Global Next Generation Memory Market

Market Size in USD Billion

USD

11.74 Billion

USD

94.65 Billion

2025

2033

USD

11.74 Billion

USD

94.65 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 11.74 Billion |

Market Size (Forecast Year) |

USD 94.65 Billion |

CAGR |

% |

Major Markets Players |

|

Next-Generation Memory Market Size

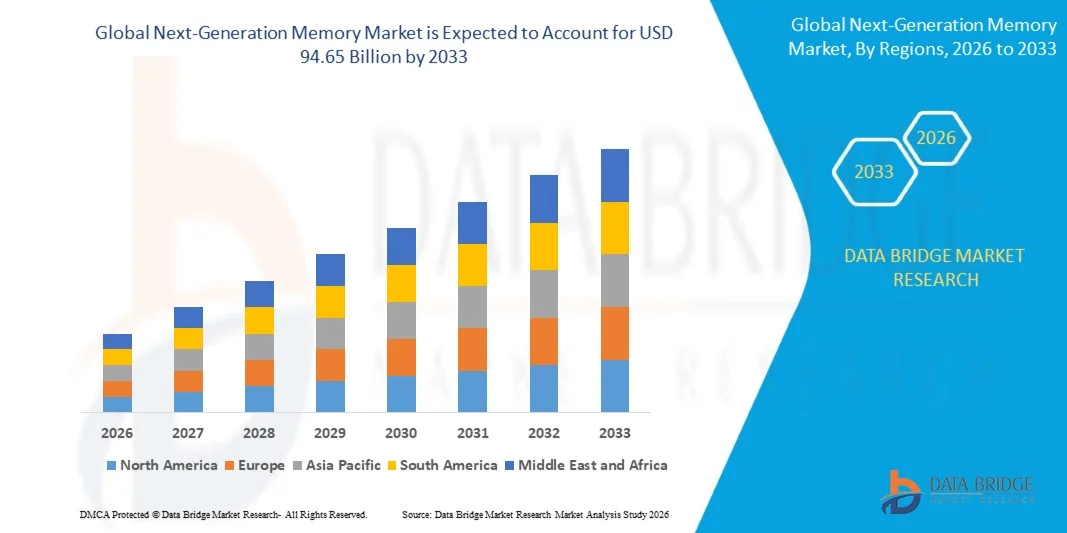

- The global next-generation memory market size was valued at USD 11.74 billion in 2025 and is expected to reach USD 94.65 billion by 2033, at a CAGR of 29.8% during the forecast period

- The next-generation memory market growth is largely fueled by the rising demand for high-performance, energy-efficient memory solutions across data-intensive applications such as AI, cloud computing, and edge computing. Increasing reliance on advanced computing and data storage is driving the adoption of next-generation memory technologies across enterprise and consumer sectors

- Furthermore, the need for faster, more reliable, and scalable memory solutions in data centers, automotive electronics, and industrial systems is encouraging investment in innovative memory types such as MRAM, ReRAM, and 3D NAND. These converging factors are accelerating the deployment of advanced memory solutions, thereby significantly boosting market growth

Next-Generation Memory Market Analysis

- Next-generation memory, including technologies such as MRAM, ReRAM, PCM, and high-bandwidth memory, is becoming a critical component in modern computing systems due to its speed, non-volatility, and ability to support high-density data storage in compact form factors

- The escalating demand for next-generation memory is primarily driven by the growth of cloud infrastructure, AI-driven applications, and connected devices across consumer electronics, automotive, and industrial sectors. In addition, increasing focus on low-power, high-speed memory solutions is further fueling adoption across multiple industries

- Asia-Pacific dominated the next-generation memory market with a share of 56.93% in 2025, due to the strong presence of semiconductor manufacturing hubs, increasing demand for high-performance memory in consumer electronics, and rapid expansion of data centers across the region

- North America is expected to be the fastest growing region in the next-generation memory market during the forecast period due to strong demand for advanced memory solutions in data centers, AI applications, and high-performance computing

