Global Next Generation Products Market

Market Size in USD Billion

USD

13.70 Billion

USD

115.24 Billion

2025

2033

USD

13.70 Billion

USD

115.24 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 13.70 Billion |

Market Size (Forecast Year) |

USD 115.24 Billion |

CAGR |

% |

Major Markets Players |

|

Next Generation Products Market Size

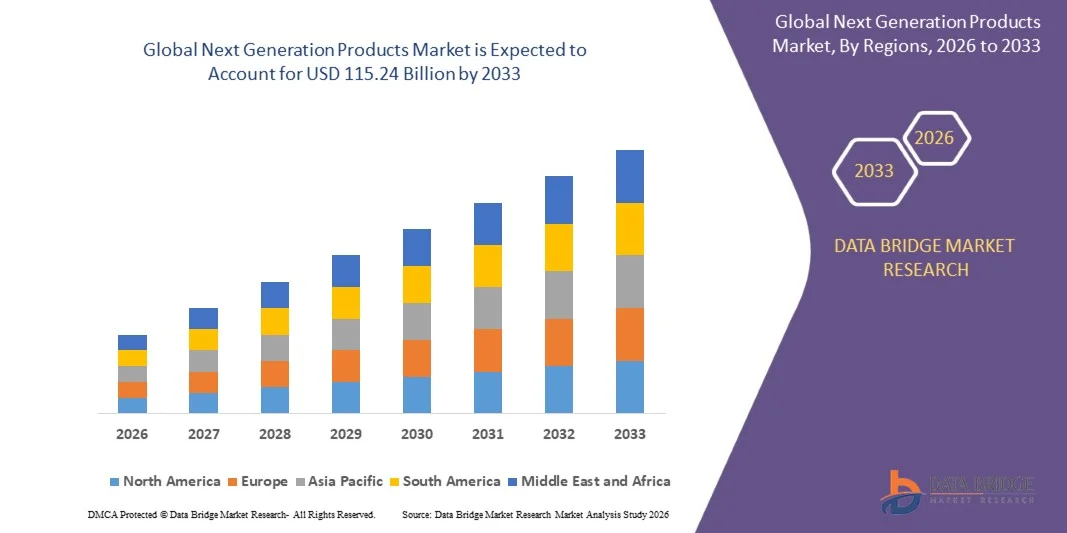

- The global next generation products market size was valued at USD 13.70 billion in 2025 and is expected to reach USD 115.24 billion by 2033, at a CAGR of 30.5% during the forecast period

- The market growth is largely driven by rising consumer inclination toward innovative, reduced-risk nicotine alternatives and continuous technological progress in heating, vaporization, and flavor delivery systems, which is reshaping consumption preferences across key regions

- Furthermore, expanding regulatory acceptance for reduced-harm products in several markets, combined with strong investments by leading tobacco companies in R&D and product diversification, is accelerating the shift from traditional cigarettes to next-generation offerings, thereby strengthening overall market expansion

Next Generation Products Market Analysis

- Next-generation products, comprising e-cigarettes, heated tobacco devices, and modern oral nicotine formats, are becoming central to the global tobacco industry's transformation due to their potential harm-reduction profile, customizable usage experience, and strong adoption among adult smokers seeking alternatives

- The growing demand for these products is primarily supported by increasing health-conscious behavior among adult consumers, rapid product innovation in device efficiency and aerosol delivery, and a broad industry push toward smoke-free portfolio strategies aimed at long-term sustainability

- North America dominated next generation products market in 2025, due to strong adoption of advanced digital solutions and increasing dependence on modernized technology infrastructures

- Asia-Pacific is expected to be the fastest growing region in the next generation products market during the forecast period due to rapid urbanization, expanding digital penetration, and increasing investment in technology-driven infrastructures across major countries such as China, Japan, and India

