Global Non 24 Hour Sleep Wake Disorder Drug Market

Market Size in USD Billion

USD

1.50 Billion

USD

3.20 Billion

2024

2032

USD

1.50 Billion

USD

3.20 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.50 Billion | |

| USD 3.20 Billion | |

| % | |

|

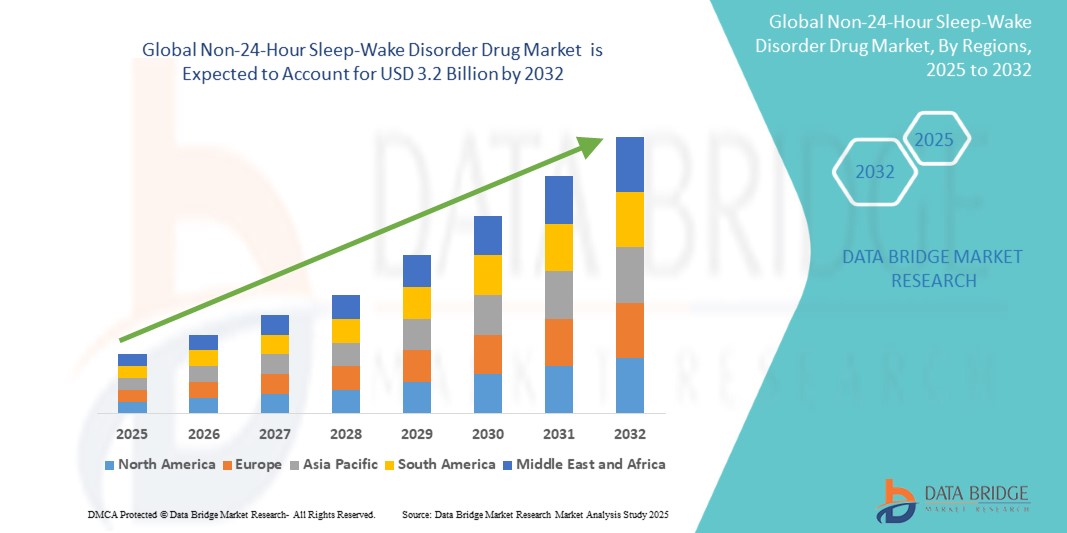

Non-24-Hour Sleep-Wake Disorder Drug Market Size

- The Global Non-24-Hour Sleep-Wake Disorder Drug Market size was valued at USD 1.5 billion in 2024 and is expected to reach USD 3.2 billion by 2032, at a CAGR of 9.2% during the forecast period

- This growth is driven by factors such as rising awareness of circadian rhythm disorders, increasing diagnosis among visually impaired individuals, and the growing availability of melatonin-based prescription therapies

Non-24-Hour Sleep-Wake Disorder Drug Market Analysis

- Non-24-Hour Sleep-Wake Disorder (Non-24) is primarily seen in totally blind individuals with no light perception, disrupting their circadian rhythms. The market is growing due to increased healthcare focus on sleep health, FDA approvals of targeted therapies, and patient advocacy efforts improving diagnosis rates

- The demand for these microscopes is significantly driven by the increasing prevalence of age-related eye conditions and advancements in surgical techniques

- North America is expected to dominate the Non-24-Hour Sleep-Wake Disorder Drugs market due to strong clinical infrastructure and availability of drugs like tasimelteon, while developing markets are expanding awareness through neurology and sleep medicine networks

- Asia-Pacific is expected to be the fastest growing region in the Non-24-Hour Sleep-Wake Disorder Drug market during the forecast period due to increasing awareness of sleep disorders and advancements in healthcare infrastructure.

