading neurosurgical device manufacturers including Medtronic, Abbott, Stryker, and Boston Scientific.

- Industries across the region place strong emphasis on innovation adoption, with high rates of robotic-assisted neurosurgery utilization, early-stage clinical trial participation, and physician openness to next-generation neurostimulation and navigation technologies, driving consistent device upgrades and new system installations.

- This strong market position is further supported by substantial federal and private R&D investment in neuroscience, favorable FDA pathways for breakthrough neurosurgical devices, a high volume of annual neurosurgical procedures, and growing deployment of AI-integrated intraoperative imaging and navigation platforms across academic medical centers and community hospitals alike.

U.S. Neurosurgical Devices Market Insight

The U.S. Neurosurgical Devices market holds the dominant global position, driven by the highest incidence of neurosurgical procedures worldwide, strong Medicare and private payer reimbursement for complex neurosurgical interventions, presence of world-class academic neurosurgery centers, and a highly receptive clinical environment for emerging technologies. Increasing adoption of robotic-assisted neurosurgery, next-generation adaptive DBS systems, real-time AI navigation, and minimally invasive spine platforms are further strengthening market growth. The U.S. accounts for the majority of global neurosurgical device revenue and is expected to maintain this leadership through continued innovation and high procedural volumes.

Europe Neurosurgical Devices Market Insight

The Europe Neurosurgical Devices market is witnessing steady growth, driven by strong neurological disease prevalence across Germany, France, the United Kingdom, and Italy, well-developed neurosurgery care infrastructure, and increasing adoption of minimally invasive and robotic-assisted neurosurgical techniques. European health systems' growing focus on value-based care and improved patient outcomes is accelerating adoption of advanced navigation, monitoring, and neurostimulation technologies. Expanding reimbursement coverage and rising investments in neuro-oncology and movement disorder treatment capacity are further supporting market development.

U.K. Neurosurgical Devices Market Insight

The U.K. Neurosurgical Devices market is experiencing steady growth, supported by NHS investments in neuroscience center capacity, rising rates of Parkinson's disease and brain tumor diagnoses, and increasing adoption of DBS and minimally invasive neurosurgical approaches. Growing focus on technological innovation in NHS specialist neuroscience centers, combined with an active clinical research ecosystem and increasing use of robotic-assisted surgery, is supporting continued market expansion.

Germany Neurosurgical Devices Market Insight

The Germany Neurosurgical Devices market is expected to grow steadily, driven by a highly developed neurology and neurosurgery care ecosystem, strong national research investment in neuroscience, advanced industrial base supporting medical device innovation, and high adoption of precision surgical technologies in both academic and community hospital settings. Germany's emphasis on high-quality surgical outcomes, evidence-based device adoption, and the presence of leading device manufacturers and distributors are contributing to sustained market expansion.

Japan Neurosurgical Devices Market Insight

The Japan Neurosurgical Devices market is witnessing steady growth, driven by the world's most rapidly aging population, extremely high neurological disease burden, advanced healthcare infrastructure, and strong national focus on minimally invasive surgical techniques. Japan's established culture of medical device technology adoption, combined with robust National Health Insurance coverage for neurosurgical procedures and growing DBS utilization for Parkinson's disease, is supporting market expansion. Increasing R&D collaboration between Japanese academic institutions and global medical device companies is further driving innovation and adoption.

India Neurosurgical Devices Market Insight

The India Neurosurgical Devices market is experiencing strong growth, driven by rapidly rising neurological disorder incidence, expanding tertiary hospital neuroscience center capacity, growing government and private sector investment in advanced surgical infrastructure, and increasing medical tourism for complex neurosurgical procedures. Government initiatives focused on universal health coverage and healthcare infrastructure development are improving access to neurosurgical services. Rising awareness of DBS, endoscopic neurosurgery, and minimally invasive spine procedures among Indian neurosurgeons is further supporting technology adoption and market growth.

Neurosurgical Devices Market Share

The Neurosurgical Devices industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Abbott Laboratories (U.S.)

- Stryker Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Integra LifeSciences Corporation (U.S.)

- Penumbra, Inc. (U.S.)

- Elekta AB (Sweden)

- DePuy Synthes Inc. (Johnson & Johnson) (U.S.)

- Nevro Corporation (U.S.)

- NeuroPace Inc. (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Natus Medical Incorporated (U.S.)

Recent Developments in the Global Neurosurgical Devices Market

- In January 2026, Boston Scientific Corporation announced a definitive agreement to acquire Penumbra, Inc., a leading neurovascular intervention device company. This acquisition significantly strengthens Boston Scientific's neurovascular portfolio and provides direct entry into the fast-growing mechanical thrombectomy and neurointerventional segments, reflecting ongoing market consolidation among major neurosurgical device players.

- In April 2025, Medtronic plc received U.S. FDA approval for its next-generation adaptive deep brain stimulation (aDBS) system featuring real-time neural sensing capabilities, enabling automated, closed-loop therapy adjustments for Parkinson's disease patients — representing a major advancement in responsive neurostimulation technology.

- In September 2024, Abbott Laboratories launched an expanded indication for its Proclaim XR spinal cord stimulation platform, broadening its applicability to additional chronic pain indications and further reinforcing its competitive position in the neurostimulation devices segment.

- In June 2024, Stryker Corporation announced continued expansion of its Q Guidance System navigation platform, incorporating enhanced AI-powered intraoperative imaging integration tools to improve surgical accuracy and workflow efficiency in complex spinal and cranial procedures.

- In March 2025, NeuroPace, Inc. reported strong real-world clinical outcome data from its RNS System (responsive neurostimulation) for drug-resistant focal epilepsy, demonstrating sustained seizure reduction at long-term follow-up and supporting growing adoption of closed-loop neurostimulation for epilepsy management globally.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.