- Products and services segment dominated the market with a market share of 54.7% in 2025, due to large-scale adoption of high-throughput NGS instruments, advanced automation systems, and data interpretation solutions. Industry demand is high due to the rising use of integrated sequencing systems in clinical genomics and translational research, creating sustained revenue for instrument manufacturers and service providers. Research institutions and hospitals rely on comprehensive sequencing workflows, which strengthens uptake of bundled products and outsourced sequencing services. The segment also benefits from continuous innovation, which ensures recurring upgrades and long-term customer dependence on complete sequencing ecosystems

Report Scope and Next Generation Products Market Segmentation

|

Attributes |

Next Generation Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Next Generation Products Market Trends

Growing Shift Toward Smoke-Free and Reduced-Risk Products

- A major trend in the next generation products market is the accelerating transition toward smoke-free and reduced-risk nicotine alternatives as consumers prioritize health-conscious choices and seek products that significantly lower exposure to harmful substances. This shift is strengthening the adoption of heated tobacco devices, nicotine pouches, and advanced vapor systems across key markets

- For instance, Philip Morris International and British American Tobacco are expanding portfolios of reduced-risk products supported by scientific validation and advanced nicotine delivery technologies. These offerings enhance product safety profiles and help brands meet evolving consumer expectations for cleaner and more controlled usage experiences

- The preference for smoke-free formats is rising among adult users seeking odor-free, discreet, and technologically enhanced solutions that improve convenience and minimize traditional smoking drawbacks. This is strengthening demand in both mature and emerging regions

- The increasing role of device innovations such as temperature control systems, improved aerosol generation, and heat-not-burn mechanisms is elevating user experience and reinforcing the broader shift toward modern nicotine consumption methods

- Strong marketing communication focused on harm reduction, product transparency, and evolving lifestyle trends is encouraging higher adoption among young adult consumers and accelerating market transformation

- The market is experiencing heightened momentum as regulatory authorities in several regions recognize reduced-risk categories, supporting product development and structured commercial expansion. This ongoing transition is positioning next generation products as key alternatives within the global nicotine ecosystem

Next Generation Products Market Dynamics

Driver

Rising Consumer Demand for Harm-Reduction Nicotine Options

- The market is being propelled by a growing preference for nicotine products that offer significantly lower toxicant exposure compared with conventional cigarettes, driven by health awareness and a shift toward safer consumption habits. This rising demand is encouraging rapid adoption of alternative formats that prioritize user safety without eliminating nicotine intake

- For instance, Japan Tobacco International and Imperial Brands continue to invest in advanced heated tobacco systems and vapor products engineered to reduce combustion-related harm. These innovations support consumer transition away from traditional cigarettes while maintaining satisfaction through controlled nicotine delivery

- Increasing urbanization and changing lifestyle patterns are expanding acceptance of next generation devices that offer ease of use, reduced odor, and improved social acceptability. These factors are reinforcing long-term demand across diversified demographic groups

- Advancements in nicotine formulation, battery efficiency, and device design are further strengthening the overall consumer value proposition. This is cementing the role of harm-reduction products as core growth drivers within the market

- Rising awareness of scientific studies highlighting reduced-risk profiles is reinforcing consumer confidence, supporting sustained market expansion and shaping industry innovation strategies

Restraint/Challenge

Strict Regulatory Requirements Across Major Markets

- The market faces challenges due to stringent regulatory frameworks governing nicotine concentration, product testing, packaging, and marketing claims, which increase compliance burdens and restrict operational flexibility for manufacturers. These regulations vary widely across regions, creating barriers to consistent product rollout

- For instance, companies such as Altria and BAT must comply with rigorous standards such as premarket authorization, ingredient disclosure, and safety assessments before commercializing next generation products. These processes are resource-intensive and lengthen market entry timelines

- Complex taxation policies and advertising limitations in many countries add pressure on manufacturers to navigate evolving legal structures while ensuring affordability and brand visibility

- High compliance costs and rigid approval pathways challenge companies to balance innovation speed with regulatory expectations, slowing down the introduction of advanced technologies

