Global Night Vision System Market

Market Size in USD Billion

USD

4.90 Billion

USD

13.08 Billion

2025

2033

USD

4.90 Billion

USD

13.08 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.90 Billion | |

| USD 13.08 Billion | |

| % | |

|

Night Vision System Market Overview

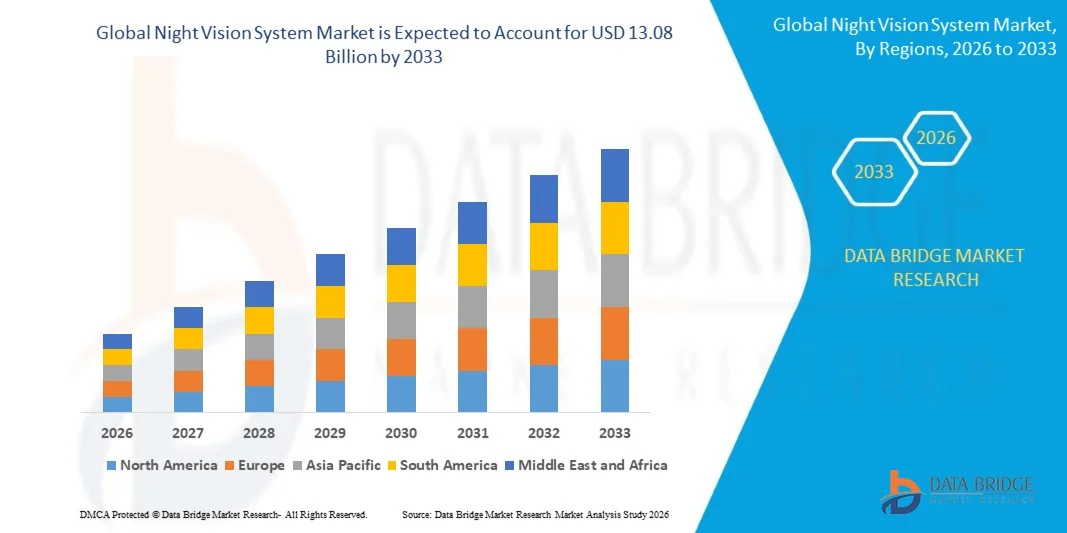

The Night Vision System Market was valued at USD 4.90 Billion in 2025 and is projected to reach USD 13.08 Billion by 2033, growing at a CAGR of 13.06% from 2026 to 2033. The market is experiencing consistent growth driven by increasing adoption of advanced driver assistance systems, rising demand for enhanced vehicle safety technologies, and growing integration of infrared imaging solutions in premium and autonomous vehicles. Expanding deployment of thermal cameras and advancements in sensor technologies are further supporting market expansion across the automotive sector.

The increasing global focus on reducing road accidents and improving driver visibility under low-light conditions, combined with stringent vehicle safety regulations, is encouraging automakers to incorporate advanced night vision technologies into modern vehicles. Night vision systems are increasingly being integrated with ADAS and autonomous driving platforms to improve pedestrian detection and situational awareness, helping manufacturers enhance safety performance and driving efficiency.

Key Market Trends & Insights

- North America dominated the Night Vision System Market with the largest revenue share of 40.24% in 2025, supported by high adoption of advanced driver assistance systems, strong penetration of premium and luxury vehicles, and rapid integration of automotive safety technologies

- The passenger vehicle segment led the market with a 70% share in 2025, driven by high consumer demand for advanced safety and comfort features in mid-range and premium cars

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 13.8% from 2026 to 2033, fueled by rapid automotive production growth, increasing adoption of premium vehicles, and rising focus on road safety technologies

- Head-up display are the fastest-growing display type, projected to register a CAGR of 15% from 2026 to 2033, supported by rising demand for augmented driving assistance and minimal driver distraction. Integration of night vision outputs into windshield-projected displays enhances safety and situational awareness

- The passive NVS segment dominated the system category with a 62% revenue share in 2025, led by its reliance on ambient infrared radiation and lower energy consumption

- NIR (Near Infrared) accounted for 58% of the market in 2025, preferred by its cost efficiency, higher image resolution in low-light driving conditions, and strong integration in advanced driver assistance systems

- The active NVS segment is the fastest-growing system category, with a CAGR of 14% from 2026 to 2033, driven by superior illumination capability using infrared light sources for enhanced object detection