- Melatonin agonists are expected to dominate due to their targeted mechanism of action and minimal side effect profiles

Report Scope and Non-24-Hour Sleep-Wake Disorder Drug Market Segmentation

|

Attributes |

Non-24-Hour Sleep-Wake Disorder Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Non-24-Hour Sleep-Wake Disorder Drug Market Trends

“Integration of Chronotherapy and Personalized Treatment Approaches”

- One prominent trend in the Global Non-24-Hour Sleep-Wake Disorder Drug Market is the growing focus on personalized chronotherapy, which aligns drug administration with an individual’s biological sleep-wake cycle.

- This approach aims to enhance treatment effectiveness by delivering medications at biologically optimal times, thereby improving sleep regulation and minimizing side effects

- For instance, in 2023, several studies and clinical trials explored circadian-timed melatonin receptor agonists, such as tasimelteon, showing improved outcomes when administered according to individual circadian profiles, paving the way for more precise and targeted therapies.

- These advancements are reshaping sleep disorder management by offering more patient-centric solutions, increasing therapeutic efficacy, and driving innovation in drug development for circadian rhythm disorders

Non-24-Hour Sleep-Wake Disorder Drug Market Dynamics

Driver

“Rising Awareness and Diagnosis of Circadian Rhythm Disorders”

- Growing recognition of circadian rhythm disorders such as Non-24 among both physicians and patients is driving market demand. Health systems are incorporating sleep health screenings and referrals to specialists more proactively

- Growing global awareness of sleep health has led to increased recognition and diagnosis of circadian rhythm disorders, including Non-24-Hour Sleep-Wake Disorder, particularly among blind individuals and those with irregular sleep patterns.

- As more individuals undergo sleep assessments and consult specialists for persistent sleep-wake disruptions, the demand for effective pharmacological treatments continues to rise, supporting market growth and fostering earlier intervention

For instance,

- in 2024, the U.S. National Institutes of Health expanded its sleep disorder research funding, accelerating the availability of diagnostic tools and treatment pathways

- As a result of increasing awareness and improved diagnosis of circadian rhythm disorders—particularly among individuals with vision impairment—there is a significant rise in the demand for Non-24-Hour Sleep-Wake Disorder drugs

Opportunity

“Expansion of Digital Health Tools and Online Pharmacies”

- Patients are increasingly accessing support through mobile health apps and online pharmacies, improving medication adherence and access to information about Non-24

- Digital health tools such as mobile sleep-tracking apps and telemedicine platforms are increasingly being used to monitor sleep patterns and identify symptoms of circadian rhythm disorders, facilitating early diagnosis and timely medical consultation.

- Additionally, the growth of online pharmacies allows patients—especially those with mobility challenges or visual impairments—to easily access Non-24-Hour Sleep-Wake Disorder drugs, improving treatment adherence and expanding market reach.

For instance,

- For example, in 2025, partnerships between sleep clinics and digital platforms in the U.S. and Germany enabled streamlined prescription renewals for melatonin-based drugs

- The integration of digital health tools and online pharmacy services can lead to improved patient outcomes, better treatment adherence, and enhanced quality of life. By leveraging remote monitoring and convenient drug access, healthcare providers can identify at-risk patients earlier and initiate timely interventions to manage Non-24-Hour Sleep-Wake Disorder effectively.

Restraint/Challenge

“High Cost and Limited Awareness in Emerging Economies”

- Despite approval in multiple countries, high cost of therapy and lack of awareness among general practitioners remain major challenges, especially in low- and middle-income markets

- The high cost of Non-24-Hour Sleep-Wake Disorder drugs, combined with limited healthcare infrastructure, can be a significant barrier in emerging economies, where treatment options may be unaffordable for many patients.

- This financial challenge, along with a lack of awareness about circadian rhythm disorders, often results in delayed diagnoses and lower adoption of treatment, limiting the market potential in these regions.