- These constraints continue to shape competitive dynamics by favoring companies with strong regulatory capabilities, while smaller players face heightened difficulty in sustaining market presence

Next Generation Products Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the Next Generation Products market is segmented into Products and Services, Consumables, and Platforms. The Products and Services segment dominated the market with the largest share of 54.7% in 2025, supported by large-scale adoption of high-throughput NGS instruments, advanced automation systems, and data interpretation solutions. Industry demand is high due to the rising use of integrated sequencing systems in clinical genomics and translational research, creating sustained revenue for instrument manufacturers and service providers. Research institutions and hospitals rely on comprehensive sequencing workflows, which strengthens uptake of bundled products and outsourced sequencing services. The segment also benefits from continuous innovation, which ensures recurring upgrades and long-term customer dependence on complete sequencing ecosystems.

The Consumables segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by recurring purchases of reagents, sample preparation kits, and library construction solutions. As sequencing throughput and sample volumes increase, laboratories require frequent replenishment of consumables, contributing to consistent revenue expansion. The segment also gains momentum from the adoption of targeted sequencing panels, precision medicine programs, and oncology testing workflows. Rising R&D investments in gene expression studies and variant analysis further elevate demand for specialized reagent kits across academic and clinical facilities.

- By Technology

On the basis of technology, the market is segmented into Sequencing by Synthesis, Ion Semiconductor Sequencing, Single-Molecule Real-Time Sequencing, Nanopore Sequencing, and Other Sequencing Technologies. Sequencing by Synthesis (SBS) dominated the market in 2025, attributed to its accuracy, established workflow, and widespread adoption across clinical diagnostics and research sequencing applications. The strong presence of SBS-based platforms in large laboratories enhances its revenue share due to continuous upgrades and higher throughput capabilities. Its compatibility with diverse assays, including oncology genomics and inherited disease testing, ensures broad utilization. Market adoption also remains high due to the robust ecosystem of reagents, analysis tools, and consumables supporting SBS technology.

Nanopore Sequencing is expected to witness the fastest growth rate from 2026 to 2033, driven by its real-time sequencing capability, portable device design, and ability to sequence long DNA fragments. Research institutions increasingly adopt nanopore platforms for rapid pathogen detection, field-based genomic analysis, and population-scale sequencing studies. The technology’s scalability and lower infrastructure requirements make it attractive for decentralized testing environments. Advancements improving accuracy and throughput further encourage adoption across clinical and research settings.

- By Application

On the basis of application, the market is segmented into Diagnostics, Drug Discovery, Agriculture and Animal Research, and Other Applications. Diagnostics dominated the market in 2025, supported by the integration of genomic testing into oncology, infectious disease monitoring, and rare disease detection. Increasing healthcare system acceptance of sequencing-based diagnostic tools enhances patient outcomes through personalized care and targeted treatment planning. The segment continues to benefit from broader reimbursement approvals and regulatory acceptance of NGS-based testing kits. Hospitals and labs adopt diagnostic sequencing due to its precision, clinical utility, and ability to deliver actionable genomic insights.

Drug Discovery is projected to witness the fastest growth rate from 2026 to 2033, driven by expanding use of sequencing for biomarker identification, therapeutic target discovery, and pharmacogenomics studies. Pharmaceutical companies increasingly integrate NGS platforms into preclinical and clinical pipelines to accelerate decision-making and reduce development timelines. Sequencing-based models enhance understanding of molecular interactions, enabling efficient evaluation of drug candidates. Rising investment in precision therapeutics and biologics further strengthens the segment’s upward trajectory.

- By End User

On the basis of end user, the market is segmented into Academic Institutes and Research Centers, Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, and Other End Users. Academic Institutes and Research Centers dominated the market in 2025, owing to extensive genome research programs, population-scale sequencing initiatives, and continuous funding for advanced molecular biology studies. These institutions operate high-throughput sequencing platforms for varied applications ranging from structural genomics to environmental DNA analysis. Their collaborations with biotechnology companies and government bodies accelerate adoption of next-generation sequencing systems. The segment’s growth is reinforced by the increasing number of genomic research laboratories worldwide.