Market Size & Forecast

- Global Market Value (2025): USD 4.90 Billion

- Expected Market Value (2033): USD 13.08 Billion

- Forecast CAGR (2026–2033): 13.06%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Night Vision System Market Segmentation

|

Attributes |

Night Vision System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· AISIN SEIKI Co. Ltd. (Japan) · Valeo (France) · Veoneer Inc. (Sweden) · OMRON Corporation (Japan) · Magna International Inc. (Canada) · DENSO CORPORATION (Japan) · ZF Friedrichshafen AG (Germany) · Aptiv (Ireland) · Robert Bosch GmbH (Germany) · Continental AG (Germany) · Autoliv Inc. (Sweden) · Visteon Corporation (U.S.) · ATN Corp. (U.S.) · FLIR Systems, Inc. (U.S.) · SATIR (Denmark) · BAE Systems (U.K.) · Bharat Electronics (India) · Thales (France) · Adorama Camera, Inc (U.S.) |

|

Market Opportunities |

· Expansion of Night Vision Systems in Electric Vehicles · Growing Adoption of Head-Up Display-Based Night Vision Solutions · Increasing Deployment of Thermal Imaging Systems in Commercial Vehicles |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Night Vision System Market Trends

Trend: Integration of Night Vision Systems with ADAS and Autonomous Driving Platforms

Automotive manufacturers are increasingly integrating night vision systems with advanced driver assistance systems (ADAS) and autonomous driving technologies to improve pedestrian detection, obstacle recognition, and overall road safety in low-light conditions. The combination of thermal imaging, infrared sensors, and AI-based object classification is enhancing real-time situational awareness for drivers. Premium vehicle manufacturers are introducing night vision capabilities as part of broader intelligent safety suites, accelerating technology adoption across luxury and electric vehicles. Increasing investments in autonomous mobility solutions are further strengthening the role of night vision technologies in next-generation vehicles.

Companies such as Mercedes-Benz and BMW Group have integrated night vision systems with pedestrian detection functions in several premium models, supporting the growing convergence of thermal imaging and ADAS technologies.

Night Vision System Market Dynamics

Key Market Driver: Rising Demand for Advanced Vehicle Safety and Driver Assistance Technologies

Growing concerns regarding road safety and increasing demand for intelligent driver assistance technologies are significantly driving the adoption of night vision systems. According to the World Health Organization, road traffic accidents cause approximately 1.19 million deaths annually worldwide, encouraging governments and automakers to strengthen vehicle safety features. Night vision systems help improve visibility during darkness, fog, and adverse weather conditions, reducing the risk of collisions involving pedestrians and animals. Increasing penetration of ADAS-equipped vehicles and stricter safety regulations are further supporting market expansion.

Major companies such as Continental AG, DENSO CORPORATION, and Robert Bosch GmbH are continuously developing advanced imaging and sensor technologies to enhance vehicle safety and strengthen their presence in the global market.

Key Restraint/Challenge: High Cost of Infrared Sensors and System Integration

A major challenge in the Night Vision System market is the high cost associated with infrared cameras, thermal sensors, image processing units, and system integration. Advanced thermal imaging modules and specialized sensors increase overall vehicle production costs, limiting adoption primarily to premium and luxury vehicle segments. Complex calibration requirements and the need for seamless integration with ADAS platforms further increase development expenses for manufacturers. These factors restrict widespread penetration across mass-market vehicles and emerging economies.

For instance, night vision technologies offered by companies such as Valeo and Veoneer Inc. are mainly deployed in premium vehicle platforms due to the relatively high costs associated with thermal imaging components and advanced electronic architectures.

Key Market Opportunity: Growing Adoption of Head-Up Display-Based Night Vision Solutions

Increasing deployment of head-up displays (HUDs) in premium and electric vehicles is creating significant opportunities for the Night Vision System market. Integration of night vision imagery directly onto the windshield enables drivers to receive real-time alerts while maintaining focus on the road, enhancing driving safety and convenience. Advancements in augmented reality displays and digital cockpit technologies are improving the effectiveness and commercial viability of HUD-based night vision solutions. Rising investments in intelligent vehicle interfaces are expected to further accelerate adoption across next-generation vehicles.

Companies such as Hyundai Mobis and Panasonic Automotive Systems are expanding their augmented reality head-up display technologies, supporting the integration of advanced night vision information into future connected and autonomous vehicle platforms.

Night Vision System Market Scope

The night vision system market is segmented on the basis of technology, component, system, vehicle type, display, frequency range, and sale channel.