- Non-volatile memory segment dominated the market with a market share of 80.2% in 2025, due to its ability to retain data without continuous power supply, making it highly suitable for long-term data storage and energy-efficient applications. Technologies such as 3D NAND and emerging storage-class memory are increasingly being adopted in data centers, enterprise storage, and mobile devices due to their scalability and high storage density. The growing demand for persistent memory solutions that combine speed and durability is further strengthening the position of non-volatile memory

Report Scope and Next-Generation Memory Market Segmentation

|

Attributes |

Next-Generation Memory Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Next-Generation Memory Market Trends

“Rising Adoption of Non-Volatile and High-Performance Memory Technologies”

- A significant trend in the next-generation memory market is the increasing adoption of non-volatile and high-performance memory technologies across data-intensive applications, driven by growing demand for faster, energy-efficient, and scalable storage solutions in cloud computing, AI, and edge computing environments

- For instance, Everspin Technologies’ MRAM products are widely used in automotive and industrial applications for high-speed, durable, and low-power memory storage, enabling real-time processing and enhanced reliability under harsh operating conditions. Such solutions are reinforcing the deployment of next-generation memory in mission-critical systems

- The market is witnessing rising adoption of advanced memory in data centers and enterprise storage where technologies such as Micron’s DDR5 RDIMM and Samsung’s high-performance NAND-based memory enhance computational efficiency and reduce latency. These implementations are positioning next-generation memory as a key component for accelerating AI workloads and large-scale data processing

- Consumer electronics are increasingly integrating advanced memory solutions to support high-resolution content creation, gaming, and mobile computing. For instance, Kioxia’s EXCERIA G2 SD memory cards and Samsung’s Evo Plus microSD cards cater to high-speed storage needs, reflecting broader adoption trends in portable and embedded devices

- Automotive applications are contributing to growth through the integration of non-volatile memory in infotainment systems, ADAS, and autonomous driving platforms. For instance, Renesas and GlobalFoundries’ embedded ReRAM solutions are supporting faster and more efficient microcontroller performance in next-generation vehicles

- The overall market expansion is driven by the convergence of high-speed processing, energy efficiency, and reliability requirements across multiple sectors, positioning next-generation memory technologies as essential components for emerging digital infrastructures

Next-Generation Memory Market Dynamics

Driver

“Growing Demand from Data Centers, AI, and Edge Computing Applications”

- The growing reliance on advanced computing and data-intensive workloads is driving the adoption of next-generation memory solutions that offer higher speed, scalability, and energy efficiency. Data centers and AI platforms require low-latency, high-capacity memory technologies to manage large-scale processing, creating strong demand for MRAM, ReRAM, PCM, and HBM

- For instance, Micron Technology’s 128GB DDR5 RDIMM memory modules are designed to meet the increasing performance requirements of modern hyperscale data centers, supporting faster data processing and workload optimization. These solutions are enabling enterprises to efficiently manage AI, cloud, and analytics operations

- The expansion of edge computing and IoT ecosystems is further boosting demand for high-performance, compact memory solutions. Companies such as Samsung and Kioxia provide NAND-based and embedded memory solutions for smartphones, wearable devices, and industrial sensors, ensuring low power consumption while maintaining high throughput

- Automotive electronics and industrial automation applications are increasingly adopting non-volatile memory to support real-time processing, safety-critical operations, and predictive maintenance. Collaborations such as Renesas and GlobalFoundries for embedded ReRAM demonstrate the growing investment in specialized memory architectures for these sectors

- Rising adoption of AI-driven analytics, high-performance computing, and 5G infrastructure is reinforcing the need for memory solutions that can handle intensive workloads while optimizing energy efficiency and space utilization, driving sustained market growth

Restraint/Challenge

“High Manufacturing Costs and Complex Fabrication Processes”

- The next-generation memory market faces challenges due to the complex fabrication processes and high production costs associated with emerging memory technologies. Advanced memory types such as MRAM, ReRAM, and PCM require specialized materials, precise lithography, and high-end equipment, which increase manufacturing complexity and capital expenditure