Pharmaceutical and Biotechnology Companies are expected to witness the fastest growth rate from 2026 to 2033, driven by growing use of sequencing technologies in drug development, biomarker research, and precision medicine pipelines. Biopharma companies require sequencing tools to support clinical trial stratification, variant detection, and therapeutic response analysis. The expansion of targeted therapy development boosts demand for specialized sequencing platforms. Investments in genomics-driven R&D and biomanufacturing also enhance adoption within this segment.

Next Generation Products Market Regional Analysis

- North America dominated the next generation products market with the largest revenue share in 2025, driven by strong adoption of advanced digital solutions and increasing dependence on modernized technology infrastructures

- Organizations across the region prioritize next generation platforms that enhance operational efficiency, improve data management, and support real-time decision-making capabilities

- This rising preference is reinforced by a mature technology ecosystem, high digital literacy, and rapid acceptance of innovative enterprise solutions. Enterprises and consumers consistently seek improved accessibility, streamlined workflows, and integrated digital systems, strengthening the region’s leadership in next generation product adoption

U.S. Next Generation Products Market Insight

The U.S. next generation products market captured the largest revenue share in 2025 within North America, driven by accelerated digital transformation efforts and rising demand for advanced solutions across enterprise and consumer environments. Organizations focus heavily on upgrading existing systems with next generation tools that support automation, cloud integration, and enhanced performance capabilities. The growing shift toward connected platforms and remote-enabled operations further elevates market uptake. High adoption of AI-driven systems, cloud-based applications, and mobile-centric solutions continues to propel market expansion across industries.

Europe Next Generation Products Market Insight

The Europe next generation products market is projected to expand at a substantial CAGR during the forecast period, supported by strong regulatory frameworks promoting digital adoption and enhanced technological modernization. Rising emphasis on structured digital infrastructure, secure data handling, and efficient system deployment is contributing to increasing usage across both enterprise and public sectors. Consumers and organizations across Europe prefer solutions that improve operational transparency, reduce manual processes, and support reliable connectivity. The region exhibits strong adoption across diverse applications as next generation products become integral to modernization initiatives and smart ecosystem development.

U.K. Next Generation Products Market Insight

The U.K. next generation products market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by increasing focus on digital transformation and rising demand for flexible, modernized technology solutions. Organizations across sectors are adopting next generation tools to strengthen operational productivity and improve user experience. Heightened security needs and evolving digital service expectations encourage businesses to integrate advanced systems that support streamlined workflows. The country’s well-established digital infrastructure and rapid acceptance of connected solutions continue to drive market growth.

Germany Next Generation Products Market Insight

The Germany next generation products market is expected to expand at a considerable CAGR during the forecast period, supported by strong awareness of digital modernization and preference for technologically advanced, reliable solutions. The country's emphasis on innovation, structured system upgrades, and sustainability-focused digital tools accelerates adoption across enterprise and consumer segments. Germany’s robust industrial base and preference for secure, efficient, and automation-driven systems encourage widespread integration of next generation products into daily operations. Growing incorporation of modern platforms into organizational frameworks continues to support market development.

Asia-Pacific Next Generation Products Market Insight

The Asia-Pacific next generation products market is poised to grow at the fastest CAGR during 2026–2033, supported by rapid urbanization, expanding digital penetration, and increasing investment in technology-driven infrastructures across major countries such as China, Japan, and India. Rising digital awareness and government-led modernization initiatives strengthen the region’s transition toward next generation systems. The region’s role as a technology manufacturing hub enhances accessibility and affordability, broadening adoption across enterprises and consumers. Increasing reliance on connected devices and emerging digital platforms contributes strongly to APAC’s accelerated growth.