- By Technology

On the basis of technology, the Night Vision System Market is segmented into FIR (Far Infrared) and NIR (Near Infrared). The NIR segment dominated the market with the largest share of 58% in 2025, driven by its cost efficiency, higher image resolution in low-light driving conditions, and strong integration in advanced driver assistance systems. It is widely adopted in premium and mid-range vehicles due to its ability to enhance short to mid-range object detection. Strong compatibility with existing automotive camera systems further reinforces its leading position. Continuous OEM adoption across passenger vehicles sustains its dominance.

The FIR segment is projected to register the fastest growth at a CAGR of 12.5% from 2026 to 2033, driven by superior long-range detection capabilities in complete darkness and adverse weather conditions. Increasing demand for enhanced pedestrian and animal detection in autonomous and semi-autonomous vehicles is accelerating adoption. Advancements in thermal imaging sensors and cost optimization of infrared components are improving commercial viability. Rising safety regulations across major automotive markets are further supporting expansion.

- By Component

On the basis of component, the Night Vision System Market is segmented into controlling unit, display unit, and sensor. The sensor segment dominated the market with a share of 40% in 2025, driven by its critical role in capturing infrared signals and enabling real-time object detection. Increasing deployment of high-sensitivity CMOS and thermal sensors in modern vehicles strengthens demand. Integration with ADAS platforms enhances system performance and reliability. Continuous innovation in compact sensor design further reinforces market leadership.

The display unit segment is projected to register the fastest growth at a CAGR of 13% from 2026 to 2033, driven by rising adoption of advanced visualization systems in instrument clusters and head-up displays. Growing focus on driver-centric interfaces and real-time situational awareness is boosting demand. Automotive manufacturers are increasingly integrating high-resolution displays for improved night-time visibility. Expansion of digital cockpit systems further accelerates segment growth.

- By System

On the basis of system, the Night Vision System Market is segmented into active NVS and passive NVS. The passive NVS segment dominated the market with a share of 62% in 2025, driven by its reliance on ambient infrared radiation and lower energy consumption. It is widely preferred in passenger vehicles due to its cost efficiency and simpler integration architecture. Strong compatibility with ADAS and camera-based safety systems enhances adoption. Large-scale deployment across OEM platforms supports continued dominance.

The active NVS segment is projected to register the fastest growth at a CAGR of 14% from 2026 to 2033, driven by superior illumination capability using infrared light sources for enhanced object detection. Increasing demand for high-performance night driving assistance in luxury and autonomous vehicles is fueling adoption. Technological advancements in infrared emitters and system miniaturization are improving efficiency. Rising emphasis on advanced safety systems is further accelerating market penetration.

- By Vehicle Type

On the basis of vehicle type, the Night Vision System Market is segmented into passenger vehicle and commercial vehicle. The passenger vehicle segment dominated the market with a share of 70% in 2025, driven by high consumer demand for advanced safety and comfort features in mid-range and premium cars. Increasing integration of ADAS technologies in personal mobility solutions strengthens adoption. Rising urbanization and road safety awareness further support growth. Strong OEM penetration across luxury vehicle models reinforces market leadership.

The commercial vehicle segment is projected to register the fastest growth at a CAGR of 11.5% from 2026 to 2033, driven by increasing demand for fleet safety management and accident prevention systems. Adoption of night vision technologies in logistics and long-haul transportation is improving driver visibility and operational safety. Regulatory focus on reducing road accidents is encouraging deployment across commercial fleets. Expansion of e-commerce logistics networks further accelerates segment growth.

- By Display

On the basis of display, the Night Vision System Market is segmented into head-up display, instrument cluster, and navigation display. The instrument cluster segment dominated the market with a share of 48% in 2025, driven by its direct integration with vehicle dashboards and real-time driving data visualization. Increasing adoption of digital clusters in modern vehicles enhances night vision system output clarity. Strong OEM preference for centralized driver information systems supports demand. Continuous upgrades in digital cockpit architecture reinforce dominance.

The head-up display segment is projected to register the fastest growth at a CAGR of 15% from 2026 to 2033, driven by rising demand for augmented driving assistance and minimal driver distraction. Integration of night vision outputs into windshield-projected displays enhances safety and situational awareness. Rapid adoption in premium and electric vehicles is supporting expansion. Advancements in projection technology and brightness optimization further accelerate growth.

- By Frequency Range

On the basis of frequency range, the Night Vision System Market is segmented into low, medium, and high. The medium frequency segment dominated the market with a share of 50% in 2025, driven by its balanced performance in resolution, detection range, and cost efficiency. It is widely adopted in passenger vehicles for standard night vision applications. Strong compatibility with existing automotive imaging systems enhances integration efficiency. Broad OEM deployment across global markets supports dominance.