For instance,

- A 2023 study published in the Journal of Sleep Research reported that over 60% of neurologists in Southeast Asia were unaware of Non-24-specific treatment protocols, limiting patient referrals

- Consequently, these limitations can lead to disparities in access to effective treatments and early diagnosis, ultimately hindering the overall growth of the Non-24-Hour Sleep-Wake Disorder drug market in emerging economies

Non-24-Hour Sleep-Wake Disorder Drug Market Scope

The market is segmented on the basis drug type, route of administration, end user, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Drug Type |

|

|

By Route of Administration |

|

|

By End User |

|

|

By Distribution Channel

|

|

In 2025, the Melatonin Agonists is projected to dominate the market with a largest share in drug type segment

The Melatonin Agonists segment is expected to dominate the Non-24-Hour Sleep-Wake Disorder Drug market with the largest share of 56.22% in 2025 due to its proven efficacy in regulating circadian rhythms and treating sleep-wake cycle disturbances. The growing prevalence of circadian rhythm disorders, particularly among blind individuals, along with the increasing demand for targeted, precision-based therapies, supports this segment's leading position. Additionally, heightened awareness, ongoing clinical research, and favorable regulatory approvals contribute to the strong market outlook for melatonin receptor agonists.

The oral is expected to account for the largest share during the forecast period in route of administration market

In 2025, the oral segment is expected to dominate the market with the largest market share of 51.31% due to the convenience, patient compliance, and widespread availability of oral formulations. Oral drugs, such as melatonin receptor agonists, are preferred for long-term management of circadian rhythm disorders due to ease of administration and consistent therapeutic outcomes. The growing patient population, especially among individuals with limited access to specialized care, further drives the demand for oral treatments, reinforcing this segment's market leadership.

Non-24-Hour Sleep-Wake Disorder Drug Market Regional Analysis

“North America Holds the Largest Share in the Non-24-Hour Sleep-Wake Disorder Drug Market”

- North America dominates the Non-24-Hour Sleep-Wake Disorder Drug market, driven by its advanced healthcare infrastructure, high awareness of sleep disorders, and strong presence of leading pharmaceutical companies.

- The U.S. holds a significant share due to growing recognition of circadian rhythm disorders among both blind and sighted populations, increasing diagnosis rates, and greater access to specialized sleep medicine.

- Well-established reimbursement frameworks and substantial investment in clinical research and development by key industry players further support market growth.

- Additionally, the rising use of digital health platforms and telemedicine in sleep disorder management is accelerating treatment accessibility and fueling market expansion across the region

“Asia-Pacific is Projected to Register the Highest CAGR in the Non-24-Hour Sleep-Wake Disorder Drug Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the Non-24-Hour Sleep-Wake Disorder Drug market, driven by rapid improvements in healthcare infrastructure, increasing public awareness of sleep and circadian rhythm disorders, and rising access to diagnostic services

- Countries such as China, India, and Japan are emerging as key markets due to their large populations and growing recognition of sleep health, particularly among visually impaired individuals who are at higher risk for Non-24-Hour Sleep-Wake Disorder.

- Japan, with its progressive healthcare system and emphasis on neurological and sleep research, plays a crucial role in advancing treatment adoption across the region.

- Meanwhile, China and India are experiencing increased investments from both government and private sectors to expand access to sleep medicine, promote awareness campaigns, and improve the availability of specialized treatments, contributing to strong market expansion

Non-24-Hour Sleep-Wake Disorder Drug Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Vanda Pharmaceuticals (United States)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceuticals (Israel)

- Glenmark Pharmaceuticals (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Torrent Pharmaceuticals Ltd. (India)

- Apotex Inc. (Canada)

- Cipla Ltd. (India)

Latest Developments in Global Non-24-Hour Sleep-Wake Disorder Drug Market

- In January 2025, Vanda Pharmaceuticals launched a direct-to-patient education portal to improve awareness and facilitate online consultations for Non-24.

- In February 2025, Takeda announced clinical trial results for a novel melatonin receptor agonist showing improved sleep parameters in Non-24 patients.

- In March 2025, Glenmark Pharmaceuticals entered into a licensing agreement to distribute Non-24 therapies in Latin America.

- In April 2025, Apotex initiated a clinical trial for a generic formulation of tasimelteon to expand access in emerging markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.