- For instance, Everspin Technologies and Avalanche Technology employ intricate wafer processing and deposition techniques to ensure reliability, endurance, and performance of MRAM and ReRAM devices. These specialized processes demand skilled labor, precise environmental control, and stringent quality assurance, elevating overall costs

- Producing high-speed, high-density memory with consistent performance and non-volatility requires extensive testing and validation, further lengthening production cycles and increasing operational expenditures. These factors impact scalability and cost-effectiveness for manufacturers

- Reliance on rare or advanced materials and state-of-the-art semiconductor fabs exposes manufacturers to supply chain vulnerabilities, material price fluctuations, and technological bottlenecks

- Scaling production to meet growing demand while maintaining reliability, energy efficiency, and competitive pricing remains a critical challenge. Companies must balance innovation with economic feasibility to sustain market growth in the face of manufacturing complexity and cost pressures

Next-Generation Memory Market Scope

The market is segmented on the basis of technology, storage type, wafer size, and industry.

• By Technology

On the basis of technology, the next-generation memory market is segmented into volatile memory and non-volatile memory. The non-volatile memory segment dominated the market with the largest market revenue share of 80.2% in 2025, driven by its ability to retain data without continuous power supply, making it highly suitable for long-term data storage and energy-efficient applications. Technologies such as 3D NAND and emerging storage-class memory are increasingly being adopted in data centers, enterprise storage, and mobile devices due to their scalability and high storage density. The growing demand for persistent memory solutions that combine speed and durability is further strengthening the position of non-volatile memory. In addition, advancements in memory architectures and increasing investments by semiconductor companies are supporting continuous innovation and performance enhancement in this segment. The ability of non-volatile memory to support AI workloads and big data analytics is also contributing to its widespread adoption across industries.

The volatile memory segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for high-speed data processing and real-time computing applications. Volatile memory technologies such as DRAM and emerging MRAM are essential for applications requiring rapid read and write cycles, particularly in AI, gaming, and high-performance computing environments. The increasing deployment of cloud computing and edge computing solutions is further driving the need for faster memory access and reduced latency. Continuous technological advancements aimed at improving speed and reducing power consumption are enhancing the attractiveness of volatile memory. Moreover, the integration of volatile memory in advanced processors and graphics units is supporting its growing adoption.

• By Storage Type

On the basis of storage type, the next-generation memory market is segmented into mass storage, embedded storage, and others. The mass storage segment dominated the market with the largest market revenue share in 2025, driven by the exponential growth of data generation across enterprises, cloud platforms, and digital services. Organizations increasingly rely on high-capacity storage solutions to manage large volumes of structured and unstructured data, leading to strong demand for advanced memory technologies. The adoption of solid-state drives and high-density storage devices is further supporting the expansion of this segment. In addition, the rapid growth of data centers and hyperscale infrastructure is creating sustained demand for scalable and efficient storage solutions. Continuous improvements in storage density and cost efficiency are also strengthening the dominance of mass storage systems.

The embedded storage segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing integration of memory components within consumer electronics, IoT devices, and automotive systems. Embedded storage solutions offer compact design, faster data access, and improved energy efficiency, making them ideal for space-constrained and performance-sensitive applications. The growing adoption of smart devices, wearables, and connected technologies is significantly boosting demand for embedded memory. Furthermore, advancements in system-on-chip architectures are enabling seamless integration of storage within processors. The rising focus on edge computing and real-time data processing is also accelerating the growth of this segment.

• By Wafer Size

On the basis of wafer size, the next-generation memory market is segmented into 200 mm, 300 mm, and 450 mm. The 300 mm wafer segment dominated the market with the largest market revenue share in 2025, driven by its higher production efficiency and cost advantages compared to smaller wafer sizes. Semiconductor manufacturers widely adopt 300 mm wafers for memory fabrication as they allow more chips to be produced per wafer, improving overall yield and reducing manufacturing costs. The strong presence of advanced fabrication facilities and continuous process optimization further support the growth of this segment. In addition, increasing demand for high-performance memory solutions is encouraging manufacturers to expand 300 mm wafer production capacity. The scalability and economic benefits associated with this wafer size make it a preferred choice across the industry.