The high frequency segment is projected to register the fastest growth at a CAGR of 14% from 2026 to 2033, driven by superior imaging precision and enhanced long-range detection capabilities. Increasing demand for advanced autonomous driving features is accelerating adoption. Improvements in high-frequency sensor technology are enhancing image clarity in extreme conditions. Rising focus on next-generation safety systems further supports segment expansion.

- By Sales Channel

On the basis of sales channel, the Night Vision System Market is segmented into original equipment manufacturers (OEMs) and distributors. The OEM segment dominated the market with a share of 78% in 2025, driven by direct integration of night vision systems during vehicle manufacturing. Increasing collaboration between automotive manufacturers and technology providers enhances system standardization. Strong demand for factory-fitted advanced safety systems supports adoption. Large-scale deployment in premium vehicle segments reinforces dominance.

The distributors segment is projected to register the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by rising aftermarket installation demand and retrofit solutions for existing vehicles. Increasing consumer interest in upgrading vehicle safety features is supporting sales growth. Expansion of automotive accessory distribution networks is improving product accessibility. Growing awareness of night driving safety enhancements further accelerates segment adoption.

Night Vision System Market Regional Analysis

North America dominated the night vision system market and accounted for the largest revenue share of 40.24% in 2025, driven by high adoption of advanced driver assistance systems, strong penetration of premium and luxury vehicles, and rapid integration of automotive safety technologies. The region benefits from a mature automotive ecosystem, strong presence of leading OEMs, and early adoption of infrared and thermal imaging-based safety solutions. Increasing consumer preference for enhanced night driving safety and regulatory emphasis on vehicle safety standards are further strengthening market growth. In addition, continuous investments in autonomous driving technologies and connected vehicle infrastructure continue to reinforce North America’s leadership position in the global market.

U.S. Night Vision System Market Insight

The U.S. Night Vision System market is experiencing strong growth driven by rapid deployment of ADAS features, increasing demand for luxury vehicles equipped with advanced safety systems, and rising focus on reducing nighttime road accidents. Automakers are heavily investing in infrared-based imaging and AI-enabled detection systems to improve pedestrian and obstacle recognition. The country’s strong semiconductor ecosystem and advanced automotive R&D capabilities are enabling continuous innovation in night vision technologies. In addition, growing adoption of electric and autonomous vehicles is further accelerating demand for integrated night vision systems across the U.S. automotive sector.

Canada Night Vision System Market Insight

The Canada Night Vision System market is witnessing steady growth supported by rising vehicle safety awareness, increasing adoption of premium SUVs, and growing integration of advanced driver assistance technologies. Harsh weather conditions and low visibility driving environments are encouraging the use of night vision systems for improved road safety. Automotive manufacturers are gradually incorporating infrared-based systems in high-end vehicle models to enhance driver confidence. In addition, expanding automotive import penetration and growing consumer preference for safety-enhanced vehicles are further contributing to market growth in Canada.

Europe Night Vision System Market Insight

The Europe Night Vision System market is expanding steadily due to stringent vehicle safety regulations, strong adoption of automotive safety innovations, and increasing demand for premium and electric vehicles. The region benefits from a highly advanced automotive manufacturing base and strong focus on reducing road fatalities through intelligent safety systems. Automotive OEMs across the region are actively integrating infrared and thermal imaging technologies into luxury vehicle platforms. In addition, rising investments in autonomous driving and connected mobility solutions are further supporting market expansion across Europe.

U.K. Night Vision System Market Insight

The U.K. Night Vision System market is growing steadily, driven by increasing adoption of luxury vehicles, rising focus on road safety enhancements, and strong penetration of advanced automotive electronics. Automakers are integrating night vision technologies into premium models to improve driver awareness in low-light conditions. The country’s well developed automotive aftermarket and growing demand for safety upgrades are further supporting market expansion. In addition, rising investments in intelligent mobility solutions and autonomous driving technologies are strengthening adoption in the U.K.

Germany Night Vision System Market Insight

The Germany Night Vision System market is expanding due to strong presence of luxury automotive manufacturers, high adoption of advanced vehicle safety systems, and continuous innovation in automotive electronics. Leading OEMs are integrating infrared-based night vision technologies into high-end vehicle platforms to enhance driver assistance capabilities. The country’s strong engineering base and focus on automotive safety innovation are driving continuous product development. In addition, increasing investment in autonomous driving and premium vehicle production is further accelerating market growth in Germany.