Japan Next Generation Products Market Insight

The Japan next generation products market is gaining momentum due to the country’s strong technological orientation, rapid urban expansion, and preference for highly efficient digital systems. Consumers and enterprises adopt next generation products to enhance convenience, reliability, and functionality across various applications. Integration with connected ecosystems and growing use of modern digital devices elevate market uptake. Japan’s demographic trends and demand for user-friendly, secure, and adaptable solutions further strengthen market progression.

China Next Generation Products Market Insight

The China next generation products market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid urbanization, expanding middle-class adoption, and strong technological engagement across industries. China stands as a key contributor to digital product demand due to its large consumer base and high rate of technology acceptance. The rise of smart ecosystems, increasing deployment of digital platforms, and strong domestic production capabilities significantly boost market penetration. Growing availability of cost-effective next generation solutions drives widespread usage across residential, commercial, and industrial environments.

Next Generation Products Market Share

The next generation products industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- BGI Group (China)

- PerkinElmer Inc. (U.S.)

- Macrogen (South Korea)

- Hamilton Company (U.S.)

- Lucigen (U.S.)

- Intrexon Bioinformatics GmbH (Germany)

- Partek Incorporated (U.S.)

- DNASTAR, Inc. (U.S.)

- DNAnexus (U.S.)

- SciGenom Labs Pvt. Ltd. (India)

- GENEWIZ (U.S.)

- Takara Bio Inc. (Japan)

- Eurofins Scientific (Luxembourg)

- 10x Genomics (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Becton Dickinson and Company (U.S.)

- Danaher (U.S.)

- Lexogen GmbH (Austria)

- Tecan Trading AG (Switzerland)

- Zymo Research (U.S.)

- Oxford Nanopore Technologies (U.K.)

- Agilent Technologies, Inc. (U.S.)

- QIAGEN (Germany)

Latest Developments in Global Next Generation Products Market

- In December 2025, BASF and Welion New Energy Technology introduced a next-generation solid-state battery pack at the Guangzhou International Automobile Exhibition, marking a major advancement for the electric vehicle market. The integration of BASF’s advanced material solutions—Ultramid®, Ultradur®, and polyurethane systems—strengthens battery safety, improves thermal stability, and reduces vehicle weight, accelerating the shift toward commercial solid-state EV adoption and reinforcing industry movement toward safer, higher-performing energy storage technologies

- In December 2025, FUJIFILM launched ZEMATES, an advanced solution for next-generation semiconductor packaging, significantly influencing the semiconductor manufacturing market. The technology enables higher-density chip designs, enhanced reliability, and improved production precision, aligning with growing demand for compact and high-performance devices across AI, 5G, and IoT applications. This launch strengthens FUJIFILM’s role in next-gen semiconductor innovation by supporting manufacturers in achieving superior efficiency and next-level chip integration

- In October 2025, Applied Materials unveiled a new portfolio of next-generation chipmaking products designed to support advanced node manufacturing and elevate AI computing performance. This development reshapes the semiconductor equipment market by enabling chipmakers to deliver faster processing, improved energy efficiency, and more complex architectures needed for demanding AI workloads. The launch reinforces Applied Materials’ leadership in next-gen fabrication technologies and supports global momentum toward high-performance semiconductor production

- In October 2025, Amway India introduced Artistry Skin Nutrition’s next-generation skincare range powered by Nutrilite plant-based science, impacting the premium beauty and skincare market. The line responds to rising demand for wellness-driven, clean-label formulations that combine nutritional science with dermatological efficacy. This launch strengthens Amway’s presence in next-gen skincare by offering advanced solutions that align with evolving consumer expectations for holistic and science-backed skin health

- In June 2025, Bayer and Kimitec launched two next-generation biological products to enhance regenerative agriculture, influencing the sustainable farming and biologicals market. These solutions provide natural alternatives for crop protection and enhancement, supporting soil health and improving yield resilience in environmentally conscious farming systems. The collaboration accelerates the adoption of next-gen biological inputs and reinforces industry movement toward regenerative and eco-friendly agricultural practices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.