The 450 mm wafer segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by ongoing research and development aimed at enhancing semiconductor manufacturing efficiency. Larger wafer sizes offer the potential for significantly higher output and lower cost per chip, making them attractive for future large-scale production. Although still in the developmental and early adoption stage, increasing investments by leading semiconductor companies are accelerating progress in this segment. The growing need for cost-effective memory solutions in high-demand applications is further driving interest in 450 mm wafers. Technological advancements and infrastructure upgrades are expected to support the gradual commercialization of this wafer size.

• By Industry

On the basis of industry, the next-generation memory market is segmented into enterprise storage, consumer electronics, military and aerospace, industrial, automotive and transportation, telecommunications, energy and power, healthcare, agriculture, and retail. The consumer electronics segment dominated the market with the largest market revenue share in 2025, driven by the widespread adoption of smartphones, laptops, gaming devices, and wearable technologies. Increasing consumer demand for high-speed, high-capacity devices is fueling the integration of advanced memory solutions in electronic products. Continuous product innovation and shorter device replacement cycles are further supporting demand growth in this segment. In addition, the rising popularity of high-resolution content and mobile gaming is increasing the need for enhanced memory performance. The expansion of connected devices and smart ecosystems is also contributing to the strong position of consumer electronics in the market.

The automotive and transportation segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the rapid adoption of advanced driver-assistance systems, electric vehicles, and autonomous driving technologies. These applications require high-performance memory solutions capable of processing large volumes of real-time data with low latency. The increasing integration of infotainment systems and vehicle connectivity features is further boosting demand for next-generation memory. In addition, the shift toward software-defined vehicles is accelerating the need for reliable and scalable memory architectures. Growing investments in automotive electronics and intelligent mobility solutions are expected to sustain strong growth in this segment.

Next-Generation Memory Market Regional Analysis

- Asia-Pacific dominated the next-generation memory market with the largest revenue share of 56.93% in 2025, driven by the strong presence of semiconductor manufacturing hubs, increasing demand for high-performance memory in consumer electronics, and rapid expansion of data centers across the region

- The region’s cost-efficient manufacturing capabilities, rising investments in advanced semiconductor fabrication facilities, and growing adoption of AI, IoT, and 5G technologies are accelerating market expansion

- The availability of skilled workforce, supportive government initiatives for semiconductor self-sufficiency, and continuous technological advancements are contributing to increased production and consumption of next-generation memory solutions

China Next-Generation Memory Market Insight

China held the largest share in the Asia-Pacific next-generation memory market in 2025, owing to its dominance in semiconductor manufacturing and extensive investments in memory chip production. The country’s strong government support through funding programs and policies aimed at reducing dependence on imports is driving domestic innovation. Growing demand from consumer electronics, data centers, and AI applications is further strengthening market growth.

India Next-Generation Memory Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by increasing digitalization, expansion of data center infrastructure, and rising demand for advanced electronics. Government initiatives promoting semiconductor manufacturing and growing investments in electronics production are supporting market development. In addition, the rapid adoption of cloud computing, 5G deployment, and AI-driven applications is contributing to rising demand for next-generation memory.

Europe Next-Generation Memory Market Insight

The Europe next-generation memory market is expanding steadily, supported by strong focus on semiconductor innovation, increasing investments in advanced manufacturing technologies, and growing demand for high-performance computing solutions. The region emphasizes energy-efficient and sustainable memory technologies, particularly for industrial automation and automotive applications. Rising adoption of AI and edge computing is further enhancing market growth.

Germany Next-Generation Memory Market Insight

Germany’s next-generation memory market is driven by its leadership in automotive electronics, industrial automation, and strong semiconductor ecosystem. The country benefits from well-established research institutions and collaborations between industry and academia, fostering innovation in advanced memory technologies. Demand is particularly strong in applications related to electric vehicles, Industry 4.0, and high-performance computing.