Asia-Pacific Night Vision System Market Insight

The Asia-Pacific Night Vision System market is expected to register the fastest growth with a CAGR of 13.8% from 2026 to 2033, driven by rapid automotive production growth, increasing adoption of premium vehicles, and rising focus on road safety technologies. Expanding middle-class population and growing demand for advanced vehicle safety features are significantly boosting market penetration. Countries such as China, India, Japan, and South Korea are witnessing strong adoption of ADAS-integrated vehicles with night vision capabilities. In addition, increasing investments in smart mobility and autonomous vehicle development are further accelerating regional market expansion.

Japan Night Vision System Market Insight

The Japan Night Vision System market is witnessing steady growth supported by high automotive technology adoption, strong presence of leading OEMs, and increasing integration of advanced safety systems in passenger vehicles. Automakers are focusing on enhancing driver assistance features through infrared and thermal imaging technologies. The country’s strong robotics and electronics industry is enabling continuous innovation in sensor-based safety systems. In addition, rising demand for premium vehicles and autonomous driving technologies is further strengthening market growth in Japan.

China Night Vision System Market Insight

The China Night Vision System market is growing rapidly due to strong automotive production base, increasing adoption of luxury vehicles, and rapid expansion of ADAS technologies. Domestic and international OEMs are integrating advanced night vision systems to enhance vehicle safety and competitiveness. The country’s strong semiconductor manufacturing capabilities and AI-driven automotive innovation are supporting large-scale deployment. In addition, rising government focus on road safety improvements and smart vehicle technologies is further driving market growth in China.

Night Vision System Market Share

The night vision system industry is primarily led by well-established companies, including:

- AISIN SEIKI Co. Ltd. (Japan)

- Valeo (France)

- Veoneer Inc. (Sweden)

- OMRON Corporation (Japan)

- Magna International Inc. (Canada)

- DENSO CORPORATION (Japan)

- ZF Friedrichshafen AG (Germany)

- Aptiv (Ireland)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Autoliv Inc. (Sweden)

- Visteon Corporation (U.S.)

- ATN Corp. (U.S.)

- FLIR Systems, Inc. (U.S.)

- SATIR (Denmark)

- BAE Systems (U.K.)

- Bharat Electronics (India)

- Thales (France)

- Adorama Camera, Inc (U.S.)

Latest Developments in Night Vision System Market

- In June 2026, Teledyne FLIR Defense announced the expansion of its next-generation thermal imaging night vision portfolio with upgraded dual-sensor systems designed for enhanced long-range target detection and improved performance in extreme weather conditions. This development strengthens its position in advanced infrared imaging technologies and supports growing demand for high-precision surveillance and reconnaissance systems. The upgrade is expected to accelerate adoption across defense modernization programs and border security applications globally

- In May 2025, Elbit Systems introduced its Gen-4+ Night Vision Monocular featuring 640x480 resolution and a 60Hz refresh rate, significantly improving image clarity, motion smoothness, and target detection accuracy in low-light environments. This advancement strengthens the competitive positioning of high-resolution night vision devices, driving greater adoption in both defense modernization programs and advanced surveillance applications. The enhancement in sensor precision and real-time responsiveness is expected to accelerate demand for next-generation monocular systems across military end users

- In May 2025, BAE Systems secured a major contract from the U.S. Army to supply over 150,000 Enhanced Night Vision Goggles (ENVG III), reflecting strong institutional demand for advanced soldier vision systems. This large-scale procurement reinforces the shift toward integrated night vision and augmented reality-enabled battlefield awareness solutions. The contract also highlights growing investment in soldier modernization programs, which is expected to significantly expand production volumes and strengthen long-term market growth in defense applications

- In March 2025, Raytheon Technologies and Elbit Systems entered a strategic partnership to co-develop next-generation night vision systems for military use, combining advanced sensor technologies with proven imaging expertise. This collaboration is expected to accelerate innovation in multi-spectral imaging systems, enhancing operational performance in complex combat environments. The partnership also strengthens global supply chain capabilities for defense-grade night vision solutions, supporting wider adoption across allied defense forces

- In January 2024, L3Harris Technologies launched the AN/AVS-3 Helmet Mounted Display System (HMDS) featuring integrated thermal and visible light imaging capabilities, significantly improving situational awareness in low-visibility conditions. This development enhances soldier performance by combining multiple imaging modes into a single wearable system, reducing reliance on separate devices. The innovation is expected to drive increased adoption of integrated helmet-mounted night vision systems in modern military operations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Night Vision System Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Night Vision System Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Night Vision System Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.