U.K. Next-Generation Memory Market Insight

The U.K. market is supported by growing investments in semiconductor research, increasing demand for memory solutions in data-intensive applications, and a strong presence of technology-driven industries. Focus on AI, fintech, and cloud-based services is driving the need for high-speed and reliable memory systems. The country’s emphasis on innovation and digital transformation is further contributing to market expansion.

North America Next-Generation Memory Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by strong demand for advanced memory solutions in data centers, AI applications, and high-performance computing. The presence of leading technology companies, continuous R&D investments, and rapid adoption of cloud and edge computing technologies are boosting market growth. In addition, increasing focus on semiconductor manufacturing and supply chain resilience is supporting expansion.

U.S. Next-Generation Memory Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its advanced semiconductor industry, strong innovation ecosystem, and significant investments in memory technology development. The country’s leadership in AI, cloud computing, and data center infrastructure is driving demand for high-performance memory solutions. Presence of major market players and continuous technological advancements further strengthen the U.S. position in the region.

Next-Generation Memory Market Share

The next-generation memory industry is primarily led by well-established companies, including:

- 4DS Memory Limited (U.S.)

- Adesto Technologies Corporation (U.S.)

- Avalanche Technology (U.S.)

- Cypress Semiconductor Corporation (U.S.)

- Everspin Technologies Inc. (U.S.)

- FUJITSU (Japan)

- IBM Corporation (U.S.)

- Microchip Technology Inc. (U.S.)

- Nantero (U.S.)

- SAMSUNG (South Korea)

- Rambus (U.S.)

- SK HYNIX INC. (South Korea)

- Spin Memory Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Toshiba CORPORATION (Japan)

- Texas Instruments Incorporated (U.S.)

- Western Digital Corporation (U.S.)

Latest Developments in Global Next-Generation Memory Market

- In February 2026, Everspin Technologies achieved AEC-Q100 Grade 1 qualification for its 1 Gbit STT-MRAM, enabling reliable operation across a wide temperature range from -40 °C to 125 °C. This milestone significantly enhances the credibility of MRAM technology for deployment in automotive electronics and industrial systems where durability and thermal stability are critical. It is expected to accelerate adoption in advanced driver-assistance systems and mission-critical applications, thereby strengthening the role of next-generation memory in high-reliability environments and expanding its commercial viability

- In January 2026, Renesas Electronics entered into a partnership with GlobalFoundries to co-develop embedded ReRAM solutions for next-generation automotive microcontrollers. This collaboration is aimed at integrating faster, more energy-efficient, and scalable memory into automotive chips, supporting the transition toward software-defined and autonomous vehicles. The development is likely to boost innovation in embedded memory architectures while enabling automakers to enhance real-time processing capabilities, ultimately driving increased demand for next-generation memory in the automotive sector

- In May 2024, Micron Technology, Inc. announced the shipment of its 128GB DDR5 RDIMM designed for data center applications, delivering speeds of up to 5,600 MT/s along with significantly higher memory capacity. This advancement addresses the growing need for faster data processing, improved bandwidth, and efficient workload management in modern cloud and enterprise environments. It is expected to strengthen Micron’s position in high-performance memory while supporting the rapid expansion of hyperscale data centers and AI-driven computing infrastructure

- In April 2024, Samsung introduced its Evo Select and Evo Plus microSD memory cards in the U.S. with enhanced read speeds of up to 160 MB/s, representing a notable improvement over its previous generation products. This upgrade is aligned with increasing consumer demand for faster data transfer and seamless performance across smartphones, cameras, and gaming devices. The development is expected to reinforce Samsung’s competitiveness in the consumer memory segment while driving broader adoption of high-speed portable storage solutions

- In April 2024, Kioxia Corporation launched the EXCERIA G2 SD memory card series with storage capacities reaching up to 1TB, specifically designed for extended 4K video recording and high-resolution content capture. This innovation caters to the growing needs of professional content creators and advanced consumer electronics users requiring large storage capacity and consistent performance. It is expected to enhance Kioxia’s market presence while contributing to the expansion of next-generation memory applications in multimedia and data-intensive use cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Next Generation Memory Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Next Generation Memory Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Next Generation Memory Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.